Global Type 1 Diabetes Market

Market Size in USD Billion

USD

8.43 Billion

USD

16.02 Billion

2025

2033

USD

8.43 Billion

USD

16.02 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.43 Billion | |

| USD 16.02 Billion | |

| % | |

|

Type 1 Diabetes Market Overview

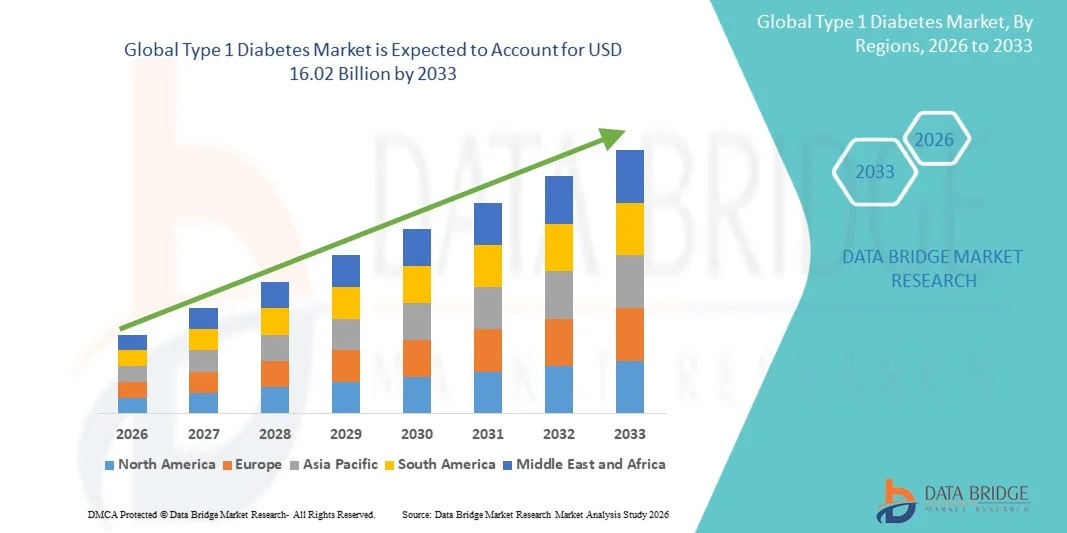

The Type 1 Diabetes Market was valued at USD 8.43 billion in 2025 and is projected to reach USD 16.02 billion by 2033, growing at a CAGR of 7.40% from 2026 to 2033. Market growth is supported by rising incidence of type 1 diabetes among pediatric and adult populations globally, increasing adoption of advanced insulin delivery systems, and growing awareness regarding effective glycemic management strategies.

The expanding pipeline of novel insulin analogs with improved pharmacokinetic profiles, alongside the integration of continuous glucose monitoring (CGM) systems with insulin delivery devices, is transforming diabetes management paradigms. Technological advancements in automated insulin delivery systems, including hybrid closed-loop systems and artificial pancreas technologies, are improving patient outcomes by enabling more precise and personalized insulin dosing. In addition, growing healthcare expenditure, expanding reimbursement coverage for diabetes management devices, and increasing investments in diabetes research across developed and emerging markets are creating significant opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Type 1 Diabetes Market with the largest revenue share of 42.8% in 2025, supported by high prevalence rates, strong reimbursement frameworks, advanced healthcare infrastructure, and the presence of leading insulin and device manufacturers.

- Europe is expected to be the second-largest market, driven by established diabetes care programs, favorable regulatory pathways for novel therapies, and increasing adoption of advanced insulin delivery technologies across the region.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.15% from 2026 to 2033, driven by rising diabetes prevalence, expanding healthcare access, increasing disposable incomes, and growing awareness of advanced diabetes management solutions.

- The Rapid-Acting Insulin segment led the insulin analog category with a 48.2% market share in 2025, reflecting its critical role in mealtime glucose control and widespread integration with insulin pump therapies for optimized glycemic management.

- The Long-Acting Insulin segment is anticipated to be the fastest-growing insulin analog category, driven by development of next-generation basal insulins with extended duration profiles, reduced hypoglycemia risk, and improved patient adherence.

- The Insulin Pump segment dominated the devices category with a 39.5% market share in 2025, supported by increasing adoption of automated insulin delivery systems, technological integration with CGM devices, and improved clinical outcomes associated with pump therapy.

- The Blood Glucose Meter segment is expected to witness strong growth during the forecast period, driven by increasing demand for accurate point-of-care glucose monitoring and integration capabilities with digital health platforms.

- The Hospital segment dominated the end-user category with a 45.3% market share in 2025, supported by comprehensive diabetes management programs, specialist endocrinology services, and access to advanced insulin delivery technologies.

- The Home Care segment is expected to witness the fastest growth during the forecast period, driven by patient preference for self-management, expansion of telehealth services, and increasing availability of user-friendly insulin delivery and monitoring devices.

Market Size & Forecast

- Global Market Value (2025): USD 8.43 Billion

- Expected Market Value (2033): USD 16.02 Billion

- Forecast CAGR (2026–2033): 7.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Type 1 Diabetes Market Segmentation

|

Attributes |

Type 1 Diabetes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Novo Nordisk A/S (Denmark) · Sanofi (France) · Lilly USA, LLC (U.S.) · Medtronic plc (Ireland) · Insulet Corporation (U.S.) · Tandem Diabetes Care Inc. (U.S.) · Abbott Laboratories (U.S.) · Dexcom Inc. (U.S.) · Ypsomed AG (Switzerland) · Beta Bionics Inc. (U.S.) · Bigfoot Biomedical Inc. (U.S.) · Zealand Pharma A/S (Denmark) |

|

Market Opportunities |

· Development of fully automated closed-loop insulin delivery systems with enhanced artificial intelligence algorithms for personalized glycemic control · Expansion of advanced diabetes management technologies into emerging markets with growing healthcare infrastructure and increasing diabetes prevalence |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Type 1 Diabetes Market Trends

Trend: Integration of Artificial Intelligence and Automated Insulin Delivery Systems

Clinical adoption of advanced diabetes management technologies continues to accelerate as artificial intelligence (AI) and machine learning algorithms are integrated into insulin delivery systems. Automated insulin delivery (AID) systems, including hybrid closed-loop and fully closed-loop technologies, leverage real-time continuous glucose monitoring data to autonomously adjust basal insulin delivery, reducing glycemic variability and minimizing hypoglycemia risk. These systems are transforming type 1 diabetes management by enabling personalized, data-driven insulin dosing without requiring constant patient intervention.

For instance,

The integration of CGM systems with insulin pumps in devices such as the Medtronic MiniMed 780G and Tandem Control-IQ has demonstrated significant improvements in time-in-range metrics, with clinical trials showing patients achieving over 70% time in target glucose range compared to approximately 60% with standard pump therapy.

In addition, emerging AI-powered predictive algorithms are enabling anticipatory insulin adjustments based on meal patterns, physical activity, and historical glucose trends, further improving glycemic outcomes and reducing the burden of diabetes self-management. The convergence of digital health technologies with insulin delivery systems is expected to drive continued innovation and market expansion throughout the forecast period.

Type 1 Diabetes Market Dynamics

Key Market Driver: Rising Global Prevalence of Type 1 Diabetes

The increasing incidence of type 1 diabetes worldwide is a primary driver of market growth. Type 1 diabetes affects approximately 8.4 million individuals globally, with projections indicating this number could exceed 17 million by 2040. The condition typically manifests during childhood and adolescence, creating a growing patient population requiring lifelong insulin therapy and diabetes management devices. Rising diagnostic rates, improved disease awareness, and expanded screening programs are contributing to earlier identification and treatment initiation.

For instance,

According to the International Diabetes Federation (IDF), approximately 1.2 million children and adolescents under 20 years of age are living with type 1 diabetes globally, with over 100,000 new cases diagnosed annually in this age group. The expanding patient population requiring continuous insulin therapy is expected to drive sustained demand for insulin analogs and advanced delivery devices throughout the forecast period.

Key Restraint/Challenge: High Treatment Costs and Limited Access in Developing Regions

The substantial costs associated with insulin therapy, insulin delivery devices, and continuous glucose monitoring systems present significant barriers to optimal diabetes management, particularly in low- and middle-income countries. The cumulative annual cost of insulin pumps, consumables, CGM sensors, and insulin analogs can exceed USD 15,000 per patient in developed markets, limiting accessibility for uninsured or underinsured populations. Additionally, inconsistent reimbursement policies and limited healthcare infrastructure in developing regions restrict access to advanced diabetes management technologies.

For instance,

Global disparities in insulin access remain significant, with the World Health Organization estimating that only 50% of people requiring insulin worldwide have reliable access to the medication. High treatment costs continue to present substantial challenges for healthcare systems and patients, particularly in resource-limited settings where out-of-pocket expenses constitute the primary payment mechanism.

Key Market Opportunity: Development of Next-Generation Insulin Formulations and Delivery Technologies

The ongoing development of ultra-rapid-acting insulins, glucose-responsive smart insulins, and once-weekly basal insulin formulations represents significant market opportunities. These innovations aim to improve glycemic control while reducing injection frequency and hypoglycemia risk. Simultaneously, advances in patch pump technology, tubeless insulin delivery systems, and implantable insulin pumps are expanding treatment options and improving patient convenience and adherence.

For instance,

Clinical development of once-weekly basal insulin formulations, including insulin icodec (Novo Nordisk), has demonstrated non-inferior glycemic control compared to daily basal insulins while significantly reducing injection burden. The FDA approval of insulin icodec in 2024 marked a significant milestone in diabetes treatment, offering patients a simplified dosing regimen and potentially improving long-term adherence. Continued innovation in insulin formulations and delivery technologies is expected to create substantial growth opportunities across the forecast period.

Type 1 Diabetes Market Scope

The type 1 diabetes market is segmented on the basis of insulin analog, devices, and end-user.

By Insulin Analog

On the basis of insulin analog, the Type 1 Diabetes Market is segmented into rapid-acting insulin, short-acting insulin, and long-acting insulin. The rapid-acting insulin segment dominated the market with a 48.2% market share in 2025, reflecting its essential role in mealtime glucose control and widespread integration with insulin pump therapy for optimized postprandial glycemic management. Rapid-acting insulin analogs, including insulin lispro, insulin aspart, and insulin glulisine, offer faster onset and shorter duration of action compared to regular human insulin, enabling more precise prandial coverage and improved glycemic control. The segment's dominance is further supported by the development of ultra-rapid-acting formulations with enhanced absorption profiles.

The long-acting insulin segment is expected to witness the fastest growth from 2026 to 2033, driven by development of next-generation basal insulins with extended duration profiles exceeding 24 hours, flatter pharmacokinetic profiles reducing nocturnal hypoglycemia risk, and improved patient adherence through simplified once-daily or once-weekly dosing regimens. The approval of insulin icodec and continued development of glucose-responsive basal insulin technologies are expected to accelerate segment growth.

By Devices

On the basis of devices, the Type 1 Diabetes Market is segmented into insulin pump, insulin pen, blood glucose meter, and others. The insulin pump segment dominated the market with a 39.5% market share in 2025, supported by increasing adoption of automated insulin delivery systems, seamless integration with continuous glucose monitoring devices, and demonstrated clinical benefits including improved time-in-range and reduced hypoglycemia. Technological advancements in hybrid closed-loop systems, tubeless patch pumps, and AI-powered dosing algorithms are driving pump therapy adoption across pediatric and adult patient populations. Major players including Medtronic, Tandem Diabetes Care, and Insulet Corporation continue to expand their product portfolios with increasingly sophisticated pump technologies.

The blood glucose meter segment is expected to witness strong growth during the forecast period, driven by continued demand for accurate point-of-care glucose monitoring, particularly among patients not utilizing continuous glucose monitoring systems. Integration of blood glucose meters with smartphone applications and cloud-based data platforms is enhancing their clinical utility and supporting informed treatment decisions.

By End-User

On the basis of end-user, the Type 1 Diabetes Market is segmented into hospital, research institutes, and home care. The hospital segment dominated the market with a 45.3% market share in 2025, driven by comprehensive diabetes management programs, specialist endocrinology and pediatric diabetes services, and access to advanced insulin delivery technologies and patient education resources. Hospitals serve as primary centers for newly diagnosed type 1 diabetes patients, providing intensive insulin therapy initiation, carbohydrate counting education, and ongoing clinical management. The concentration of multidisciplinary diabetes care teams and access to advanced diagnostic and treatment technologies contributes to segment leadership.

The home care segment is expected to witness the fastest growth from 2026 to 2033, driven by patient preference for self-management, expansion of telehealth and remote monitoring services, and increasing availability of user-friendly insulin delivery and glucose monitoring devices. The shift toward patient-centric care models, supported by digital health platforms enabling real-time data sharing with healthcare providers, is accelerating home care segment expansion. Improved device usability, extended sensor wear times, and simplified insulin delivery systems are reducing barriers to effective home-based diabetes management.

Type 1 Diabetes Market Regional Analysis

North America dominated the type 1 diabetes market with a revenue share of 42.8% in 2025, supported by high prevalence rates, advanced healthcare infrastructure, strong reimbursement frameworks, and the presence of leading insulin and device manufacturers including Eli Lilly, Medtronic, Tandem Diabetes Care, and Insulet Corporation. Favorable regulatory pathways, extensive clinical research activity, and high adoption rates of advanced diabetes management technologies contribute to regional market leadership.

U.S. Type 1 Diabetes Market Insight

The U.S. type 1 diabetes market represents the largest national market globally, benefiting from approximately 1.9 million individuals living with type 1 diabetes, extensive insurance coverage for insulin and diabetes devices, and high adoption rates of insulin pump therapy and continuous glucose monitoring. The Affordable Care Act provisions ensuring coverage of essential health benefits, including diabetes supplies, and favorable Medicare coverage determinations for CGM systems have expanded patient access to advanced technologies. Strong clinical guideline recommendations from the American Diabetes Association supporting intensive insulin therapy and technology utilization drive treatment adoption.

Europe Type 1 Diabetes Market Insight

The Europe type 1 diabetes market remains a major contributor, with established diabetes care programs across Germany, the U.K., France, and Nordic countries. Strong public healthcare systems provide broad coverage for insulin therapy and diabetes management devices, while favorable regulatory pathways through the European Medicines Agency facilitate timely access to novel therapies. Growing adoption of automated insulin delivery systems and expanding CGM utilization are improving patient outcomes across the region.

U.K. Type 1 Diabetes Market Insight

The U.K. type 1 diabetes market is characterized by comprehensive National Health Service (NHS) diabetes care programs and increasing investment in advanced diabetes technologies. NHS England's commitment to expanding access to hybrid closed-loop systems and CGM technology is improving glycemic outcomes for patients with type 1 diabetes. The U.K. holds a 7.8% share of the global market in 2025, supported by strong clinical infrastructure and specialized diabetes centers.

Germany Type 1 Diabetes Market Insight

Germany's robust healthcare infrastructure and favorable statutory health insurance coverage support comprehensive diabetes management programs. High adoption rates of insulin pump therapy and CGM technology, combined with strong clinical expertise and patient education programs, contribute to improved treatment outcomes. Germany represents the largest market within Europe, with established reimbursement pathways for advanced diabetes technologies.

Asia-Pacific Type 1 Diabetes Market Insight

The Asia-Pacific type 1 diabetes market is poised for rapid growth with a CAGR of 9.15% during the forecast period, driven by rising diabetes prevalence, expanding healthcare access, increasing disposable incomes, and growing awareness of advanced diabetes management solutions. Japan, China, Australia, and South Korea represent key markets, with increasing investment in diabetes care infrastructure and expanding adoption of insulin delivery technologies.

Japan Type 1 Diabetes Market Insight

The Japan type 1 diabetes market benefits from advanced healthcare infrastructure, universal health insurance coverage, and strong adoption of diabetes management technologies. Japanese regulatory approvals for automated insulin delivery systems and CGM devices are expanding treatment options, while established endocrinology networks provide specialized care. Japan holds a 6.2% share of the global market in 2025.

China Type 1 Diabetes Market Insight

The China type 1 diabetes market is experiencing rapid growth driven by healthcare modernization initiatives, expanding private healthcare networks, and increasing patient demand for advanced treatment options. Growing awareness of type 1 diabetes, improving diagnostic capabilities, and expanding access to insulin analogs and delivery devices are supporting market expansion. China is expected to be among the fastest-growing national markets, with a projected CAGR of 10.2% from 2026 to 2033.

Type 1 Diabetes Market Share

The type 1 diabetes industry is primarily led by well-established companies, including:

- Novo Nordisk A/S (Denmark)

- Sanofi (France)

- Lilly USA, LLC (U.S.)

- Medtronic plc (Ireland)

- Insulet Corporation (U.S.)

- Tandem Diabetes Care Inc. (U.S.)

- Abbott Laboratories (U.S.)

- Dexcom Inc. (U.S.)

- Ypsomed AG (Switzerland)

- Beta Bionics Inc. (U.S.)

- Bigfoot Biomedical Inc. (U.S.)

- Zealand Pharma A/S (Denmark)

Latest Developments in Type 1 Diabetes Market

- In March 2026, Tandem Diabetes Care announced the FDA clearance of its Mobi insulin pump with Control-IQ technology for pediatric patients as young as two years old. The expanded indication represents a significant milestone in automated insulin delivery for the youngest type 1 diabetes patients, offering families access to advanced pump technology with simplified management capabilities.

- In January 2026, Novo Nordisk announced positive Phase 3 clinical trial results for its once-weekly basal insulin icodec in pediatric patients with type 1 diabetes. The ONWARDS TEEN trial demonstrated non-inferior glycemic control compared to once-daily insulin degludec, supporting potential expanded indications for the weekly insulin formulation.

- In November 2025, Insulet Corporation received FDA clearance for its Omnipod 5 Automated Insulin Delivery System integration with the Abbott FreeStyle Libre 2 Plus continuous glucose monitoring system. The expanded CGM compatibility provides patients with additional choice and flexibility in their diabetes management technology ecosystem.

- In September 2025, Medtronic announced the commercial launch of its MiniMed 780G Advanced Hybrid Closed-Loop System in additional European markets, expanding access to its latest automated insulin delivery technology featuring meal detection algorithms and simplified user interface.

- In June 2025, Beta Bionics received FDA approval for its iLet Bionic Pancreas System for patients with type 1 diabetes. The fully automated insulin delivery system requires only the user's weight for initialization and autonomously determines all insulin dosing, representing a significant advancement in diabetes management simplification.

- In April 2025, Eli Lilly and Company announced FDA approval of Lyumjev (insulin lispro-aabc) in a concentrated U-200 formulation for use in insulin pumps. The concentrated formulation enables extended pump reservoir duration and reduced refill frequency for patients with higher insulin requirements.

- In February 2025, Dexcom Inc. announced the FDA clearance of its G7 continuous glucose monitoring system for integration with multiple automated insulin delivery systems. The expanded compatibility and 60-minute warm-up time enhance the G7's clinical utility and patient convenience.

- In December 2024, Sanofi received FDA approval for Tzield (teplizumab-mzwv) for the delay of Stage 3 type 1 diabetes in adults and pediatric patients 8 years and older with Stage 2 type 1 diabetes. The approval marked the first disease-modifying therapy for type 1 diabetes, representing a significant advancement in early intervention strategies.

- In October 2024, Abbott Laboratories announced the FDA clearance of its FreeStyle Libre 3 continuous glucose monitoring system for integration with automated insulin delivery systems. The world's smallest and thinnest CGM sensor offers enhanced accuracy and user convenience.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.