Global Tissue Diagnostics Market

Market Size in USD Million

USD

602.95 Million

USD

1,005.40 Million

2024

2032

USD

602.95 Million

USD

1,005.40 Million

2024

2032

| 2025 - 2032 | |

| USD 602.95 Million | |

| USD 1,005.40 Million | |

| % | |

|

Tissue Diagnostics Market Size

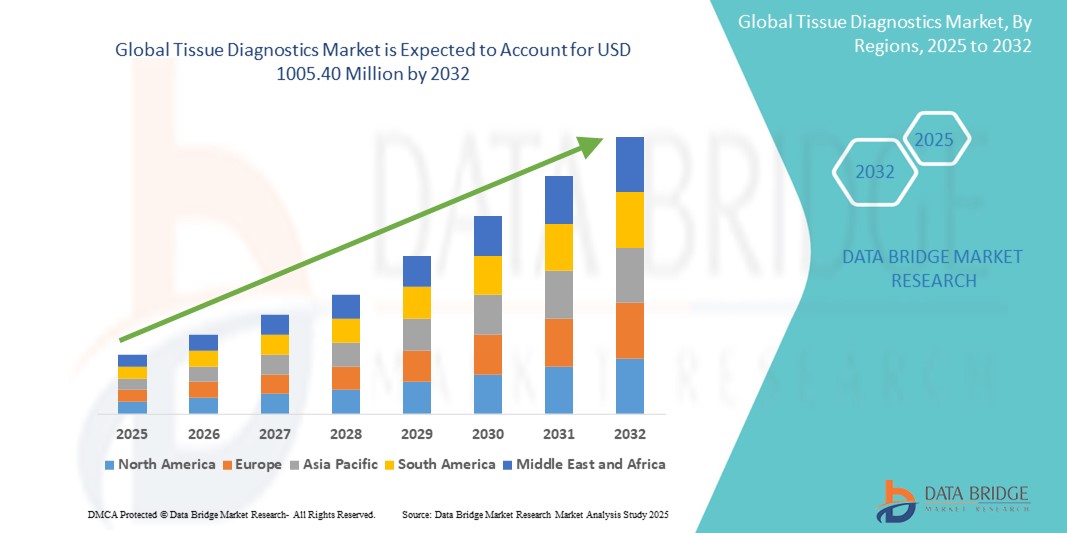

- The global tissue diagnostics market size was valued at USD 602.95 Million in 2024 and is expected to reach USD 1,005.40 Million by 2032, at a CAGR of 6.60% during the forecast period

- The market growth in tissue diagnostics is largely fueled by the increasing prevalence of cancer and other chronic diseases worldwide, along with significant technological progress, leading to enhanced diagnostic accuracy and efficiency in both clinical and research settings

- Furthermore, rising demand for precise, early detection and personalized medicine approaches is establishing advanced tissue diagnostics solutions, such as digital pathology and molecular diagnostics, as the modern standard for disease management. These converging factors are accelerating the uptake of Tissue Diagnostics solutions, thereby significantly boosting the industry's growth

Tissue Diagnostics Market Analysis

- Tissue diagnostics, offering detailed insights into cellular and molecular changes in tissues, are increasingly vital components of modern disease diagnosis, prognosis, and treatment selection in both clinical and research settings. This is due to their enhanced accuracy, ability to identify specific biomarkers, and seamless integration with personalized medicine approaches

- The escalating demand for tissue diagnostics is primarily fueled by the widespread and rising global incidence of cancer and other chronic diseases, growing emphasis on early and precise disease detection, and a rising preference for tailored therapeutic strategies. The global cancer burden is projected to reach over 28 million new cases by 2040, underscoring the critical need for advanced diagnostic tools

- North America dominates the tissue diagnostics market, with the largest revenue share of 41.4% 2024, characterized by advanced healthcare infrastructure, high healthcare expenditure, a strong focus on research and development in genomics and proteomics, and the early adoption of cutting-edge diagnostic technologies

- Asia-Pacific is expected to be the fastest-growing region in the tissue diagnostics market during the forecast period, with a projected CAGR of 10.6%, driven by increasing healthcare expenditure, rising awareness of cancer screening, improving healthcare infrastructure, and a large patient pool in countries such as China, India, and Japan

- Breast Cancer segment dominates the Global tissue diagnostics market with the largest market revenue share of 50.66% in 2024, driven by the increasing incidence of breast cancer globally, rising awareness about early detection and diagnosis, and the critical need for precise tissue diagnostics for effective treatment planning.

Report Scope and Tissue Diagnostics Market Segmentation

|

Attributes |

Tissue Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Tissue Diagnostics Market Trends

“Deepening Integration of Advanced Digital Pathology Solutions”

- A significant and accelerating trend in the global tissue diagnostics market is the deepening integration of advanced digital pathology solutions. This fusion of technologies is significantly enhancing diagnostic efficiency, precision, and the overall capabilities of pathology labs and research

- For instance, digital pathology platforms from companies such as Paige.AI or Aiforia seamlessly integrate algorithms to analyze whole-slide images. This assists pathologists with tasks such as tumor detection, grading, and quantification of biomarkers. This allows for automated analysis of large datasets, reducing manual effort and improving turnaround times

- The integration of digital tools in tissue diagnostics enables features such as learning from vast datasets of tissue images to improve diagnostic accuracy over time, and providing intelligent alerts for suspicious areas or rare disease patterns. For instance, some models can assist in identifying subtle morphological changes indicative of early-stage cancer or predict treatment responses based on tissue biomarkers. Furthermore, automation helps in standardizing workflows, reducing variability among observers, and enhancing throughput in high-volume laboratories

- The seamless integration of digital tissue diagnostic tools with laboratory information systems (LIS) and broader digital healthcare platforms facilitates centralized control and comprehensive data management. Through a unified interface, pathologists and researchers can manage digital slides, access patient data, and integrate findings with other diagnostic modalities, creating a unified and automated diagnostic and research ecosystem

- This trend towards more intelligent, intuitive, and interconnected diagnostic systems is fundamentally reshaping user expectations for pathology. Consequently, companies are developing digital pathology solutions with features such as automated prescreening of slides, intelligent case prioritization, and decision support tools for complex diagnoses

- The demand for tissue diagnostic solutions that offer seamless digital integration is growing rapidly across both clinical pathology and research sectors, as healthcare providers increasingly prioritize efficiency, accuracy, and comprehensive insights for personalized medicine and improved patient outcomes

Tissue Diagnostics Market Dynamics

Driver

“Growing Need Due to Rising Cancer Burden and Advancements in Personalized Medicine”

- The increasing prevalence of cancer and other chronic diseases globally, coupled with the accelerating adoption of personalized medicine approaches, is a significant driver for the heightened demand for tissue diagnostics.

- For instance, the global incidence of cancer is projected to rise by 60% by 2040, emphasizing the urgent need for accurate and advanced diagnostic tools

- As healthcare systems become more aware of the critical role of early and precise disease detection in improving patient outcomes, tissue diagnostics offer advanced features such as biomarker identification, molecular profiling, and disease stratification, providing compelling insights for targeted therapies

- Furthermore, the growing popularity of precision medicine and the desire for tailored treatment strategies are making tissue diagnostics an integral component of modern healthcare, offering seamless integration with therapeutic decision-making and patient management platforms

- The ability to detect diseases at an early stage, predict therapeutic response, and monitor disease progression with high accuracy are key factors propelling the adoption of tissue diagnostics in both clinical and research sectors. The trend towards digital pathology installations and the increasing availability of sophisticated diagnostic solutions further contributes to market growth

Restraint/Challenge

“Concerns Regarding High Initial Costs and Stringent Regulatory Requirements”

- Concerns surrounding the high initial cost of advanced tissue diagnostic instruments and reagents pose a significant challenge to broader market penetration, particularly in developing regions or for smaller diagnostic laboratories.

- For instance, new digital pathology systems generally range from USD 50,000 to USD 200,000, with high-end models potentially costing up to USD 300,000. These substantial upfront investments can be a barrier for many healthcare facilities

- In addition, stringent regulatory requirements, such as those imposed by the FDA (for instance, Class III devices requiring exhaustive Premarket Approval (PMA)) and the EU's IVDR, create significant hurdles for companies aiming to introduce innovative products. These regulations can lead to lengthy approval processes, increased compliance costs, and potential delays in market entry

- Addressing these cost and regulatory concerns through research and development of more affordable technologies, streamlining regulatory pathways, and providing robust economic justifications for new diagnostic solutions is crucial for building wider adoption. While efforts are being made to develop more cost-effective solutions and harmonize regulations globally, the perceived premium for advanced diagnostic technology and the complexity of regulatory compliance can still hinder widespread adoption, especially for institutions with budget constraints

- Overcoming these challenges through enhanced accessibility, consumer/provider education on the long-term benefits of early and precise diagnostics, and the development of more affordable tissue diagnostics options will be vital for sustained market growth

Tissue diagnostics market Scope

The market is segmented on the basis of product, technology, disease and end user.

- By Product

On the basis of product, the Global tissue diagnostics market is segmented into consumables and instruments. The consumables segment dominates the market, with 59.2% of the market share in 2024. This dominance is driven by the recurring nature and high consumption rate of products like fixatives, embedding mediums, various stains, antibodies, and probes, which are essential for routine diagnostic procedures.

The instruments segment is anticipated to grow at a considerable rate, fueled by technological advancements in automated systems and digital pathology.

- By Technology

On the basis of technology, the tissue diagnostics market is segmented into immunohistochemistry, in situ hybridization, digital pathology and workflow management, and special staining. The immunohistochemistry segment dominated the market in terms of revenue share, accounting for 25.79% in 2024. Immunohistochemistry widespread use in cancer diagnosis due to its ability to detect specific target proteins in tissue samples contributes to its leading position.

The digital pathology and workflow management segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by increasing adoption of whole-slide imaging, AI integration for image analysis, and the demand for enhanced workflow efficiency and remote diagnostics.

- By Disease

On the basis of disease, the tissue diagnostics market is segmented into breast cancer, gastric cancer, lymphoma, prostate cancer, non-small cell lung cancer, and other diseases. The breast cancer segment held the largest market share of 50.66% in 2024 and is anticipated to grow at the fastest CAGR, driven by the increasing incidence of breast cancer globally, rising awareness, and the critical need for precise tissue diagnostics for early detection, diagnosis, and treatment planning.

- By End User

On the basis of end user, the tissue diagnostics market is segmented into hospitals, pharmaceutical companies, research laboratories, diagnostic centres, ambulatory surgical centres, and others. The hospitals segment dominated the market in 2024. This is attributed to the high volume of patient admissions for diagnostic and treatment purposes, the availability of developed infrastructure, and the increasing usage of tissue diagnostic systems and services within hospital settings.

The diagnostic centers segment is expected to witness significant growth, driven by the increasing demand for specialized diagnostic services and outsourcing by healthcare providers.

Tissue Diagnostics Market Regional Analysis

- North America dominates the Global Tissue diagnostics market with the largest revenue share, accounting for 41.4% in 2024. This leadership is driven by highly developed healthcare infrastructure, significant investments in research and development, a high prevalence of cancer, favorable reimbursement policies, and the early adoption of advanced diagnostic technologies such as digital pathology and AI-powered solutions

- This widespread adoption is further supported by high healthcare expenditure, a technologically advanced population, and the growing preference for personalized medicine approaches, establishing tissue diagnostics as a favored solution for both clinical pathology and research applications

U.S. Tissue Diagnostics Market Insight

The U.S. tissue diagnostics market captured the largest revenue share of 46.5% in 2024 within North America, fueled by the swift uptake of advanced diagnostic technologies and the expanding trend of personalized medicine. Consumers and healthcare providers are increasingly prioritizing precise diagnosis and tailored treatment strategies through advanced tissue analysis. The growing emphasis on early cancer detection, combined with robust demand for molecular profiling and digital pathology systems, further propels the Tissue Diagnostics industry. Moreover, the increasing integration of AI-powered analytics and companion diagnostics is significantly contributing to the market's expansion, driven by strong R&D and a robust healthcare infrastructure.

Europe Tissue Diagnostics Market Insight

The Europe Tissue diagnostics market is projected to expand at a substantial CAGR from 2025 to 2032, driven primarily by the rising incidence of chronic diseases, an aging population, and increasing access to advanced healthcare. The increase in cancer burden, coupled with the demand for automated and digital diagnostic solutions, is fostering the adoption of sophisticated tissue diagnostics. European healthcare systems are also drawn to the efficiency and accuracy these devices offer. The region is experiencing significant growth across hospital, diagnostic center, and research laboratory applications, with tissue diagnostics being incorporated into both routine diagnostics and groundbreaking research initiatives.

U.K. Tissue Diagnostics Market Insight

The U.K. tissue diagnostics market is anticipated to grow at a noteworthy CAGR during the forecast period. This growth is driven by the escalating focus on early cancer detection, rising incidence of cancer, and a desire for heightened diagnostic precision. In addition, initiatives within the NHS to adopt digital pathology and streamline diagnostic workflows are encouraging healthcare providers to invest in advanced tissue analysis solutions. The UK’s embrace of technological advancements in healthcare, alongside its robust research infrastructure, is expected to continue to stimulate market growth.

Germany Tissue Diagnostics Market Insight

The Germany tissue diagnostics market is expected to expand at a considerable CAGR from 2025 to 2032, fueled by increasing awareness of precision medicine and the demand for technologically advanced, high-quality diagnostic solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and robust research activities, promotes the adoption of tissue diagnostics, particularly in oncology and specialized diagnostics. The integration of digital pathology with laboratory information systems is also becoming increasingly prevalent, with a strong preference for secure, high-accuracy solutions aligning with local healthcare expectations.

Asia-Pacific Tissue Diagnostics Market Insight

The Asia-Pacific tissue diagnostics market is poised to grow at the fastest CAGR of 10.6% from 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards improving healthcare access and quality, supported by government initiatives promoting digitalization and healthcare infrastructure development, is driving the adoption of tissue diagnostics. Furthermore, as APAC emerges as a significant hub for healthcare investment and local manufacturing capabilities, the affordability and accessibility of tissue diagnostics are expanding to a wider patient base.

Japan Tissue Diagnostics Market Insight

The Japan tissue diagnostics market is gaining momentum with a projected CAGR of 9.7% from 2025 to 2032 due to the country’s high-tech culture, rapid aging population, and demand for advanced healthcare solutions. The Japanese market places a significant emphasis on precision medicine and advanced diagnostics, and the adoption of tissue diagnostics is driven by the increasing incidence of age-related diseases, particularly cancer. The integration of digital pathology with other healthcare IT systems, such as hospital information systems, is fueling growth. Moreover, Japan's focus on innovative research and early detection programs is likely to spur demand for accurate and efficient diagnostic solutions in both clinical and research sectors.

China Tissue Diagnostics Market Insight

The China tissue diagnostics market accounted for a significant market revenue in Asia Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and high rates of technological adoption in healthcare. the tissue diagnostics market in China is expected to grow at a CAGR of 9.3% from 2025 to 2032. China stands as one of the largest patient populations globally, and advanced tissue diagnostics are becoming increasingly critical in cancer diagnosis, treatment selection, and research. The push towards healthcare reforms and the availability of increasingly sophisticated yet affordable diagnostic options, alongside strong domestic manufacturers and a growing R&D focus, are key factors propelling the market in China.

Tissue Diagnostics Market Share

The tissue diagnostics industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd (Switzerland)

- Danaher Corporation (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Abbott (U.S.)

- Agilent Technologies Inc. (U.S.)

- Merck KGaA (U.S.)

- Sakura Finetek Japan Co., Ltd. (Japan)

- BD (U.S.)

- QIAGEN (Germany)

- Bio SB (U.S.)

- BioGenex (U.S.)

- Abcam Limited (U.K.)

- Cell Signaling Technology, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- The Menarini Group (Italy)

- Enzo Biochem Inc. (U.S.)

- Lunaphore Technologies SA. (Switzerland)

- 3DHISTECH Ltd. (Hungary)

- Biocare Medical, LLC. (U.S.)

- Exact Sciences Corporation (U.S.)

Latest Developments in Global Tissue Diagnostics Market

- In April 2025, F. Hoffmann-La Roche Ltd (Switzerland) announced that its VENTANA TROP2 (EPR20043) RxDx Device received FDA Breakthrough Device Designation. This is the first Breakthrough Device Designation for a computational pathology companion diagnostic (CDx) device, leveraging AI-based image analysis for non-small cell lung cancer (NSCLC) to enable more precise diagnosis

- In April 2025, Agilent Technologies Inc. (U.S.) received European IVDR certification for its PD-L1 IHC 22C3 pharmDx companion diagnostic assay for use in gastric or gastroesophageal junction (GEJ) adenocarcinoma. This expands its utility in identifying patients eligible for KEYTRUDA therapy

- In April 2025, Leica Biosystems and Bio-Techne expanded their partnership to offer innovative spatial multiomics solutions for automated spatial multiomics on the BOND RX Research Staining Instrument, further advancing the capabilities of spatial biology research

- In March 2025, Leica Biosystems and CellCarta partnered to accelerate companion diagnostics development in China. This collaboration aims to provide pharmaceutical and biotechnology companies with a comprehensive range of biomarker services in China for China

- In January 2025, Leica Biosystems launched the HistoCore CHROMAX Workstation, advancing its coverslipping and staining portfolio. This new workstation automates reagent management, enhancing efficiency in anatomical pathology workflows

- In January 2025, Philips (Netherlands) and Ibex Medical Analytics (Ibex) expanded their partnership to further accelerate the adoption of AI-enabled digital pathology workflows for better patient care. This aims to improve diagnostic accuracy and efficiency in prostate, breast, and gastric cancer diagnostics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.