Global Thyroid Eye Disease Treatment Market

Market Size in USD Billion

USD

2.67 Billion

USD

5.45 Billion

2025

2033

USD

2.67 Billion

USD

5.45 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.67 Billion | |

| USD 5.45 Billion | |

| % | |

|

Thyroid Eye Disease Treatment Market Size

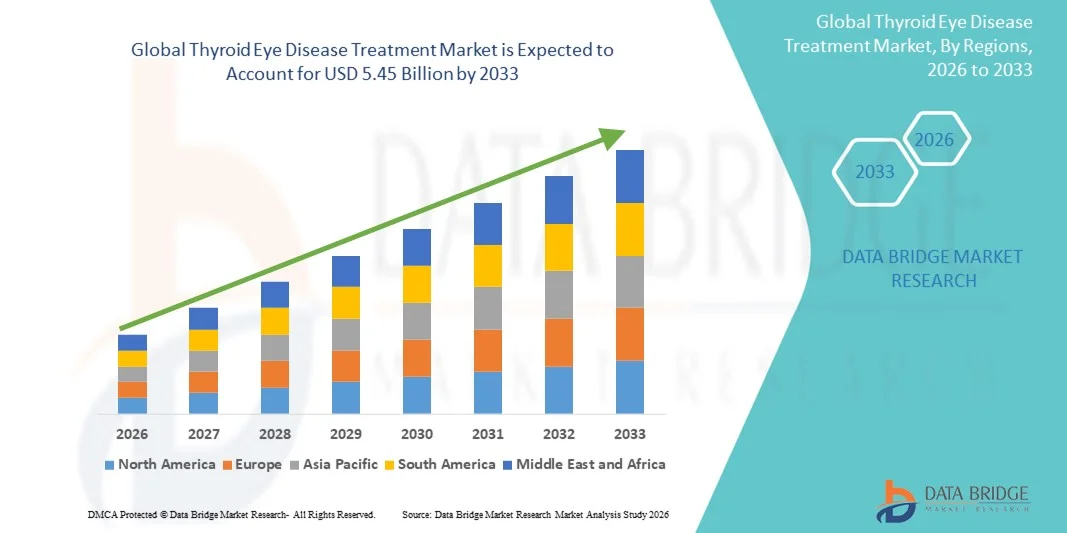

- The global thyroid eye disease treatment market size was valued at USD 2.67 billion in 2025 and is expected to reach USD 5.45 billion by 2033, at a CAGR of 9.34% during the forecast period

- The market growth is largely fueled by the increasing prevalence of thyroid disorders worldwide, coupled with rising awareness of ophthalmic complications associated with thyroid dysfunction

- Furthermore, advancements in targeted therapies, biologics, and minimally invasive surgical interventions, along with growing access to specialized ophthalmology care, are accelerating the uptake of Thyroid Eye Disease Treatment solutions, thereby significantly boosting the industry's growth

Thyroid Eye Disease Treatment Market Analysis

- Thyroid Eye Disease Treatment, offering advanced therapeutic interventions for ocular complications associated with thyroid disorders, is increasingly vital in modern healthcare systems in both clinical and hospital settings due to its effectiveness, improved safety profile, and integration with multidisciplinary treatment approaches

- The escalating demand for Thyroid Eye Disease Treatment is primarily fueled by the growing prevalence of thyroid-related ocular disorders, increasing awareness among patients and healthcare professionals, and the rising adoption of innovative therapeutic solutions

- North America dominated the thyroid eye disease treatment market with the largest revenue share of 40% in 2025, supported by advanced healthcare infrastructure, high adoption of specialized ophthalmic treatments, well-established healthcare networks, and a strong presence of key pharmaceutical and biotechnology companies

- Asia-Pacific is expected to be the fastest growing region in the thyroid eye disease treatment market during the forecast period, driven by rising healthcare expenditure, growing awareness about thyroid-related ocular disorders, increasing urbanization, and improving access to advanced treatment options in countries such as China, India, and Japan

- The Medication segment accounted for the largest market revenue share of 54.2% in 2025, fueled by the demand for systemic control of thyroid dysfunction and inflammation

Report Scope and Thyroid Eye Disease Treatment Market Segmentation

|

Attributes |

Thyroid Eye Disease Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Sanofi (France) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Thyroid Eye Disease Treatment Market Trends

Rising Focus on Advanced Therapeutics and Personalized Treatment Approaches

- A significant and accelerating trend in the global thyroid eye disease treatment market is the growing adoption of advanced therapeutics and personalized treatment strategies. This includes the increasing use of monoclonal antibodies, targeted corticosteroid therapies, and minimally invasive surgical interventions that are tailored to individual patient profiles

- For instance, recent advancements in monoclonal antibody therapy for moderate-to-severe thyroid eye disease have enabled more precise targeting of inflammatory pathways, reducing tissue damage and improving patient outcomes. Similarly, improved diagnostic tools such as orbital imaging and blood biomarker analysis allow clinicians to develop personalized treatment plans

- Integration of multimodal treatment strategies, combining surgery, radiation therapy, and pharmacologic interventions, is becoming more common. Clinicians now leverage evidence-based protocols that optimize timing, dosing, and combination therapy to enhance efficacy and minimize side effects

- The trend towards minimally invasive and non-surgical treatment options is being driven by patient demand for therapies with fewer complications, reduced recovery time, and improved cosmetic outcomes

- Pharmaceutical innovations such as novel corticosteroid formulations and oral monoclonal antibodies further support the adoption of personalized treatment. These therapies not only address the underlying pathophysiology but also improve adherence and reduce systemic side effect

- Overall, the increasing emphasis on individualized treatment plans, evidence-based guidelines, and combination therapy protocols is fundamentally reshaping patient management in thyroid eye disease and expanding the therapeutic landscape

Thyroid Eye Disease Treatment Market Dynamics

Driver

Rising Prevalence and Growing Awareness of Thyroid Eye Disease

- The increasing prevalence of thyroid disorders, particularly autoimmune thyroid conditions such as Graves’ disease, is a primary driver of market growth. With thyroid eye disease affecting an estimated 25–50% of patients with Graves’ disease, the demand for effective therapeutic solutions is expanding globally

- For instance, increased screening programs and patient education campaigns in developed regions encourage proactive management, while emerging economies are witnessing gradual improvement in diagnostic access

- Rising awareness among patients and healthcare professionals about the potential complications, including vision impairment and disfigurement, has led to earlier diagnosis and treatment initiation. This early intervention approach improves prognosis and reduces long-term healthcare costs

- Healthcare infrastructure expansion, improved access to specialized ophthalmology clinics, and increasing availability of endocrinology and ophthalmology collaboration networks are supporting timely treatment adoption

- Overall, the combination of higher disease prevalence, improved awareness, and better access to specialized care continues to drive the Thyroid Eye Disease Treatment market growth

Restraint/Challenge

High Treatment Costs and Limited Accessibility in Certain Regions

- Despite technological advancements, the high cost of monoclonal antibodies, surgical interventions, and advanced imaging remains a significant barrier, particularly in developing regions. Many patients face financial constraints that limit access to optimal treatment

- For instance, in 2024, a report from the Asia-Pacific region highlighted that less than 30% of patients with moderate-to-severe thyroid eye disease could access monoclonal antibody therapy due to cost and limited hospital availability, illustrating the real-world impact of these barriers

- Moreover, the requirement for specialized healthcare infrastructure, including trained ophthalmologists and orbital surgeons, can restrict therapy availability in rural or underdeveloped areas

- Treatment adherence is also a challenge due to prolonged therapy duration, potential side effects, and frequent follow-ups required for monitoring disease progression and therapeutic response

- Insurance coverage variability further affects patient access, with many advanced therapies being partially reimbursed or excluded entirely in certain markets

- Addressing these challenges through cost-effective treatment options, patient assistance programs, and wider distribution of specialized care centers is critical to sustaining market expansion

Thyroid Eye Disease Treatment Market Scope

The market is segmented on the basis of drug, treatment, diagnosis, dosage, route of administration, end-users, and distribution channel.

- By Drug

On the basis of drug, the Thyroid Eye Disease Treatment market is segmented into Monoclonal Antibody, Vitamin, Corticosteroid, and Others. The Monoclonal Antibody segment dominated the largest market revenue share of 48.6% in 2025, driven by the growing adoption of targeted biologic therapies for patients with moderate-to-severe thyroid eye disease. Monoclonal antibodies are preferred for their effectiveness in reducing inflammation, controlling proptosis, and preventing disease progression. Clinical trials and approvals of drugs such as Teprotumumab have increased awareness and confidence among ophthalmologists. Hospitals and specialty clinics favor monoclonal antibodies due to their predictable therapeutic outcomes and standardized dosing protocols. The segment benefits from increasing healthcare expenditure, insurance coverage, and expanding patient access programs. Furthermore, targeted therapy minimizes side effects compared to traditional corticosteroids, enhancing patient adherence. Growing prevalence of thyroid dysfunction, particularly in aging populations, continues to boost demand. Awareness campaigns by healthcare organizations emphasize early intervention with monoclonal antibodies. Partnerships between pharmaceutical companies and healthcare providers enhance distribution and accessibility. Advanced research in biologics further supports pipeline expansion, reinforcing market dominance.

The Vitamin segment is expected to witness the fastest CAGR of 12.8% from 2026 to 2033, driven by increasing awareness of supportive therapies for thyroid eye disease. Vitamins, particularly antioxidants and selenium supplements, are used to complement standard treatments and improve quality of life. Rising adoption among patients with mild or early-stage disease contributes to segment growth. Vitamins are often recommended in outpatient settings, facilitating convenient administration and monitoring. Clinical studies highlighting their potential benefits in slowing disease progression boost usage. Retail and online pharmacy availability further accelerates adoption. Growth in health-conscious populations seeking complementary therapies supports expansion. The preference for non-invasive and low-risk interventions encourages wider acceptance. Rising physician recommendations for adjunctive vitamin therapy drive segment penetration. Market education and awareness campaigns strengthen patient confidence in vitamin supplementation.

- By Treatment

On the basis of treatment, the market is segmented into Surgery, Radioactive Iodine Therapy, and Medication. The Medication segment accounted for the largest market revenue share of 54.2% in 2025, fueled by the demand for systemic control of thyroid dysfunction and inflammation. Medication, including corticosteroids and immunomodulatory drugs, is widely used due to ease of administration and effectiveness in early and moderate disease stages. Clinicians prefer medication for initial treatment to reduce disease activity and prevent vision-threatening complications. Increasing prevalence of autoimmune thyroid disorders drives adoption. Pharmaceutical companies focus on developing combination therapies to enhance outcomes. Accessibility through hospitals and pharmacies supports segment dominance. Clinical guidelines recommending early intervention with medications further reinforce its market share. Expansion of chronic care programs improves long-term treatment adherence. Insurance coverage and government health schemes enhance affordability and reach. Patient preference for non-invasive interventions over surgery contributes to medication dominance.

The Surgery segment is expected to witness the fastest CAGR of 11.9% from 2026 to 2033, primarily driven by advancements in orbital decompression and strabismus procedures. Surgical interventions are required for severe or refractory cases where medications are insufficient. Technological improvements and minimally invasive techniques improve patient safety and reduce recovery times. Rising availability of specialized ophthalmic surgeons supports growth. Increasing awareness of surgical options among patients and clinicians boosts adoption. Surgical procedures for functional and cosmetic restoration gain popularity. Integration of preoperative imaging and planning enhances success rates. Expansion of tertiary care hospitals and specialized eye centers accelerates segment growth. Improved postoperative outcomes encourage more patients to opt for surgery. Partnerships between medical device companies and hospitals drive adoption of advanced surgical tools.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Imaging Test, Orbital Ultrasound, Blood Test, Radioactive Iodine Uptake Test, and Physical Exam. The Imaging Test segment dominated the largest market revenue share of 49.5% in 2025, due to its critical role in assessing orbital tissue changes, extraocular muscle involvement, and disease severity. Imaging techniques such as CT and MRI provide detailed structural information essential for treatment planning. Hospitals and specialized eye clinics heavily rely on imaging for both baseline and follow-up evaluations. Increasing availability of advanced imaging equipment in emerging economies supports market dominance. Imaging enables precise monitoring of treatment response, aiding in clinical decision-making. Integration with electronic health records facilitates longitudinal tracking of patients. Radiologists and ophthalmologists prefer imaging for preoperative assessments. Reimbursement policies and insurance coverage support higher utilization. Expansion of diagnostic centers and adoption of automated image analysis improve efficiency. Patient preference for non-invasive diagnostics reinforces imaging test dominance.

The Orbital Ultrasound segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by its cost-effectiveness, accessibility, and ability to assess extraocular muscle thickness and orbital fat. Portable ultrasound devices allow point-of-care diagnostics, supporting clinic-level adoption. Ultrasound aids in monitoring treatment response and disease progression. Growing adoption in outpatient clinics accelerates segment growth. Clinical research validating ultrasound effectiveness boosts confidence among clinicians. Expansion of diagnostic training programs enhances usage. Rising awareness of non-invasive diagnostic options among patients encourages preference. Integration with digital imaging systems enhances reporting and record-keeping. The segment’s portability and reduced radiation exposure support wider adoption.

- By Dosage

On the basis of dosage, the market is segmented into Tablet, Injection, and Others. The Tablet segment accounted for the largest market revenue share of 51.6% in 2025, owing to patient convenience, ease of self-administration, and cost-effectiveness. Tablets are preferred for long-term management of thyroid hormone levels and anti-inflammatory therapies. High patient adherence and well-established manufacturing processes reinforce dominance. Widespread availability in hospitals, clinics, and pharmacies supports large market share. Clinical preference for oral dosing in early and moderate disease stages drives adoption. Patient familiarity with tablets ensures better compliance. Expansion of retail pharmacy networks ensures accessibility. Regulatory approvals and standardization of dosing strengthen market leadership. Increasing chronic thyroid disease prevalence sustains demand.

The Injection segment is expected to witness the fastest CAGR of 13.1% from 2026 to 2033, primarily due to rising use of monoclonal antibody therapies and corticosteroid injections for severe cases. Injectable therapies offer rapid onset and targeted action. Hospital administration and clinic adoption drive segment growth. Technological advancements in auto-injectors and biosimilars enhance accessibility. Increasing physician preference for precise dosing accelerates market expansion. Growing insurance coverage for advanced injections improves affordability. Patient outcomes and reduced side effects boost adoption. Expansion of specialty clinics supports injectable therapy penetration. Rising clinical awareness and guideline recommendations further reinforce growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Intravenous, Topical, and Others. The Oral segment dominated the largest market revenue share of 53.2% in 2025, due to its widespread use in corticosteroid and hormone therapies. Oral administration ensures ease of use, patient compliance, and cost efficiency. Tablets and capsules are preferred in both hospital and clinic settings for chronic management. Accessibility through retail and hospital pharmacies reinforces dominance. Clinical guidelines favor oral therapy for early and moderate disease stages. Patient familiarity and comfort with oral dosing enhance adherence. Expansion of outpatient care supports growth. Insurance coverage and standardized dosing further boost utilization.

The Intravenous segment is expected to witness the fastest CAGR of 12.6% from 2026 to 2033, driven by monoclonal antibody therapies requiring hospital or clinic administration. IV therapy ensures controlled delivery, rapid action, and monitoring of adverse events. Hospital adoption of IV-based treatment protocols accelerates growth. Specialized infusion centers and trained staff improve accessibility. Clinical research supporting efficacy promotes physician confidence. Rising prevalence of severe thyroid eye disease encourages IV therapy adoption. Integration with outpatient infusion programs enhances convenience.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment dominated the largest market revenue share of 60.3% in 2025, driven by high patient volume, availability of specialized ophthalmologists, and infrastructure for advanced diagnostics and treatment. Hospitals offer comprehensive care including imaging, injections, and surgery. Insurance coverage and centralized procurement reinforce market dominance. Referral networks and government health initiatives support hospital adoption. Clinical guidelines often recommend hospital-based management for severe cases.

The Clinic segment is expected to witness the fastest CAGR of 10.1% from 2026 to 2033, due to increasing outpatient visits and growing awareness of early disease management. Clinics provide convenient access for monitoring mild-to-moderate cases. Expansion of specialty ophthalmology and endocrinology clinics supports growth. Portable diagnostic tools and point-of-care therapies boost adoption. Telemedicine integration enables wider reach. Rising patient preference for outpatient care enhances growth potential.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 57.4% in 2025, as hospitals procure both oral and injectable therapies in bulk for inpatient and outpatient care. Centralized procurement, regulatory compliance, and quality assurance reinforce leadership. Strategic partnerships with pharmaceutical companies ensure consistent supply. The Hospital Pharmacy segment also benefits from trained pharmacists who can provide patient counseling, ensuring correct usage and adherence to treatment protocols. In addition, hospitals often participate in clinical trials and patient assistance programs, further strengthening the segment’s dominance and expanding access to advanced therapies

The Online Pharmacy segment is expected to witness the fastest CAGR of 12.9% from 2026 to 2033, due to growth in e-commerce and digital healthcare platforms. Online pharmacies offer convenient ordering, home delivery, and subscription models. Increased internet penetration and smartphone usage boost adoption. Home-based therapy kits and oral medication availability further drive growth. Telemedicine and digital health consultations enhance consumer confidence. Remote patient populations benefit from improved accessibility. Rising preference for contactless delivery supports expansion. Competitive pricing and promotional offers strengthen adoption.

Thyroid Eye Disease Treatment Market Regional Analysis

- North America dominated the thyroid eye disease treatment market with the largest revenue share of 40% in 2025

- Supported by advanced healthcare infrastructure, high adoption of specialized ophthalmic treatments

- Well-established healthcare networks, and a strong presence of key pharmaceutical and biotechnology companies

U.S. Thyroid Eye Disease Treatment Market Insight

The U.S. thyroid eye disease treatment market captured the largest revenue share in 2025 within North America, driven by increased diagnosis of thyroid eye disease, rising adoption of biologics and monoclonal antibody therapies, and strong healthcare reimbursement frameworks. The presence of advanced ophthalmic centers and research initiatives for innovative therapies further supports market growth.

Europe Thyroid Eye Disease Treatment Market Insight

The Europe thyroid eye disease treatment market is projected to expand at a substantial CAGR during the forecast period due to increasing prevalence of thyroid disorders, well-developed healthcare infrastructure, and growing adoption of advanced treatment modalities. Countries such as Germany, France, and the U.K. are witnessing significant growth across both clinical and hospital settings.

U.K. Thyroid Eye Disease Treatment Market Insight

The U.K. thyroid eye disease treatment market is anticipated to grow steadily during the forecast period, driven by rising patient awareness, government health initiatives for early diagnosis, and increasing adoption of both pharmacological and surgical interventions for thyroid eye disease.

Germany Thyroid Eye Disease Treatment Market Insight

Germany thyroid eye disease treatment market is expected to witness notable growth, fueled by robust healthcare systems, advanced ophthalmology centers, and the increasing focus on personalized treatment approaches for thyroid eye disease.

Asia-Pacific Thyroid Eye Disease Treatment Market Insight

The Asia-Pacific thyroid eye disease treatment market is poised to grow at the fastest CAGR from 2026 to 2033, driven by rising healthcare expenditure, growing prevalence of thyroid disorders, urbanization, and improving access to advanced treatment options in countries such as China, India, and Japan.

Japan Thyroid Eye Disease Treatment Market Insight

Japan’s thyroid eye disease treatment market is growing due to high awareness of thyroid-related ocular disorders, increasing geriatric population, and demand for biologic therapies and advanced ophthalmic care in both hospitals and specialized clinics.

China Thyroid Eye Disease Treatment Market Insight

China thyroid eye disease treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing patient awareness, rapid urbanization, improving healthcare infrastructure, and growing availability of advanced treatment options for thyroid eye disease across hospital and clinic settings.

Thyroid Eye Disease Treatment Market Share

The Thyroid Eye Disease Treatment industry is primarily led by well-established companies, including:

• Sanofi (France)

• Pfizer Inc. (U.S.)

• AbbVie Inc. (U.S.)

• Merck & Co., Inc. (U.S.)

• Bristol-Myers Squibb (U.S.)

• Amgen Inc. (U.S.)

• Eli Lilly and Company (U.S.)

• Astellas Pharma Inc. (Japan)

• Takeda Pharmaceutical Company Limited (Japan)

• Bayer AG (Germany)

• Fujifilm Pharma (Japan)

• Spectra Laboratories (U.S.)

• Teva Pharmaceutical Industries Ltd. (Israel)

• Glenmark Pharmaceuticals (India)

• Sun Pharmaceutical Industries Ltd. (India)

• Hikma Pharmaceuticals PLC (U.K.)

• Celgene Corporation (U.S.)

• Janssen Pharmaceuticals (Belgium)

Latest Developments in Global Thyroid Eye Disease Treatment Market

- In April 2023, the U.S. FDA approved an updated indication for Tepezza (teprotumumab‑trbw), allowing its use in patients with thyroid eye disease regardless of disease activity or duration. This followed data from a Phase 4 trial showing that even patients with low activity scores experienced significant reductions in eye bulging after 24 weeks

- In November 2023, Acelyrin reported positive Phase 1/2 proof-of-concept results for lonigutamab, a subcutaneous monoclonal antibody targeting IGF‑1R in TED. Patients showed rapid improvements in proptosis and Clinical Activity Score within just three weeks of the first dose

- In June 2023, Immunovant published Phase 2 data for batoclimab (HBM9161), an FcRn inhibitor designed to lower pathogenic antibodies in thyroid eye disease. Early results showed favorable safety and reductions in disease biomarkers, suggesting a new autoimmune-focused treatment pathway

- In September 2024, Viridian Therapeutics announced that its experimental therapy veligrotug, an IGF‑1R inhibitor, achieved its primary and secondary endpoints in a late-stage trial: 64% of patients saw a meaningful reduction in proptosis after 15 weeks

- In April 2025, the European Medicines Agency’s (EMA) CHMP gave a positive opinion recommending the first-ever marketing authorization of Tepezza (teprotumumab) for adults with moderate-to-severe thyroid eye disease in Europe

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.