Global Type 2 Diabetes Market

Market Size in USD Billion

USD

48.64 Billion

USD

78.71 Billion

2025

2033

USD

48.64 Billion

USD

78.71 Billion

2025

2033

| 2026 - 2033 | |

| USD 48.64 Billion | |

| USD 78.71 Billion | |

| % | |

|

Type 2 Diabetes Market Overview

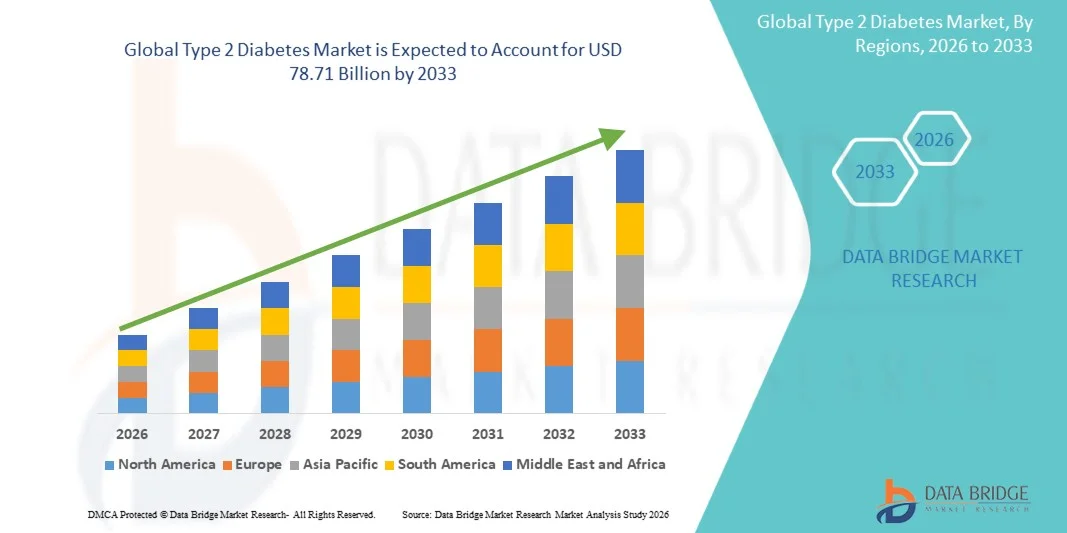

The Type 2 Diabetes Market was valued at USD 48.64 billion in 2025 and is projected to reach USD 78.71 billion by 2033, growing at a CAGR of 6.20% from 2026 to 2033. Market growth is supported by rising prevalence of type 2 diabetes driven by sedentary lifestyles, urbanization, and increasing obesity rates among the global population, alongside the widespread adoption of advanced therapeutic interventions.

The excellent efficacy connected to novel drug classes, combined with improved glycemic control and reduced cardiovascular risk compared to traditional therapies, are driving increased adoption among both patients and healthcare providers. Ongoing technological advancements in drug formulations, including once-weekly injectables, oral GLP-1 receptor agonists, and combination therapies, are expanding the clinical applicability of type 2 diabetes treatments across diverse patient populations. In addition, growing healthcare infrastructure investments in emerging markets and the expansion of diabetes care programs are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Type 2 Diabetes Market with the largest revenue share of 38.7% in 2025, supported by high adoption rates of advanced therapeutic technologies, strong reimbursement frameworks, and the presence of leading market players.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.45% from 2026 to 2033, driven by expanding healthcare infrastructure, rising diabetes prevalence, and increasing healthcare expenditure.

- The Glucagon-Like Peptide-1 (GLP-1) Receptor Agonists segment led the market with a 34.2% market share in 2025, reflecting its established position as a preferred therapeutic class with strong clinical evidence supporting improved glycemic control and cardiovascular outcomes.

- The Sodium-Glucose Cotransporter 2 Inhibitors (SGLT2) segment is anticipated to be the fastest-growing drug type category, driven by increasing evidence of cardiorenal benefits, expanding indications, and growing physician preference for combination therapy regimens.

- The Oral segment dominated the route of administration category with a 62.8% market share in 2025, supported by patient preference for non-injectable therapies, ease of administration, and broad availability of oral antidiabetic agents.

- The Subcutaneous segment is expected to witness strong growth during the forecast period, driven by rising adoption of GLP-1 receptor agonists, insulin therapies, and combination injectable products.

- The Retail Pharmacies segment dominated the distribution channel category with a 54.3% market share in 2025, supported by widespread accessibility, patient convenience, and established prescription fulfillment networks.

- The Hospital Pharmacies segment is expected to witness strong growth during the forecast period, driven by increasing hospitalization of diabetes patients with complications and expanding inpatient diabetes management programs.

Market Size & Forecast

- Global Market Value (2025): USD 48.64 Billion

- Expected Market Value (2033): USD 78.71 Billion

- Forecast CAGR (2026–2033): 6.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Type 2 Diabetes Market Segmentation

|

Attributes |

Type 2 Diabetes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Novo Nordisk A/S (Denmark) · Eli Lilly and Company (U.S.) · Sanofi S.A. (France) · Merck & Co., Inc. (U.S.) · AstraZeneca PLC (U.K.) · Boehringer Ingelheim International GmbH (Germany) · Johnson & Johnson and its affiliates (U.S.) · Takeda Pharmaceutical Company Limited (Japan) · Bristol-Myers Squibb Company (U.S.) · Pfizer Inc. (U.S.) · Amgen Inc. (U.S.) · Novartis AG (Switzerland) |

|

Market Opportunities |

· Expansion of GLP-1 receptor agonists and SGLT2 inhibitors into emerging markets with growing diabetes prevalence and healthcare infrastructure · Development of oral GLP-1 formulations and fixed-dose combination therapies enabling improved patient adherence and treatment outcomes |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Type 2 Diabetes Market Trends

Trend: Shift Toward Novel Drug Classes with Cardiorenal Benefits

Clinical adoption of type 2 diabetes therapies continues to evolve as newer drug classes demonstrate benefits beyond glycemic control. GLP-1 receptor agonists and SGLT2 inhibitors have emerged as preferred therapeutic options due to their proven cardiovascular and renal protective effects, driving a paradigm shift in diabetes management guidelines. Advanced formulations, including once-weekly injectables and oral GLP-1 receptor agonists, enable improved patient adherence and reduce treatment burden, supporting broader adoption across patient populations.

For instance,

The oral semaglutide formulation (Rybelsus) has gained significant market traction due to its convenient once-daily dosing, eliminating the need for injections while delivering efficacy comparable to injectable GLP-1 receptor agonists, providing patients with an accessible entry point into advanced diabetes therapy.

In addition, research demonstrates that SGLT2 inhibitors reduce hospitalization for heart failure and slow progression of chronic kidney disease in patients with type 2 diabetes, supporting expanding indications and guideline-directed therapy adoption.

The shift toward novel drug classes with cardiorenal benefits is expected to strengthen the adoption of advanced type 2 diabetes therapies globally.

Type 2 Diabetes Market Dynamics

Key Market Driver: Rising Prevalence of Type 2 Diabetes Globally

The growing prevalence of type 2 diabetes among the global population is a primary driver of market growth. Sedentary lifestyles, urbanization, dietary changes, and rising obesity rates are contributing to the steady increase in diabetes diagnoses worldwide. The demand for effective therapies has increased significantly as type 2 diabetes is becoming more prevalent, particularly among middle-aged and older populations.

For instance,

According to the International Diabetes Federation (IDF) Diabetes Atlas 2025, approximately 590 million adults (20-79 years) are living with diabetes globally, with over 90% having type 2 diabetes. By 2050, projections indicate that 853 million adults will be living with diabetes, representing a 46% increase.

Healthcare systems are under significant strain as a result of the increase in diabetes diagnoses, which has raised demand for medications that help control blood sugar levels. The persistent increase in prevalence suggests that the market for type 2 diabetes therapeutics will continue to grow.

The rising prevalence of type 2 diabetes globally is expected to drive sustained market expansion across the forecast period.

Key Restraint/Challenge: High Cost of Novel Therapies and Affordability Concerns

The substantial cost of novel therapeutic classes, including GLP-1 receptor agonists and SGLT2 inhibitors, presents a significant barrier to adoption, particularly in low- and middle-income countries and for patients without adequate insurance coverage. The pricing differential between innovative therapies and generic alternatives, such as metformin and sulfonylureas, limits access for cost-sensitive healthcare systems and patients.

For instance,

Healthcare systems evaluating diabetes therapy adoption must balance the clinical benefits of novel drug classes against significant cost implications, with branded GLP-1 receptor agonists requiring substantially higher expenditure compared to established generic alternatives.

High costs of novel therapies may constrain adoption, particularly among budget-sensitive healthcare providers and patients in emerging markets.

Key Market Opportunity: Expansion of Combination Therapies and Personalized Medicine

The development of fixed-dose combination therapies and personalized medicine approaches is creating opportunities for improved treatment outcomes and market expansion. Combination products incorporating multiple mechanisms of action, such as GLP-1/GIP dual agonists and fixed-dose oral combinations, offer enhanced glycemic control and simplified treatment regimens. Simultaneously, advances in precision medicine and biomarker-based patient stratification are enabling targeted therapeutic interventions optimized for individual patient characteristics.

Expansion of combination therapies and personalized medicine approaches is expected to create significant opportunities for market growth and improved patient outcomes.

Type 2 Diabetes Market Scope

The type 2 diabetes market is segmented on the basis of drug type, route of administration, and distribution channel.

By Drug Type

On the basis of drug type, the Type 2 Diabetes Market is segmented into dipeptidyl peptidase-4 (DPP-4) inhibitors, alpha-glucosidase inhibitors, biguanides, glucagon-like peptide-1 (GLP-1) receptor agonists, sodium-glucose cotransporter 2 inhibitors (SGLT2), sulfonylureas, and other. The Glucagon-Like Peptide-1 (GLP-1) Receptor Agonists segment dominated the market with a 34.2% market share in 2025, reflecting its established position as a preferred therapeutic class with strong clinical evidence supporting improved glycemic control, weight reduction, and cardiovascular outcomes. High prescription volumes for semaglutide, liraglutide, and dulaglutide products across North America and Europe contribute to segment leadership.

The Sodium-Glucose Cotransporter 2 Inhibitors (SGLT2) segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing evidence of cardiovascular and renal protective benefits, expanding indications beyond glycemic control, and growing physician preference for SGLT2 inhibitors in combination therapy regimens. Favorable guideline recommendations for patients with heart failure and chronic kidney disease are supporting broader clinical adoption.

By Route of Administration

On the basis of route of administration, the Type 2 Diabetes Market is segmented into oral, subcutaneous, and intravenous. The Oral segment dominated the market with a market share of 62.8% in 2025, driven by patient preference for non-injectable therapies, ease of administration, and broad availability of oral antidiabetic agents including metformin, DPP-4 inhibitors, SGLT2 inhibitors, and sulfonylureas. The introduction of oral semaglutide has further strengthened the oral segment by providing GLP-1 receptor agonist efficacy without injection requirements.

The Subcutaneous segment is expected to witness the fastest growth from 2026 to 2033, driven by rising adoption of once-weekly GLP-1 receptor agonists, combination injectable products, and basal insulin therapies. Improved injection devices, including autoinjectors and pen systems, are reducing patient barriers to injectable therapy initiation and supporting segment expansion.

By Distribution Channel

On the basis of distribution channel, the Type 2 Diabetes Market is segmented into retail pharmacies, hospital pharmacies, and others. The Retail Pharmacies segment dominated the market with a market share of 54.3% in 2025, driven by widespread accessibility, patient convenience, and established prescription fulfillment networks. Chronic disease management models emphasizing outpatient care and medication adherence programs support high prescription volumes through retail pharmacy channels.

The Hospital Pharmacies segment is expected to witness strong growth from 2026 to 2033, driven by increasing hospitalization of diabetes patients with cardiovascular and renal complications, expanding inpatient diabetes management programs, and specialty medication initiation protocols requiring clinical oversight. Rising healthcare infrastructure investments in emerging markets are supporting hospital pharmacy channel expansion.

Type 2 Diabetes Market Regional Analysis

North America dominated the type 2 diabetes market with a revenue share of 38.7% in 2025, supported by high adoption rates of advanced therapeutic technologies, strong reimbursement frameworks, and the presence of leading market players. Favorable regulatory pathways, robust clinical guideline adherence, and extensive physician experience with novel drug classes contribute to regional market leadership.

U.S. Type 2 Diabetes Market Insight

The U.S. type 2 diabetes market benefits from the highest adoption rates of GLP-1 receptor agonists and SGLT2 inhibitors globally, extensive direct-to-consumer advertising, and strong commercial payer coverage for branded diabetes therapies. Academic medical centers, integrated health systems, and specialty endocrinology practices continue to expand advanced diabetes treatment programs. Favorable Medicare Part D and commercial payer reimbursement supports prescription volumes and therapeutic innovation adoption.

Europe Type 2 Diabetes Market Insight

The Europe type 2 diabetes market remains a major contributor, with strong guideline-directed therapy adoption across Germany, the U.K., France, and Italy. Growing prescription of GLP-1 receptor agonists and SGLT2 inhibitors is supported by favorable reimbursement decisions from health technology assessment bodies. Cross-national guidelines and structured diabetes care pathways are improving treatment outcomes and standardizing care delivery.

U.K. Type 2 Diabetes Market Insight

The U.K. type 2 diabetes market is characterized by expanding adoption of NICE-recommended therapies within NHS diabetes care programs. Investment in structured diabetes management pathways and digital health interventions is improving access to advanced therapies and supporting medication adherence.

Germany Type 2 Diabetes Market Insight

Germany's robust healthcare infrastructure and favorable reimbursement frameworks support comprehensive diabetes treatment programs. Strong clinical evidence requirements and health technology assessments drive adoption of therapies demonstrating cardiovascular and renal benefits beyond glycemic control.

Asia-Pacific Type 2 Diabetes Market Insight

The Asia-Pacific type 2 diabetes market is poised for rapid growth with a CAGR of 8.45% during the forecast period, driven by expanding healthcare infrastructure, rising diabetes prevalence, and increasing healthcare expenditure. China dominated the Asia-Pacific market with a 42.3% regional share in 2025, supported by large patient populations and expanding diabetes care programs. Private and public healthcare systems in China, Japan, India, and South Korea are investing in advanced diabetes therapies to address growing patient demand and improve clinical outcomes.

Japan Type 2 Diabetes Market Insight

The Japan type 2 diabetes market benefits from advanced healthcare infrastructure, strong physician expertise, and favorable reimbursement for novel therapies. DPP-4 inhibitors and SGLT2 inhibitors maintain strong market positions, with expanding adoption of GLP-1 receptor agonists across endocrinology and primary care settings.

China Type 2 Diabetes Market Insight

The China type 2 diabetes market is experiencing rapid growth driven by healthcare modernization initiatives, expanding diabetes care infrastructure, and increasing patient demand for advanced therapeutic options. Volume-based procurement policies are reshaping competitive dynamics while improving access to generic and innovative therapies.

Type 2 Diabetes Market Share

The type 2 diabetes industry is primarily led by well-established companies, including:

- Novo Nordisk A/S (Denmark)

- Eli Lilly and Company (U.S.)

- Sanofi S.A. (France)

- Merck & Co., Inc. (U.S.)

- AstraZeneca PLC (U.K.)

- Boehringer Ingelheim International GmbH (Germany)

- Johnson & Johnson and its affiliates (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Bristol-Myers Squibb Company (U.S.)

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- Novartis AG (Switzerland)

Latest Developments in Type 2 Diabetes Market

- In March 2026, Eli Lilly and Company announced the U.S. FDA approval of tirzepatide (Mounjaro) for an expanded indication in patients with type 2 diabetes and chronic kidney disease, supporting broader clinical adoption and reinforcing the company's leadership in the GLP-1/GIP dual agonist therapeutic class.

- In January 2026, Novo Nordisk A/S reported positive Phase 3 results for oral semaglutide 25 mg and 50 mg doses, demonstrating superior glycemic control and weight reduction compared to lower doses, supporting potential label expansion and market growth for the Rybelsus product franchise.

- In December 2025, Medtronic received U.S. FDA clearance for its Hugo Robotic-Assisted Surgery (RAS) System for urologic surgical procedures, with implications for diabetes-related surgical interventions in patients with complex comorbidities.

- In October 2025, AstraZeneca PLC announced the publication of DAPA-CKD long-term follow-up data demonstrating sustained renal and cardiovascular benefits of dapagliflozin (Farxiga) in patients with type 2 diabetes and chronic kidney disease, supporting expanded therapeutic positioning.

- In August 2025, Boehringer Ingelheim International GmbH and Eli Lilly and Company announced the completion of the EMPA-KIDNEY extended follow-up study, confirming long-term renal protective effects of empagliflozin in diabetic kidney disease patients, strengthening the evidence base for SGLT2 inhibitor adoption.

- In June 2025, Novo Nordisk A/S announced the submission of a supplemental New Drug Application to the U.S. FDA for semaglutide injection for cardiovascular risk reduction in patients with type 2 diabetes without established cardiovascular disease, expanding potential market indications.

- In April 2025, Eli Lilly and Company reported that its retatrutide Phase 3 clinical program demonstrated significant glycemic control and weight reduction in patients with type 2 diabetes, positioning the GLP-1/GIP/glucagon triple agonist as a potential next-generation therapeutic option.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.