Global Total Lab Automation Market

Market Size in USD Billion

USD

6.91 Billion

USD

12.41 Billion

2025

2033

USD

6.91 Billion

USD

12.41 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.91 Billion | |

| USD 12.41 Billion | |

| % | |

|

Total Lab Automation Market Overview

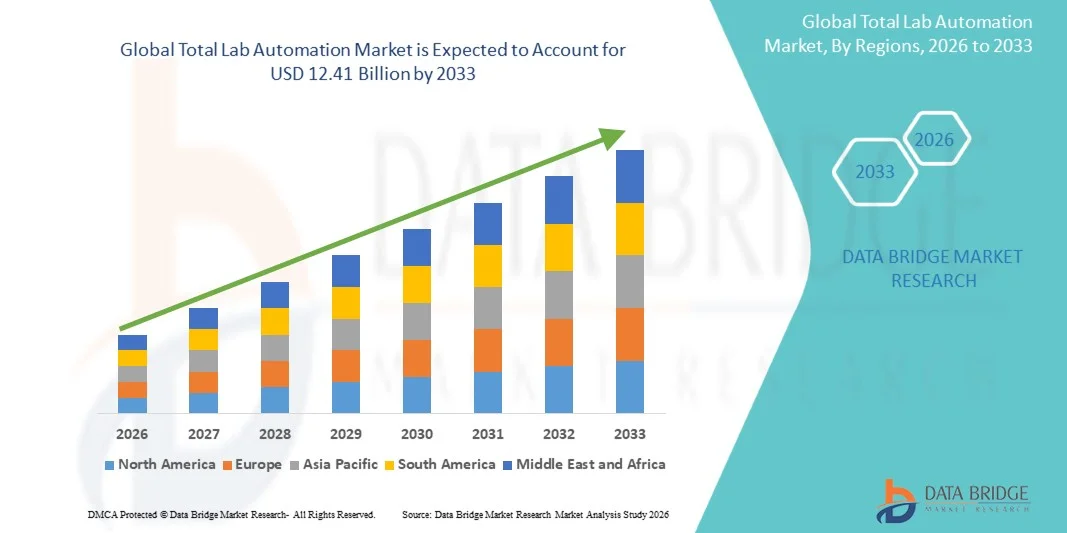

The Total Lab Automation Market was valued at USD 6.91 billion in 2025 and is projected to reach USD 12.41 billion by 2033, growing at a CAGR of 7.60% from 2026 to 2033. The market is witnessing steady expansion driven by rising demand for high-throughput laboratory workflows, increasing pressure to improve diagnostic accuracy, and growing adoption of automation across clinical, pharmaceutical, and research laboratories.

The growing burden of chronic diseases, coupled with increasing volumes of diagnostic testing and drug discovery activities, is encouraging laboratories to shift toward fully integrated automation systems. Advances in robotics, artificial intelligence, and laboratory information management systems (LIMS) are enabling seamless sample handling, reduced human error, and faster turnaround times. As healthcare systems and life sciences organizations focus on efficiency, scalability, and data-driven decision-making, total lab automation solutions are becoming a key component of modern laboratory infrastructure.

Key Market Trends & Insights

- North America dominated the Total Lab Automation Market with the largest revenue share of 38.6% in 2025, supported by strong pharmaceutical R&D expenditure, advanced healthcare infrastructure, and early adoption of integrated laboratory technologies.

- The Automated Liquid Handlers segment led the market with a 34.9% share in 2025, driven by their critical role in high-throughput sample preparation, precision pipetting, and reduction of manual errors in laboratory workflows.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.8% from 2026 to 2033, fueled by expanding healthcare infrastructure, growing biotech investments, and rapid laboratory modernization in China, India, and Japan.

- Automated Storage and Retrieval Systems (ASRS) are the fastest-growing equipment type, projected to register a CAGR of 8.3%, reflecting the surge in demand for efficient sample tracking, long-term storage automation, and space optimization in high-volume laboratories.

- The Laboratory Information Management System (LIMS) segment dominated the software type category with a 38.7% revenue share in 2025, led by central role in managing laboratory workflows, sample tracking, data integration, and regulatory compliance.

- Clinical Diagnostics deployment accounted for 42.3% of the market, preferred by increasing test volumes, rising prevalence of chronic and infectious diseases, and growing demand for rapid diagnostic turnaround.

- The Genomics segment is the fastest-growing application category, with a CAGR of 9.0%, driven by the rapid expansion in sequencing technologies and personalized medicine applications.

Market Size & Forecast

- Global Market Value (2025): USD 6.91 Billion

- Expected Market Value (2033): USD 12.41 Billion

- Forecast CAGR (2026–2033): 7.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Total Lab Automation Market Segmentation

|

Attributes |

Total Lab Automation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· F. Hoffmann-La Roche Ltd (Switzerland) · Thermo Fisher Scientific Inc. (U.S.) · Danaher (U.S.) · Beckman Coulter, Inc. (U.S.) · Siemens Healthineers AG (Germany) · Abbott (U.S.) · Agilent Technologies, Inc. (U.S.) · Bio-Rad Laboratories, Inc. (U.S.) · BD (U.S.) · Revvity, Inc. (U.S.) · Waters Corporation (U.S.) · Illumina, Inc. (U.S.) · Sartorius AG (Germany) · Tecan Group Ltd. (Switzerland) · Hamilton Company (U.S.) · Eppendorf SE (Germany) · Shimadzu Corporation (Japan) · Sysmex Corporation (Japan) · QIAGEN (Netherlands) · Mettler-Toledo International Inc. (U.S.) |

|

Market Opportunities |

· Growing opportunity in fully integrated “walk-away” laboratories · Expansion of lab automation in emerging biotech hubs · Increasing demand for AI-enabled predictive lab workflows |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Total Lab Automation Market Trends

Trend: Rising Adoption of Integrated High-Throughput Laboratory Systems

Clinical and research laboratories are increasingly shifting toward fully integrated automation platforms that combine sample handling, processing, and analysis within a unified workflow to improve efficiency and reduce turnaround times. The integration of robotics, automated analyzers, and Laboratory Information Management Systems is enabling continuous, error-free operations in high-volume diagnostic and pharmaceutical environments. AI-driven data interpretation and real-time workflow monitoring are further enhancing reproducibility and scalability across complex laboratory processes, while modular automation systems are allowing flexible expansion based on testing demand. For instance, Roche’s cobas automation platforms and Thermo Fisher’s automated lab systems illustrate large-scale deployment of end-to-end laboratory integration in clinical diagnostics and life sciences research.

Total Lab Automation Market Dynamics

Key Market Driver: Increasing Demand for High-Volume Diagnostic and Drug Discovery Automation

The rising burden of chronic diseases and expanding pharmaceutical R&D pipelines are significantly increasing laboratory workloads, driving strong demand for automated systems that can process large sample volumes with speed and precision. Laboratories are adopting total automation to minimize manual intervention, reduce error rates, and accelerate diagnostic reporting and compound screening processes. This shift is further supported by advancements in robotics, AI-based analytics, and integrated software platforms that enable seamless coordination of laboratory instruments and workflows. For instance, widespread adoption of automated clinical chemistry and immunoassay platforms in large hospital networks and pharma companies highlights the growing reliance on scalable lab automation solutions.

Key Restraint/Challenge: High Capital Investment and Complex System Integration Requirements

A major challenge in the total lab automation market is the high upfront cost associated with deploying fully integrated automation systems, including robotics, software platforms, and specialized instrumentation. The complexity of integrating automation solutions with existing laboratory infrastructure and legacy systems further increases implementation time and operational disruption. In addition, ongoing costs related to maintenance, software upgrades, and technical training limit adoption among small and mid-sized laboratories.

For instance, large-scale automation installations in centralized diagnostic laboratories demonstrate significant capital intensity, often restricting adoption to well-funded hospital chains, pharmaceutical companies, and research institutions.

Key Market Opportunity: Expansion of AI-Driven Cloud-Based Laboratory Automation Platforms

The integration of artificial intelligence and cloud computing into laboratory automation systems presents a significant growth opportunity by enabling remote monitoring, predictive analytics, and intelligent workflow optimization. These technologies allow laboratories to manage data centrally, improve decision-making accuracy, and scale operations without proportional increases in physical infrastructure. Cloud-based automation also supports collaboration across geographically distributed research facilities and contract research organizations. For instance, AI-enabled digital laboratory platforms used in pharmaceutical research networks demonstrate how cloud-integrated automation is enhancing efficiency, scalability, and global accessibility of advanced laboratory operations.

Total Lab Automation Market Scope

The total lab automation market is segmented on the basis of equipment type, software type, application, and end user.

- By Equipment Type

On the basis of equipment type, the Total Lab Automation Market is segmented into automated liquid handlers, automated plate handlers, robotic arms, automated storage and retrieval systems (ASRS), and analyzers. The Automated Liquid Handlers segment dominated the market with a 34.9% share in 2025, driven by their critical role in high-throughput sample preparation, precision pipetting, and reduction of manual errors in laboratory workflows. These systems are widely adopted in pharmaceutical R&D and clinical diagnostics due to their ability to handle repetitive liquid transfer tasks with high accuracy. They significantly improve reproducibility in drug discovery and molecular biology applications. Increasing integration with robotics and LIMS platforms is further strengthening workflow efficiency. Their scalability across small and large laboratories also supports widespread adoption. Continuous advancements in miniaturization and multi-channel dispensing are reinforcing their market leadership.

The Automated Storage and Retrieval Systems (ASRS) segment is expected to register the fastest growth at a CAGR of 8.3% from 2026 to 2033, driven by rising demand for efficient sample tracking, long-term storage automation, and space optimization in high-volume laboratories. These systems enable secure, temperature-controlled storage with rapid retrieval capabilities, reducing sample loss and improving operational efficiency. Increasing biobanking activities and large-scale genomic research projects are accelerating adoption. Integration with AI-based inventory management systems is further enhancing accuracy and traceability. Growing need for 24/7 unattended laboratory operations is also supporting demand. Rising investments in centralized diagnostic and research facilities are strengthening deployment across developed and emerging markets.

- By Software Type

On the basis of software type, the Total Lab Automation Market is segmented into Laboratory Information Management System (LIMS), Laboratory Information System (LIS), Chromatography Data System (CDS), Electronic Lab Notebook (ELN), and Scientific Data Management System (SDMS). The Laboratory Information Management System (LIMS) segment dominated the market with a 38.7% share in 2025, due to its central role in managing laboratory workflows, sample tracking, data integration, and regulatory compliance. LIMS solutions are widely used across pharmaceutical, biotechnology, and clinical laboratories to ensure standardized operations and audit readiness. They enable seamless coordination between automated instruments and digital platforms. Increasing regulatory pressure for data integrity and traceability is further strengthening adoption. Integration with AI and cloud-based systems is enhancing real-time data visibility. Continuous upgrades toward interoperable and scalable platforms are reinforcing its dominance.

The Scientific Data Management System (SDMS) segment is expected to register the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by the exponential growth of complex scientific data generated from genomics, proteomics, and drug discovery workflows. SDMS platforms enable centralized storage, organization, and analysis of large datasets generated by automated laboratory instruments. Increasing demand for advanced analytics and AI-driven insights is accelerating adoption. Growing need for data harmonization across multi-site research organizations is further supporting growth. Integration with cloud computing and machine learning tools is enhancing predictive research capabilities. Rising focus on digital transformation in life sciences is also driving rapid adoption globally.

- By Application

On the basis of application, the Total Lab Automation Market is segmented into drug discovery, genomics, proteomics, protein engineering, bioanalysis, analytical chemistry, clinical diagnostics, and other applications. The Clinical Diagnostics segment dominated the market with a 42.3% share in 2025, driven by increasing test volumes, rising prevalence of chronic and infectious diseases, and growing demand for rapid diagnostic turnaround. Automated systems are widely used in hospital laboratories to improve accuracy and efficiency in blood testing, immunoassays, and molecular diagnostics. Rising pressure on healthcare systems to process high sample volumes is further supporting adoption. Integration of automation with diagnostic analyzers is improving workflow speed and reliability. Expanding laboratory networks in both developed and emerging economies is strengthening demand. Continuous advancements in precision diagnostics are reinforcing segment leadership.

The Genomics segment is expected to register the fastest growth at a CAGR of 9.0% from 2026 to 2033, driven by rapid expansion in sequencing technologies and personalized medicine applications. Total lab automation enables high-throughput genomic sample processing with improved accuracy and reduced turnaround time. Increasing use of next-generation sequencing (NGS) is accelerating automation requirements. Large-scale population genomics projects are further boosting demand. Integration of AI-driven bioinformatics tools is enhancing data interpretation capabilities. Growing investments in precision medicine research are also contributing to strong segment expansion.

- By End User

On the basis of end user, the Total Lab Automation Market is segmented into biotechnology and pharmaceuticals, and diagnostic labs. The Biotechnology and Pharmaceuticals segment dominated the market with a 46.1% share in 2025, driven by extensive use of automation in drug discovery, compound screening, clinical trials, and quality control processes. These organizations rely on high-throughput systems to accelerate R&D pipelines and reduce time-to-market. Increasing complexity of biologics and precision medicines is further driving automation adoption. Integration with AI-based drug discovery platforms is enhancing efficiency and success rates. Strong investment capacity allows deployment of advanced integrated laboratory systems. Continuous innovation in pharmaceutical R&D workflows is reinforcing segment dominance.

The Diagnostic Labs segment is expected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by rising demand for centralized testing services and increasing outsourcing of diagnostic processes. Growing patient load and chronic disease prevalence are pushing labs to adopt automation for faster turnaround and reduced operational costs. Expansion of large-scale diagnostic chains is further supporting adoption. Integration with digital health platforms is improving efficiency and data management. Increasing need for standardized, high-volume testing is also accelerating growth. Government initiatives to strengthen diagnostic infrastructure are further boosting adoption globally.

Total Lab Automation Market Regional Analysis

North America dominated the Total Lab Automation Market with the largest revenue share of 38.6% in 2025, supported by strong pharmaceutical R&D expenditure, advanced healthcare infrastructure, and early adoption of integrated laboratory technologies. The region also benefits from the presence of leading life science companies, high penetration of LIMS and AI-enabled laboratory platforms, and strong regulatory emphasis on data accuracy and compliance. Increasing demand for high-throughput drug discovery, clinical diagnostics, and precision medicine continues to strengthen North America’s leadership position in the global market.

U.S. Total Lab Automation Market Insight

The U.S. total lab automation market is witnessing strong growth due to rising investments in pharmaceutical R&D, advanced clinical diagnostics infrastructure, and increasing adoption of AI-driven laboratory technologies. The country’s mature life sciences ecosystem, along with widespread deployment of LIMS, robotic systems, and integrated automation platforms, is driving demand across drug discovery, genomics, and clinical testing applications. In addition, growing emphasis on improving laboratory efficiency, reducing turnaround times, and enhancing data accuracy is accelerating automation adoption across hospitals, diagnostic labs, and biotechnology companies.

Europe Total Lab Automation Market Insight

The Europe total lab automation market remains a major contributor to global revenue, driven by strong regulatory frameworks, advanced healthcare systems, and high adoption of standardized laboratory automation solutions. The widespread use of automated systems in pharmaceutical research, clinical diagnostics, and academic laboratories is supporting market expansion across the region. Increasing investments in digital laboratory transformation, coupled with strong focus on data integrity and quality compliance, continue to enhance adoption. Growing demand for precision medicine and high-throughput screening further strengthens Europe’s position in the global market.

U.K. Total Lab Automation Market Insight

The U.K. total lab automation market is experiencing steady growth, supported by rising adoption of digital laboratory systems in pharmaceutical research, clinical diagnostics, and biotechnology applications. Increasing investments in AI-enabled laboratory platforms and cloud-based data management systems are contributing to market expansion. Furthermore, strong presence of research institutions and growing demand for efficient diagnostic workflows are accelerating automation adoption. The integration of LIMS, ELN, and SDMS platforms is improving laboratory efficiency and positioning the U.K. as a key innovation hub in laboratory automation.

Germany Total Lab Automation Market Insight

The Germany total lab automation market is expanding steadily due to the country’s strong pharmaceutical manufacturing base, advanced engineering capabilities, and increasing adoption of high-precision laboratory technologies. Pharmaceutical companies, research institutes, and diagnostic laboratories are increasingly deploying automated liquid handling systems, robotic platforms, and integrated software solutions for R&D and testing activities. Continuous advancements in robotics, AI integration, and data-driven laboratory workflows, along with strong emphasis on quality control and regulatory compliance, are further driving market growth in Germany.

Asia-Pacific Total Lab Automation Market Insight

The Asia-Pacific total lab automation market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising biotechnology investments, and increasing demand for high-throughput diagnostic and research solutions across countries such as China, India, and Japan. Growing awareness of laboratory efficiency, rising chronic disease burden, and increasing adoption of digital healthcare systems are supporting regional market expansion. In addition, the growing presence of contract research organizations and pharmaceutical manufacturing hubs is accelerating automation adoption across clinical and research laboratories.

Japan Total Lab Automation Market Insight

The Japan total lab automation market is witnessing consistent growth due to rising investments in advanced healthcare technologies, pharmaceutical innovation, and precision diagnostics. Laboratory automation systems are increasingly being adopted across hospitals, biotech firms, and research institutes for high-accuracy testing and efficient workflow management. Moreover, increasing integration of robotics, AI-based analytics, and digital laboratory platforms is further contributing to market growth. The country’s strong focus on efficiency, quality control, and technological advancement continues to strengthen adoption across laboratory environments.

China Total Lab Automation Market Insight

The China total lab automation market is growing rapidly, driven by increasing healthcare modernization, expanding pharmaceutical R&D activities, and rising demand for efficient diagnostic services. Growing adoption of AI-enabled laboratory systems, automated analyzers, and integrated data management platforms is significantly boosting market demand. In addition, strong government support for biotechnology development, increasing investments in precision medicine, and rapid expansion of clinical laboratory networks are positioning China as one of the fastest-growing markets for total lab automation globally.

Total Lab Automation Market Share

The total lab automation industry is primarily led by well-established companies, including:

- Hoffmann-La Roche Ltd (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher (U.S.)

- Beckman Coulter, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Abbott (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- BD (U.S.)

- Revvity, Inc. (U.S.)

- Waters Corporation (U.S.)

- Illumina, Inc. (U.S.)

- Sartorius AG (Germany)

- Tecan Group Ltd. (Switzerland)

- Hamilton Company (U.S.)

- Eppendorf SE (Germany)

- Shimadzu Corporation (Japan)

- Sysmex Corporation (Japan)

- QIAGEN (Netherlands)

- Mettler-Toledo International Inc. (U.S.)

Latest Developments in Total Lab Automation Market

- In March 2024, Roche announced advancements in its cobas® integrated laboratory automation and diagnostics platform, focusing on improved connectivity, workflow efficiency, and system integration across clinical laboratories. The updates enhance high-throughput testing capabilities and support better data management across laboratory networks. These innovations are widely applied in clinical chemistry and immunodiagnostics workflows. This reinforces Roche’s leadership in fully integrated laboratory automation ecosystems

- In October 2023, Danaher Corporation, through its subsidiary Beckman Coulter Life Sciences, introduced enhancements to its laboratory automation and liquid handling workflow systems. The updates are designed to improve scalability, precision, and integration across complex laboratory environments, particularly in pharmaceutical and biotechnology research applications. These advancements support faster and more reproducible experimental workflows. This development underscores Danaher’s continued investment in next-generation laboratory automation technologies

- In April 2023, Thermo Fisher Scientific announced continued expansion of its laboratory automation and workflow solutions portfolio, strengthening its capabilities in integrated diagnostics and life sciences research. The enhancements focus on improving end-to-end sample processing, data connectivity, and laboratory efficiency through automated systems and digital integration. These developments support high-throughput research and clinical testing environments. This reflects Thermo Fisher’s strategy to accelerate digital transformation in laboratory operations globally

- In June 2022, Siemens Healthineers expanded its Atellica® Solution portfolio with enhanced automation and integrated diagnostic capabilities for clinical laboratories. The upgrade strengthens high-speed sample processing, workflow consolidation, and interoperability across laboratory instruments. The solution is widely used in hospital and reference laboratories to improve turnaround time and operational efficiency. This expansion reinforces Siemens Healthineers’ position in scalable laboratory automation and diagnostic workflow optimization

- In September 2021, BD (Becton, Dickinson and Company), a leading medical technology company, announced the expansion and commercialization of its BD COR™ system for high-throughput molecular diagnostics automation in clinical laboratories. The system is designed to automate complex molecular testing workflows, improving efficiency, reducing manual intervention, and enhancing result accuracy in infectious disease and women’s health testing. This development highlights BD’s focus on advancing fully integrated diagnostic automation platforms to support increasing laboratory testing demand

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.