Global Tympanostomy Products Market

Market Size in USD Million

USD

153.77 Million

USD

181.58 Million

2025

2033

USD

153.77 Million

USD

181.58 Million

2025

2033

| 2026 - 2033 | |

| USD 153.77 Million | |

| USD 181.58 Million | |

| % | |

|

Tympanostomy Products Market Size

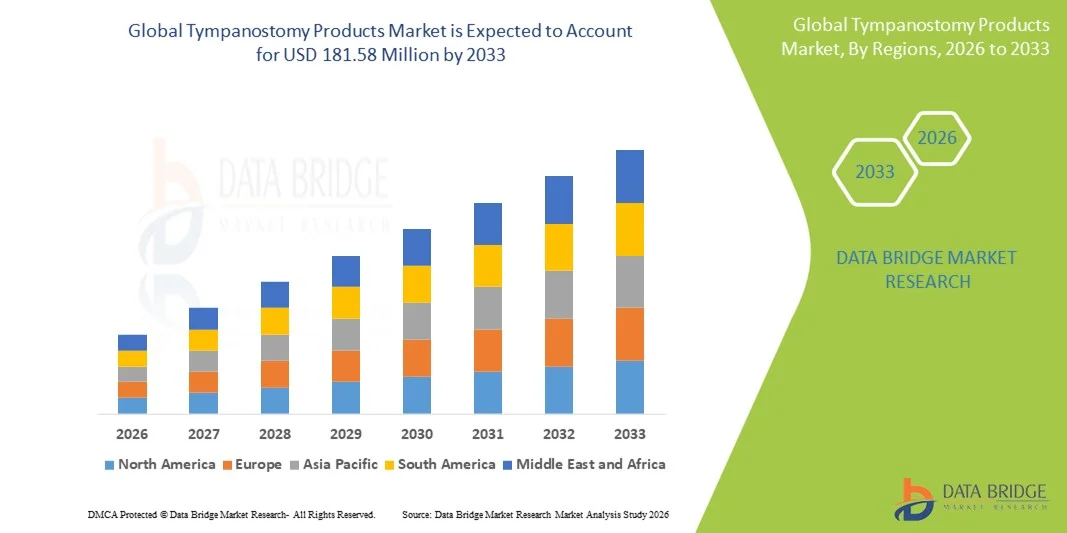

- The global Tympanostomy Products market size was valued at USD 153.77 Million in 2025 and is expected to reach USD 181.58 Million by 2033, at a CAGR of 2.10% during the forecast period

- The market growth is largely fueled by the rising prevalence of otitis media and other middle-ear disorders, along with continuous technological advancements in minimally invasive ENT surgical solutions, leading to increased adoption of tympanostomy products across hospitals and ambulatory surgical centers

- Furthermore, growing demand for safe, effective, and patient-friendly ear ventilation solutions—particularly for pediatric and geriatric populations—is establishing tympanostomy products as a standard of care in middle-ear disease management. These converging factors are accelerating the uptake of Tympanostomy Products solutions, thereby significantly boosting the industry’s overall growth

Tympanostomy Products Market Analysis

- Tympanostomy products, which include ventilation tubes and related insertion instruments used in middle-ear procedures, are essential components of modern otolaryngology care across both pediatric and adult patient populations due to their role in relieving middle-ear effusion, reducing infection recurrence, and improving hearing outcomes

- The escalating demand for tympanostomy products is primarily fueled by the high and rising prevalence of otitis media, particularly among children, along with increasing awareness regarding early diagnosis and surgical intervention to prevent long-term hearing complications

- North America dominated the tympanostomy products market with the largest revenue share of 38.6% in 2025, characterized by a well-established healthcare infrastructure, high procedure volumes for pediatric ENT surgeries, favorable reimbursement policies, and strong adoption of advanced minimally invasive tympanostomy devices, especially in the United States

- Asia-Pacific is expected to be the fastest-growing region in the tympanostomy products market during the forecast period, registering a CAGR of 7.9% from 2026 to 2033, driven by increasing pediatric populations, improving access to ENT care, rising healthcare expenditure, and growing awareness of middle-ear disease management in countries such as China and India

- The Recurrent Otitis Media with Effusion segment dominated with a revenue share of 58.7% in 2025, owing to the high prevalence among pediatric patients and strong clinical guidelines recommending timely tube placement

Report Scope and Tympanostomy Products Market Segmentation

|

Attributes |

Tympanostomy Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Medtronic (Ireland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Tympanostomy Products Market Trends

Rising Adoption of Minimally Invasive ENT Procedures

- A significant and accelerating trend in the global tympanostomy products market is the growing preference for minimally invasive ear procedures to manage chronic otitis media and middle-ear effusion, particularly in pediatric populations. These procedures enable faster recovery, reduced hospital stays, and improved patient comfort compared to conventional surgical approaches

- For instance, the increasing adoption of in-office tympanostomy tube placement systems using local anesthesia has gained traction in the U.S. and Europe, allowing ENT specialists to treat pediatric patients without general anesthesia, thereby improving procedural efficiency and safety

- Technological advancements in tympanostomy tubes, including improved biocompatible materials, antimicrobial coatings, and optimized tube designs, are enhancing clinical outcomes by reducing infection risk, tube blockage, and premature extrusion

- The growing use of disposable and single-use tympanostomy devices is also contributing to this trend, as healthcare providers aim to minimize cross-contamination risks and comply with stringent infection control protocols in outpatient and hospital settings

- This shift toward minimally invasive and patient-centric ENT solutions is reshaping clinical practice patterns, encouraging manufacturers to focus on innovative, easy-to-use, and cost-effective tympanostomy products. Consequently, companies such as Medtronic and Olympus are investing in next-generation tympanostomy systems designed for rapid deployment and improved procedural precision

- The demand for advanced tympanostomy products is increasing across hospitals, ambulatory surgical centers, and ENT clinics as healthcare systems emphasize efficiency, safety, and improved patient outcomes

Tympanostomy Products Market Dynamics

Driver

Growing Prevalence of Otitis Media and Pediatric ENT Disorders

- The rising incidence of otitis media, particularly among infants and young children, is a major driver fueling demand for tympanostomy products globally. Recurrent ear infections and chronic middle-ear effusion remain among the most common pediatric conditions requiring surgical intervention

- For instance, according to clinical studies and healthcare data, tympanostomy tube insertion remains one of the most frequently performed pediatric surgeries worldwide, supporting sustained demand for ventilation tubes and related devices

- Increased awareness among parents and caregivers regarding early diagnosis and timely surgical management is further accelerating adoption, as untreated middle-ear conditions can lead to hearing loss and developmental delays

- In addition, the expansion of ENT services, growing access to specialized healthcare, and improved reimbursement coverage in developed markets are supporting higher procedural volumes

- The growing preference for outpatient and ambulatory surgical procedures is also contributing to market growth, as tympanostomy procedures can be safely performed in non-hospital settings, reducing overall healthcare costs

- These factors collectively continue to drive consistent growth in the Tympanostomy Products market across both developed and emerging regions

Restraint/Challenge

Procedure-Related Risks and Limited Awareness in Developing Regions

- Despite strong demand, the Tympanostomy Products market faces challenges related to potential procedure-associated complications, including postoperative infections, otorrhea, tube obstruction, and early extrusion, which may deter some patients and caregivers

- For instance, concerns regarding repeated tube insertions in pediatric patients have led some clinicians to adopt a more conservative treatment approach, potentially limiting procedural volumes in certain cases

- Limited awareness about tympanostomy procedures and treatment options in low- and middle-income countries further restricts market penetration, particularly in rural and underserved areas

- In addition, disparities in access to ENT specialists and surgical infrastructure in developing regions pose a barrier to widespread adoption of tympanostomy products

- Cost sensitivity in emerging markets and limited reimbursement coverage for elective ENT procedures can also hinder market growth

- Addressing these challenges through physician education programs, patient awareness initiatives, and the development of affordable, high-quality tympanostomy solutions will be critical for sustained market expansion

Tympanostomy Products Market Scope

The market is segmented on the basis of product, material, application, and end-user.

- By Product

On the basis of product, the Tympanostomy Products market is segmented into Tube Applicators / Inserters and Tympanostomy Tubes. The Tympanostomy Tubes segment dominated the market with a revenue share of 57.8% in 2025, driven by their wide clinical adoption for middle ear ventilation, ease of insertion, and effectiveness in treating recurrent otitis media with effusion. The growing awareness among ENT specialists and patients about timely interventions, coupled with continuous product innovations improving durability and patient comfort, has reinforced its leadership. Hospitals and specialty clinics favor Tympanostomy Tubes due to their standardized sizes, proven safety profiles, and high procedural success rates. In addition, reimbursement support and guideline recommendations for otitis media treatment have further strengthened demand. The market for Tympanostomy Tubes is also bolstered by increased pediatric patient volumes and adoption in emerging economies, where preventive treatment for hearing loss is prioritized. The segment benefits from both outpatient and surgical center applications, making it highly versatile across various healthcare setups. Manufacturers are increasingly investing in research to develop tubes with anti-infection coatings and bioresorbable options, which are expected to further cement market dominance. The high volume of ENT procedures in North America and Europe continues to sustain market leadership. Supply chain expansions and partnerships with distributors have also enhanced accessibility. Overall, consistent clinical efficacy and broad physician preference drive the segment’s continued supremacy in the market.

The Tube Applicators / Inserters segment is expected to witness the fastest CAGR of 22.3% from 2026 to 2033, owing to rising demand for minimally invasive and efficient procedural tools. Applicators improve procedural precision, reduce surgery time, and enhance patient safety during tube insertion, attracting hospitals and ambulatory surgical centers. Increasing focus on operator ergonomics, reduced infection risks, and automation in device handling is accelerating adoption. Emerging markets are adopting applicators rapidly as training and surgical standardization improve. Moreover, growing awareness of device-assisted procedures among clinicians, coupled with rising pediatric ENT cases, is creating a strong growth pipeline. Product innovations including single-use applicators and enhanced material durability are also contributing. Expansion of surgical centers in Asia-Pacific and Latin America is further fueling the segment’s rapid growth. Manufacturers are launching applicators compatible with multiple tube types, increasing versatility and preference. Regulatory approvals and endorsements for safety features have enhanced trust among healthcare providers. The integration of user-friendly designs and cost-effective solutions is attracting smaller clinics and specialty centers. Overall, the segment’s growth is driven by efficiency, safety, and technological improvements in tube delivery methods.

- By Material

On the basis of material, the Tympanostomy Products market is segmented into Fluoroplastic, Silicone, Titanium, and Stainless Steel. The Fluoroplastic segment dominated the market with a revenue share of 51.6% in 2025, supported by its biocompatibility, low tissue reactivity, and superior durability in middle ear applications. ENT specialists prefer fluoroplastic tubes due to reduced infection rates and lower extrusion rates, which minimize repeat procedures. The material’s versatility across multiple patient age groups and procedural types enhances clinical preference. Continuous product innovations, including coated and drug-eluting variants, reinforce the segment’s leading position. Fluoroplastic tubes are widely recommended in pediatric and adult populations for recurrent otitis media, providing predictable outcomes. Strong presence in developed markets, coupled with physician familiarity and clinical guideline endorsements, further consolidates demand. The material is cost-effective, easily sterilizable, and integrates well with tube applicators, increasing adoption in both hospital and ambulatory surgical settings. Robust supply chains and manufacturer investments in product quality continue to drive market dominance. Training programs highlighting material benefits also contribute to widespread adoption. In addition, increasing procedural volumes in high-income regions support sustained revenue leadership. Fluoroplastic’s clinical reliability remains the key growth driver in the material segment.

The Titanium segment is expected to witness the fastest CAGR of 23.5% from 2026 to 2033, driven by increasing preference for long-lasting, biocompatible, and MRI-safe devices. Titanium tubes provide enhanced mechanical strength, lower risk of infection, and compatibility with advanced surgical imaging. Growing adoption in specialty clinics and tertiary hospitals, along with increasing awareness of metallic tubes’ longevity, fuels growth. Rising pediatric ENT procedures and demand for durable, non-reactive materials encourage titanium usage. Manufacturers are introducing lightweight, cost-efficient titanium tubes, widening adoption. Expansion of high-end surgical facilities and urban hospitals in emerging markets is a key growth factor. Titanium’s growing application in recurrent and chronic otitis media treatment ensures consistent market uptake. Regulatory approvals for safety and biocompatibility support broader acceptance. Technological advances such as anti-biofilm coatings further enhance attractiveness. Education of clinicians regarding material benefits contributes to adoption momentum. Overall, titanium tubes’ durability and clinical advantages position them as the fastest-growing material segment globally.

- By Application

On the basis of application, the Tympanostomy Products market is segmented into Recurrent Otitis Media with Effusion, Chronic Otitis Media, and Others. The Recurrent Otitis Media with Effusion segment dominated with a revenue share of 58.7% in 2025, owing to the high prevalence among pediatric patients and strong clinical guidelines recommending timely tube placement. Hospitals and specialty clinics favor interventions to prevent hearing loss, language development delays, and repeated infections. Awareness campaigns by pediatric associations and ENT societies contribute to early diagnosis and procedural adoption. Innovations in tube design, coating, and delivery improve procedural efficiency, patient comfort, and long-term outcomes, driving segment leadership. Increased procedural volumes in North America and Europe, where preventive treatment is prioritized, further support dominance. Fluoroplastic and silicone tubes are most commonly used in these cases, reinforcing material and product synergy. Growing insurance coverage and reimbursement support procedural uptake. Multi-organizational studies validate treatment efficacy, fostering clinician confidence. Ambulatory surgical centers are increasingly performing these procedures, enhancing reach. High procedure success rates and low complication profiles continue to attract patients and providers. The segment benefits from ongoing research and development initiatives enhancing procedural effectiveness. Overall, recurrent otitis media remains the primary driver of market volume and revenue.

The Chronic Otitis Media segment is expected to witness the fastest CAGR of 21.9% from 2026 to 2033, driven by rising adult ENT cases and increasing focus on early intervention to prevent long-term hearing impairment. Growing prevalence of chronic infections, otorrhea, and eardrum perforations is fueling demand for tympanostomy tubes. Specialty clinics and ambulatory surgical centers are expanding procedural offerings. Advances in tube design, including drug-eluting and durable options, improve patient outcomes. Rising healthcare infrastructure in Asia-Pacific and Latin America supports adoption. Physician awareness programs and updated treatment guidelines encourage tube usage. Product innovations ensure longer tube retention and reduced complications. The growing need for minimally invasive, office-based procedures accelerates segment adoption. Chronic otitis media patients increasingly prefer outpatient settings, creating additional growth opportunities. Overall, technological enhancements and unmet clinical needs are key growth drivers in this segment.

- By End-User

On the basis of end-user, the Tympanostomy Products market is segmented into Hospitals, Ambulatory Surgical Centers, and Specialty Clinics. The Hospitals segment dominated with a revenue share of 54.3% in 2025, owing to high procedural volumes, availability of advanced surgical infrastructure, and experienced ENT specialists. Hospitals handle complex and pediatric cases, driving consistent demand for Tympanostomy Products. Strong procedural reimbursement policies, structured ENT departments, and multi-specialty integration contribute to segment leadership. Hospitals also benefit from established supply chains and bulk procurement capabilities, ensuring continuous availability. Growing awareness of preventive treatment and timely intervention in recurrent otitis media further supports adoption. Training programs for hospital staff on new tube types and applicators improve operational efficiency. Product launches tailored to hospital requirements reinforce dominance. Developed markets with high hospital penetration maintain a strong lead. In addition, hospitals’ capacity to conduct multiple procedures per day enhances volume. Consistent procedural outcomes and long-term patient monitoring capabilities make hospitals the preferred end-user. Overall, hospital-based adoption drives the market’s largest share.

The Ambulatory Surgical Centers segment is expected to witness the fastest CAGR of 22.8% from 2026 to 2033, due to increasing preference for outpatient procedures, reduced hospital stays, and lower treatment costs. Rising patient awareness of convenient, minimally invasive options is fueling ASC adoption. Expansion of specialized ENT-focused centers, particularly in North America and Asia-Pacific, supports growth. Ambulatory centers provide flexible scheduling, shorter procedure times, and personalized care. Technological advancements, such as portable tube applicators, enhance procedural efficiency. Regulatory approvals and certifications enable wider acceptance. Collaboration with pediatric and adult ENT specialists drives procedural adoption. The increasing number of ASCs in urban and semi-urban areas creates additional opportunities. Cost-effectiveness and patient preference for outpatient care accelerate uptake. Overall, ASCs are rapidly emerging as the fastest-growing end-user segment.

Tympanostomy Products Market Regional Analysis

- North America dominated the tympanostomy products market with the largest revenue share of approximately 38.6% in 2025, supported by a well-established healthcare infrastructure, high volumes of pediatric ENT procedures, and favorable reimbursement policies for middle-ear surgeries

- The region benefits from strong adoption of advanced and minimally invasive tympanostomy devices, including short-term and long-term ventilation tubes, driven by clinical preference for improved patient outcomes and reduced complication rates

- In addition, the presence of leading medical device manufacturers, high healthcare expenditure, and widespread awareness of early intervention for otitis media continue to reinforce North America’s leadership in the global tympanostomy products market

U.S. Tympanostomy Products Market Insight

The U.S. tympanostomy products market accounted for the largest revenue share within North America in 2025, driven by a high prevalence of pediatric ear infections and a strong emphasis on early diagnosis and surgical intervention. The country records a large number of tympanostomy tube insertion procedures annually, particularly among children aged below five years. Advanced clinical practices, access to specialized ENT surgeons, and favorable insurance coverage further support market growth. Continuous innovation in tube materials, designs, and insertion techniques is also contributing to the sustained expansion of the U.S. market.

Europe Tympanostomy Products Market Insight

The Europe tympanostomy products market is expected to expand at a steady CAGR over the forecast period, driven by increasing awareness of middle-ear disorders, rising pediatric populations in certain regions, and well-structured public healthcare systems. Countries across Europe emphasize early medical intervention and evidence-based ENT treatments, supporting consistent demand for tympanostomy procedures. Technological advancements in biocompatible tube materials and increasing adoption of minimally invasive surgical approaches are further enhancing market growth across the region.

U.K. Tympanostomy Products Market Insight

The U.K. tympanostomy products market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by a strong national healthcare system and standardized clinical guidelines for the management of otitis media with effusion. Increasing referrals for pediatric ENT care, coupled with rising awareness among parents regarding hearing loss prevention, are driving procedure volumes. Ongoing improvements in surgical efficiency and postoperative outcomes are further supporting market expansion in the country.

Germany Tympanostomy Products Market Insight

The Germany tympanostomy products market is projected to grow at a considerable CAGR, driven by advanced hospital infrastructure, high healthcare spending, and a strong focus on medical innovation. Germany’s emphasis on quality care and early treatment of ENT disorders supports steady demand for tympanostomy devices. The adoption of advanced ventilation tube designs and improved surgical techniques is contributing to favorable clinical outcomes, reinforcing the country’s position as a key European market.

Asia-Pacific Tympanostomy Products Market Insight

The Asia-Pacific tympanostomy products market is expected to register the fastest CAGR of approximately 7.9% from 2026 to 2033, driven by large and growing pediatric populations, improving access to ENT care, and rising healthcare expenditure. Increasing awareness of middle-ear disease management and expanding hospital infrastructure across emerging economies are accelerating market growth. Government initiatives aimed at strengthening pediatric healthcare services are further supporting the adoption of tympanostomy procedures across the region.

Japan Tympanostomy Products Market Insight

The Japan tympanostomy products market is witnessing steady growth due to the country’s advanced healthcare system, high diagnostic accuracy, and strong focus on early disease management. Japan places significant emphasis on minimally invasive procedures and high-quality medical devices, supporting the adoption of advanced tympanostomy products. An aging population, along with increased attention to hearing preservation and quality of life, is also contributing to market growth in both pediatric and adult patient segments.

China Tympanostomy Products Market Insight

The tympanostomy products market held a significant revenue share within the Asia-Pacific region in 2025, driven by a large pediatric population, rapid healthcare infrastructure development, and rising awareness of ear-related disorders. Increasing healthcare investment, expansion of tertiary hospitals, and growing availability of trained ENT specialists are supporting higher procedure volumes. In addition, the presence of domestic medical device manufacturers offering cost-effective tympanostomy products is improving accessibility and accelerating market growth across urban and semi-urban areas.

Tympanostomy Products Market Share

The Tympanostomy Products industry is primarily led by well-established companies, including:

• Medtronic (Ireland)

• Smith & Nephew (U.K.)

• Bionix (U.S.)

• Spiggle & Theis Medizintechnik GmbH (Germany)

• Grace Medical (U.S.)

• Advanced Medical Technologies (U.S.)

• Entellus Medical (U.S.)

• Cook Medical (U.S.)

• HEINE Optotechnik GmbH & Co. KG (Germany)

• Olympus Corporation (Japan)

• MED-EL (Austria)

• ReSound / GN Store Nord (Denmark)

• Otopront GmbH (Germany)

• Karl Storz SE & Co. KG (Germany)

• Young Medical (U.S.)

• Interacoustics A/S (Denmark)

• Natus Medical Incorporated (U.S.)

• Armstrong Medical (U.S.)

• Ear Technology Corporation (U.S.)

• Medicover (Sweden)

Latest Developments in Global Tympanostomy Products Market

- In January 2021, Preceptis Medical introduced the next‑generation Hummingbird Tympanostomy Tube System, a novel in‑office pediatric ear tube procedure device designed to streamline tympanostomy tube placement with advanced ergonomic features for efficiency and reduced invasiveness

- In August 2023, Medtronic launched an advanced novel tympanostomy tube system designed to enhance the efficacy and safety of ear surgeries by minimizing epithelial migration and reducing the risk of tube obstruction, representing a notable product innovation in tympanostomy devices

- In 2023, a bioabsorbable tympanostomy tube was launched in Germany by a medical technology company, featuring absorbable materials targeted at reducing the need for secondary tube removal procedures in pediatric patients

- In 2023, a major U.S.‑based manufacturer received FDA 510(k) clearance for an advanced automated tympanostomy tube delivery system for pediatric outpatient settings, enabling quicker, anesthesia‑free tube placement outside traditional operating rooms

- In June 2024, AventaMed, a KARL STORZ company, launched the Solo+ ear tube placement device, designed for streamlined pediatric tympanostomy procedures with regulatory certifications under European MDR and FDA 510(k), advancing in‑office procedural options

- In September 2024, Transparency Market Research reported continued market growth and highlighted the launch and adoption of less invasive tympanostomy solutions, including devices like the Hummingbird and similar office‑based tube systems that reduce the need for general anesthesia

- In May 2025, Smith+Nephew announced the market introduction and first commercial procedure using the Tula System, an in‑office tympanostomy tube placement solution that allows ENT surgeons to place ear tubes in awake children without general anesthesia, significantly improving patient comfort and procedure efficiency

- In April 2025, AventaMed’s Solo+ Tympanostomy Tube handpiece and cartridge device received 510(k) clearance from the U.S. FDA, further expanding minimally invasive options for tympanostomy procedures in pediatric care settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.