Global Third Party Banking Software Market

Market Size in USD Billion

USD

36.90 Billion

USD

65.81 Billion

2025

2033

USD

36.90 Billion

USD

65.81 Billion

2025

2033

| 2026 - 2033 | |

| USD 36.90 Billion | |

| USD 65.81 Billion | |

| % | |

|

Third-Party Banking Software Market Overview

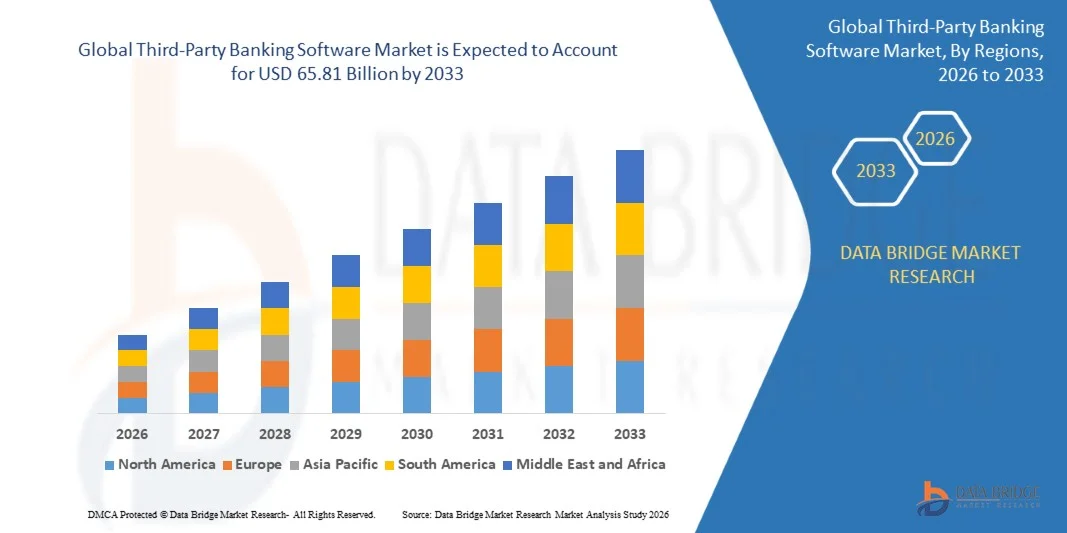

As per Data Bridge Market Research Analysis the third-party banking software market was valued at USD 36.9 billion in 2025 and is projected to reach USD 65.81 billion by 2033, registering a CAGR of 7.50% during the forecast period. The market is expanding as banks and financial institutions continue investing in digital transformation initiatives to improve operational efficiency, modernize legacy infrastructure, reduce operating costs, and deliver enhanced customer experiences. Growing regulatory requirements, increasing cloud adoption, and demand for secure digital banking solutions are further supporting market growth.

Third-party banking software comprises technology platforms developed by independent software vendors to support banks and financial institutions in managing core operations, improving customer engagement, strengthening regulatory compliance, and enhancing operational efficiency. These solutions include core banking, digital banking, payment processing, risk management, analytics, and wealth management applications. Organizations increasingly adopt third-party platforms because they reduce development time, improve scalability, and provide access to advanced technologies.

Market Size & Forecast

- Market Value (2025): USD 36.9 Billion

- Expected Market Value (2033): USD 65.81 Billion

- Forecast CAGR (2026–2033): 7.50%

- Leading Region in 2025: Europe

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- Europe accounts for the largest share of the market due to advanced banking infrastructure, widespread digital transformation initiatives, and supportive regulatory policies such as PSD2, which encourage open banking and third-party software integration. Germany, the UK, France, and the Netherlands lead this transformation, with ongoing upgrades to legacy systems to align with digital-first models. Europe accounted for approximately 36.6% of the market share in 2024.

- North America holds a significant market position with high adoption rates, driven by the increasing digital transformation in the banking sector and the presence of major software vendors. The U.S. core banking software market was estimated at US$3.0 billion in 2025.

- Asia-Pacific is expected to witness the fastest growth during the forecast period, driven by rapid digital transformation, strong economic growth, financial inclusion efforts, and increasing demand for digital banking services across countries such as China, India, and Southeast Asian nations. China is forecast to reach a projected market size of US$7.3 billion by 2032, trailing a CAGR of 21.7%.

- The core banking software segment accounts for a major share of the market as banks continue replacing legacy platforms with modern systems that improve transaction processing, customer account management, and regulatory compliance. The core banking software market was valued at USD 19.67 billion in 2025.

- The cloud deployment segment is witnessing strong growth as banks increasingly embrace cloud technology for agility, fintech integration, and enhanced service delivery. Cloud platforms offer flexible, cost-effective, and scalable solutions, enabling banks to boost efficiency and transition from outdated systems.

- Ai-powered banking solutions are emerging as a transformative trend, with financial institutions integrating ai and automation technologies into banking systems to enhance decision-making capabilities and enable smarter choices. The increasing adoption of ai-powered banking solutions, rising investment in cybersecurity platforms, and the expansion of open banking ecosystems are expected to drive market growth.

Report Scope and Third-Party Banking Software Market Segmentation

|

Attributes |

Third-Party Banking Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Third-Party Banking Software Market Trends

Trend: AI-Powered Banking and Automation

The integration of artificial intelligence and automation technologies into banking systems is a defining trend reshaping the market. AI-powered banking enhances decision-making capabilities and enables smarter choices, offering personalized customer experiences with reduced manual intervention. Financial institutions are increasingly adopting AI for fraud detection, customer service automation, and predictive analytics. For instance, in March 2025, NatWest integrated OpenAI into its digital assistants Cora and AskArchie to bolster fraud prevention and enhance customer service, leading to a 150% rise in customer satisfaction. This trend is expected to accelerate as banks seek to improve operational efficiency and customer engagement.

Third-Party Banking Software Market Dynamics

Key Market Driver: Rising Cybersecurity Threats

The growing frequency and sophistication of cyberattacks are encouraging financial institutions to invest in advanced banking software that strengthens security, fraud detection, regulatory compliance, and continuous monitoring of digital banking operations. This rise in cyberattacks is fueled by the growing digitalization of data and services, which expands the attack surface and creates more opportunities for cybercriminals to exploit vulnerabilities. Third-party banking software helps mitigate cyber threats by providing banks with access to advanced security technologies, continuous monitoring, and enhanced protection, ensuring swift responses to emerging threats. For example, a report from June 2025 by the UK's Department for Science, Innovation and Technology noted a significant increase in ransomware incidents among businesses, with affected cases rising from less than 0.5% in 2024 to 1% in 2025.

Key Restraint/Challenge: Data Security and Privacy Concerns

A significant challenge facing the third-party banking software market is the increasing concerns over data security and privacy. Since banking software frequently integrates with multiple external vendors and cloud platforms, financial institutions face increasing concerns regarding third-party security risks, data privacy, regulatory compliance, and vendor management. These factors can slow software adoption, particularly among institutions handling highly sensitive financial information. Additionally, concerns regarding privacy and security among enterprises are increasing, which is anticipated to restrain market expansion.

Key Market Opportunity: Cloud-Based Banking Platforms

Cloud technology is revolutionizing the third-party banking software market, presenting tremendous opportunities for growth. Cloud platforms provide flexible, cost-effective, and scalable solutions, enabling banks to boost efficiency, transition from outdated systems, and better meet digital demands. Banks increasingly embrace the cloud for agility, fintech integration, and enhanced service delivery. For example, in April 2025, nCino, a cloud-native banking software provider, grew its global presence by acquiring DocFox, FullCircl, and Sandbox Banking between 2024 and early 2025. By 2025, nCino will serve more than 2,700 banks globally, including TD Bank and Santander. Cloud platforms offer faster updates, improved cybersecurity, and easier compliance, while supporting APIs, AI, and data analytics for smart banking features.

Third-Party Banking Software Market Scope

The third-party banking software market is segmented on the basis of product, deployment, application, end use, and region.

- By Product

On the basis of product, the third-party banking software market is segmented into core banking software, omnichannel banking software, business intelligence software, wealth management software, and others. Core banking software accounts for a major share of the market as banks continue replacing legacy platforms with modern systems that improve transaction processing, customer account management, and regulatory compliance. The global core banking software market was valued at USD 19.67 billion in 2025 and is projected to grow substantially. Omnichannel banking software is gaining traction as banks seek to provide seamless customer experiences across multiple channels. Business intelligence software is increasingly adopted for data-driven decision-making and analytics.

- By Deployment

On the basis of deployment, the third-party banking software market is segmented into on-premises and cloud. The cloud segment is projected to experience the fastest growth, as banks increasingly embrace cloud technology for agility, fintech integration, and enhanced service delivery. Cloud platforms offer flexible, cost-effective, and scalable solutions, enabling banks to boost efficiency and transition from outdated systems. The on-premises segment currently holds a significant market share, preferred by organizations that require high data security and control. However, the cloud segment is expected to witness significant growth during the forecast period, driven by increasing adoption of cloud computing technologies and the need for real-time data access.

- By Application

On the basis of application, the third-party banking software market is segmented into risk management, information security, and business intelligence. Risk management applications are critical for banks to navigate complex regulatory landscapes and ensure compliance. Information security applications are increasingly important as cybersecurity threats continue to rise. Business intelligence applications enable data-driven decision-making and analytics, helping banks improve operational efficiency and customer experience.

- By End Use

On the basis of end use, the third-party banking software market is segmented into retail banks and commercial banks. Retail banks represent a significant market segment, driven by the need for digital banking solutions, mobile applications, and personalized customer experiences. Commercial banks are also major adopters, seeking to enhance operational efficiency, improve risk management, and ensure regulatory compliance.

- By Region

On the basis of region, the third-party banking software market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Europe remains the leader, supported by a mature financial landscape and progressive regulations. North America holds a significant market position with high adoption rates. Asia-Pacific is expected to witness the fastest growth during the forecast period.

Third-Party Banking Software Market Regional Analysis

Europe Third-Party Banking Software Market Insight

Europe continues to lead the market due to strong digital banking adoption, supportive regulatory initiatives, extensive modernization of banking infrastructure, and the presence of leading banking technology providers. Germany, the UK, France, and the Netherlands lead this transformation, with ongoing upgrades to legacy systems to align with digital-first models. Germany and the UK stand out due to their active fintech ecosystems and strong IT capabilities. UK banks have widely adopted third-party tools for real-time payments, mobile apps, and AI-powered services. The region accounted for approximately 36.6% of the market share in 2024.

North America Third-Party Banking Software Market Insight

North America holds a significant market position with high adoption rates, driven by the increasing digital transformation in the banking sector and the presence of major software vendors. The U.S. core banking software market was estimated at US$3.0 billion in 2025. The region is characterized by mature enterprise software ecosystems and significant investments in AI-enabled banking solutions. Organizations in North America are at the forefront of adopting advanced banking capabilities, including AI-powered fraud detection, real-time payment processing, and cloud-based infrastructure.

Asia-Pacific Third-Party Banking Software Market Insight

Asia-Pacific is expected to witness the fastest growth in the third-party banking software market, driven by rapid digital transformation, strong economic growth, and financial inclusion efforts. The region's expanding banking sector and increasing demand for digital banking services are supporting market expansion. China is forecast to reach a projected market size of US$7.3 billion by 2032, trailing a CAGR of 21.7%. India's market is evolving in response to the rapid growth of digital banking and fintech adoption, with organizations increasingly recognizing the need for robust software solutions.

Middle East & Africa Third-Party Banking Software Market Insight

The Middle East and Africa region represents an emerging market for third-party banking software, with demand primarily concentrated in the Gulf Cooperation Council (GCC) countries and South Africa. Governments across the region are increasing investments in digital infrastructure and technology sectors to diversify their economies. The UAE and Saudi Arabia are investing in smart city initiatives and digital transformation programs, creating opportunities for banking software applications. However, relatively low adoption of advanced technologies and limited digital infrastructure continue to restrain market growth in certain parts of the region.

South America Third-Party Banking Software Market Insight

South America represents an emerging market for third-party banking software, with growing demand influenced by increasing digitalization of business operations, rising fintech adoption, and expanding banking services. Brazil dominates the Latin American market, driven by the country's large economy, growing fintech sector, and increasing government focus on digital transformation. However, market growth is currently constrained by limited digital infrastructure, budget constraints, and economic volatility compared to more developed regions.

Third-Party Banking Software Market Share

The third-party banking software industry is primarily led by well-established companies, including:

- Oracle Corporation (U.S.)

- Tata Consultancy Services (India)

- Temenos Group (Switzerland)

- Nucleus Software (India)

- FIS Group (U.S.)

- Fiserv (U.S.)

- Jack Henry & Associates (U.S.)

- Path Solutions (Kuwait)

- Misys (U.K.)

- Sopra Banking Software (France)

- Infosys (India)

- SAP SE (Germany)

- Sungard Ambit (U.S.)

- Polaris Financial Technology (India)

- Diasoft Software Solutions (Russia)

- nCino (U.S.)

- Capgemini Services SAS (France)

- Fidelity National Information Services (U.S.)

- Finastra (U.K.)

- Backbase (Netherlands)

- Mambu (Germany)

- Thought Machine (U.K.)

Latest Developments in Third-Party Banking Software Market

- In August 2025, CSI, a leading core banking provider, announced the acquisition of digital banking provider Apiture. The acquisition is part of CSI's strategy to integrate core banking, digital banking, customer engagement, and lending into a single platform for community banks and credit unions. Apiture's platform includes account onboarding, open banking, and data analytics capabilities, enabling CSI to deliver an "integrated ecosystem of technologies" for financial institutions. Financial details of the deal were not disclosed, and the acquisition was expected to be finalized in the fourth quarter of 2025.

- In November 2025, nCino announced the acquisition of Sandbox Banking, a digital transformation leader serving the financial services industry. The acquisition strengthens nCino's ability to enhance data connectivity and streamline operations for banks and credit unions through an industry-leading Integration Platform as a Service (iPaaS) solution. This acquisition gives nCino a better ability to empower institutions with a flexible, reliable data environment for greater agility to quickly integrate third-party systems, AI, and new technologies without disruptions.

- In September 2025, FIS completed its acquisition of Amount, a leading provider of unified digital banking origination and decisioning experiences for financial institutions. With more than 150 million new account applications processed, Amount provides a best-in-class digital account opening experience for consumers and small businesses across lending, cards, and deposits. Its cloud-native, unified solution with embedded AI functionality simplifies the online account opening experience. The acquisition aligns with FIS's strategy to add innovative, cloud-native, and modular solutions across the world's money lifecycle.

- In October 2025, UST, a leading AI and technology transformation solutions company, acquired Modus Information Systems Private Limited, a core banking implementation partner serving banks in India and across the broader Global South. This strategic move strengthens UST's position in the financial sector and equips it to serve emerging markets. The acquisition aligns with UST's Banking-as-a-Service utility offering, BanktrUST, and represents a step forward in building a robust global financial services practice. Modus brings deep expertise in implementing industry-leading core banking solutions with a team of approximately 340 skilled professionals.

- In November 2025, RUGR announced the acquisition of Saraswat Infotech Private Limited (SIPL), one of the leading banking technology providers in India. This acquisition brings together SIPL's trusted legacy in the BFSI industry with RUGR's AI-powered and cloud-based ecosystem, allowing banks to enhance their operations using scalable and compliant technologies. The collaboration was showcased at the Global Fintech Fest 2025 with the launch of RUGR Udaan, a connected banking solution designed for merchant payouts and payroll processing.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.