Global Thermal Interface Materials Market

Market Size in USD Billion

USD

4.60 Billion

USD

11.38 Billion

2025

2033

USD

4.60 Billion

USD

11.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.60 Billion | |

| USD 11.38 Billion | |

| % | |

|

Thermal Interface Materials Market Overview

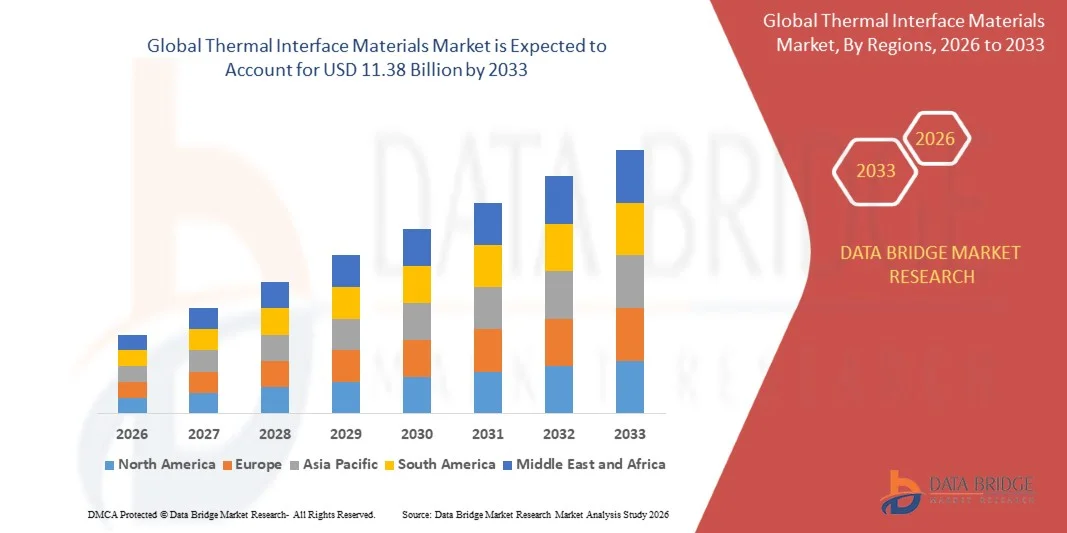

As per Data Bridge Market Research analysis the thermal interface materials market was valued at USD 4.60 billion in 2025 and is projected to reach USD 11.38 billion by 2033, growing at a CAGR of 12.00% from 2026 to 2033. The market is witnessing significant growth driven by increasing demand for efficient thermal management solutions across electronics, automotive, telecommunications, and data center applications. Rising adoption of high-performance computing systems, electric vehicles, advanced semiconductor devices, and compact electronic components is accelerating the need for materials that improve heat dissipation and enhance device reliability.

The growing complexity and miniaturization of electronic devices, along with increasing power density in processors and semiconductor components, are encouraging manufacturers to adopt advanced thermal interface materials such as thermal greases, pads, phase change materials, and gap fillers. The rapid expansion of artificial intelligence infrastructure, cloud computing, and electric mobility is further strengthening market demand as industries focus on improving energy efficiency, reducing overheating risks, and extending the operational lifespan of electronic systems.

Market Size & Forecast

- Market Value (2025): USD 4.60 Billion

- Expected Market Value (2033): USD 11.38 Billion

- Forecast CAGR (2026–2033): 12.00%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Key Market Trends & Insights

- Asia-Pacific dominated the thermal interface materials market with the largest revenue share of 39.8% in 2025, supported by rapid expansion of semiconductor manufacturing, consumer electronics production, electric vehicle manufacturing, and data center infrastructure across China, Japan, South Korea, India, and Taiwan.

- North America is expected to witness the fastest growth rate from 2026 to 2033, supported by the strong presence of semiconductor manufacturers, electric vehicle production, advanced electronics, and hyperscale data centers.

- The pads & gap fillers segment held the largest market revenue share in 2025, driven by increasing adoption in electric vehicle battery packs, power electronics, semiconductor devices, and high-performance computing systems. Pads and gap fillers are widely preferred due to their ability to accommodate surface irregularities, provide reliable thermal contact, and support automated manufacturing processes in automotive and electronics applications.

- The greases & pastes segment is projected to register the fastest growth at a CAGR from 2026 to 2033, driven by rising demand for high thermal conductivity solutions in processors, GPUs, data centers, and advanced electronic components. Thermal pastes provide efficient heat transfer between chips and heat sinks, making them essential for AI servers, gaming hardware, and semiconductor applications requiring improved thermal performance.

- The automotive electronics segment held the largest market revenue share of approximately in 2025, driven by the rapid growth of electric vehicle production, increasing integration of battery thermal management systems, and rising adoption of power electronics in modern vehicles. Thermal interface materials are extensively used in battery packs, inverters, onboard chargers, electric motors, and advanced driver assistance systems (ADAS) to efficiently dissipate heat, improve component reliability, enhance battery safety, and support fast-charging capabilities, making automotive the leading end-use segment in the thermal interface materials market.

- The data center & telecom segment is projected to register the fastest growth at a CAGR from 2026 to 2033, supported by rapid expansion of artificial intelligence workloads, cloud computing infrastructure, and high-performance servers. Increasing power consumption and heat generation from AI processors and networking equipment are accelerating adoption of advanced thermal interface solutions such as thermal pads, gap fillers, and liquid cooling-compatible materials.

Report Scope and Thermal Interface Materials Market Segmentation

|

Attributes |

Thermal Interface Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Thermal Interface Materials Market Trends

Trend: Growth In Advanced Thermal Management Solutions For High-Performance Computing And Electric Vehicle Applications

Increasing demand for efficient heat dissipation technologies across semiconductor, automotive, telecommunications, and data center industries is accelerating the adoption of advanced thermal interface materials (TIMs). The rapid increase in chip power density, artificial intelligence (AI) workloads, and electrification of transportation is creating significant thermal management challenges, encouraging industries to replace conventional heat transfer solutions with high-performance materials such as thermal greases, thermal pads, gap fillers, phase change materials, and electrically conductive interfaces.

In modern electric vehicles, manufacturers are integrating thermal interface materials into battery packs, power electronics, and charging systems to improve thermal conductivity, maintain stable operating temperatures, and enhance battery safety. For instance, in May 2026, Henkel AG & Co. KGaA introduced advanced thermal gap fillers and thermally conductive adhesives for electric vehicle battery applications, supporting improved heat dissipation and optimized battery assembly processes.

The rapid expansion of AI servers, high-performance computing infrastructure, and advanced semiconductor manufacturing is further increasing demand for thermal interface materials capable of handling higher heat flux levels. For instance, NVIDIA Corporation is promoting liquid-cooled AI data center architectures, increasing the need for advanced thermal materials that enable efficient heat transfer between high-power chips and cooling systems.

In addition, semiconductor manufacturers are adopting advanced packaging technologies that require efficient thermal management solutions to maintain chip reliability and performance. The increasing integration of thermal interface materials in EVs, AI infrastructure, consumer electronics, and industrial electronics is creating strong market growth opportunities for high-conductivity and low-resistance thermal materials.

Thermal Interface Materials Market Dynamics

Key Market Driver: Rising Demand For High-Performance Thermal Management In Electronics And Electric Vehicles

Industries worldwide are facing increasing requirements to improve energy efficiency, enhance device reliability, and manage rising heat generation from advanced electronic components. The continuous development of smaller semiconductor nodes, powerful processors, electric vehicle batteries, and high-density electronic systems is generating higher thermal loads, increasing demand for efficient thermal interface materials that improve heat transfer between components and cooling systems.

Automotive manufacturers are increasingly adopting TIMs in electric vehicle battery modules, power electronics, and motor systems to maintain optimal temperature conditions and improve vehicle performance. Similarly, consumer electronics and semiconductor industries are utilizing thermal interface materials to reduce overheating risks in processors, graphics processing units (GPUs), and compact electronic devices.

For instance, in May 2024, Henkel AG & Co. KGaA showcased its thermal management solutions at Battery Show Europe, including thermal gap fillers and thermally conductive adhesives designed for EV battery assembly and improved thermal performance. These solutions help manufacturers improve battery safety, reduce thermal resistance, and support next-generation battery designs.

Furthermore, the growth of artificial intelligence computing is accelerating adoption of advanced thermal management materials. Data centers require highly efficient cooling systems as AI processors generate significantly higher heat output compared with traditional computing hardware, creating new demand for high-performance thermal interface materials.

Key Restraint/Challenge: High Material Costs And Reliability Issues Under Extreme Operating Conditions

The thermal interface materials market faces challenges related to high production costs, material availability, and performance limitations in extreme environments. Advanced TIM formulations using materials such as graphite, silver, aluminum nitride, and other high-conductivity compounds require specialized manufacturing processes, increasing overall system costs compared with conventional thermal solutions.

In addition, maintaining consistent thermal performance over long operating periods remains challenging due to issues such as material degradation, pump-out effects, thermal cycling, and mechanical stress. These limitations are particularly significant in demanding applications such as electric vehicle batteries, aerospace electronics, industrial machinery, and high-performance computing systems.

For instance, in May 2024, Henkel AG & Co. KGaA showcased advanced thermal management materials for electric vehicle battery applications, highlighting the need for thermally conductive adhesives and gap fillers capable of handling mechanical stress, vibration, and temperature fluctuations in next-generation battery designs. These challenges increase the complexity of TIM formulation and raise manufacturing costs for high-performance applications.

Key Market Opportunity: Expansion Of Electric Vehicles, AI Data Centers, And Advanced Semiconductor Packaging

The increasing adoption of electric vehicles, artificial intelligence infrastructure, and advanced semiconductor technologies is creating significant growth opportunities for thermal interface material manufacturers. Modern electronic systems require compact, lightweight, and highly efficient thermal management solutions to handle increasing power densities while maintaining reliability and operational efficiency.

Electric vehicle manufacturers are increasingly incorporating thermal interface materials into battery packs, inverter systems, and power electronics to improve temperature control and enable faster charging capabilities.

The expansion of AI-powered computing infrastructure is also creating new opportunities for high-performance thermal interface materials. For instance, NVIDIA Corporation is advancing liquid cooling solutions for AI factories as next-generation processors require improved thermal management capabilities. These developments are expected to increase demand for advanced thermal interface materials used between processors, cooling plates, and heat spreaders.

In addition, innovations in graphene-based thermal materials, phase change materials, and next-generation polymer composites are expected to improve thermal conductivity and reliability, expanding applications across aerospace, telecommunications, automotive electronics, and high-performance computing markets. The growing need for efficient heat management in compact and power-intensive systems is expected to create long-term opportunities for advanced thermal interface material solutions.

Thermal Interface Materials Market Scope

The market is segmented on the basis of type and end-use application.

- By Type

On the basis of type, the thermal interface materials market is segmented into tapes & films, metal, pads & gap fillers, greases & pastes, and others. The pads & gap fillers segment held the largest market revenue share in 2025, driven by increasing adoption in electric vehicle battery packs, power electronics, semiconductor devices, and high-performance computing systems. Pads and gap fillers are widely preferred due to their ability to accommodate surface irregularities, provide reliable thermal contact, and support automated manufacturing processes in automotive and electronics applications.

The greases & pastes segment is projected to register the fastest growth at a CAGR from 2026 to 2033, driven by rising demand for high thermal conductivity solutions in processors, GPUs, data centers, and advanced electronic components. Thermal pastes provide efficient heat transfer between chips and heat sinks, making them essential for AI servers, gaming hardware, and semiconductor applications requiring improved thermal performance.

- By End-use

On the basis of end-use, the thermal interface materials market is segmented into automotive, consumer electronics, data center & telecom, industrial & energy, and others. The automotive electronics segment held the largest market revenue share of approximately in 2025, driven by the rapid growth of electric vehicle production, increasing integration of battery thermal management systems, and rising adoption of power electronics in modern vehicles. Thermal interface materials are extensively used in battery packs, inverters, onboard chargers, electric motors, and advanced driver assistance systems (ADAS) to efficiently dissipate heat, improve component reliability, enhance battery safety, and support fast-charging capabilities, making automotive the leading end-use segment in the thermal interface materials market.

The data center & telecom segment is projected to register the fastest growth at a CAGR from 2026 to 2033, supported by rapid expansion of artificial intelligence workloads, cloud computing infrastructure, and high-performance servers. Increasing power consumption and heat generation from AI processors and networking equipment are accelerating adoption of advanced thermal interface solutions such as thermal pads, gap fillers, and liquid cooling-compatible materials.

Thermal Interface Materials Market Regional Analysis

Asia-Pacific Thermal Interface Materials Market Insight

The Asia-Pacific dominated the thermal interface materials market with the largest revenue share of 39.8% in 2025, supported by rapid expansion of semiconductor manufacturing, consumer electronics production, electric vehicle manufacturing, and data center infrastructure across China, Japan, South Korea, India, and Taiwan. Rising investments in AI technologies, 5G deployment, and advanced packaging technologies are significantly increasing demand for high-performance thermal interface materials. The region's strong electronics manufacturing base and cost-effective production capabilities further support market growth.

Japan Thermal Interface Materials Market Insight

The Japan thermal interface materials market is expected to witness significant growth from 2026 to 2033 due to the country's strong semiconductor industry, advanced automotive sector, and leadership in precision electronic manufacturing. Increasing investments in next-generation semiconductor packaging, electric vehicles, robotics, and industrial automation are driving demand for high-performance thermal interface materials. The growing focus on miniaturized electronic devices and energy-efficient thermal management technologies is further supporting market expansion.

China Thermal Interface Materials Market Insight

The China thermal interface materials market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's dominant semiconductor packaging industry, expanding electric vehicle production, and large-scale consumer electronics manufacturing. China continues to invest heavily in AI computing infrastructure, battery manufacturing, and domestic semiconductor production, significantly increasing demand for advanced thermal management materials. Strong government support for high-tech manufacturing and the presence of leading electronics and EV manufacturers continue to position China as the largest regional market for thermal interface materials.

North America Thermal Interface Materials Market Insight

North America is expected to witness the fastest growth rate from 2026 to 2033, supported by the strong presence of semiconductor manufacturers, electric vehicle production, advanced electronics, and hyperscale data centers. The region benefits from continuous investments in AI computing infrastructure, 5G deployment, and high-performance computing technologies, all of which require efficient thermal management solutions. Growing adoption of electric vehicles and increasing demand for advanced battery thermal management systems further strengthen the demand for thermal interface materials across automotive and industrial applications.

U.S. Thermal Interface Materials Market Insight

The U.S. thermal interface materials market captured the largest revenue share in 2025 within North America, fueled by rapid expansion of AI data centers, semiconductor manufacturing, and electric vehicle production. Increasing investments in advanced chip packaging, cloud computing infrastructure, and defense electronics are accelerating demand for high-performance thermal interface materials. Moreover, the presence of leading technology companies, growing deployment of liquid-cooled AI servers, and increasing adoption of EV battery thermal management systems continue to drive market growth across the country.

Canada Thermal Interface Materials Market Insight

The Canada thermal interface materials market is expected to witness substantial growth from 2026 to 2033, driven by increasing investments in electric vehicle battery manufacturing, clean energy technologies, advanced electronics, and data center infrastructure. The country's growing focus on electrification, supported by government incentives for zero-emission vehicles and domestic battery supply chain development, is accelerating demand for thermal interface materials used in battery packs, power electronics, and charging systems. Furthermore, expanding semiconductor research, renewable energy projects, and the presence of major battery manufacturing investments are expected to boost the adoption of high-performance thermal management materials across automotive, industrial, and energy applications.

Europe Thermal Interface Materials Market Insight

The Europe thermal interface materials market is expected to witness significant growth from 2026 to 2033, primarily driven by accelerating electric vehicle adoption, stringent vehicle emission regulations, and increasing investments in semiconductor and industrial automation technologies. Rising deployment of renewable energy systems, power electronics, and advanced manufacturing facilities is creating sustained demand for efficient thermal management materials. Growing emphasis on sustainable mobility and energy-efficient electronics is further supporting market expansion across the region.

U.K. Thermal Interface Materials Market Insight

The U.K. thermal interface materials market is expected to witness notable growth from 2026 to 2033, driven by increasing investments in electric vehicle manufacturing, battery innovation, aerospace technologies, and AI-enabled computing infrastructure. Expanding research activities in advanced materials and growing adoption of high-performance electronics are increasing the demand for thermally conductive adhesives, gap fillers, and thermal pads. The country's focus on next-generation semiconductor technologies is expected to further support market growth.

Germany Thermal Interface Materials Market Insight

The Germany thermal interface materials market is expected to witness strong growth from 2026 to 2033, fueled by the country's leadership in automotive manufacturing, industrial automation, and advanced engineering. Increasing production of electric vehicles, battery systems, and power electronics is driving widespread adoption of thermal interface materials for improved heat dissipation and system reliability. Germany's strong semiconductor ecosystem and emphasis on high-quality manufacturing continue to accelerate demand for advanced thermal management solutions.

Thermal Interface Materials Market Share

The Thermal Interface Materials industry is primarily led by well-established companies, including:

- 3M (U.S.)

- Henkel AG & Co. KGaA (Germany)

- Parker Hannifin Corporation (U.S.)

- Dow Inc. (U.S.)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Indium Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- Fujipoly Ltd. (Japan)

- Wacker Chemie AG (Germany)

- Momentive Performance Materials Inc. (U.S.)

- Laird Performance Materials (U.K.)

- Boyd Corporation (U.S.)

- DuPont (U.S.)

- Aavid Thermalloy (Boyd Corporation) (U.S.)

- Denka Company Limited (Japan)

Latest Developments in Thermal Interface Materials Market

- In December 2025, Henkel AG & Co. KGaA launched BERGQUIST TGF 10000, a high-performance 10 W/mK liquid thermal gap filler designed for automotive electronics, telecommunications, computing, and network infrastructure applications. The new material improves heat transfer between electronic components while enabling automated dispensing and manufacturing efficiency. It supports next-generation high-power electronic systems requiring enhanced thermal reliability and long-term performance. The launch strengthens Henkel's thermal management portfolio and accelerates innovation in high-density electronics and EV applications.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Thermal Interface Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Thermal Interface Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Thermal Interface Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.