Global Telecom Cloud Market

Market Size in USD Billion

CAGR :

%

USD

39.83 Billion

USD

218.35 Billion

2025

2033

USD

39.83 Billion

USD

218.35 Billion

2025

2033

| 2026 –2033 | |

| USD 39.83 Billion | |

| USD 218.35 Billion | |

| % | |

|

Telecom Cloud Market Overview

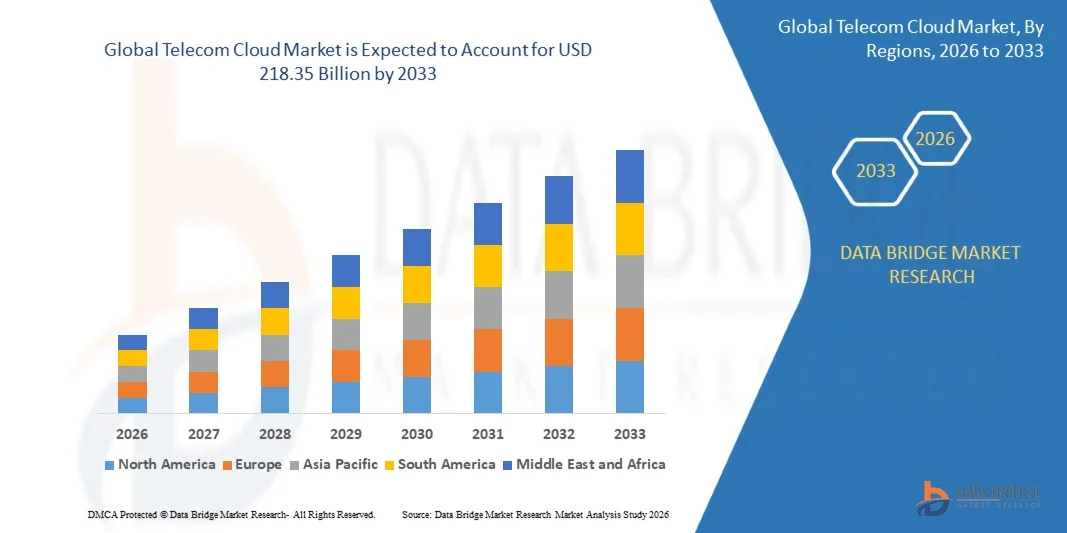

The global telecom cloud market was valued at USD 39.83 Billion in 2025 and is projected to reach USD 218.35 Billion by 2033, growing at a CAGR of 23.7% from 2026 to 2033. The market is experiencing consistent growth driven by rapid 5G deployment, increasing virtualization of telecom networks, and rising adoption of cloud-native architectures by telecom operators. Expanding investments in edge computing, network function virtualization (NFV), and software-defined networking (SDN) are further accelerating the transition toward scalable and flexible telecom cloud infrastructures across global markets.

The growing demand for high-speed connectivity, low-latency communication, and cost-efficient network management is significantly driving telecom operators to shift from legacy infrastructure to cloud-based platforms. Increasing digital transformation initiatives across enterprises, along with rising consumption of data-intensive services such as streaming, IoT, and smart applications, is further strengthening the adoption of telecom cloud solutions worldwide.

Key Market Trends & Insights

- Asia-Pacific dominated the global telecom cloud market with the largest revenue share of 36.3% in 2025, supported by rapid 5G deployment, large-scale telecom infrastructure expansion, and strong digital transformation initiatives across emerging economies

- The solutions segment led the market with a 59.3% share in 2025, driven by rising deployment of cloud-native telecom infrastructure, virtualization of network functions, and increasing adoption of software-defined networking across telecom operators

- North America is expected to be the fastest-growing region at a CAGR of 19.5% from 2026 to 2033, fueled by advanced telecom infrastructure, strong cloud adoption, and rapid deployment of 5G and edge computing technologies

- Hybrid cloud are the fastest-growing deployment mode type, projected to register a CAGR of 25.2% from 2026 to 2033, supported by the need for flexible, scalable, and cost-efficient telecom infrastructure

- The traffic management segment dominated the application category with a 41.7% revenue share in 2025, led by increasing data consumption, rising mobile traffic, and growing demand for real-time network optimization

- Infrastructure as a Service (IaaS) accounted for 34.8% of the market in 2025, preferred by strong demand for scalable computing resources, storage, and virtualized infrastructure among telecom operators

- The Network as a Service (NaaS) segment is the fastest-growing service model category, with a CAGR of 21.3% from 2026 to 2033, driven by rising adoption of software-defined networking and cloud-based connectivity solutions

Market Size & Forecast

- Global Market Value (2025): USD 39.83 Billion

- Expected Market Value (2033): USD 218.35 Billion

- Forecast CAGR (2026–2033): 23.7%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Global Telecom Cloud Market Segmentation

|

Attributes |

Telecom Cloud Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· AT&T Intellectual Property (U.S.) · BT (U.K.) · Verizon (U.S.) · CenturyLink (U.S.) · Telefonaktiebolaget LM Ericsson (Sweden) · Deutsche Telekom AG (Germany) · NTT Communications Corporation (Japan) · Singtel (Singapore) · Microsoft (U.S.) · Epsilon Telecommunications Limited (U.K.) · Logicalis Group (U.K.) · Orange Business Services (France) · Telstra Enterprise (Australia) · Fusion Connect, Inc. (U.S.) · ZTE Corporation (China) · Vodafone Idea Limited (India) · China Telecom Global Limited (China) · TELUS (Canada) · T-Mobile USA, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Edge Computing in Telecom Networks · Growth in Network Function Virtualization (NFV) and SDN Adoption · Rising Demand for Enterprise Unified Cloud Communication Services |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Global Telecom Cloud Market Trends

Trend: Rapid Adoption of 5G-Driven Cloud-Native Telecom Networks

Telecom operators are increasingly shifting toward cloud-native architectures to support large-scale 5G deployment, enabling higher scalability, automation, and service agility across networks. Cloud-native telecom infrastructure allows virtualization of core network functions, reducing dependency on legacy hardware and improving real-time service delivery. The rapid expansion of 5G services, IoT ecosystems, and edge-based applications is accelerating adoption of cloud-based telecom architectures across global markets.

Companies such as Verizon and Deutsche Telekom AG are actively deploying cloud-native 5G core networks and edge-enabled telecom cloud platforms to enhance network performance and support next-generation digital services across enterprise and consumer applications.

Global Telecom Cloud Market Dynamics

Key Market Driver: Rising Demand for Scalable and Cost-Efficient Network Infrastructure

The increasing demand for scalable, flexible, and cost-efficient telecom infrastructure is significantly driving the adoption of telecom cloud solutions worldwide. Telecom operators are replacing capital-intensive legacy systems with cloud-based infrastructure to optimize operational costs, improve network efficiency, and support growing data traffic demands. The expansion of digital services, streaming platforms, and connected devices is further intensifying the need for agile and high-capacity telecom networks.

Companies such as AT&T and BT Group are heavily investing in cloud transformation initiatives, including network virtualization and software-defined networking, to reduce infrastructure costs and improve service scalability across their telecom operations.

Key Restraint/Challenge: High Complexity in Legacy Network Migration to Cloud Environments

A major challenge in the Telecom Cloud market is the high complexity associated with migrating legacy telecom infrastructure to cloud-based environments. Telecom operators face integration issues, interoperability challenges, and high transition costs while modernizing traditional network systems. Ensuring service continuity during migration and maintaining security across hybrid environments further increases implementation difficulty.

For instance, Orange Business Services and Telstra Enterprise have highlighted the operational complexity involved in transitioning legacy network systems to cloud-native architectures while maintaining uninterrupted enterprise and telecom service delivery across global networks.

Key Market Opportunity: Expansion of Edge Computing in Telecom Networks

The rapid expansion of edge computing is creating significant growth opportunities in the Telecom Cloud market by enabling ultra-low latency processing and real-time data management closer to end users. Edge-based telecom cloud solutions support advanced applications such as autonomous systems, smart cities, and industrial IoT, improving network responsiveness and reducing bandwidth congestion. The integration of edge computing with 5G networks is further enhancing service quality and enabling new revenue streams for telecom operators.

Companies such as Microsoft and NTT Communications Corporation are actively investing in edge-enabled telecom cloud infrastructure to support distributed computing, real-time analytics, and next-generation digital services across global telecom ecosystems.

Global Telecom Cloud Market Scope

The telecom cloud market is segmented on the basis of type, service model, organization size, deployment mode, application, and end user.

- By Type

On the basis of type, the global Telecom Cloud market is segmented into solutions and services. The Solutions segment dominated the market with the largest share of 59.3% in 2025, driven by rising deployment of cloud-native telecom infrastructure, virtualization of network functions, and increasing adoption of software-defined networking across telecom operators. Telecom companies are heavily investing in scalable cloud platforms to improve network efficiency, reduce operational costs, and support 5G and edge computing workloads. Growing demand for real-time data processing and automated network orchestration further strengthens segment dominance.

The Services segment is projected to register the fastest growth with a CAGR of 18.7% from 2026 to 2033, driven by increasing reliance on managed services, integration support, and cloud migration consulting. Telecom operators are outsourcing cloud operations to improve flexibility, reduce infrastructure complexity, and accelerate digital transformation. Rising adoption of hybrid and multi-cloud environments is further boosting demand for professional and managed telecom cloud services.

- By Service Model

On the basis of service model, the Telecom Cloud market is segmented into Infrastructure as a Service (IaaS), Software as a Service (SaaS), Platform as a Service (PaaS), Community as a Service (CaaS), and Network as a Service (NaaS). The IaaS segment dominated the market with a share of 34.8% in 2025, driven by strong demand for scalable computing resources, storage, and virtualized infrastructure among telecom operators. It enables flexible network expansion, efficient workload management, and cost optimization for large-scale telecom operations. Increasing deployment of 5G infrastructure and edge data centers further reinforces its leadership.

The NaaS segment is projected to register the fastest growth with a CAGR of 21.3% from 2026 to 2033, driven by rising adoption of software-defined networking and cloud-based connectivity solutions. Telecom operators are increasingly shifting toward on-demand network services to improve agility, scalability, and service customization. Expansion of 5G, IoT ecosystems, and ultra-low latency applications is further accelerating demand for network-as-a-service models.

- By Organization Size

On the basis of organization size, the Telecom Cloud market is segmented into small and medium enterprises and large enterprises. The Large Enterprises segment dominated the market with a share of 51.1% in 2025, driven by extensive cloud transformation initiatives, large-scale telecom infrastructure investments, and high adoption of advanced virtualization technologies. These organizations have strong financial capacity to deploy private and hybrid cloud solutions for mission-critical network operations. Rising demand for secure, scalable, and high-performance telecom infrastructure further strengthens their dominance.

The Small and Medium Enterprises segment is projected to register the fastest growth with a CAGR of 19.5% from 2026 to 2033, driven by increasing cloud affordability, subscription-based models, and rapid digitalization. SMEs are adopting telecom cloud solutions to reduce capital expenditure and improve operational efficiency. Expansion of cloud service accessibility and managed telecom platforms is further accelerating adoption among smaller operators and service providers.

- By Deployment Mode

On the basis of deployment mode, the Telecom Cloud market is segmented into public cloud, private cloud, and hybrid cloud. The Private Cloud segment dominated the market with a share of 39.6% in 2025, driven by high demand for data security, regulatory compliance, and dedicated telecom infrastructure control. Telecom operators prefer private cloud environments for core network functions and sensitive customer data management. Increasing concerns regarding data privacy and network reliability further reinforce its dominant position.

The Hybrid Cloud segment is projected to register the fastest growth with a CAGR of 25.2% from 2026 to 2033, driven by the need for flexible, scalable, and cost-efficient telecom infrastructure. Operators are increasingly combining public and private cloud environments to balance performance, security, and cost optimization. Rising deployment of 5G services and edge computing applications is further accelerating hybrid cloud adoption across telecom ecosystems.

- By Application

On the basis of application, the Telecom Cloud market is segmented into billing and provisioning, traffic management, and others. The Traffic Management segment dominated the market with a share of 41.7% in 2025, driven by increasing data consumption, rising mobile traffic, and growing demand for real-time network optimization. Telecom operators are deploying cloud-based traffic management systems to ensure network efficiency, reduce congestion, and enhance user experience. Rapid expansion of 5G and IoT ecosystems further strengthens segment leadership.

The Billing and Provisioning segment is projected to register the fastest growth with a CAGR of 18.9% from 2026 to 2033, driven by increasing demand for automated billing systems, real-time charging solutions, and flexible subscription models. Telecom operators are adopting cloud-based billing platforms to improve accuracy, scalability, and customer experience. Rising adoption of digital services and pay-as-you-go models further accelerates segment expansion.

- By End User

On the basis of end user, the Telecom Cloud market is segmented into BFSI, retail and consumer goods, healthcare and life sciences, government and public sector, transportation and distribution, media and entertainment, and others. The BFSI segment dominated the market with a share of 28.9% in 2025, driven by high demand for secure communication networks, cloud-based data processing, and real-time transaction systems. Financial institutions rely on telecom cloud infrastructure for secure, low-latency, and high-availability services. Increasing digital banking and fintech adoption further strengthens segment dominance.

The Healthcare and Life Sciences segment is projected to register the fastest growth with a CAGR of 21.6% from 2026 to 2033, driven by rising adoption of telemedicine, remote patient monitoring, and cloud-based health data management. Healthcare providers are increasingly relying on telecom cloud platforms for secure data transmission and real-time connectivity. Expansion of digital health ecosystems and IoT-enabled medical devices further accelerates market growth.

Global Telecom Cloud Market Regional Analysis

Asia-Pacific dominated the telecom cloud market and accounted for the largest revenue share of 36.3% in 2025, supported by rapid 5G deployment, large-scale telecom infrastructure expansion, and strong digital transformation initiatives across emerging economies. The region benefits from a massive subscriber base, increasing mobile data consumption, and strong investments in cloud-native telecom architectures. Growing adoption of edge computing, virtualization, and network automation is further accelerating market expansion across major economies. In addition, government-led digitalization programs and rising data center investments are strengthening regional dominance.

China Telecom Cloud Market Insight

China held the largest share in the Asia-Pacific Telecom Cloud market in 2025, driven by aggressive 5G rollout, strong cloud infrastructure investments, and rapid expansion of hyperscale data centers. The country’s telecom operators are heavily investing in cloud-native network functions and AI-driven traffic management systems. Strong demand from industrial internet applications and smart city projects is further supporting market growth. In addition, the presence of major cloud and telecom players such as China Telecom and Huawei is reinforcing China’s leadership in the regional market.

India Telecom Cloud Market Insight

India is witnessing the fastest growth in the Asia-Pacific region with a CAGR of 21.4% from 2026 to 2033, driven by rapid 5G adoption, increasing smartphone penetration, and strong expansion of digital services. Telecom operators are increasingly shifting toward cloud-based network infrastructure to support rising data traffic and cost optimization. Growth in fintech, OTT platforms, and e-governance services is further accelerating demand for telecom cloud solutions. In addition, strong investments by Reliance Jio and Bharti Airtel in cloud-native telecom networks are boosting long-term market expansion.

Europe Telecom Cloud Market Insight

The Europe Telecom Cloud market is expanding steadily, supported by strong regulatory frameworks, increasing adoption of 5G infrastructure, and growing demand for secure cloud-based telecom services. Telecom operators are investing in hybrid cloud and edge computing solutions to enhance network efficiency and data security. Rising demand from BFSI, industrial automation, and smart mobility applications is further supporting market growth. In addition, strong focus on data privacy regulations such as GDPR is driving adoption of private and hybrid cloud deployments.

Germany Telecom Cloud Market Insight

Germany accounted for the largest share in the Europe Telecom Cloud market in 2025, driven by advanced industrial digitization, strong 5G infrastructure development, and high adoption of cloud-based telecom solutions in enterprise networks. The country benefits from a robust manufacturing ecosystem that increasingly relies on low-latency connectivity and edge computing. Strong investments in Industry 4.0 and smart factory initiatives are further boosting demand. In addition, collaboration between telecom operators and cloud providers is reinforcing Germany’s leadership position in the regional market.

U.K. Telecom Cloud Market Insight

The U.K. market is supported by rapid digital transformation across financial services, media, and public sector applications. Telecom operators are increasingly adopting cloud-native architectures to improve network scalability and service delivery efficiency. Strong growth in 5G-enabled services, streaming platforms, and digital banking is further driving demand. In addition, government-led initiatives to enhance national connectivity infrastructure are supporting continued market expansion.

North America Telecom Cloud Market Insight

North America is projected to grow at the fastest CAGR of 19.5% from 2026 to 2033, driven by advanced telecom infrastructure, strong cloud adoption, and rapid deployment of 5G and edge computing technologies. Telecom operators in the region are heavily investing in virtualization, network automation, and AI-driven traffic management systems. Rising demand from hyperscale data centers, BFSI, and media streaming services is further accelerating growth. In addition, strong presence of leading cloud providers and telecom giants is boosting regional market expansion.

U.S. Telecom Cloud Market Insight

The U.S. accounted for the largest share in the North America Telecom Cloud market in 2025, supported by early 5G commercialization, large-scale cloud infrastructure deployment, and strong digital ecosystem maturity. The country benefits from extensive investments in edge computing, private 5G networks, and cloud-native telecom platforms. Strong demand from enterprises, hyperscale data centers, and OTT service providers is further driving growth. In addition, the presence of major players such as AT&T, Verizon, AWS, and Microsoft is reinforcing the U.S. leadership position in the global Telecom Cloud market.

Global Telecom Cloud Market Share

The telecom cloud industry is primarily led by well-established companies, including:

- AT&T Intellectual Property (U.S.)

- BT (U.K.)

- Verizon (U.S.)

- CenturyLink (U.S.)

- Telefonaktiebolaget LM Ericsson (Sweden)

- Deutsche Telekom AG (Germany)

- NTT Communications Corporation (Japan)

- Singtel (Singapore)

- Microsoft (U.S.)

- Epsilon Telecommunications Limited (U.K.)

- Logicalis Group (U.K.)

- Orange Business Services (France)

- Telstra Enterprise (Australia)

- Fusion Connect, Inc. (U.S.)

- ZTE Corporation (China)

- Vodafone Idea Limited (India)

- China Telecom Global Limited (China)

- TELUS (Canada)

- T-Mobile USA, Inc. (U.S.)

Latest Developments in Global Telecom Cloud Market

- In August 2025, Bharti Airtel’s Xtelify launch strengthened the Telecom Cloud market by introducing an integrated cloud platform combined with AI-powered solutions tailored for telecom operators and enterprise customers. The offering enhances cloud adoption by enabling scalable infrastructure-as-a-service (IaaS) and platform-as-a-service (PaaS) capabilities, supporting secure migration and flexible deployment across telecom networks. Through partnerships with Singtel, Globe Telecom, and Airtel Africa, the initiative expands cross-border telecom cloud interoperability and accelerates digital transformation in emerging markets, reinforcing Airtel’s position in the cloud-enabled telecom ecosystem

- In February 2024, Dell Technologies expanded its Telecom Cloud capabilities by launching enhanced solutions for communications service providers aimed at accelerating network cloud adoption and improving operational economics. These solutions support CSPs in simplifying deployment, automating network operations, and improving lifecycle management of distributed cloud infrastructure. The development strengthens telecom cloud modernization by enabling more efficient 5G network rollouts and improving infrastructure agility, thereby increasing demand for cloud-native telecom infrastructure across global operators

- In June 2023, Nokia Corporation partnered with Red Hat to integrate open-source cloud technologies such as Red Hat OpenShift and OpenStack into its telecom network applications, strengthening the Telecom Cloud ecosystem. This collaboration improves flexibility, scalability, and deployment efficiency for telecom operators by enabling cloud-native network functions and hybrid cloud architectures. The integration supports faster innovation in 5G network development and enhances the adoption of open telecom cloud frameworks across global service providers

- In February 2023, Snowflake Inc. launched its Telecom Data Cloud, strengthening the Telecom Cloud market by enabling industry-specific data analytics and real-time insights for telecom operators. The platform helps operators improve decision-making, optimize network performance, and enhance revenue generation through advanced data management capabilities. This development accelerates the shift toward data-driven telecom cloud ecosystems, supporting modernization of network operations and improving efficiency across telecom infrastructure

- In February 2023, Dell Technologies introduced Dell Telecom Infrastructure Blocks for Red Hat, enhancing telecom cloud deployment by enabling open and scalable network architectures for 5G and RAN applications. The solution simplifies infrastructure integration and supports faster deployment of cloud-native telecom networks, improving operational efficiency for service providers. This development strengthens the adoption of standardized telecom cloud infrastructure, accelerating virtualization and automation across global telecom networks

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.