Global Topoisomerase I Payload Adc Drugs Market

Market Size in USD Billion

USD

4.88 Billion

USD

16.33 Billion

2025

2033

USD

4.88 Billion

USD

16.33 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.88 Billion | |

| USD 16.33 Billion | |

| % | |

|

Topoisomerase-I Payload ADC Drugs Market Size

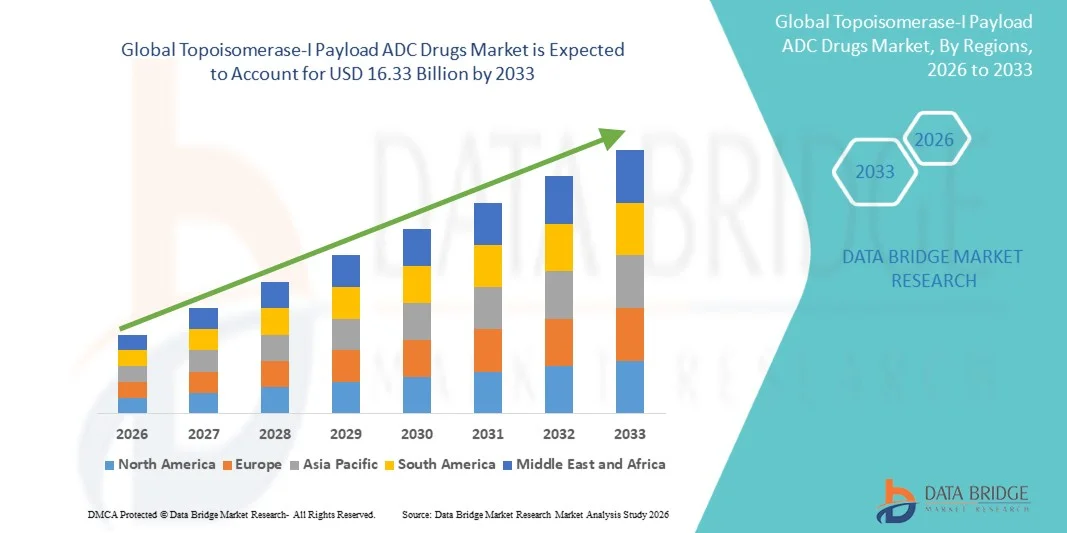

- The global Topoisomerase-I Payload ADC Drugs market size was valued at USD 4.88 billion in 2025 and is expected to reach USD 16.33 billion by 2033, at a CAGR of 16.30% during the forecast period

- The market growth is largely fueled by the increasing adoption of targeted cancer therapies and continuous technological advancements in antibody-drug conjugates (ADCs) incorporating Topoisomerase-I payloads. These innovations enable more precise drug delivery, improved efficacy, and reduced systemic toxicity, driving adoption across oncology hospitals, research centers, and clinical trial settings

- Furthermore, rising demand for effective, personalized cancer treatments is establishing Topoisomerase-I Payload ADCs as a preferred solution for a range of solid tumors and hematological malignancies. These converging factors — including expanding oncology pipelines, regulatory approvals of new ADCs, and growing awareness of targeted therapy benefits — are significantly accelerating the uptake of Topoisomerase-I Payload ADC Drugs, thereby boosting overall market growth

Topoisomerase-I Payload ADC Drugs Market Analysis

- Topoisomerase-I Payload ADC Drugs, offering targeted delivery of cytotoxic agents to cancer cells via antibody-drug conjugates, are increasingly vital components of modern oncology treatment due to their enhanced precision, reduced systemic toxicity, and ability to improve patient outcomes across multiple solid tumors and hematological malignancies

- The escalating demand for Topoisomerase-I Payload ADC Drugs is primarily fueled by the growing adoption of targeted cancer therapies, expansion of clinical pipelines, rising cancer prevalence, and increasing investments in oncology research and biopharmaceutical innovation, driving adoption across hospitals, specialty cancer centers, and research institutions worldwide

- North America dominated the Topoisomerase‑I Payload ADC Drugs market with the largest revenue share of approximately 42% in 2025, supported by a robust biopharmaceutical ecosystem, high R&D investment, advanced healthcare infrastructure, and early adoption of targeted oncology therapies. The U.S. leads this regional dominance, driven by leading pharmaceutical and biotech companies, extensive clinical trial networks, and favorable regulatory frameworks

- Asia Pacific is expected to be the fastest-growing region in the Topoisomerase‑I Payload ADC Drugs market during the forecast period, fueled by increasing cancer incidence, rising healthcare expenditure, expanding pharmaceutical manufacturing capabilities, and growing participation in global clinical trials. Key countries contributing to growth include China, Japan, and India

- The Monoclonal Antibody segment dominated the largest market revenue share of 61.3% in 2025, driven by its well-established clinical success, broad regulatory acceptance, and proven safety profile

Report Scope and Topoisomerase-I Payload ADC Drugs Market Segmentation

|

Attributes |

Topoisomerase-I Payload ADC Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Topoisomerase-I Payload ADC Drugs Market Trends

“Advancements in Targeted Therapy and Payload Optimization”

- A significant and accelerating trend in the global Topoisomerase-I Payload ADC Drugs market is the growing focus on precision-targeted therapy using antibody-drug conjugates (ADCs) with optimized Topoisomerase-I payloads. These therapies are designed to deliver cytotoxic agents specifically to cancer cells, minimizing damage to healthy tissues and improving therapeutic outcomes

- For instance, several leading pharmaceutical companies are developing ADCs with novel linker technologies and enhanced stability, allowing more controlled release of Topoisomerase-I payloads and improved pharmacokinetics. This trend is particularly evident in late-stage clinical trials targeting breast, ovarian, and colorectal cancers

- Another notable trend is the increasing combination of Topoisomerase-I ADCs with immunotherapy or other targeted agents, aiming to enhance efficacy and overcome drug resistance. Pharmaceutical firms are also investing in next-generation ADC platforms that allow flexible payload conjugation, better tumor penetration, and reduced systemic toxicity

- The trend toward personalized medicine is further accelerating adoption, as patient-specific biomarkers are increasingly used to identify candidates most likely to benefit from Topoisomerase-I ADC therapy

- With regulatory approvals and breakthrough designations in multiple regions, the market is seeing robust growth driven by the need for more effective and safer cancer treatments

Topoisomerase-I Payload ADC Drugs Market Dynamics

Driver

“Rising Incidence of Targeted Cancers and Need for Precision Oncology”

- The increasing prevalence of cancers such as breast, ovarian, colorectal, and lung cancer is a key driver for the growth of Topoisomerase-I Payload ADCs. Patients and clinicians are seeking therapies that offer targeted action with reduced systemic toxicity compared to conventional chemotherapy.

- For instance, in March 2024, ImmunoGen, Inc. reported positive Phase III trial results for mirvetuximab soravtansine, a Topoisomerase-I ADC for ovarian cancer, demonstrating improved progression-free survival and tolerability, which is expected to drive adoption globally

- Growing awareness and demand for personalized medicine and biomarker-driven therapy further support the development and clinical uptake of Topoisomerase-I ADCs

- Advances in ADC technology, including better linkers and payload optimization, are enhancing drug stability and efficacy, making these treatments more attractive to healthcare providers and patients alike

- Increased investment by pharmaceutical companies in oncology R&D is fueling the development pipeline of new Topoisomerase-I ADCs. For example, companies such as Daiichi Sankyo, Seagen, and Mersana Therapeutics are actively expanding clinical trials targeting multiple solid tumors

- Regulatory incentives and accelerated approval pathways, such as FDA’s Fast Track and Breakthrough Therapy designations, are encouraging rapid development and commercialization of Topoisomerase-I ADCs

- Rising adoption of combination therapies, where Topoisomerase-I ADCs are paired with immunotherapy or other targeted treatments, is further expanding market potential and improving clinical outcomes

- Growing healthcare infrastructure in emerging markets is also enabling better access to advanced oncology treatments, contributing to global market growth

Restraint/Challenge

“High Cost of Development, Regulatory Hurdles, and Safety Concerns”

- The high cost of R&D and complex manufacturing processes for Topoisomerase-I ADCs remain major challenges for market expansion. Conjugating cytotoxic payloads to antibodies requires advanced technology and stringent quality control, increasing production costs

- For instance, Seagen and Daiichi Sankyo have cited production and clinical trial costs as key considerations in pricing strategies, impacting accessibility in price-sensitive regions

- Stringent regulatory requirements for clinical trials, safety evaluations, and approvals in major markets such as the U.S., EU, and Japan can delay commercialization and create barriers for new entrants

- Safety concerns and adverse effects, including myelosuppression, neutropenia, and gastrointestinal toxicity, may limit clinical adoption or require additional monitoring protocols. This can affect physician preference and slow market uptake

- Market penetration in developing countries is limited due to high treatment costs, lack of advanced oncology centers, and limited reimbursement policies

- Intellectual property (IP) and patent challenges for ADC technologies may also hinder entry for smaller biotech firms, as large pharmaceutical companies often hold exclusive rights to critical ADC platforms and linker technologies

- Overcoming these challenges through process optimization, advanced manufacturing techniques, licensing partnerships, and cost-effective delivery platforms is crucial for sustained growth

- Continuous clinical research and real-world evidence generation are needed to demonstrate long-term efficacy and safety, which will boost confidence among physicians, patients, and payers

Topoisomerase-I Payload ADC Drugs Market Scope

The market is segmented on the basis of payload type, antibody type, and linker technology.

• By Payload Type

On the basis of payload type, the Topoisomerase-I Payload ADC Drugs market is segmented into SN-38, DXd, Camptothecin Derivatives, Indenoisoquinolines, and Others. The SN-38 segment dominated the largest market revenue share of 44.1% in 2025, driven by its proven efficacy in targeting DNA topoisomerase-I in cancer cells and established clinical success. SN-38, the active metabolite of irinotecan, is widely used in the development of antibody-drug conjugates (ADCs) due to its potent cytotoxicity and compatibility with multiple linker technologies. Leading pharmaceutical companies are focusing on SN-38-based ADCs for solid tumors such as breast, colorectal, and lung cancers, which further supports adoption. Clinical trials demonstrating improved safety and therapeutic index have reinforced confidence in SN-38 payloads. The payload’s compatibility with both monoclonal and bispecific antibodies enables flexible ADC design. Ongoing regulatory approvals and expanded treatment indications boost commercial utilization. SN-38 ADCs benefit from established manufacturing processes and scalable production. Strong pipeline activity, supportive patent protection, and strategic collaborations among biotech companies continue to reinforce dominance. Its predictable pharmacokinetics and reduced systemic toxicity make it a preferred choice for oncology ADCs. The segment maintains strong adoption across North America, Europe, and Asia-Pacific markets, reflecting high clinical trust and commercial penetration.

The DXd segment is anticipated to witness the fastest CAGR of 22.5% from 2026 to 2033, driven by its superior potency and targeted delivery capabilities. DXd-based ADCs, developed by innovative pharmaceutical companies, have demonstrated remarkable efficacy in preclinical and clinical trials for breast, gastric, and lung cancers. Its high stability in circulation, controlled payload release, and compatibility with cleavable linkers enable precise tumor targeting while minimizing off-target toxicity. Growing approvals in multiple oncology indications accelerate adoption. DXd payloads are increasingly incorporated into next-generation ADCs with enhanced linker and antibody engineering. Rising investment in research for difficult-to-treat solid tumors and the push for precision oncology further fuels market growth. Its adoption is supported by strategic collaborations between biotech firms and large pharma companies. Increasing patient preference for ADCs with improved safety and effectiveness contributes to the rapid uptake. North America and Europe remain the largest markets, while Asia-Pacific is witnessing accelerated clinical trial activity. DXd payloads are expected to dominate the innovation pipeline, supporting high CAGR during the forecast period. Overall, DXd represents the fastest-growing and most innovative segment of the Topoisomerase-I ADC market.

• By Antibody Type

On the basis of antibody type, the market is segmented into Monoclonal Antibody, Bispecific Antibody, and Others. The Monoclonal Antibody segment dominated the largest market revenue share of 61.3% in 2025, driven by its well-established clinical success, broad regulatory acceptance, and proven safety profile. Monoclonal antibodies (mAbs) serve as effective targeting moieties for Topoisomerase-I payloads, delivering cytotoxic drugs directly to tumor cells with high specificity. The majority of approved and late-stage ADCs utilize mAbs due to predictable pharmacokinetics, scalable manufacturing, and strong clinical validation. Their high affinity to tumor-associated antigens reduces off-target effects and enhances therapeutic outcomes. Leading oncology ADC programs heavily rely on monoclonal antibodies for solid tumors such as breast, ovarian, and lung cancers. The segment benefits from long-standing investment in antibody engineering and optimized Fc-region modifications to enhance stability, half-life, and immune system engagement. Strategic partnerships, licensing agreements, and collaborations further support widespread adoption. The segment is strongly established in North America and Europe, with emerging adoption in Asia-Pacific markets. Regulatory approvals, clinical trial pipelines, and commercial production experience maintain the dominance of monoclonal antibody-based Topoisomerase-I ADCs.

The Bispecific Antibody segment is expected to witness the fastest CAGR of 24.1% from 2026 to 2033, fueled by its innovative approach to simultaneously target multiple tumor antigens or engage immune cells. Bispecific antibodies improve the therapeutic window, enable dual mechanisms of action, and allow ADCs to overcome resistance mechanisms seen with traditional monoclonal antibodies. The segment is gaining traction in clinical trials for hematological malignancies and solid tumors. Technological advancements in antibody design, linker optimization, and payload conjugation accelerate adoption. Increased collaboration between biotech innovators and large pharmaceutical firms drives pipeline expansion. The bispecific approach is expected to address unmet clinical needs in difficult-to-treat cancers. Rising investment in precision oncology, targeted therapies, and immuno-oncology combinations further supports growth. Adoption is boosted by regulatory guidance encouraging novel therapies. North America and Asia-Pacific are leading regions for bispecific ADC development. The segment’s high innovation potential and clinical benefits underpin its status as the fastest-growing antibody type.

• By Linker Technology

On the basis of linker technology, the market is segmented into Cleavable Linker, Non-Cleavable Linker, and Others. The Cleavable Linker segment dominated the largest market revenue share of 57.6% in 2025, owing to its ability to release payloads specifically inside target cells while minimizing systemic toxicity. Cleavable linkers are widely used in Topoisomerase-I ADCs to ensure controlled and effective drug release upon reaching the tumor microenvironment. They are compatible with a variety of payloads, including SN-38, DXd, and Camptothecin derivatives. The segment benefits from extensive clinical validation, regulatory approvals, and established manufacturing processes. Cleavable linkers contribute to improved therapeutic index, high efficacy, and predictable pharmacokinetics, supporting adoption across approved ADCs. Leading oncology programs utilize cleavable linkers to target breast, colorectal, and lung cancers. The segment’s dominance is reinforced by optimized conjugation chemistry, stability in circulation, and enhanced tumor penetration. Strategic collaborations and licensing of linker technologies further accelerate growth. Strong pipeline activity for new ADC candidates ensures sustained demand. Cleavable linkers also support combination therapies and multi-drug strategies. Regional adoption is highest in North America and Europe, with rapid expansion in Asia-Pacific clinical trials. Overall, cleavable linkers remain the most widely used and clinically trusted technology.

The Non-Cleavable Linker segment is anticipated to witness the fastest CAGR of 21.9% from 2026 to 2033, driven by increasing focus on enhancing safety and reducing off-target toxicity in next-generation ADCs. Non-cleavable linkers provide highly stable conjugation, preventing premature payload release in circulation. Their adoption is growing in oncology programs for solid tumors where controlled release improves therapeutic outcomes. Pharmaceutical companies are actively exploring non-cleavable linker ADCs for combination therapies and personalized medicine. Rising clinical trials targeting rare cancers and difficult-to-treat malignancies support rapid market growth. Technological advances in antibody engineering and linker chemistry enhance efficacy and stability. Non-cleavable linkers offer a longer half-life and better tolerability, making them attractive for sensitive patient populations. Strategic partnerships and licensing initiatives further boost adoption. Increasing use in bispecific antibody-based ADCs also accelerates growth. Adoption is growing in North America, Europe, and Asia-Pacific. The segment represents innovation in precision oncology ADC design, supporting high projected CAGR.

Topoisomerase-I Payload ADC Drugs Market Regional Analysis

- North America dominated the Topoisomerase‑I Payload ADC Drugs market with the largest revenue share of approximately 42% in 2025. This strong position is supported by a robust biopharmaceutical ecosystem, high R&D investment, advanced healthcare infrastructure, and early adoption of targeted oncology therapies

- The markket leads this regional dominance, driven by leading pharmaceutical and biotech companies, extensive clinical trial networks, and favorable regulatory frameworks. The presence of major players such as ImmunoGen, Daiichi Sankyo, and Seagen, coupled with supportive reimbursement policies, has accelerated the uptake of Topoisomerase‑I ADCs for cancers including breast, ovarian, and colorectal

- In addition, the well-established healthcare infrastructure facilitates rapid commercialization and patient access to innovative therapies

U.S. Topoisomerase-I Payload ADC Drugs Market Insight

The U.S. Topoisomerase‑I Payload ADC Drugs market captured the largest revenue share within North America in 2025, fueled by extensive clinical trials, early adoption of novel therapies, and strong collaborations between pharmaceutical companies and research institutions. High awareness of precision oncology and a growing preference for targeted treatment options have contributed to the adoption of Topoisomerase‑I Payload ADCs. Furthermore, investments in biomarker-driven patient stratification and personalized medicine approaches are enabling improved efficacy and safety profiles, enhancing market growth. The presence of advanced manufacturing facilities and regulatory incentives such as FDA Breakthrough Therapy designation further strengthen the U.S. market.

Europe Topoisomerase-I Payload ADC Drugs Market Insight

The Europe Topoisomerase‑I Payload ADC Drugs market is projected to expand at a substantial CAGR during the forecast period. Market growth is primarily driven by increasing cancer prevalence, stringent healthcare regulations, and rising demand for advanced targeted therapies. Key markets such as Germany, the U.K., and France are witnessing higher adoption rates due to the presence of specialized oncology centers, advanced clinical trial infrastructure, and supportive reimbursement frameworks. European pharmaceutical companies are actively investing in research and development of novel ADCs, further boosting regional market expansion.

U.K. Topoisomerase-I Payload ADC Drugs Market Insight

The U.K. Topoisomerase‑I Payload ADC Drugs market is anticipated to grow at a noteworthy CAGR, supported by a well-established healthcare system, increasing cancer incidence, and high expenditure on oncology treatments. National Health Service (NHS) initiatives for early cancer detection and precision medicine are encouraging the use of advanced therapies such as Topoisomerase‑I ADCs. Additionally, the country’s strong clinical research network and collaborations between biotech firms and hospitals facilitate rapid clinical adoption of novel ADCs.

Germany Topoisomerase-I Payload ADC Drugs Market Insight

Germany Topoisomerase‑I Payload ADC Drugs market is expected to be one of the fastest-growing markets in Europe due to expanding oncology infrastructure, increasing investments in drug development, and rising awareness of precision therapies among clinicians and patients. The country’s focus on innovation, coupled with well-developed manufacturing capabilities and a favorable regulatory environment, supports the introduction and commercialization of Topoisomerase‑I ADCs. Growth is further aided by government funding for cancer research and strong hospital networks capable of administering targeted therapies.

Asia-Pacific Topoisomerase-I Payload ADC Drugs Market Insight

The Asia-Pacific Topoisomerase‑I Payload ADC Drugs market is expected to be the fastest-growing region during the forecast period. Growth is fueled by increasing cancer incidence, rising healthcare expenditure, expanding pharmaceutical manufacturing capabilities, and growing participation in global clinical trials. Key countries contributing to this growth include China, Japan, and India. Improving healthcare infrastructure, higher access to oncology care, and government initiatives supporting precision medicine and local biopharma development are enabling rapid adoption of Topoisomerase‑I ADCs.

Japan Topoisomerase-I Payload ADC Drugs Market Insight

The Japanese Topoisomerase‑I Payload ADC Drugs market is witnessing significant growth due to a high prevalence of cancer, advanced healthcare infrastructure, and an emphasis on precision oncology. The adoption of Topoisomerase‑I ADCs is further supported by strong clinical research capabilities, government support for innovative therapies, and an increasing focus on patient-specific treatments. Collaborations between domestic biotech firms and international pharmaceutical companies are accelerating clinical development and market availability of new ADCs.

China Topoisomerase-I Payload ADC Drugs Market Insight

China Topoisomerase‑I Payload ADC Drugs market accounted for a significant share of the Asia-Pacific Topoisomerase‑I Payload ADC Drugs market in 2025. The country’s expanding middle class, increasing cancer prevalence, rising healthcare spending, and strong government initiatives promoting local biopharmaceutical innovation are driving market growth. China’s participation in global clinical trials and the emergence of local manufacturing hubs for ADCs are also supporting broader accessibility and adoption of Topoisomerase‑I ADC therapies across the country.

Topoisomerase-I Payload ADC Drugs Market Share

The Topoisomerase-I Payload ADC Drugs industry is primarily led by well-established companies, including:

- Daiichi Sankyo Company, Limited (Japan)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Roche Holding AG (Switzerland)

- AstraZeneca plc (U.K.)

- Genentech, Inc. (U.S.)

- Mersana Therapeutics, Inc. (U.S.)

- MedImmune (U.S.)

- Synaffix B.V. (Netherlands)

- Sorrento Therapeutics, Inc. (U.S.)

- Stemcentrx (U.S.)

- Immunomedics, Inc. (U.S.)

- BioNTech SE (Germany)

- RemeGen Co., Ltd. (China)

- Zymeworks Inc. (Canada)

- AbbVie Biotherapeutics (U.S.)

- Catalent, Inc. (U.S.)

Latest Developments in Global Topoisomerase-I Payload ADC Drugs Market

- In December 2021, the U.S. Food and Drug Administration (FDA) granted Breakthrough Therapy Designation to patritumab deruxtecan, an investigational antibody‑drug conjugate (ADC) combining Daiichi Sankyo’s proprietary DXd topoisomerase‑I inhibitor payload with a HER3‑targeting monoclonal antibody, for the treatment of patients with EGFR‑mutated locally advanced or metastatic non‑small cell lung cancer (NSCLC). This designation recognized the promising early clinical efficacy and potential to address an unmet treatment need in this patient population

- In October 2023, Daiichi Sankyo and Merck & Co. entered a global collaboration to develop and commercialize three DXd‑based ADC candidates including patritumab deruxtecan (HER3‑DXd), ifinatamab deruxtecan (I‑DXd, targeting B7‑H3), and raludotatug deruxtecan (R‑DXd, targeting CDH6). This partnership expanded the global clinical development program for topoisomerase‑I payload ADCs across multiple solid tumor indications

- In January 2025, the FDA approved datopotamab deruxtecan‑dlnk (Datroway) for adult patients with unresectable or metastatic hormone receptor‑positive, HER2‑negative breast cancer who have received prior endocrine therapy and chemotherapy. Datroway uses Daiichi Sankyo’s DXd topoisomerase‑I inhibitor payload linked to an anti‑TROP2 antibody and represents a key regulatory milestone for topoisomerase‑I ADCs in new breast cancer subtypes

- In April 2025, Datroway (datopotamab deruxtecan) also secured European Union approval for the same indication — unresectable or metastatic HR‑positive, HER2‑negative breast cancer — broadening its global regulatory footprint and treatment availability for patients across major markets

- In June 2025, the Phase III IDEATE‑Lung02 trial of ifinatamab deruxtecan (I‑DXd) was initiated in patients with relapsed small cell lung cancer (SCLC), representing a significant step for topoisomerase‑I payload ADCs into late‑stage clinical evaluation in a difficult‑to‑treat tumor type. Ifinatamab is also advancing into a Phase III program for metastatic castration‑resistant prostate cancer — illustrating expansion into multiple oncology areas

- In September 2025, the investigational DXd‑based ADC raludotatug deruxtecan (R‑DXd) received Breakthrough Therapy Designation from the FDA for the treatment of platinum‑resistant ovarian, primary peritoneal, or fallopian tube cancers expressing CDH6, reinforcing momentum in topoisomerase‑I ADC development for rare and resistant tumors

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.