Global T Cell Lymphoma Treatment Market

Market Size in USD Billion

CAGR :

%

USD

1.85 Billion

USD

3.69 Billion

2025

2033

USD

1.85 Billion

USD

3.69 Billion

2025

2033

| 2026 –2033 | |

| USD 1.85 Billion | |

| USD 3.69 Billion | |

| % | |

|

Thymus (T)-Cell Lymphoma Treatment Market Size

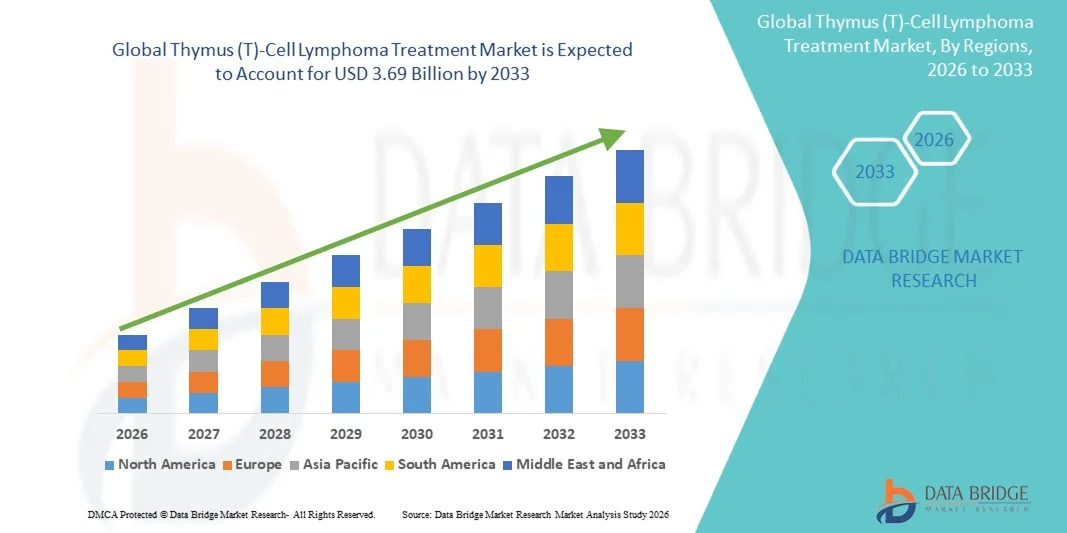

- The global thymus (T)-cell lymphoma treatment market size was valued at USD 1.85 billion in 2025 and is expected to reach USD 3.69 billion by 2033, at a CAGR of 9.02% during the forecast period

- The market growth is largely fueled by the increasing incidence of rare hematologic malignancies and continuous advancements in targeted therapies, immunotherapies, and biologics, leading to improved diagnosis and treatment outcomes across healthcare systems

- Furthermore, rising demand for personalized medicine, growing awareness among patients and clinicians, and enhanced access to advanced oncology care are establishing T-cell lymphoma treatments as a critical component of modern cancer management. These converging factors are accelerating the adoption of innovative therapies, thereby significantly boosting the industry's growth

Thymus (T)-Cell Lymphoma Treatment Market Analysis

- Thymus (T)-cell lymphoma treatment, encompassing a range of therapeutic approaches such as chemotherapy, radiation therapy, and advanced medications, plays a crucial role in managing aggressive and rare subtypes of non-Hodgkin lymphoma, with growing emphasis on early diagnosis and personalized treatment strategies

- The escalating demand for thymus (T)-cell lymphoma treatment is primarily fueled by the rising incidence of hematologic malignancies, increasing awareness regarding early detection, and continuous advancements in diagnostic technologies and targeted therapies that enhance treatment effectiveness and patient survival rates

- North America dominated the thymus (T)-cell lymphoma treatment market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, strong presence of leading pharmaceutical companies, and high adoption of innovative diagnostic and treatment solutions, with the U.S. witnessing significant growth driven by increasing clinical research and access to novel therapies

- Asia-Pacific is expected to be the fastest growing region in the thymus (T)-cell lymphoma treatment market during the forecast period due to improving healthcare infrastructure, rising patient awareness, and increasing investments in oncology care and diagnostic capabilities

- Chemotherapy segment dominated the thymus (T)-cell lymphoma treatment market with a market share of 42.3% in 2025, driven by its widespread use as a first-line treatment option, established clinical efficacy, and broad applicability across multiple T-cell lymphoma subtypes

Report Scope and Thymus (T)-Cell Lymphoma Treatment Market Segmentation

|

Attributes |

Thymus (T)-Cell Lymphoma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Thymus (T)-Cell Lymphoma Treatment Market Trends

“Advancement in Targeted Therapies and Precision Oncology”

- A significant and accelerating trend in the global thymus (T)-cell lymphoma treatment market is the growing integration of targeted therapies and precision medicine approaches such as monoclonal antibodies, CAR-T cell therapy, and molecular-guided treatments. This evolution is significantly improving treatment specificity and patient outcomes

- For instance, brentuximab vedotin and other targeted agents are increasingly being incorporated into treatment regimens, offering improved efficacy in specific T-cell lymphoma subtypes. Similarly, CAR-T cell therapies are emerging as promising options for relapsed or refractory cases, enhancing survival prospects

- Precision medicine integration in thymus (T)-cell lymphoma treatment enables clinicians to tailor therapies based on genetic and molecular profiling, leading to more effective and less toxic treatment plans. For instance, biomarker-driven approaches help identify patients most likely to benefit from specific therapies and support better clinical decision-making. Furthermore, advanced therapies provide improved disease monitoring and response assessment, allowing timely intervention

- The seamless integration of advanced diagnostics with targeted treatment strategies facilitates a more personalized approach to cancer care. Through coordinated use of imaging, molecular testing, and therapy selection, healthcare providers can optimize treatment pathways and improve overall patient management

- This trend towards more precise, personalized, and innovative treatment solutions is fundamentally reshaping expectations in oncology care. Consequently, companies are increasingly investing in next-generation biologics and cell-based therapies with enhanced efficacy and reduced side effects

- The demand for thymus (T)-cell lymphoma treatment solutions that offer precision, improved safety, and higher efficacy is growing rapidly across healthcare systems, as providers increasingly prioritize advanced oncology care and better patient outcomes

- Increasing collaborations between pharmaceutical companies and research institutions are accelerating drug development pipelines, leading to faster introduction of innovative therapies and expanding treatment options for patients

Thymus (T)-Cell Lymphoma Treatment Market Dynamics

Driver

“Rising Incidence of Hematologic Malignancies and Advancements in Oncology Care”

- The increasing prevalence of T-cell lymphomas and other hematologic cancers, coupled with rapid advancements in oncology research and treatment modalities, is a significant driver for the heightened demand for thymus (T)-cell lymphoma treatment

- For instance, in recent years, several pharmaceutical companies have accelerated clinical trials and approvals of targeted therapies and biologics, aiming to improve treatment outcomes and expand therapeutic options. Such strategies by key companies are expected to drive the thymus (T)-cell lymphoma treatment market growth in the forecast period

- As awareness of rare cancers increases and diagnostic capabilities improve, more patients are being identified and treated at earlier stages, boosting demand for effective therapies. In addition, the availability of novel drugs and combination therapies is enhancing survival rates and quality of life

- Furthermore, the growing investment in healthcare infrastructure and oncology research is supporting the adoption of advanced treatment options, enabling broader access to innovative therapies across developed and emerging markets

- The increasing focus on personalized medicine, improved reimbursement scenarios, and government support for cancer treatment programs are key factors propelling the adoption of thymus (T)-cell lymphoma treatment solutions globally. The expansion of specialty cancer centers and clinical research initiatives further contributes to market growth

- Growing participation in clinical trials and expanded regulatory support for orphan drugs are encouraging innovation and speeding up the availability of new treatment options for rare lymphoma subtypes

- Increasing use of combination therapies integrating chemotherapy, radiation, and targeted drugs is improving overall treatment efficacy and driving higher adoption rates across healthcare providers

Restraint/Challenge

“High Treatment Costs and Limited Accessibility in Emerging Regions”

- Concerns surrounding the high cost of advanced therapies, including biologics and cell-based treatments, pose a significant challenge to broader market penetration. As these treatments require specialized infrastructure and expertise, affordability and accessibility remain key barriers

- For instance, CAR-T cell therapies and targeted biologics often involve substantial treatment costs, limiting their accessibility for patients in low- and middle-income regions and creating disparities in care

- Addressing these cost-related challenges through pricing strategies, insurance coverage expansion, and government support is crucial for improving patient access. Companies are also focusing on developing cost-effective treatment alternatives and expanding clinical trials to broaden availability. In addition, limited awareness and delayed diagnosis in certain regions further hinder timely treatment initiation

- While healthcare systems are gradually improving, disparities in access to advanced diagnostics and therapies continue to restrict market growth, particularly in underdeveloped areas where oncology care infrastructure is still evolving

- Overcoming these challenges through enhanced healthcare investments, improved reimbursement frameworks, and increased awareness initiatives will be vital for sustained market growth and equitable access to thymus (T)-cell lymphoma treatment solutions

- Stringent regulatory requirements and lengthy drug approval timelines can delay the commercialization of innovative therapies, limiting timely access to new treatment options

- Potential side effects and toxicity associated with aggressive treatment regimens may lead to patient reluctance and treatment discontinuation, thereby impacting overall market growth

Thymus (T)-Cell Lymphoma Treatment Market Scope

The market is segmented on the basis of type, treatment, diagnosis, dosage, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the thymus (T)-cell lymphoma treatment market is segmented into peripheral T-cell lymphoma, cutaneous T-cell lymphoma, anaplastic large cell lymphoma, and others. The peripheral T-cell lymphoma segment dominated the market with the largest revenue share in 2025, driven by its higher prevalence and aggressive disease nature requiring intensive multi-line treatment. This subtype often involves complex therapeutic regimens, including chemotherapy and targeted therapies, leading to higher treatment costs and demand. Increasing research focus and clinical trials targeting this subtype are further supporting its dominance. In addition, improved diagnostic techniques are enabling earlier identification and intervention. The growing burden of this subtype across regions also contributes to its leading position. Strong physician awareness and availability of established treatment protocols further reinforce its dominance.

The cutaneous T-cell lymphoma segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing diagnosis rates and rising awareness of skin-related lymphomas. Advancements in dermatology and oncology integration are improving early-stage detection and treatment outcomes. The availability of specialized therapies such as light therapy and topical medications is supporting segment expansion. Patients increasingly prefer less invasive treatment options, which is further driving growth. Ongoing research into targeted therapies for cutaneous variants is also accelerating adoption. Expanding healthcare access in emerging markets is contributing to the rapid growth of this segment.

- By Treatment

On the basis of treatment, the market is segmented into radiation, chemotherapy, light therapy, surgery, medication, and others. The chemotherapy segment dominated the market with the largest revenue share of 42.3% in 2025, owing to its widespread use as the standard first-line therapy for multiple T-cell lymphoma subtypes. Chemotherapy remains a widely accepted and clinically proven treatment option with established protocols. It is frequently used in combination with other therapies, enhancing its effectiveness and demand. The affordability of chemotherapy compared to advanced biologics also supports its dominance, particularly in developing regions. Strong physician familiarity and availability across healthcare settings further contribute to its extensive use. In addition, its applicability across both early and advanced disease stages strengthens its position.

The medication segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of targeted therapies, immunotherapies, and biologics. These advanced treatments offer improved specificity and reduced toxicity compared to conventional chemotherapy. Continuous regulatory approvals and expanding drug pipelines are enhancing availability. Growing emphasis on personalized medicine is encouraging the use of targeted medications. Improved patient outcomes and longer survival rates are further driving demand. Increasing investments in oncology drug development are also accelerating segment growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood cell counts, tissue biopsy, computed tomography (CT) scan, positron emission tomography (PET) scan, magnetic resonance imaging (MRI) scan, and others. The tissue biopsy segment dominated the market with the largest revenue share in 2025, as it remains the gold standard for accurate diagnosis and classification of T-cell lymphoma. Biopsy provides detailed histological and molecular insights necessary for effective treatment planning. It plays a crucial role in differentiating between lymphoma subtypes. Advancements in biopsy techniques are improving diagnostic precision and reliability. Integration with molecular testing further enhances its clinical importance. Strong reliance by clinicians ensures its continued dominance in the market.

The positron emission tomography (PET) scan segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its ability to provide functional imaging for staging and monitoring treatment response. PET scans are increasingly used for evaluating disease progression and therapy effectiveness. The rising demand for non-invasive and highly accurate diagnostic tools is supporting adoption. Technological advancements in imaging systems are improving accessibility and performance. Increased healthcare investments in diagnostic infrastructure are further boosting growth. Growing preference for early and precise disease detection is also contributing to segment expansion.

- By Dosage

On the basis of dosage, the market is segmented into injection, tablet, and others. The injection segment dominated the market with the largest revenue share in 2025, due to the extensive use of injectable formulations in chemotherapy and biologic therapies. Injectable drugs ensure rapid onset of action and controlled dosing, which is critical in cancer treatment. Most hospital-administered therapies rely on injection-based delivery systems. The increasing use of monoclonal antibodies and advanced biologics further strengthens this segment. In addition, clinical preference for supervised drug administration enhances safety and effectiveness. The dominance of hospital-based treatment settings also supports this segment’s growth.

The tablet segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the growing availability of oral targeted therapies. Tablets offer convenience and improved patient compliance, especially for long-term treatment regimens. Patients prefer oral medications as they reduce the need for frequent hospital visits. Advancements in pharmaceutical formulations are enabling effective oral drug delivery. Increasing adoption of outpatient care models is also supporting growth. The shift toward patient-centric treatment approaches is further accelerating demand.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, topical, and others. The parenteral segment dominated the market with the largest revenue share in 2025, driven by the high use of intravenous and injectable therapies in oncology. Parenteral administration ensures maximum bioavailability and rapid therapeutic effects. Most chemotherapy drugs and biologics are administered through this route, supporting its dominance. Hospital-based care settings further reinforce its widespread use. The ability to deliver precise dosages under medical supervision enhances treatment outcomes. Increasing use of advanced injectable therapies also contributes to segment growth.

The oral segment is expected to witness the fastest growth rate from 2026 to 2033, supported by increasing development of oral targeted therapies. Oral administration offers convenience and flexibility for patients undergoing long-term treatment. It reduces dependency on hospital infrastructure and lowers overall treatment costs. Growing patient preference for non-invasive treatment options is driving adoption. Advances in drug development are expanding the range of oral therapies available. The focus on improving patient quality of life is further boosting segment growth.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The hospital segment dominated the market with the largest revenue share in 2025, owing to the availability of advanced oncology infrastructure and skilled healthcare professionals. Hospitals serve as primary centers for diagnosis, treatment, and management of complex lymphoma cases. The presence of multidisciplinary teams ensures comprehensive patient care. Access to advanced diagnostic and therapeutic technologies supports better treatment outcomes. Increasing patient admissions for cancer treatment further strengthen this segment. Strong reimbursement frameworks in hospitals also contribute to dominance.

The clinic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising shift toward outpatient care and specialized oncology clinics. Clinics offer cost-effective and accessible treatment options for patients. Growing establishment of dedicated cancer care centers is supporting segment expansion. Patients prefer clinics for follow-up treatments and routine monitoring. Shorter waiting times and personalized care enhance patient experience. Increasing healthcare accessibility in emerging regions is also contributing to growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share in 2025, driven by the high volume of oncology treatments administered in hospitals. Hospital pharmacies ensure proper storage and handling of specialized and high-cost medications. They also facilitate direct coordination with healthcare providers for accurate dispensing. The increasing use of injectable and biologic drugs supports this segment’s dominance. In addition, strict regulatory compliance ensures safe distribution of cancer therapies. Growing hospital-based treatment rates further strengthen this segment.

The online pharmacy segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing digitalization in healthcare and rising adoption of e-pharmacy platforms. Online pharmacies provide convenience and home delivery options for patients. Growing internet penetration and smartphone usage are supporting segment expansion. Competitive pricing and discounts are attracting more consumers. Improved regulatory frameworks are enhancing trust in online platforms. The shift toward digital healthcare solutions is accelerating adoption globally.

Thymus (T)-Cell Lymphoma Treatment Market Regional Analysis

- North America dominated the thymus (T)-cell lymphoma treatment market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, strong presence of leading pharmaceutical companies, and high adoption of innovative diagnostic and treatment solutions

- Patients and healthcare providers in the region highly value the availability of advanced therapies, improved diagnostic technologies, and integrated cancer care systems that enhance treatment outcomes and survival rates

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare expenditure, a strong presence of leading pharmaceutical companies, and increasing focus on research and clinical trials, establishing thymus (T)-cell lymphoma treatment as a critical component of modern oncology care across healthcare settings

U.S. Thymus (T)-Cell Lymphoma Treatment Market Insight

The U.S. thymus (T)-cell lymphoma treatment market captured the largest revenue share within North America in 2025, fueled by the strong presence of advanced healthcare infrastructure and rapid adoption of innovative oncology therapies. Patients and healthcare providers are increasingly prioritizing early diagnosis and access to targeted treatments and biologics to improve survival outcomes. The growing emphasis on precision medicine, combined with robust clinical research activities and high healthcare spending, further propels the market. Moreover, the increasing number of FDA approvals and ongoing clinical trials for novel therapies is significantly contributing to the market's expansion.

Europe Thymus (T)-Cell Lymphoma Treatment Market Insight

The Europe thymus (T)-cell lymphoma treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong healthcare systems and increasing focus on cancer management. The rise in cancer prevalence, coupled with advancements in diagnostic and treatment technologies, is fostering the adoption of advanced therapies. European patients are also benefiting from favorable reimbursement policies and access to innovative treatments. The region is experiencing significant growth across hospital and specialty care settings, with advanced lymphoma therapies being incorporated into both standard treatment protocols and clinical research programs.

U.K. Thymus (T)-Cell Lymphoma Treatment Market Insight

The U.K. thymus (T)-cell lymphoma treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of rare cancers and improved access to specialized oncology care. In addition, government support and national health programs are encouraging early diagnosis and timely treatment. The U.K.’s strong clinical research ecosystem, alongside its well-established healthcare infrastructure, is expected to continue to stimulate market growth. The adoption of advanced diagnostic techniques and targeted therapies is further supporting improved patient outcomes.

Germany Thymus (T)-Cell Lymphoma Treatment Market Insight

The Germany thymus (T)-cell lymphoma treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by rising demand for advanced cancer therapies and increasing focus on precision medicine. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and research, promotes the adoption of novel treatment approaches. The integration of advanced diagnostic tools with targeted therapies is also becoming increasingly prevalent. In addition, strong regulatory support and investment in oncology research align with the country’s focus on high-quality patient care.

Asia-Pacific Thymus (T)-Cell Lymphoma Treatment Market Insight

The Asia-Pacific thymus (T)-cell lymphoma treatment market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by improving healthcare infrastructure, rising patient population, and increasing awareness of cancer diagnosis and treatment. The region's growing focus on expanding access to oncology care, supported by government initiatives, is driving the adoption of advanced therapies. Furthermore, as Asia-Pacific emerges as a key region for clinical trials and pharmaceutical manufacturing, the availability and affordability of treatments are improving, expanding access to a wider patient base.

Japan Thymus (T)-Cell Lymphoma Treatment Market Insight

The Japan thymus (T)-cell lymphoma treatment market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong focus on oncology innovation. The Japanese market places a significant emphasis on early diagnosis and effective treatment, driving the adoption of advanced therapies. The integration of innovative diagnostic technologies with targeted treatments is fueling growth. Moreover, Japan's increasing investment in cancer research is expected to spur demand for effective and personalized treatment solutions in both hospital and specialized care settings.

India Thymus (T)-Cell Lymphoma Treatment Market Insight

The India thymus (T)-cell lymphoma treatment market accounted for a significant market share in Asia Pacific in 2025, attributed to the country's growing healthcare sector, rising cancer burden, and improving access to medical services. India stands as a rapidly growing market for oncology treatments, with increasing adoption across hospitals and specialty clinics. The push towards healthcare infrastructure development and government initiatives for cancer care, alongside the availability of cost-effective treatment options, are key factors propelling the market in India

Thymus (T)-Cell Lymphoma Treatment Market Share

The Thymus (T)-Cell Lymphoma Treatment industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Gilead Sciences, Inc. (U.S.)

- Incyte Corporation (U.S.)

- Seagen Inc. (U.S.)

- Kyowa Kirin Co., Ltd. (Japan)

- Genmab A/S (Denmark)

- Eisai Co., Ltd. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Autolus Therapeutics plc (U.K.)

- Affimed N.V. (Germany)

- Citius Pharmaceuticals, Inc. (U.S.)

- Acrotech Biopharma LLC (U.S.)

- Innate Pharma S.A. (France)

- Johnson & Johnson Services, Inc. (U.S.)

- Chipscreen Biosciences Co., Ltd. (China)

What are the Recent Developments in Global Thymus (T)-Cell Lymphoma Treatment Market?

- In June 2025, the European Commission approved brentuximab vedotin-based combination therapy (BrECADD regimen) for newly diagnosed advanced-stage Hodgkin lymphoma patients. The approval followed positive Phase 3 trial results demonstrating improved safety and efficacy compared to standard regimens. This milestone strengthens the role of brentuximab vedotin as a backbone therapy across lymphoma indications, including T-cell lymphomas, and reflects continued expansion of targeted biologics in oncology treatment protocols

- In February 2025, the U.S. Food and Drug Administration (FDA) approved brentuximab vedotin (Adcetris) in combination with lenalidomide and rituximab for patients with relapsed or refractory large B-cell lymphoma, including aggressive lymphoma subtypes. This approval was based on the Phase 3 ECHELON-3 trial, which demonstrated improved overall survival and clinical benefit in heavily pretreated patients. The development highlights the growing role of antibody-drug conjugates and combination therapies in lymphoma treatment

- In May 2024, the U.S. FDA expanded the approval of Bristol Myers Squibb’s CAR-T cell therapy (Breyanzi) for additional lymphoma indications, including relapsed or refractory mantle cell lymphoma. The therapy showed significant efficacy, with a high percentage of patients achieving cancer remission. This expansion underscores the increasing importance of CAR-T therapies in treating aggressive lymphomas and highlights the shift toward personalized, cell-based immunotherapies in the market

- In March 2024, the U.S. FDA further expanded the use of Breyanzi to treat chronic lymphocytic leukemia (CLL) and small lymphocytic lymphoma (SLL), following earlier approvals for large B-cell lymphoma. Clinical studies demonstrated meaningful tumor reduction and remission in patients with limited treatment options. This development reflects the rapid evolution of CAR-T therapies and their growing applicability across multiple hematologic malignancies, including T-cell-related lymphomas

- In November 2022, the U.S. FDA approved brentuximab vedotin in combination with chemotherapy for pediatric patients with high-risk classical Hodgkin lymphoma. This marked a significant expansion of the drug’s indication into younger populations and reinforced its role in frontline lymphoma treatment. The approval highlights ongoing efforts to broaden access to targeted therapies across different patient groups and disease stages within the lymphoma treatment landscape

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.