Global Technical Films Market

Market Size in USD Billion

USD

42.67 Billion

USD

64.25 Billion

2025

2033

USD

42.67 Billion

USD

64.25 Billion

2025

2033

| 2026 - 2033 | |

| USD 42.67 Billion | |

| USD 64.25 Billion | |

| % | |

|

Technical Films Market Overview

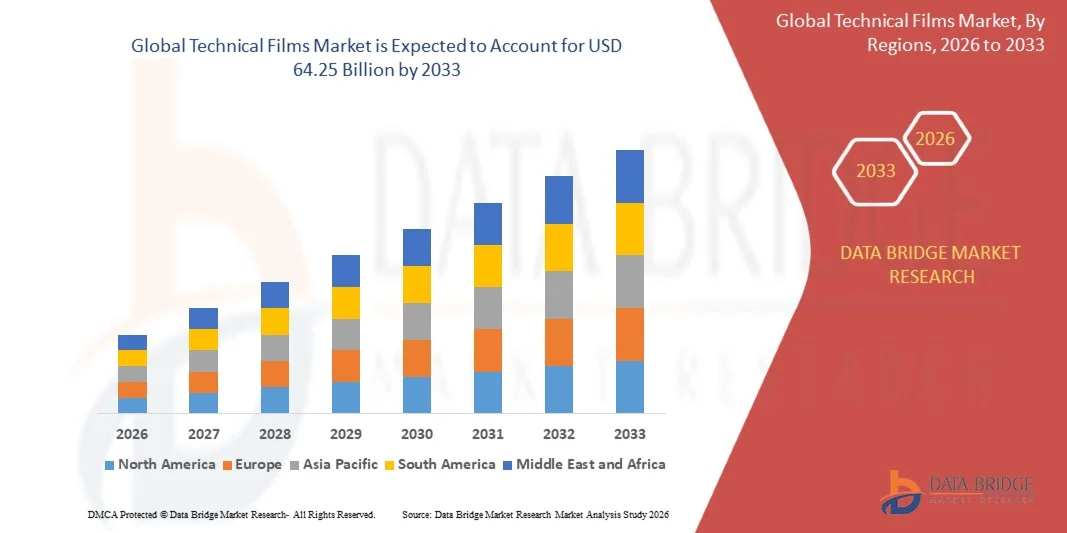

As per Data Bridge Market Research analysis the Technical Films Market was valued at USD 42.67 billion in 2025 and is projected to reach USD 64.25 billion by 2033, growing at a CAGR of 5.25% from 2026 to 2033. The market is experiencing steady growth driven by increasing demand for high-performance packaging materials, expanding use of specialty films in automotive and construction applications, and rising adoption of protective, barrier, and functional films across industrial sectors.

The growing need for lightweight, durable, and application-specific materials is encouraging manufacturers to adopt technical films with enhanced barrier properties, heat resistance, optical clarity, and chemical resistance. Technical films are increasingly used in flexible packaging, solar panels, electronic displays, automotive interiors, medical products, and building applications, where conventional films may not meet performance requirements. The expansion of sustainable packaging initiatives and growing development of recyclable, bio-based, and mono-material film solutions are further accelerating demand for advanced technical films across global markets.

Key Market Trends & Insights

- North America dominated the technical films market with the largest revenue share in 2025, supported by strong demand for advanced packaging materials, established food and beverage processing industries, expanding pharmaceutical packaging requirements, and increasing adoption of protective, insulation, and specialty films across automotive, construction, and electronics sectors.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 6.40% from 2026 to 2033. Growth is driven by rapid industrialization, expanding flexible packaging production, rising food and beverage consumption, increasing electric vehicle and electronics manufacturing, and growing investments in polymer processing capacity across China, Japan, India, and South Korea.

- The barrier film segment held the largest market revenue share of approximately 28.6% in 2025 driven by its widespread use in food packaging, pharmaceutical packaging, medical products, and industrial protective applications. Barrier films are preferred due to their ability to protect products from moisture, oxygen, aroma loss, ultraviolet radiation, and contamination, supporting longer shelf life and improved product integrity.

- The conductive film segment is projected to register the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing demand for touch panels, flexible displays, printed electronics, electric vehicle components, and electromagnetic shielding applications. Rising adoption of smart devices and advanced electronic systems is accelerating segment expansion.

- The non-degradable film segment held the largest market revenue share of approximately 76.4% in 2025 driven by its extensive use across flexible packaging, automotive, construction, electrical, and industrial applications. Non-degradable films are widely preferred due to their high durability, moisture resistance, mechanical strength, and compatibility with high-speed manufacturing and packaging processes.

- The degradable film segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by growing restrictions on single-use plastics, rising demand for compostable packaging, and increasing investment in bio-based polymer technologies. Expanding adoption of biodegradable films across food service, agriculture, and consumer goods packaging is accelerating segment growth.

- The food and beverage segment held the largest market revenue share of approximately 31.7% in 2025 driven by high demand for flexible packaging, barrier pouches, lidding films, shrink sleeves, and protective wraps. Technical films are increasingly used to extend shelf life, maintain food quality, and support lightweight packaging requirements across retail and foodservice applications.

- The electrical and electronic segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising production of smartphones, display panels, flexible circuits, batteries, and semiconductor components. Growing demand for optical, conductive, insulating, and protective films in consumer electronics and electric vehicle systems is accelerating segment expansion.

- The polyethylene segment held the largest market revenue share of approximately 29.4% in 2025 driven by its widespread use in stretch films, protective packaging, agricultural films, and industrial wrapping applications. Polyethylene films are preferred due to their flexibility, moisture resistance, low cost, and compatibility with recyclable mono-material packaging structures.

- The polyethylene terephthalate segment is projected to register the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing demand for high-strength, transparent, heat-resistant, and recyclable films in packaging, electronics, solar panels, and automotive applications. Rising use of PET films in flexible displays, electrical insulation, and high-barrier packaging is accelerating segment expansion.

- The 25–50 microns segment held the largest market revenue share of approximately 35.8% in 2025 driven by its widespread use in flexible packaging, labels, laminates, shrink sleeves, and protective films. Films within this thickness range provide a balance between material efficiency, flexibility, barrier performance, and mechanical strength, making them suitable for high-volume consumer and industrial applications.

- The 50–100 microns segment is projected to register the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing demand for durable automotive films, construction membranes, electrical insulation films, and industrial protective applications. Rising adoption of thicker films for battery protection, surface protection, and high-performance packaging is accelerating segment expansion.

Market Size & Forecast

- Global Market Value (2025): USD 42.67 Billion

- Expected Market Value (2033): USD 64.25 Billion

- Forecast CAGR (2026–2033): 5.25%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Technical Films Market Segmentation

|

Attributes |

Technical Films Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• SABIC (Saudi Arabia) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Technical Films Market Trends

Trend: Growing Demand For Sustainable High-Barrier And Functional Technical Films

Increasing demand for lightweight, durable, and high-performance materials across packaging, automotive, electronics, construction, and healthcare sectors is accelerating the adoption of technical films. Conventional packaging and protective materials often provide limited barrier performance and can be difficult to recycle, encouraging manufacturers to develop multilayer, mono-material, recyclable, and bio-based film solutions with improved moisture, oxygen, chemical, and heat resistance.

In flexible packaging, manufacturers are increasingly using high-barrier technical films to extend product shelf life and reduce food waste. For instance, the Food and Agriculture Organization estimates that approximately 13% of food is lost after harvest and before reaching retail markets globally, increasing the need for packaging materials that protect products during transportation and storage. Technical films with oxygen and moisture barriers are widely used in food, pharmaceutical, and medical packaging to maintain product quality while reducing material use through thinner and lighter film structures.

The rapid expansion of electric vehicles, solar energy systems, and consumer electronics is also increasing demand for specialty films with insulation, flame resistance, optical clarity, and thermal stability properties. Technical films are used in battery packs, display panels, photovoltaic back sheets, automotive interiors, and electronic component protection. In addition, the global shift toward circular packaging is encouraging film producers to invest in recyclable polyethylene and polypropylene-based structures that can replace complex multilayer laminates in selected applications.

Technical Films Market Dynamics

Key Market Driver: Rising Demand For High-Performance Packaging And Industrial Applications

Industries worldwide are facing increasing demand for packaging and material solutions that provide higher protection, lower weight, and improved functional performance. The growing need to protect food, pharmaceutical products, electronics, and industrial components from moisture, oxygen, contamination, ultraviolet radiation, and mechanical damage is creating strong demand for advanced technical films. These films are increasingly engineered with specialized coatings, multilayer structures, and barrier layers to meet application-specific performance requirements.

Packaging companies are increasingly deploying technical films in flexible food packaging, medical packaging, industrial wraps, and protective laminates to improve product safety and shelf life. For instance, the United Nations Environment Programme reported that 931 million tonnes of food waste were generated globally in 2019, highlighting the importance of packaging systems that can reduce spoilage throughout the supply chain. High-barrier films are used to protect perishable products, while heat-sealable and puncture-resistant films support efficient automated packaging operations.

Similarly, automotive and construction industries are adopting technical films for paint protection, window films, decorative surfaces, insulation layers, and lightweight interior components. The International Energy Agency reported that global electric car sales exceeded 17 million units in 2024, increasing demand for dielectric, flame-retardant, and thermal management films used in electric vehicle battery and electronic systems. Growing industrial automation and demand for durable materials are further supporting technical film adoption across manufacturing applications

Key Restraint/Challenge: Volatile Raw Material Prices And Recycling Complexity

Technical films are commonly manufactured using polymer resins such as polyethylene, polypropylene, polyester, polyamide, polyvinyl chloride, and specialty fluoropolymers. Price fluctuations in crude oil, natural gas, and petrochemical feedstocks can directly affect resin costs and manufacturing margins. The use of specialty additives, coatings, adhesives, and barrier layers can further increase production expenses, creating cost pressures for film manufacturers and end users, particularly in price-sensitive packaging applications.

In addition, many high-performance technical films use multilayer structures combining different polymers, aluminum coatings, adhesives, and functional additives. While these structures provide strong barrier and durability properties, they can be difficult to separate and recycle through conventional waste management systems. The Organisation for Economic Co-operation and Development reported that only 9% of plastic waste was recycled globally in 2019, demonstrating the broader infrastructure challenge affecting the circularity of plastic-based materials.

Regulatory restrictions on single-use plastics and growing consumer concern regarding plastic waste are also increasing the need for recyclable and lower-impact technical film solutions. Manufacturers must balance barrier performance, cost, processing compatibility, and recyclability while complying with evolving packaging regulations. Developing mono-material structures and recyclable coatings can require extensive research, reformulation, and equipment investment, increasing product development timelines.

Key Market Opportunity: Expansion Of Recyclable Films In Electric Vehicles And Advanced Electronics

The growing development of electric vehicles, renewable energy systems, flexible electronics, and smart packaging is creating significant opportunities for technical film manufacturers. These applications require lightweight materials with specialized properties such as electrical insulation, flame resistance, thermal stability, chemical resistance, and optical performance. Technical films can support component protection and weight reduction while enabling compact product designs across high-growth industrial sectors.

Automotive manufacturers are increasingly using specialty films in electric vehicle battery packs, cable insulation, interior surfaces, paint protection, and display applications. For instance, electric vehicle battery systems require insulation materials that can withstand high voltage and elevated operating temperatures, while flame-retardant films can help improve battery pack safety. The International Energy Agency expects electric car sales to exceed 20 million units in 2025, creating continued demand for advanced polymer films used in vehicle electrification and battery component applications.

In consumer electronics, technical films are increasingly used in display protection, flexible circuits, touch panels, optical films, and thermal interface materials. The Semiconductor Industry Association reported that global semiconductor sales reached USD 627.6 billion in 2024, reflecting continued expansion in electronic devices and semiconductor manufacturing. Advancements in recyclable barrier coatings, bio-based polymers, and high-performance film extrusion technologies are expected to create opportunities across sustainable packaging, electric mobility, solar energy, and next-generation electronics.

Technical Films Market Scope

The market is segmented on the basis of film type, product type, end-use industry, material type, and thickness type

• By Film Type

On the basis of film type, the technical films market is segmented into stretch film, shrink film, barrier film, conductive film, safety and security film, anti-fog film, and other technical films. The barrier film segment held the largest market revenue share of approximately 28.6% in 2025 driven by its widespread use in food packaging, pharmaceutical packaging, medical products, and industrial protective applications. Barrier films are preferred due to their ability to protect products from moisture, oxygen, aroma loss, ultraviolet radiation, and contamination, supporting longer shelf life and improved product integrity.

The conductive film segment is projected to register the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing demand for touch panels, flexible displays, printed electronics, electric vehicle components, and electromagnetic shielding applications. Rising adoption of smart devices and advanced electronic systems is accelerating segment expansion.

• By Product Type

On the basis of product type, the technical films market is segmented into degradable film and non-degradable film. The non-degradable film segment held the largest market revenue share of approximately 76.4% in 2025 driven by its extensive use across flexible packaging, automotive, construction, electrical, and industrial applications. Non-degradable films are widely preferred due to their high durability, moisture resistance, mechanical strength, and compatibility with high-speed manufacturing and packaging processes.

The degradable film segment is projected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by growing restrictions on single-use plastics, rising demand for compostable packaging, and increasing investment in bio-based polymer technologies. Expanding adoption of biodegradable films across food service, agriculture, and consumer goods packaging is accelerating segment growth.

• By End-Use Industry

On the basis of end-use industry, the technical films market is segmented into food and beverage, cosmetic and personal care, chemical, agriculture, building and construction, pharmaceutical, electrical and electronic, and automobile. The food and beverage segment held the largest market revenue share of approximately 31.7% in 2025 driven by high demand for flexible packaging, barrier pouches, lidding films, shrink sleeves, and protective wraps. Technical films are increasingly used to extend shelf life, maintain food quality, and support lightweight packaging requirements across retail and foodservice applications.

The electrical and electronic segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising production of smartphones, display panels, flexible circuits, batteries, and semiconductor components. Growing demand for optical, conductive, insulating, and protective films in consumer electronics and electric vehicle systems is accelerating segment expansion.

• By Material Type

On the basis of material type, the technical films market is segmented into polyethylene (PE), polyethylene terephthalate (PET), polyamide (PA), polypropylene (PP), polyvinyl chloride (PVC), ethylene vinyl alcohol (EVOH), polyurethane (PU), aluminum, polycarbonate (PC), and others. The polyethylene segment held the largest market revenue share of approximately 29.4% in 2025 driven by its widespread use in stretch films, protective packaging, agricultural films, and industrial wrapping applications. Polyethylene films are preferred due to their flexibility, moisture resistance, low cost, and compatibility with recyclable mono-material packaging structures.

The polyethylene terephthalate segment is projected to register the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing demand for high-strength, transparent, heat-resistant, and recyclable films in packaging, electronics, solar panels, and automotive applications. Rising use of PET films in flexible displays, electrical insulation, and high-barrier packaging is accelerating segment expansion.

• By Thickness Type

On the basis of thickness type, the technical films market is segmented into up to 25 microns, 25–50 microns, 50–100 microns, and 100–150 microns. The 25–50 microns segment held the largest market revenue share of approximately 35.8% in 2025 driven by its widespread use in flexible packaging, labels, laminates, shrink sleeves, and protective films. Films within this thickness range provide a balance between material efficiency, flexibility, barrier performance, and mechanical strength, making them suitable for high-volume consumer and industrial applications.

The 50–100 microns segment is projected to register the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing demand for durable automotive films, construction membranes, electrical insulation films, and industrial protective applications. Rising adoption of thicker films for battery protection, surface protection, and high-performance packaging is accelerating segment expansion.

Technical Films Market Regional Analysis

North America Technical Films Market Insight

North America dominated the technical films market with the largest revenue share in 2025, supported by strong demand for high-performance packaging, advanced automotive materials, medical films, and electrical insulation applications. Manufacturers across the region are increasingly adopting barrier, protective, conductive, and specialty films to improve product durability, shelf life, and functional performance. The established presence of packaging converters, automotive manufacturers, electronics producers, and advanced material suppliers is further supporting market expansion across food and beverage, healthcare, construction, and industrial applications.

U.S. Technical Films Market Insight

The U.S. technical films market captured the largest revenue share in 2025 within North America, fueled by rising demand for sustainable flexible packaging, growing adoption of electric vehicles, and increasing use of specialty films in electronics and medical products. Packaging companies are increasingly deploying recyclable, high-barrier, and mono-material film structures to meet changing consumer preferences and evolving sustainability requirements. Moreover, the expansion of semiconductor manufacturing, electric vehicle battery production, and pharmaceutical packaging activities is significantly contributing to the growth of technical film applications across the country.

Europe Technical Films Market Insight

The Europe technical films market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent packaging waste regulations, rising demand for recyclable materials, and increasing adoption of high-performance films across automotive and construction applications. European manufacturers are increasingly investing in recyclable polyethylene, polypropylene, polyester, and bio-based technical films to reduce dependence on complex multilayer packaging structures. The region is experiencing significant growth across food packaging, automotive surface protection, solar energy, and industrial insulation applications, with technical films being incorporated into both new product development and sustainability-focused packaging conversion projects.

U.K. Technical Films Market Insight

The U.K. technical films market is expected to witness the fastest growth rate from 2026 to 2033, driven by growing demand for sustainable packaging, expanding e-commerce activity, and increasing use of protective films in construction and consumer goods applications. The rising focus on reducing plastic waste is encouraging packaging manufacturers and brand owners to adopt recyclable and lightweight technical film solutions. The U.K.’s established food processing, pharmaceutical, and retail sectors, combined with growing investment in advanced packaging technologies, are expected to continue stimulating market growth.

Germany Technical Films Market Insight

The Germany technical films market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s strong automotive, engineering, chemical, and packaging manufacturing base. German manufacturers are increasingly adopting technical films in electric vehicle battery systems, automotive interiors, paint protection, industrial laminates, and high-barrier packaging applications. The integration of recyclable and high-performance films with automotive electrification, industrial automation, and sustainable packaging systems is also becoming increasingly prevalent across the country.

Asia-Pacific Technical Films Market Insight

The Asia-Pacific technical films market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding packaging production, rising consumer goods demand, and growing electronics and automotive manufacturing across countries such as China, Japan, India, and South Korea. The region’s increasing focus on food safety, lightweight packaging, electric mobility, and consumer electronics is driving the adoption of barrier, conductive, protective, and optical technical films. Furthermore, the presence of large-scale polymer processing facilities and expanding manufacturing supply chains is improving the affordability and accessibility of technical films across regional markets.

Japan Technical Films Market Insight

The Japan technical films market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced electronics industry, strong automotive manufacturing sector, and increasing demand for high-precision material solutions. Japanese manufacturers are increasingly using technical films in display panels, flexible circuits, semiconductor packaging, battery insulation, automotive interiors, and medical products. The growing adoption of optical, conductive, and heat-resistant films in next-generation electronics and electric vehicle applications is fueling market growth, while Japan’s focus on innovation and material quality is expected to support continued adoption.

China Technical Films Market Insight

The China technical films market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large packaging industry, expanding consumer goods production, and rapid growth in electronics and electric vehicle manufacturing. China is one of the largest markets for flexible packaging and technical film materials, with increasing use of barrier films, protective films, conductive films, and battery insulation films across food, industrial, and automotive applications. The country’s focus on electric mobility, advanced manufacturing, sustainable packaging, and domestic polymer production, alongside the presence of large film producers and packaging converters, are key factors propelling the technical films market in China.

Technical Films Market Share

The Technical Films industry is primarily led by well-established companies, including:

- SABIC (Saudi Arabia)

- Borealis AG (Austria)

- Mondi (U.K.)

- Jindal Poly Films (U.S.)

- Amcor plc (Switzerland)

- Huhtamaki (Finland)

- Sealed Air (U.S.)

- Toppan Inc., (Japan)

- Kureha Corporation (Japan)

- HPM Global, Inc. (South Korea)

- Flair Flexible Packaging Corporation (U.S.)

- Constantia Flexibles (Austria)

- MULTIVAC (Germany)

- DuPont (U.S.)

- Wihuri Group (Finland)

- BERNHARDT Packaging & Process (France)

- Uflex Limited (India)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Technical Films Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Technical Films Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Technical Films Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.