Global Trauma Care Centers Market

Market Size in USD Billion

USD

25.38 Billion

USD

39.84 Billion

2025

2033

USD

25.38 Billion

USD

39.84 Billion

2025

2033

| 2026 - 2033 | |

| USD 25.38 Billion | |

| USD 39.84 Billion | |

| % | |

|

Trauma Care Centers Market Overview

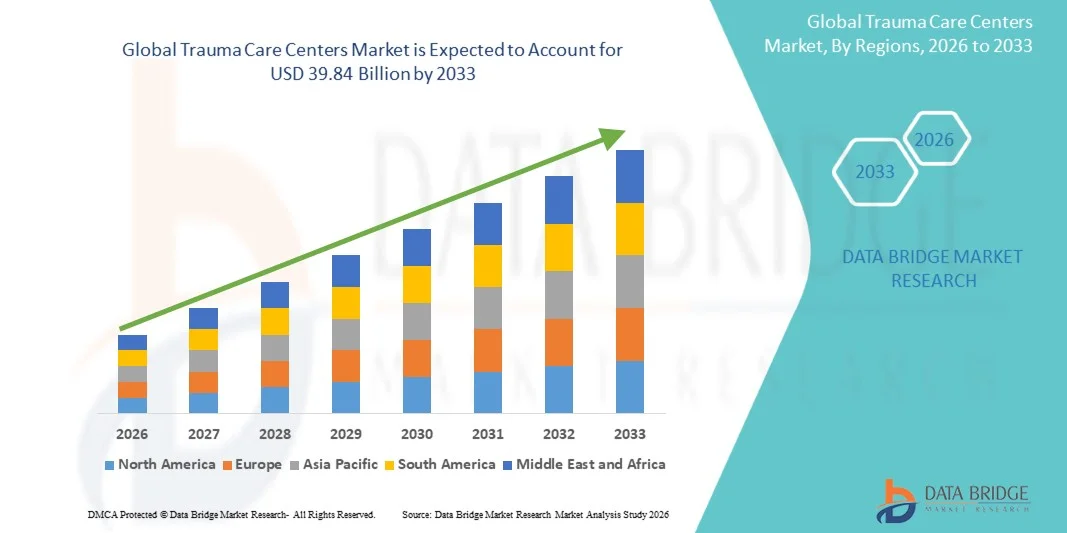

The Trauma Care Centers Market was valued at USD 25.38 billion in 2025 and is projected to reach USD 39.84 billion by 2033, growing at a CAGR of 5.80% from 2026 to 2033. The Trauma Care Centers Market is experiencing steady growth driven by the rising incidence of traumatic injuries, increasing road traffic accidents, growing prevalence of falls and workplace injuries, and expanding investments in emergency healthcare infrastructure worldwide.

The growing burden of trauma-related emergencies, coupled with increasing awareness regarding the importance of timely and specialized trauma management, is encouraging governments and healthcare providers to strengthen trauma care networks and establish advanced trauma centers. Rising urbanization, motorization, and industrial activities have contributed to a higher volume of accident-related injuries requiring immediate medical intervention. Level I and Level II trauma centers are increasingly being equipped with advanced diagnostic imaging systems, emergency surgical facilities, intensive care units, and multidisciplinary trauma teams to improve patient survival outcomes. Furthermore, advancements in emergency medical services (EMS), telemedicine integration, trauma registries, and rapid patient transportation systems are enhancing the efficiency of trauma care delivery. Growing healthcare expenditure, supportive government initiatives for emergency preparedness, and continuous investments in hospital modernization are further accelerating the adoption and expansion of trauma care centers across both developed and emerging regions.

Key Market Trends & Insights

- North America dominated the Trauma Care Centers Market with the largest revenue share of 38.62% in 2025, supported by a well-established emergency healthcare infrastructure, high concentration of Level I and Level II trauma centers, favorable reimbursement frameworks, and significant investments in advanced trauma and critical care services.

- The in-house segment dominated the market with a share of 72.84% in 2025 due to its extensive presence within multispecialty hospitals and tertiary healthcare institutions that offer integrated emergency, surgical, diagnostic, and intensive care services under a single facility.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by increasing road traffic accidents, expanding healthcare infrastructure, rising healthcare expenditure, and growing investments in emergency medical services across China, India, and Southeast Asian countries.

- Level II Trauma Centers are projected to be the fastest-growing trauma center category, registering a CAGR of 7.8%, reflecting increasing efforts by healthcare systems to expand access to specialized trauma care in secondary cities and underserved regions.

- The Road Traffic Injury segment dominated the injury type category with a 36.47% revenue share in 2025, supported by the high global burden of vehicle-related accidents and the urgent need for advanced trauma treatment and rehabilitation services.

- Hospital-Based Trauma Centers accounted for 61.25% of the market in 2025, preferred due to their integrated emergency departments, advanced diagnostic capabilities, specialized surgical teams, and intensive care facilities.

- The Advanced Trauma Care & Surgical Services segment is expected to be the fastest-growing service category, with a CAGR of 8.4%, driven by increasing adoption of minimally invasive trauma procedures, rapid diagnostic technologies, and multidisciplinary approaches to managing complex traumatic injuries.

Market Size & Forecast

- Global Market Value (2025): USD 25.38 Billion

- Expected Market Value (2033): USD 39.84 Billion

- Forecast CAGR (2026–2033): 5.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Trauma Care Centers Market Segmentation

|

Attributes |

Trauma Care Centers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• HCA Healthcare, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Trauma Care Infrastructure in Emerging Economies · Adoption of Advanced Trauma Management Technologies · Growth of Rehabilitation and Post-Trauma Care Services |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Trauma Care Centers Market Trends

Trend: Expansion of Integrated Trauma Systems and Advanced Emergency Care Networks

The Trauma Care Centers Market is witnessing a growing trend toward the development of integrated trauma systems that connect pre-hospital emergency services, trauma centers, rehabilitation facilities, and specialty care providers. Rising trauma incidence worldwide is increasing the need for coordinated emergency response networks capable of delivering rapid and specialized care. According to the World Health Organization (WHO), road traffic injuries cause approximately 1.19 million deaths annually and remain a leading cause of death among individuals aged 5–29 years. Healthcare systems are increasingly investing in Level I and Level II trauma centers equipped with advanced imaging technologies, hybrid operating rooms, telemedicine platforms, and multidisciplinary trauma teams. The adoption of trauma registries and real-time patient monitoring systems is further improving clinical decision-making and patient outcomes. In addition, several countries are expanding regional trauma networks to reduce treatment delays and improve survival rates for critically injured patients.

Trauma Care Centers Market Dynamics

Key Market Driver: Rising Burden of Traumatic Injuries and Increasing Demand for Emergency Medical Services

The growing incidence of traumatic injuries is a major driver of the Trauma Care Centers Market. Road traffic accidents, falls, workplace injuries, violence-related trauma, and sports injuries continue to generate significant demand for specialized trauma services worldwide. According to the WHO, injuries account for more than 4.4 million deaths globally each year, representing nearly 8% of all deaths worldwide. Furthermore, trauma remains one of the leading causes of hospitalization and long-term disability across both developed and developing countries. Governments and healthcare providers are increasingly investing in trauma care infrastructure, emergency medical services (EMS), trauma training programs, and advanced critical care facilities to improve patient outcomes. Growing awareness regarding the importance of the "golden hour" in trauma management and increasing availability of specialized trauma surgeons and emergency physicians are further supporting market growth.

Key Restraint/Challenge: High Operational Costs and Limited Access to Specialized Trauma Care

A significant challenge in the Trauma Care Centers Market is the substantial financial investment required to establish and maintain advanced trauma facilities. Trauma centers require highly trained multidisciplinary teams, sophisticated diagnostic equipment, dedicated operating rooms, intensive care units, blood banks, and 24/7 emergency response capabilities. Maintaining accreditation standards and ensuring continuous staff availability significantly increase operating costs. In many low- and middle-income countries, specialized trauma care facilities remain concentrated in urban areas, limiting access for rural populations. According to the WHO, many developing nations continue to face shortages of emergency care infrastructure and trained trauma professionals, contributing to disparities in trauma outcomes. In addition, reimbursement challenges and healthcare budget constraints can hinder the expansion of trauma care networks, particularly in resource-limited settings.

Key Market Opportunity: Adoption of Digital Health Technologies and Expansion of Trauma Rehabilitation Services

The integration of advanced digital health technologies presents a significant opportunity for the trauma care centers market. Hospitals and trauma centers are increasingly implementing tele-trauma services, AI-assisted imaging analysis, electronic trauma registries, predictive analytics, and remote patient monitoring systems to improve treatment efficiency and clinical outcomes. For example, telemedicine-enabled trauma consultations are helping healthcare providers deliver specialized trauma expertise to remote and underserved regions. Furthermore, growing recognition of the long-term physical and psychological impacts of traumatic injuries is driving investment in comprehensive rehabilitation services, including physical therapy, neurological rehabilitation, occupational therapy, and mental health support. The continued expansion of trauma care infrastructure, coupled with increasing government funding for emergency preparedness and healthcare modernization, is expected to create substantial growth opportunities for market participants during the forecast period.

Trauma Care Centers Market Scope

The Trauma Care Centers market is segmented on the basis of facility type, trauma type, and application.

- By Facility Type

On the basis of facility type, the Trauma Care Centers Market is segmented into in-house and standalone trauma care centers. The in-house segment dominated the market with a share of 72.84% in 2025 due to its extensive presence within multispecialty hospitals and tertiary healthcare institutions that offer integrated emergency, surgical, diagnostic, and intensive care services under a single facility. These centers provide rapid access to specialized trauma surgeons, advanced imaging systems, operating rooms, blood banks, and critical care units, significantly improving patient outcomes. Growing investments in hospital infrastructure, increasing trauma admissions, and rising demand for comprehensive emergency care services are supporting segment growth. In addition, favorable reimbursement structures, availability of multidisciplinary treatment teams, and continuous technological advancements in hospital-based trauma management are reinforcing the dominance of the in-house segment across developed and emerging healthcare markets.

The standalone segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by increasing investments in dedicated emergency care facilities and growing demand for specialized trauma treatment centers outside traditional hospital settings. Rising urbanization, increasing accident rates, and the need to reduce patient overload in large hospitals are accelerating the development of standalone trauma facilities. Furthermore, advancements in emergency response systems, telemedicine integration, and government initiatives to improve trauma care accessibility are expected to support rapid segment expansion.

- By Trauma Type

On the basis of trauma type, the Trauma Care Centers Market is segmented into falls, traffic-related injuries, stab/wound/cut injuries, burn injuries, brain injuries, and others. The traffic-related injuries segment dominated the market with a share of 36.47% in 2025 due to the high global incidence of road traffic accidents and the significant demand for emergency surgical intervention, critical care, and rehabilitation services. According to global health organizations, road traffic injuries remain among the leading causes of death and disability worldwide, particularly among younger populations. The increasing number of motor vehicles, urban congestion, distracted driving, and alcohol-related accidents continue to contribute to rising patient volumes. Trauma centers are expanding specialized trauma surgery units, emergency response teams, and intensive care capabilities to manage severe accident-related injuries effectively. Growing government investments in trauma systems and emergency healthcare infrastructure further strengthen the dominance of this segment.

The brain injuries segment is projected to register the fastest CAGR of 8.3% from 2026 to 2033, driven by increasing cases of traumatic brain injuries resulting from accidents, falls, sports-related incidents, and occupational hazards. Advancements in neurotrauma management, specialized neurosurgical facilities, neuroimaging technologies, and rehabilitation programs are supporting market growth. Rising awareness regarding early intervention and long-term neurological recovery is further accelerating demand for specialized brain injury treatment services.

- By Application

On the basis of application, the Trauma Care Centers Market is segmented into inpatient service, outpatient service, rehabilitation service, and others. The inpatient service segment dominated the market with a share of 58.92% in 2025 due to the large number of severe trauma cases requiring hospitalization, emergency surgery, intensive monitoring, and multidisciplinary treatment. Major traumatic injuries often require extended hospital stays involving trauma surgeons, orthopedic specialists, neurosurgeons, critical care physicians, and rehabilitation professionals. Increasing admissions related to road accidents, falls, burns, and penetrating injuries are driving demand for inpatient trauma services globally. The availability of advanced diagnostic technologies, intensive care units, trauma operating theaters, and comprehensive post-surgical care further strengthens the segment’s leadership position. Growing healthcare expenditure and continuous expansion of trauma care infrastructure are also supporting segment growth.

The rehabilitation service segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by increasing survival rates among trauma patients and growing emphasis on long-term functional recovery. Demand for physical therapy, occupational therapy, neurological rehabilitation, psychological counseling, and post-trauma recovery programs is increasing significantly worldwide. Healthcare providers are increasingly integrating rehabilitation services into trauma care pathways to improve patient outcomes, reduce disability rates, and enhance quality of life. Furthermore, advancements in rehabilitation technologies and increasing awareness regarding comprehensive trauma recovery are expected to accelerate segment growth during the forecast period.

Trauma Care Centers Market Regional Analysis

North America dominated the Trauma Care Centers Market and accounted for the largest revenue share of 38.62% in 2025, supported by a well-established emergency healthcare infrastructure, a high concentration of Level I and Level II trauma centers, and substantial investments in advanced trauma and critical care services. The region benefits from strong emergency medical service (EMS) networks, favorable reimbursement policies, and widespread adoption of advanced diagnostic and surgical technologies. Increasing incidences of road traffic accidents, falls, sports injuries, and trauma-related emergencies continue to drive demand for specialized trauma care. Furthermore, ongoing investments in trauma system modernization, telemedicine integration, and trauma research programs are strengthening North America's leadership position in the global market.

U.S. Trauma Care Centers Market Insight

The U.S. Trauma Care Centers market is witnessing strong growth due to the presence of one of the world's most advanced trauma care systems and a large network of accredited trauma centers. Rising rates of traumatic injuries, increasing healthcare expenditure, and growing adoption of advanced trauma management technologies are driving market expansion. Healthcare providers are investing heavily in emergency care infrastructure, trauma surgery capabilities, critical care units, and rehabilitation services. In addition, increasing utilization of tele-trauma solutions, AI-assisted diagnostics, and advanced patient monitoring systems is enhancing treatment efficiency and patient outcomes across the country.

Europe Trauma Care Centers Market Insight

The Europe Trauma Care Centers market remains a major contributor to global revenue, driven by robust healthcare systems, strong government support for emergency care services, and increasing investments in trauma care infrastructure. The region has a well-developed network of trauma centers and emergency response systems that facilitate rapid treatment of critical injuries. Rising incidences of road accidents, workplace injuries, and an aging population prone to fall-related trauma are supporting market growth. Furthermore, advancements in trauma surgery, emergency medicine, and rehabilitation services continue to improve patient outcomes and drive market expansion across Europe.

U.K. Trauma Care Centers Market Insight

The U.K. Trauma Care Centers market is experiencing steady growth, supported by the country's established Major Trauma Network and ongoing investments in emergency healthcare services. Increasing focus on improving trauma survival rates, reducing treatment delays, and expanding access to specialized trauma care is driving demand for advanced trauma facilities. The integration of digital health technologies, trauma registries, and telemedicine platforms is improving care coordination and operational efficiency. Additionally, government initiatives aimed at strengthening emergency preparedness and trauma response capabilities continue to support market development.

Germany Trauma Care Centers Market Insight

The Germany Trauma Care Centers market is expanding steadily due to its advanced healthcare infrastructure, strong emergency medical services network, and growing investments in trauma management technologies. Hospitals and trauma centers are increasingly adopting advanced imaging systems, minimally invasive surgical procedures, and multidisciplinary trauma care approaches to improve clinical outcomes. Rising road traffic injuries, occupational accidents, and an aging population are contributing to increased demand for specialized trauma services. Furthermore, continuous healthcare modernization initiatives and strong government support are driving market growth across the country.

Asia-Pacific Trauma Care Centers Market Insight

The Asia-Pacific Trauma Care Centers market is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by increasing road traffic accidents, expanding healthcare infrastructure, rising healthcare expenditure, and growing investments in emergency medical services across China, India, and Southeast Asian countries. Rapid urbanization, population growth, and increasing awareness regarding trauma management are supporting demand for advanced trauma care facilities. Governments across the region are investing in hospital modernization, emergency response systems, and trauma center development to address the growing burden of traumatic injuries. The expansion of private healthcare providers and increasing access to specialized trauma services are further accelerating market growth.

Japan Trauma Care Centers Market Insight

The Japan Trauma Care Centers market is witnessing consistent growth due to increasing investments in emergency medicine, advanced trauma surgery, and critical care infrastructure. The country's aging population has contributed to rising incidences of fall-related injuries, while continued emphasis on disaster preparedness and emergency response capabilities is supporting demand for specialized trauma services. Healthcare providers are increasingly integrating advanced imaging technologies, robotic-assisted procedures, and telemedicine platforms to improve trauma care delivery and patient outcomes.

China Trauma Care Centers Market Insight

The China Trauma Care Centers market is growing rapidly, driven by increasing urbanization, rising road traffic accident rates, and substantial government investments in healthcare infrastructure. The expansion of emergency medical services, trauma networks, and specialized trauma treatment facilities is significantly improving access to critical care across the country. Growing healthcare expenditure, rising awareness regarding trauma management, and increasing adoption of advanced diagnostic and surgical technologies are further supporting market growth. In addition, ongoing healthcare reforms and investments in hospital capacity expansion are positioning China as one of the fastest-growing trauma care markets globally.

Trauma Care Centers Market Share

The Trauma Care Centers industry is primarily led by well-established companies, including:

- HCA Healthcare, Inc. (U.S.)

- CommonSpirit Health (U.S.)

- Mayo Clinic (U.S.)

- Cleveland Clinic (U.S.)

- Ascension Health (U.S.)

- Tenet Healthcare Corporation (U.S.)

- Universal Health Services, Inc. (UHS) (U.S.)

- Community Health Systems, Inc. (U.S.)

- Mass General Brigham (U.S.)

- NYC Health + Hospitals (U.S.)

- Johns Hopkins Medicine (U.S.)

- University of Pittsburgh Medical Center (UPMC) (U.S.)

- Banner Health (U.S.)

- Intermountain Health (U.S.)

- The Royal London Hospital (U.K.)

- King's College Hospital NHS Foundation Trust (U.K.)

- Charité – Universitätsmedizin Berlin (Germany)

- University Hospital Heidelberg (Germany)

- Assistance Publique–Hôpitaux de Paris (AP-HP) (France)

- Karolinska University Hospital (Sweden)

- Apollo Hospitals Enterprise Ltd. (India)

- Fortis Healthcare Limited (India)

- Max Healthcare Institute Limited (India)

- Manipal Hospitals (India)

- Ramsay Health Care Limited (Australia)

- Singapore General Hospital (Singapore)

- Bumrungrad International Hospital (Thailand)

- Aster DM Healthcare (UAE)

- Mediclinic International plc (South Africa)

- Netcare Limited (South Africa)

Latest Developments in Trauma Care Centers Market

- In January 2022, the American College of Surgeons (ACS) introduced its updated Resources for Optimal Care of the Injured Patient: 2022 Standards, representing the most significant revision of trauma center standards in nearly a decade. The updated framework strengthened requirements for trauma center staffing, quality improvement programs, data management, resource availability, and patient care protocols, helping trauma centers worldwide enhance trauma care delivery and accreditation compliance

- In February 2023, OhioHealth announced a USD 400 million expansion project at Grant Medical Center in Columbus, Ohio, which includes the construction of a new trauma center, emergency department, and critical care pavilion. As one of Ohio’s busiest Level I trauma centers, the expansion is aimed at increasing trauma treatment capacity and modernizing emergency care infrastructure to address growing patient demand

- In April 2023, the Government of Ireland officially launched two Major Trauma Centres at Mater Misericordiae University Hospital in Dublin and Cork University Hospital as part of the National Trauma Strategy. The centers were established to provide the highest level of specialist trauma care and improve coordinated trauma services across Ireland’s national trauma networks

- In February 2024, the University of Arkansas for Medical Sciences (UAMS) successfully retained its Level I Trauma Center designation from the American College of Surgeons, reaffirming its role as Arkansas’ highest-level adult trauma care facility. The redesignation highlighted continued investments in multidisciplinary trauma teams, advanced trauma treatment capabilities, and quality improvement initiatives

- In April 2024, Intermountain Health’s St. Vincent Regional Hospital in Montana achieved official Level I Trauma Center verification from the American College of Surgeons. The designation expanded access to advanced trauma care services in the region and strengthened the hospital’s ability to manage the most complex and life-threatening injuries

- In May 2024, Harris Health System broke ground on a new USD 1.6 billion hospital in Houston, Texas, designed to become the first Level I trauma-capable hospital outside the Texas Medical Center. The project includes advanced emergency and trauma care facilities, a rooftop helipad, and expanded critical care capabilities aimed at improving access to trauma services for a rapidly growing population

- In September 2024, Lake Regional Health System renewed its Level III Trauma Center designation through the Missouri Department of Health and Senior Services. The renewal reinforced the hospital’s role in providing 24/7 trauma care and emergency services across a large geographic region with limited access to specialized trauma facilities

- In December 2024, Owensboro Health Twin Lakes Medical Center earned Level IV Trauma Center designation, enhancing its ability to provide emergency stabilization and life-saving trauma care services. The designation marked a significant step in expanding trauma care accessibility and strengthening regional emergency healthcare infrastructure

- In January 2025, Integris Health Baptist Medical Center in Oklahoma City officially opened its newly designated Level II Trauma Center. The upgrade from Level III status expanded the hospital’s trauma treatment capabilities and provided emergency responders with additional options for managing severe injury cases across the region

- In April 2025, Atrium Health Wake Forest Baptist Medical Center opened a new 45,000-square-foot adult emergency department featuring dedicated trauma rooms, advanced imaging services, expanded treatment capacity, and enhanced emergency care infrastructure. The development was designed to improve access to trauma and emergency services while increasing operational efficiency

- In July 2025, the Government of Mizoram inaugurated a new trauma care facility at Civil Hospital in Aizawl, India. The center was established to strengthen emergency medical services and includes triage areas, imaging facilities, treatment rooms, observation units, and minor operation capabilities, significantly improving trauma care accessibility in the region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.