Global T Cell Therapy Market

Market Size in USD Billion

USD

10.76 Billion

USD

41.97 Billion

2025

2033

USD

10.76 Billion

USD

41.97 Billion

2025

2033

| 2026 - 2033 | |

| USD 10.76 Billion | |

| USD 41.97 Billion | |

| % | |

|

Thymus (T)-Cell Therapy Market Overview

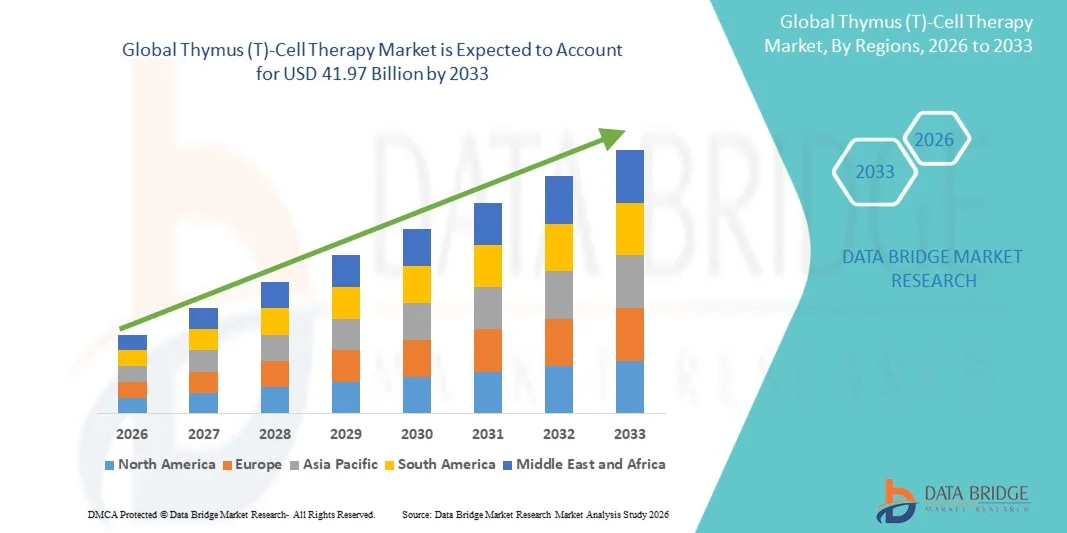

The Thymus (T)-Cell Therapy Market was valued at USD 10.76 billion in 2025 and is projected to reach USD 41.97 billion by 2033, growing at a CAGR of 18.55% from 2026 to 2033. The market is witnessing strong growth driven by the rising global burden of cancer and chronic diseases, increasing adoption of advanced immunotherapies, and rapid progress in cell engineering and genetic modification technologies. Expanding investments in biopharmaceutical research and growing focus on personalized medicine are further accelerating market development.

The increasing number of clinical trials evaluating T-cell–based therapies, including CAR-T and other engineered T-cell approaches, is significantly boosting market expansion. Regulatory approvals for novel cell therapies and improving manufacturing capabilities for scalable, cost-effective production are also supporting commercialization. In addition, the growing application of T-cell therapies beyond oncology, including autoimmune and infectious diseases, along with expanding healthcare infrastructure in emerging economies, is expected to further strengthen market growth during the forecast period.

Key Market Trends & Insights

- North America dominated the Thymus (T)-Cell Therapy Market with the largest revenue share of 42.6% in 2025, supported by strong biopharmaceutical R&D infrastructure, early adoption of advanced immunotherapies, and high concentration of leading cell therapy developers.

- The Commercialized Therapies segment led the market with a 62.4% share in 2025, driven by increasing regulatory approvals and rapid adoption of CAR-T products across major oncology centers.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 18.9% from 2026 to 2033, fueled by rising cancer prevalence, increasing clinical trial activity, and expanding investments in cell and gene therapy manufacturing capabilities.

- Research Therapies are the fastest-growing modality type, projected to register a CAGR of 20.3%, reflecting the surge in robust clinical pipeline of next-generation T-cell therapies.

- The CAR T-cell based segment dominated the therapy type category with a 48.3% revenue share in 2025, led by strong clinical success in hematologic cancers such as lymphoma and leukemia.

- Hematologic Malignancies accounted for 71.5% of the market, preferred by the high success rates of CAR-T therapies in blood cancers.

- The Solid Tumors segment is the fastest-growing indication category, with a CAGR of 22.4%, driven by ongoing advancements in overcoming tumor microenvironment barriers.

Market Size & Forecast

- Global Market Value (2025): USD 10.76 Billion

- Expected Market Value (2033): USD Billion

- Forecast CAGR (2026–2033): 18.55%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Thymus (T)-Cell Therapy Market Segmentation

|

Attributes |

Thymus (T)-Cell Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Bristol Myers Squibb Company (U.S.) · Novartis AG (Switzerland) · Gilead Sciences, Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Pfizer Inc. (U.S.) · Merck & Co., Inc. (U.S.) · AstraZeneca (U.K.) · F. Hoffmann-La Roche Ltd (Switzerland) · Amgen Inc. (U.S.) · GSK plc (U.K.) · Legend Biotech Corporation (China) · CARsgen Therapeutics Ltd. (China) · Allogene Therapeutics, Inc. (U.S.) · Cellectis S.A. (France) · Adaptimmune Therapeutics PLC (U.K.) · Iovance Biotherapeutics, Inc. (U.S.) · Kyverna Therapeutics, Inc. (U.S.) · Arcellx, Inc. (U.S.) · CRISPR Therapeutics AG (Switzerland) · bluebird bio, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of T-cell therapies into non-oncology indications such as autoimmune disorders · Development of off-the-shelf allogeneic T-cell therapies · Integration of next-generation gene editing technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Thymus (T)-Cell Therapy Market Trends

Trend: Expansion of Next-Generation Engineered T-Cell Therapies

Biopharmaceutical companies are increasingly advancing next-generation engineered T-cell therapies, including CAR-T, TCR-T, and dual-target constructs, to improve treatment precision and durability against complex cancers. The integration of gene editing and synthetic biology is enabling enhanced T-cell persistence, reduced relapse rates, and improved safety profiles in clinical applications. Academic institutes and biotech firms are also leveraging tumor-infiltrating lymphocyte (TIL) platforms to broaden treatment access beyond hematologic cancers, while personalized cell therapy manufacturing is becoming more streamlined through automation and closed-system production technologies. For instance, emerging clinical pipelines in solid tumor CAR-T programs are expanding across major oncology research centers.

Thymus (T)-Cell Therapy Market Dynamics

Key Market Driver: Rising Adoption of Cell Therapy in Oncology Treatment Paradigms

The increasing global burden of cancer and the growing shift toward immunotherapy-based treatment approaches are significantly driving demand for T-cell therapies across healthcare systems. Pharmaceutical companies and research organizations are investing heavily in clinical trials and commercialization of CAR-T and engineered T-cell platforms for refractory and relapsed cancers. Regulatory approvals and reimbursement support in developed markets are further accelerating patient access to these advanced therapies, while partnerships between biotech firms and large pharma are enhancing development pipelines. For instance, widespread adoption of CAR-T therapies in relapsed lymphoma and leukemia treatment has strengthened clinical acceptance worldwide.

Key Restraint/Challenge: High Manufacturing Complexity and Treatment Costs

A major challenge in the global T-cell therapy market is the complex and expensive manufacturing process, which requires patient-specific cell extraction, genetic modification, and stringent quality control under controlled laboratory conditions. These therapies involve highly specialized infrastructure, skilled workforce requirements, and cold-chain logistics, significantly increasing overall treatment costs. Limited scalability and long production timelines further restrict accessibility, particularly in low- and middle-income regions. For instance, autologous CAR-T manufacturing cycles often span several weeks, creating delays in treatment delivery for critically ill patients.

Key Market Opportunity: Expansion of Scalable Allogeneic and Off-the-Shelf T-Cell Platforms

The development of allogeneic “off-the-shelf” T-cell therapies presents a major opportunity by enabling mass production, reduced turnaround time, and improved global accessibility of advanced immunotherapies. Advances in gene editing, donor cell engineering, and immune evasion technologies are helping overcome rejection risks and enhancing therapeutic consistency. Companies are increasingly investing in universal donor cell platforms and automated bioprocessing systems to reduce costs and expand commercial viability. For instance, next-generation allogeneic CAR-T programs are being evaluated in multi-center clinical trials to support rapid treatment deployment across oncology indications.

Thymus (T)-Cell Therapy Market Scope

The thymus (T)-cell therapy market is segmented on the basis of modality, therapy type, indication, end-users, and distribution channel.

- By Modality

On the basis of modality, the Thymus (T)-Cell Therapy Market is segmented into research therapies and commercialized therapies. The Commercialized Therapies segment dominated the market with a 62.4% share in 2025, driven by increasing regulatory approvals and rapid adoption of CAR-T products across major oncology centers. These therapies are already integrated into clinical practice for certain hematologic malignancies, ensuring consistent revenue generation. Strong reimbursement frameworks in developed regions further support commercialization. Continuous expansion of approved indications is increasing patient eligibility. Pharmaceutical companies are scaling production to meet rising demand. The segment benefits from strong clinical validation and established treatment protocols.

The Research Therapies segment is expected to witness the fastest growth at a CAGR of 20.3% from 2026 to 2033, driven by a robust clinical pipeline of next-generation T-cell therapies. Increasing investment in early-stage trials for solid tumors and autoimmune diseases is expanding research activity. Academic institutions and biotech startups are actively exploring novel T-cell engineering approaches. Advancements in gene editing and synthetic biology are accelerating experimental therapy development. Rising collaboration between pharma companies and research institutes is strengthening innovation output. Growing demand for personalized immunotherapy is further boosting this segment.

- By Therapy Type

On the basis of therapy type, the market is segmented into CAR T-cell based, T-cell receptor (TCR) based, and tumor infiltrating lymphocytes (TIL) based therapies. The CAR T-cell based segment dominated the market with a 48.3% share in 2025, driven by strong clinical success in hematologic cancers such as lymphoma and leukemia. Widespread regulatory approvals and established commercial products are reinforcing dominance. Continuous pipeline expansion into solid tumors is broadening applications. High treatment efficacy and durable response rates are increasing physician adoption. Strong investment from large biopharma companies is accelerating development. This segment remains the most clinically validated and commercially mature.

The TIL-based therapy segment is expected to witness the fastest growth at a CAGR of 21.1% from 2026 to 2033, driven by rising focus on solid tumor immunotherapy. TIL therapies demonstrate strong potential in melanoma and other difficult-to-treat cancers. Advances in tumor microenvironment research are improving therapeutic outcomes. Increasing clinical trials are expanding global adoption of TIL approaches. Biotech firms are investing in scalable manufacturing processes to overcome production challenges. Growing demand for personalized tumor-specific treatments is further supporting this segment.

- By Indication

On the basis of indication, the market is segmented into hematologic malignancies, solid tumors, and others. The Hematologic Malignancies segment dominated the market with a 71.5% share in 2025, driven by high success rates of CAR-T therapies in blood cancers. Strong clinical evidence supports their use in relapsed and refractory cases. Regulatory approvals have primarily focused on leukemia and lymphoma treatments. Hospitals are increasingly integrating these therapies into standard oncology care. Expanding reimbursement coverage is improving patient access. Continuous innovation is further strengthening outcomes in blood cancer treatment.

The Solid Tumors segment is expected to witness the fastest growth at a CAGR of 22.4% from 2026 to 2033, driven by ongoing advancements in overcoming tumor microenvironment barriers. Researchers are developing next-generation engineered T-cells with enhanced targeting capabilities. Increasing unmet clinical need is driving significant R&D investment. Combination therapies are improving response rates in solid tumor cases. Expanding clinical trials are accelerating validation of new approaches. Pharmaceutical companies are prioritizing solid tumor indications for future expansion.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, homecare, and others. The Hospitals segment dominated the market with a 58.9% share in 2025, driven by the need for specialized infrastructure for cell therapy administration. Hospitals provide controlled environments for complex infusion procedures. Availability of trained oncology specialists supports treatment delivery. Strong institutional reimbursement systems enhance adoption. Integration with clinical trial programs further strengthens dominance. Hospitals remain the primary access point for approved T-cell therapies.

The Specialty Clinics segment is expected to witness the fastest growth at a CAGR of 19.6% from 2026 to 2033, driven by increasing decentralization of cancer care. These clinics offer focused oncology and immunotherapy services. Rising patient preference for specialized treatment centers is supporting growth. Expansion of outpatient cell therapy administration models is improving accessibility. Partnerships with biotech firms are enabling therapy availability outside major hospitals. Growing investment in advanced clinical infrastructure is further boosting adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The Hospital Pharmacy segment dominated the market with a 74.2% share in 2025, driven by the highly controlled nature of T-cell therapy administration. These therapies require direct handling within hospital systems due to strict storage and infusion protocols. Integration with oncology treatment pathways ensures centralized distribution. Strong regulatory oversight supports hospital-based dispensing. Limited outpatient availability further reinforces dominance. Hospitals remain the core supply point for approved cell therapies.

The Online Pharmacy segment is expected to witness the fastest growth at a CAGR of 18.7% from 2026 to 2033, driven by increasing digitalization of healthcare supply chains. Advancements in cold-chain logistics are enabling safe handling of biologics. Growing adoption of tele-oncology consultations is supporting remote treatment coordination. Expanding healthcare access in emerging economies is boosting online distribution demand. Digital platforms are improving ordering efficiency and traceability. However, regulatory constraints still limit full-scale adoption in many regions.

Thymus (T)-Cell Therapy Market Regional Analysis

North America dominated the Thymus (T)-Cell Therapy Market with the largest revenue share of 42.6% in 2025, supported by strong biopharmaceutical R&D infrastructure, early adoption of advanced immunotherapies, and high concentration of leading cell therapy developers. The region also benefits from a high number of FDA-approved CAR-T therapies, robust clinical trial activity, and strong healthcare reimbursement frameworks that support patient access to expensive treatments. Increasing investments from major pharmaceutical companies, along with rapid advancements in gene editing and personalized medicine, continue to strengthen North America’s leadership position in the global market.

U.S. Thymus (T)-Cell Therapy Market Insight

The U.S. thymus (T)-cell therapy market is witnessing strong growth due to rising investments in advanced immunotherapy research, increasing prevalence of cancer, and rapid adoption of CAR-T and other engineered T-cell therapies. The country’s strong biopharmaceutical ecosystem, along with extensive clinical trial activity and early regulatory approvals from the FDA, is driving market expansion across oncology treatment centers and research institutions. In addition, growing focus on personalized medicine and continuous advancements in gene editing technologies are accelerating therapy development and commercialization across the U.S.

Europe Thymus (T)-Cell Therapy Market Insight

The Europe thymus (T)-cell therapy market remains a major contributor to global revenue, driven by strong government support for biotechnology innovation, expanding clinical research programs, and increasing adoption of advanced immunotherapies. The widespread use of cell therapy in oncology treatment centers and academic hospitals is supporting regional market growth. Increasing investments in next-generation CAR-T and TCR-based therapies, coupled with stringent regulatory frameworks ensuring treatment safety and efficacy, continue to enhance the adoption of T-cell therapies across Europe.

U.K. Thymus (T)-Cell Therapy Market Insight

The U.K. thymus (T)-cell therapy market is experiencing steady growth, supported by rising clinical research activity, strong academic-industry collaborations, and increasing focus on advanced cancer treatment solutions. Growing investments in cell and gene therapy manufacturing infrastructure and expanding participation in global clinical trials are contributing to market expansion. Furthermore, integration of precision medicine approaches and government-backed funding initiatives for biotechnology innovation are positioning the U.K. as a key hub for T-cell therapy development.

Germany Thymus (T)-Cell Therapy Market Insight

The Germany thymus (T)-cell therapy market is expanding steadily due to the country’s strong pharmaceutical manufacturing base, advanced biomedical research capabilities, and increasing adoption of innovative cancer therapies. Leading hospitals, research institutes, and biotech companies are actively engaged in developing and commercializing T-cell-based treatments. Continuous advancements in cell processing technologies and strong regulatory support for innovative therapies are further driving market growth in Germany.

Asia-Pacific Thymus (T)-Cell Therapy Market Insight

The Asia-Pacific thymus (T)-cell therapy market is expected to witness rapid growth, driven by rising cancer burden, increasing healthcare investments, and expanding biopharmaceutical manufacturing capabilities across countries such as China, India, and Japan. Growing adoption of immunotherapy, rising clinical trial participation, and improving regulatory frameworks are supporting regional expansion. In addition, increasing government initiatives to promote advanced biotechnology and growing accessibility to novel cancer treatments are accelerating market growth across Asia-Pacific.

Japan Thymus (T)-Cell Therapy Market Insight

The Japan thymus (T)-cell therapy market is witnessing consistent growth due to strong investments in regenerative medicine, advanced oncology research, and increasing adoption of precision immunotherapy approaches. The country’s well-established healthcare system and active participation in clinical development of CAR-T and TCR-based therapies are supporting market expansion. Moreover, integration of cutting-edge biotechnologies and strong government support for cell therapy innovation are further contributing to market growth in Japan.

China Thymus (T)-Cell Therapy Market Insight

The China thymus (T)-cell therapy market is growing rapidly, driven by rising cancer incidence, expanding biotechnology sector, and strong government support for advanced medical innovation. Increasing investments in CAR-T manufacturing facilities, growing number of clinical trials, and rapid adoption of cell-based immunotherapies are significantly boosting market demand. In addition, supportive regulatory reforms and rising collaboration between domestic and global biotech companies are positioning China as one of the fastest-growing markets for T-cell therapy worldwide.

Thymus (T)-Cell Therapy Market Share

The thymus (T)-cell therapy industry is primarily led by well-established companies, including:

- Bristol Myers Squibb Company (U.S.)

- Novartis AG (Switzerland)

- Gilead Sciences, Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- AstraZeneca (U.K.)

- Hoffmann-La Roche Ltd (Switzerland)

- Amgen Inc. (U.S.)

- GSK plc (U.K.)

- Legend Biotech Corporation (China)

- CARsgen Therapeutics Ltd. (China)

- Allogene Therapeutics, Inc. (U.S.)

- Cellectis S.A. (France)

- Adaptimmune Therapeutics PLC (U.K.)

- Iovance Biotherapeutics, Inc. (U.S.)

- Kyverna Therapeutics, Inc. (U.S.)

- Arcellx, Inc. (U.S.)

- CRISPR Therapeutics AG (Switzerland)

- bluebird bio, Inc. (U.S.)

Latest Developments in Thymus (T)-Cell Therapy Market

- In February 2024, the FDA approved Amtagvi (lifileucel), the first tumor-infiltrating lymphocyte (TIL) therapy for advanced melanoma after prior treatment failure. Developed by Iovance Biotherapeutics, this milestone expanded T-cell therapy beyond CAR-T into solid tumor applications. The approval demonstrated the growing clinical viability of TIL-based approaches in difficult-to-treat cancers. It also represented a major breakthrough in personalized cell therapy for solid tumors

- In February 2022, the FDA approved Carvykti (ciltacabtagene autoleucel) developed by Johnson & Johnson and Legend Biotech for relapsed or refractory multiple myeloma. This dual-target CAR-T therapy showed deep and durable responses in clinical trials, significantly advancing treatment outcomes in multiple myeloma patients. Its approval strengthened competition and innovation in BCMA-directed T-cell therapies. The launch also marked a key expansion of CAR-T therapies in late-stage blood cancers

- In July 2021, the FDA approved Tecartus (brexucabtagene autoleucel) for adult patients with relapsed or refractory B-cell precursor acute lymphoblastic leukemia (ALL). Developed by Kite Pharma (Gilead Sciences), this approval expanded CAR-T therapy into a broader and more aggressive blood cancer indication. The treatment demonstrated strong efficacy in heavily pretreated patients with limited options. This milestone further established CAR-T as a standard immunotherapy platform in hematologic cancers

- In May 2021, the FDA approved Abecma (idecabtagene vicleucel), developed by Bristol Myers Squibb and bluebird bio, as the first CAR-T therapy for multiple myeloma. This milestone introduced a new treatment option for patients with relapsed or refractory disease after multiple prior therapies. The approval highlighted the expanding use of T-cell therapies beyond lymphoma into plasma cell malignancies. It also reinforced the growing clinical validation of BCMA-targeted CAR-T approaches.

- In February 2021, Bristol Myers Squibb announced the U.S. FDA approval of Breyanzi (lisocabtagene maraleucel) for relapsed or refractory large B-cell lymphoma, marking a major advancement in CAR-T cell therapy for blood cancers. The therapy is designed to reprogram a patient’s own T-cells to target CD19-positive cancer cells, improving survival outcomes in heavily pretreated patients. This approval strengthened the commercial CAR-T landscape and expanded treatment options in hematologic malignancies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.