Global Threat Hunting Market

Market Size in USD Billion

USD

4.87 Billion

USD

16.52 Billion

2025

2033

USD

4.87 Billion

USD

16.52 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.87 Billion | |

| USD 16.52 Billion | |

| % | |

|

Threat Hunting Market Size

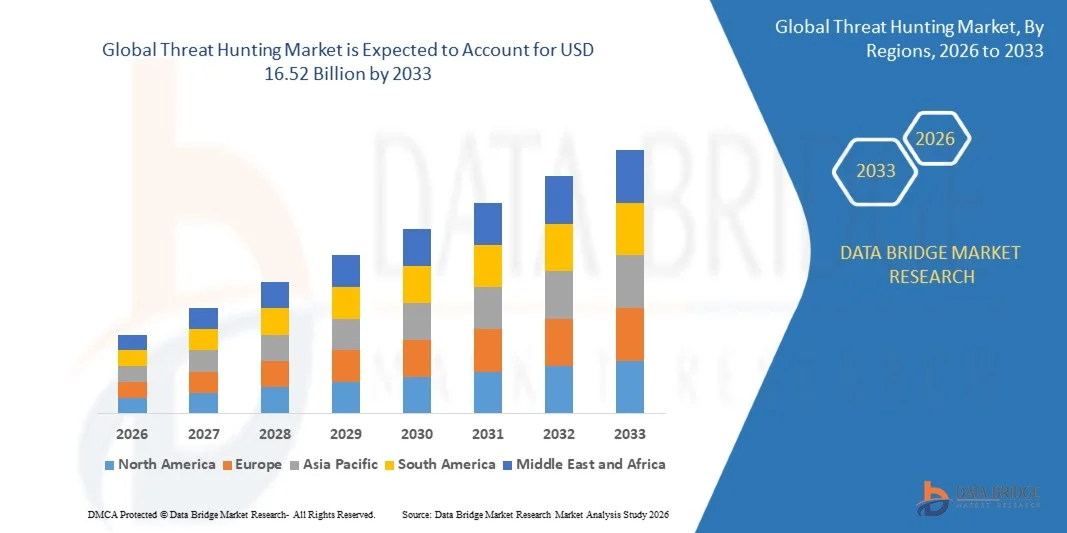

- The global threat hunting market size was valued at USD 4.87 billion in 2025 and is expected to reach USD 16.52 billion by 2033, at a CAGR of 16.50% during the forecast period

- The market growth is largely fuelled by the increasing frequency and sophistication of cyberattacks, growing adoption of advanced threat detection tools, and rising awareness of proactive cybersecurity measures among enterprises

- Rising demand for automated threat detection solutions and integration of artificial intelligence (AI) and machine learning (ML) in cybersecurity strategies are further driving market expansion

Threat Hunting Market Analysis

- The market is witnessing significant investments from enterprises in advanced threat hunting solutions to protect critical data and prevent security breaches

- Increasing regulatory compliance requirements and the adoption of cloud computing and IoT technologies are pushing organizations to enhance threat detection capabilities

- North America dominated the threat hunting market with the largest revenue share of 38.7% in 2025, driven by the increasing frequency of cyberattacks, high adoption of advanced cybersecurity solutions, and growing awareness of proactive threat detection strategies

- Asia-Pacific region is expected to witness the highest growth rate in the global threat hunting market, driven by increasing internet penetration, expanding IT and telecom sectors, and rising adoption of AI- and ML-based cybersecurity solutions

- The Cloud-Based segment held the largest market revenue share in 2025, driven by enterprises seeking scalable, flexible solutions that can be rapidly deployed across global locations. Cloud-based threat hunting enables continuous monitoring, automated updates, and integration with other cybersecurity tools, reducing operational complexity. The adoption is further fueled by the growing shift toward remote work, multi-cloud environments, and advanced analytics to detect evolving threats in real time

Report Scope and Threat Hunting Market Segmentation

|

Attributes |

Threat Hunting Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Rising Adoption Of AI-Powered Threat Hunting Solutions |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Threat Hunting Market Trends

“Rising Adoption of Proactive Cybersecurity Measures”

• The increasing frequency and sophistication of cyberattacks is significantly shaping the threat hunting market, as organizations prioritize proactive detection and mitigation strategies. Threat hunting tools enable IT security teams to identify hidden threats, anomalous behavior, and potential breaches before they escalate, strengthening overall enterprise cybersecurity posture. This trend drives adoption across finance, healthcare, IT, and government sectors, encouraging providers to develop advanced detection algorithms and automation capabilities

• Growing awareness around data privacy, regulatory compliance, and risk management has accelerated demand for threat hunting solutions in enterprise and cloud environments. Organizations are increasingly implementing threat hunting practices to detect insider threats, advanced persistent threats (APTs), and ransomware attacks. This focus promotes collaboration between cybersecurity vendors and enterprises to enhance detection capabilities and reduce incident response times

• Integration with AI, machine learning, and Security Information and Event Management (SIEM) systems is influencing purchasing decisions, enabling predictive analytics and intelligent threat prioritization. Companies leverage these integrations to optimize resource allocation and improve operational efficiency, while also ensuring compliance with industry standards and regulatory mandates

• For instance, in 2024, CrowdStrike in the U.S. and Darktrace in the U.K. expanded their threat hunting offerings by incorporating AI-driven analytics and cloud-based monitoring solutions. These launches were aimed at providing real-time threat visibility and predictive insights to enterprises, enhancing operational resilience and reducing financial and reputational risks

• While demand for threat hunting solutions is growing, sustained market expansion depends on continuous R&D, integration with existing cybersecurity infrastructure, and cost-effective deployment models. Vendors are focusing on enhancing automation, improving threat intelligence feeds, and developing scalable cloud-based solutions to support broader adoption

Threat Hunting Market Dynamics

Driver

“Rising Adoption of Proactive Cybersecurity and AI-Driven Analytics”

• Organizations are increasingly deploying threat hunting tools to proactively detect and mitigate cyber threats before they impact operations. The integration of AI and machine learning improves threat identification and reduces manual investigation efforts, driving demand across enterprises globally

• Expanding digital transformation initiatives, cloud adoption, and remote work models are fueling market growth. Enterprises require continuous monitoring and advanced threat detection capabilities to secure hybrid IT environments, prompting investments in sophisticated threat hunting platforms

• Cybersecurity vendors are promoting threat hunting solutions through managed services, training, and real-time monitoring capabilities. This is further supported by regulatory compliance requirements and increased spending on security infrastructure to protect sensitive data and critical assets

• For instance, in 2023, Palo Alto Networks in the U.S. and FireEye in the U.K. reported enhanced adoption of their threat hunting solutions among enterprise clients, focusing on automated threat detection, incident response, and compliance management. These implementations led to faster detection of advanced threats and minimized potential operational disruptions

• Although proactive cybersecurity adoption supports market growth, wider implementation depends on the availability of skilled cybersecurity professionals, integration with legacy systems, and cost considerations. Investments in automation, training, and cloud-native solutions will be critical for meeting global demand and sustaining competitive advantage

Restraint/Challenge

“Limited Skilled Workforce and High Implementation Costs”

• The scarcity of trained cybersecurity professionals with expertise in threat hunting remains a key challenge, slowing adoption in organizations with limited IT security capabilities. Shortage of personnel for monitoring, analyzing, and responding to alerts can impact the effectiveness of threat hunting initiatives

• High costs associated with advanced threat hunting solutions, including AI-driven platforms, cloud deployments, and continuous monitoring, limit adoption among small and medium-sized enterprises (SMEs). Budget constraints and the complexity of integrating new tools with existing IT infrastructure present additional barriers

• Organizational awareness and understanding of proactive threat hunting practices are uneven, particularly in emerging economies. Limited knowledge of functional benefits restricts adoption across certain industries and IT environments

• For instance, in 2024, SMEs in India and Brazil reported slower uptake of advanced threat hunting services due to budget limitations, lack of skilled personnel, and minimal awareness of operational benefits. Organizations often relied on reactive cybersecurity measures instead of investing in proactive threat detection

• Overcoming these challenges requires cost-efficient solutions, expanded training programs, and managed service offerings to support organizations with limited expertise. Collaboration with industry bodies, cybersecurity training institutes, and cloud service providers can help unlock the long-term growth potential of the global threat hunting market

Threat Hunting Market Scope

The threat hunting market is segmented on the basis of deployment type, target environment, service type, industry, and tier.

• By Deployment Type

On the basis of deployment type, the threat hunting market is segmented into On-Premises, Cloud-Based, and Hybrid. The Cloud-Based segment held the largest market revenue share in 2025, driven by enterprises seeking scalable, flexible solutions that can be rapidly deployed across global locations. Cloud-based threat hunting enables continuous monitoring, automated updates, and integration with other cybersecurity tools, reducing operational complexity. The adoption is further fueled by the growing shift toward remote work, multi-cloud environments, and advanced analytics to detect evolving threats in real time.

The On-Premises segment is expected to witness the fastest growth rate from 2026 to 2033, as organizations in highly regulated industries prefer full control over their security infrastructure and sensitive data. On-premises deployments allow for customized threat hunting strategies, in-depth forensic analysis, and direct integration with internal systems. Organizations focusing on data privacy, regulatory compliance, and low-latency threat response are increasingly adopting on-premises solutions, making it a key growth area.

• By Target Environment

On the basis of target environment, the market is segmented into Network, Cloud, Endpoint, and Hybrid. The Endpoint segment held the largest revenue share in 2025 due to the proliferation of endpoint devices such as laptops, smartphones, IoT devices, and servers, which are frequent targets for malware and ransomware. Endpoint threat hunting helps organizations proactively detect anomalies, prevent breaches, and secure distributed IT environments. Increasing remote work and device connectivity are further driving the adoption of endpoint-focused solutions.

The Cloud segment is expected to witness the fastest growth from 2026 to 2033, as businesses migrate applications and data to public, private, and hybrid cloud platforms. Cloud threat hunting offers visibility across dynamic cloud workloads, automated detection of misconfigurations, and rapid response to potential security incidents. The rising adoption of SaaS and cloud-native applications, coupled with regulatory requirements for data protection, is accelerating growth in this segment.

• By Service Type

On the basis of service type, the market is segmented into Managed, Professional, and Support services. The Managed segment accounted for the largest market share in 2025, as organizations increasingly rely on external experts for 24/7 monitoring, threat intelligence, and incident response. Managed services reduce the need for extensive in-house cybersecurity teams and provide access to advanced tools and analytics, ensuring continuous protection against sophisticated cyber threats.

The Professional segment is expected to register the fastest growth from 2026 to 2033, driven by increasing demand for expert consulting, strategic implementation, and training services. Organizations are leveraging professional threat hunting services to strengthen internal cybersecurity capabilities, improve threat detection frameworks, and achieve compliance with global regulations. These services also support tailored deployment strategies and integration with existing security operations.

• By Industry

On the basis of industry, the threat hunting market is segmented into IT and Telecom, BFSI, Healthcare, Retail, and Manufacturing. The BFSI segment held the largest market share in 2025 due to the critical need to safeguard financial systems and customer data from highly sophisticated cyberattacks. Banks, insurance companies, and financial institutions are investing heavily in proactive threat detection, continuous monitoring, and real-time analytics to prevent breaches, financial losses, and reputational damage.

The Healthcare segment is expected to witness the fastest growth from 2026 to 2033, as hospitals, clinics, and research centers increasingly adopt electronic health records (EHRs) and connected medical devices. Rising cyber threats targeting patient data, critical healthcare infrastructure, and pharmaceutical research are fueling demand for advanced threat hunting solutions. Regulatory compliance requirements, such as HIPAA and GDPR, also encourage healthcare organizations to implement robust cybersecurity strategies.

• By Tier

On the basis of tier, the market is segmented into Tier 1, Tier 2, and Tier 3 organizations. The Tier 1 segment held the largest revenue share in 2025, as large enterprises with complex IT environments invest significantly in proactive threat detection and response systems. These organizations prioritize minimizing operational disruptions, securing critical assets, and protecting sensitive customer and financial data from advanced persistent threats (APTs).

The Tier 2 segment is expected to witness the fastest growth rate from 2026 to 2033, driven by mid-sized enterprises adopting cost-effective threat hunting solutions. Tier 2 organizations are increasingly implementing hybrid and managed models to optimize security budgets while maintaining robust protection. Growth is supported by rising cyberattacks targeting mid-market businesses, increasing awareness of cybersecurity risks, and the need for scalable solutions that grow with organizational needs.

Threat Hunting Market Regional Analysis

• North America dominated the threat hunting market with the largest revenue share of 38.7% in 2025, driven by the increasing frequency of cyberattacks, high adoption of advanced cybersecurity solutions, and growing awareness of proactive threat detection strategies

• Organizations in the region are prioritizing threat hunting to safeguard critical IT infrastructure, cloud environments, and sensitive data, while reducing the risk of financial and reputational losses

• The widespread adoption is further supported by well-established IT infrastructure, regulatory compliance requirements, and increasing investments in cybersecurity technologies, establishing threat hunting as a critical solution across enterprises

U.S. Threat Hunting Market Insight

The U.S. threat hunting market captured the largest revenue share in 2025 within North America, fueled by the rapid digital transformation of enterprises and the rising sophistication of cyber threats. Organizations are increasingly implementing threat hunting frameworks to proactively identify anomalies and mitigate security breaches. The demand for real-time threat detection, AI-powered analytics, and cloud-based monitoring is further driving market growth. Moreover, the integration of threat hunting with managed security services and regulatory compliance initiatives is significantly contributing to expansion.

Europe Threat Hunting Market Insight

The Europe threat hunting market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict data protection regulations such as GDPR and the increasing need for advanced cybersecurity measures. Rising adoption of cloud computing and digital services across SMEs and large enterprises is fostering market demand. European organizations are also investing in skilled cybersecurity professionals and automated threat detection tools. The growth is particularly strong across BFSI, healthcare, and manufacturing sectors, with threat hunting becoming a key component of enterprise security strategies.

U.K. Threat Hunting Market Insight

The U.K. threat hunting market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing cybercrime incidents and rising awareness about proactive threat detection. Organizations are adopting hybrid and cloud-based threat hunting solutions to secure critical infrastructure and sensitive data. The country’s strong IT and telecom sector, coupled with robust regulatory frameworks, is accelerating the implementation of threat hunting platforms. Increasing investments in AI and machine learning for automated threat detection are further boosting market expansion.

Germany Threat Hunting Market Insight

The Germany threat hunting market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for cybersecurity solutions in manufacturing and industrial sectors. Germany’s emphasis on Industry 4.0, connected devices, and secure digital ecosystems promotes adoption. Organizations are integrating threat hunting with endpoint, network, and cloud monitoring solutions to prevent advanced persistent threats. The country’s focus on cybersecurity innovation and regulatory compliance enhances enterprise confidence in proactive threat management solutions.

Asia-Pacific Threat Hunting Market Insight

The Asia-Pacific threat hunting market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing digitization, rapid adoption of cloud services, and rising cybercrime in countries such as China, Japan, and India. Organizations across IT, BFSI, and healthcare sectors are proactively investing in threat hunting tools and services to mitigate security risks. Government initiatives supporting cybersecurity frameworks and digital infrastructure development are accelerating market adoption. Furthermore, the expansion of managed security service providers (MSSPs) is increasing the accessibility of threat hunting solutions across the region.

Japan Threat Hunting Market Insight

The Japan threat hunting market is expected to witness the fastest growth rate from 2026 to 2033, due to the country’s strong IT infrastructure, advanced digital ecosystem, and increasing need for cybersecurity in manufacturing and retail sectors. Organizations are implementing AI-driven threat detection and cloud-based monitoring platforms to protect sensitive data. The integration of threat hunting with enterprise risk management and compliance frameworks is also driving market growth. Moreover, Japan’s focus on cyber resilience and proactive security measures is boosting demand for managed and professional threat hunting services.

China Threat Hunting Market Insight

The China threat hunting market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapid digital transformation, growing cloud adoption, and rising cyberattack incidents. Enterprises are increasingly investing in network, cloud, and endpoint threat hunting solutions to secure critical operations. The emergence of MSSPs, government cybersecurity initiatives, and domestic solution providers are key factors driving market growth. In addition, the focus on smart city projects, digital banking, and e-commerce expansion is further accelerating the adoption of threat hunting solutions across industries.

Threat Hunting Market Share

The Threat Hunting industry is primarily led by well-established companies, including:

- CrowdStrike (U.S.)

- Palo Alto Networks (U.S.)

- Darktrace (U.K.)

- FireEye, Inc. (U.S.)

- IBM Corporation (U.S.)

- Cisco Systems, Inc. (U.S.)

- Fortinet, Inc. (U.S.)

- Check Point Software Technologies Ltd. (Israel)

- Rapid7, Inc. (U.S.)

- McAfee Corp. (U.S.)

- AT&T Cybersecurity (U.S.)

- Trend Micro Inc. (Japan)

- Splunk Inc. (U.S.)

- Sophos Ltd. (U.K.)

- RSA Security LLC (U.S.)

Latest Developments in Global Threat Hunting Market

- In September 2025, Palo Alto Networks (U.S.) launched a new suite of cloud-focused threat hunting tools designed to address the growing challenges of cloud security. The development aims to strengthen protection for enterprises migrating operations to cloud environments, offering advanced detection and mitigation capabilities. This expansion enhances Palo Alto Networks’ market position in cloud cybersecurity, attracts a broader client base, and encourages competitors to innovate in cloud threat-hunting solutions

- In August 2025, CrowdStrike (U.S.) announced a strategic partnership with a leading telecommunications provider to bolster threat-hunting across mobile networks. The collaboration enables integration of advanced threat intelligence with mobile security, protecting critical infrastructure and addressing emerging vulnerabilities. The move strengthens CrowdStrike’s presence in the telecom sector, opens access to new customer segments, and reinforces its competitive position in proactive cybersecurity solutions

- In July 2024, Darktrace (U.K.) secured a major contract with a multinational financial institution to implement its AI-driven threat-hunting platform. The initiative aims to leverage artificial intelligence to detect and respond to sophisticated cyber threats in real time, enhancing organizational security. This contract validates Darktrace’s AI approach, enhances credibility in the financial sector, and drives wider adoption of AI-based cybersecurity solutions across industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.