Global Uro Gynecology Market

Market Size in USD Billion

USD

27.28 Billion

USD

48.61 Billion

2024

2032

USD

27.28 Billion

USD

48.61 Billion

2024

2032

| 2025 - 2032 | |

| USD 27.28 Billion | |

| USD 48.61 Billion | |

| % | |

|

Uro-Gynecology Market Size

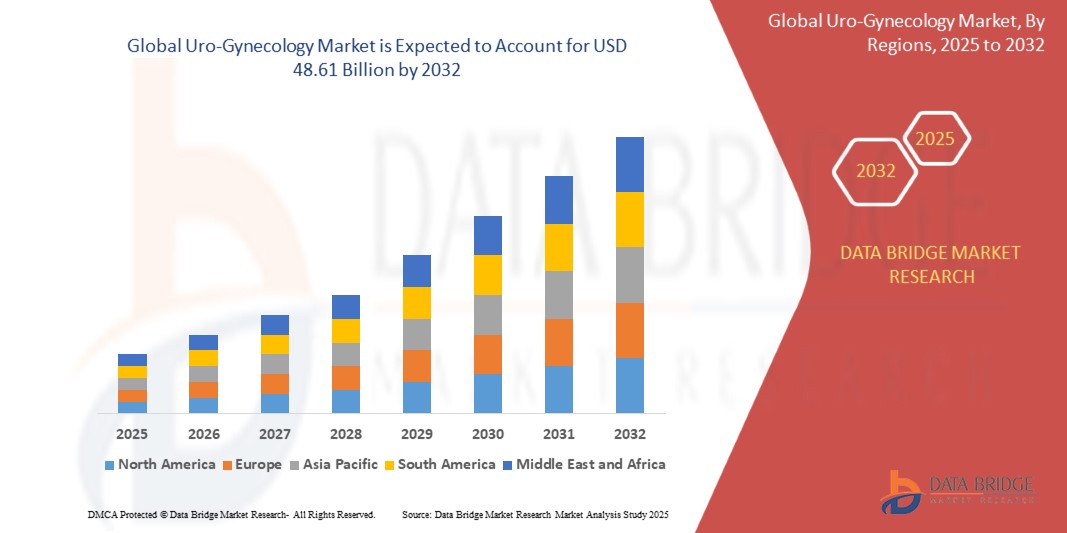

- The global uro-gynecology market size was valued at USD 27.28 billion in 2024 and is expected to reach USD 48.61 billion by 2032, at a CAGR of 7.5% during the forecast period

- The market growth is largely fueled by rising prevalence of pelvic floor disorders, increasing aging female population, and advancements in minimally invasive uro-gynecological surgical procedures

- Furthermore, growing awareness, improved diagnostic technologies, and enhanced reimbursement policies are driving adoption of uro-gynecology solutions across both developed and emerging healthcare markets

Uro-Gynecology Market Analysis

- Increasing incidence of urinary incontinence, pelvic organ prolapse, and other uro-gynecological conditions among aging women is significantly driving demand for specialized diagnostic tools, surgical devices, and therapeutic interventions

- Minimally invasive technologies such as robotic-assisted surgeries, laser therapies, and improved sling systems are transforming patient outcomes, reducing recovery time, and expanding market penetration across both hospital and outpatient settings

- North America is expected to dominate the uro-gynecology market, holding the largest revenue share of 35.96% in 2025, attributed to advanced healthcare infrastructure, high awareness of pelvic health, strong presence of leading medical device companies, favorable reimbursement policies, and early adoption of innovative surgical technologies such as robotic-assisted and minimally invasive procedures across hospitals and specialty clinics

- North America is projected to be the fastest-growing region in the uro-gynecology market during the forecast period, driven by rising geriatric female population, increasing prevalence of pelvic floor disorders, growing demand for outpatient minimally invasive treatments, continuous technological advancements, and supportive government initiatives aimed at improving women’s health and access to uro-gynecological care

- The urinary incontinence devices segment is expected to dominate the uro-gynecology market with a 68.02% share in 2025, owing to the high prevalence of incontinence among aging women, increasing awareness, improved device efficacy, and growing preference for minimally invasive and non-surgical treatment options

Report Scope and Uro-Gynecology Market Segmentation

|

Attributes |

Uro-Gynecology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America: U.S. Canada Mexico Europe:

Asia-Pacific:

South America:

Middle East and Africa:

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Uro-Gynecology Market Trends

Trends

Rising Prevalence of Pelvic Floor Disorders

- Pelvic floor disorders are becoming increasingly prevalent across both developed and developing nations, driven by shifting demographic and lifestyle factors. As populations age, especially in urbanized regions, the incidence of conditions such as urinary incontinence and pelvic organ prolapse has risen significantly

- Rising obesity rates, sedentary lifestyles, and complications related to childbirth further accelerate this trend. Improved awareness, diagnosis, and patient willingness to seek treatment have also contributed to a visible spike in reported cases

- Healthcare systems are gradually transitioning to accommodate this demand. As hospitals and clinics expand women’s health services, the field is witnessing a strong surge in demand for both surgical and non-surgical treatment options

- Manufacturers are responding with technological innovation in diagnostic tools, implants, and minimally invasive devices. In essence, the rising prevalence of pelvic floor disorders serves as a foundational driver—accelerating product development, encouraging clinical investment, and anchoring the long-term growth trajectory of pelvic care and urogynecological treatment solutions

Uro-Gynecology Market Dynamics

Driver

Growing Awareness About Female Reproductive Health Issues

- Awareness surrounding pelvic health and urogynaecology conditions is steadily gaining traction globally. Public health campaigns, media coverage, and advocacy by women's health organizations have helped reduce long-standing stigma associated with disorders such as urinary incontinence and pelvic organ prolapse

- As healthcare literacy improves and conversations about reproductive and postnatal health become more open, more women are actively seeking early diagnosis and treatment options. Much such as the changing face of urban infrastructure, this cultural shift is shaping how society approaches pelvic health as a legitimate, manageable, and treatable condition

- This growing acceptance is also reflected in the increasing demand for preventive care, lifestyle therapies, and surgical consultations. In both developed and emerging markets, the taboo once surrounding these disorders is giving way to informed discussions and timely medical interventions

- Social media, digital health platforms, and maternal health programs have amplified education and normalized treatment-seeking behavior. As a result, healthcare systems and medical device manufacturers are responding by expanding urogynaecology services and tailoring solutions for a more engaged and health-aware patient population

Restraint/Challenge

Stringent Regulatory Framework

- The industry is restrained by stringent regulatory frameworks governing the approval and commercialization of medical devices and surgical products. Regulatory agencies, such as the FDA (U.S.) and the EMA (Europe), require extensive clinical data, safety testing, and quality assurance before granting market authorization. These rigorous requirements ensure patient safety but often result in lengthy approval processes that increase costs and delay the introduction of innovative devices

- This stringent regulatory environment poses a particular barrier for new entrants and smaller manufacturers, who may lack the resources to navigate the complex compliance demands. In addition, evolving regulations and increased scrutiny on device safety, especially following past controversies involving pelvic mesh products, have led to tighter controls. Such regulatory hurdles restrain the pace of innovation and limit the availability of novel treatments, thus impeding overall growth

- Stringent regulatory frameworks across major global markets, including the U.S., the EU, the UK, Canada, Australia, and China, play a critical role in ensuring the safety and efficacy of urogynecology devices. However, these rigorous requirements often lead to prolonged approval timelines, increased compliance costs, and market withdrawals, collectively hindering timely innovation and restricting patient access to advanced treatments. The need for extensive clinical trials, complex post-market surveillance, and evolving regulatory standards creates significant barriers for manufacturers, especially smaller companies. While necessary for patient safety, these regulatory constraints remain a key challenge in expanding and accelerating the availability of urogynecological solutions worldwide

Uro-Gynecology Market Scope

The market is segmented on the basis of product, biomaterial type, material form, indication, end user, and distribution channel.

- By Product

On the basis of product, the uro-gynecology market is segmented into urinary incontinence devices, pelvic organ prolapse devices and others. In 2025, the urinary incontinence devices segment will dominate the market with a 68.02% share, driven by increasing cases of incontinence among aging women, rising awareness, improved diagnostic rates, preference for minimally invasive solutions, and technological advancements enhancing product efficacy and patient comfort.

The urinary incontinence devices segment is anticipated to witness the fastest growth rate of 7.6% from 2025 to 2032, fueled by rising geriatric population, growing demand for non-invasive treatment options, increasing healthcare expenditure, greater awareness of women’s health issues, and continuous innovation in device technology.

- By Biomaterial Type

On the basis of biomaterial type, the uro-gynecology market is segmented into synthetic biomaterials, natural biomaterials, and others. The synthetic biomaterials segment held the largest market revenue share in 2025, driven by high durability, better biocompatibility, cost-effectiveness, ease of manufacturing, and widespread use in uro-gynecological implants and meshes.

The biomaterial type segment is expected to witness the fastest CAGR from 2025 to 2032, driven by rising demand for biocompatible materials, continuous innovation in tissue engineering, increased adoption in uro-gynecological procedures, and growing preference for safer, customizable, and long-lasting implantable solutions across healthcare settings.

- By Material Form

On the basis of material form, the uro-gynecology market is segmented into knitted meshes, scaffolds, injectable gels, and others. The knitted meshes segment held the largest market revenue share in 2025, driven by their high tensile strength, flexibility, ease of implantation, and widespread use in pelvic floor repair procedures.

The knitted meshes segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing adoption in minimally invasive surgeries, advancements in mesh design and materials, growing preference for long-lasting pelvic support solutions, and rising demand for effective treatment of pelvic organ prolapse and incontinence.

- By Indication

On the basis of indication, the uro-gynecology market is segmented into urinary incontinence and pelvic organ prolapse. The urinary incontinence segment held the largest market revenue share in 2025, driven by its higher global prevalence, increasing awareness among women, expanding elderly population, and rising adoption of advanced treatment and diagnostic solutions.

The urinary incontinence segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing geriatric population, rising incidence of stress and urge incontinence, improved access to care, increasing acceptance of non-invasive treatments, and continuous advancements in diagnostic tools and therapeutic devices.

- By End-User

On the basis of end-user, the uro-gynecology market is segmented into hospitals, ambulatory surgical centers (ASCs), specialty clinics, academic & research institutes, home care settings, and others. The hospitals segment held the largest market revenue share in 2025, driven by availability of advanced infrastructure, skilled professionals, high patient footfall, and comprehensive treatment capabilities.

The hospitals segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing adoption of advanced uro-gynecological procedures, rising patient preference for multidisciplinary care, expanding healthcare investments, and the availability of specialized surgical units and post-operative care within hospital settings.

- By Distribution Channel

On the basis of distribution channel, the uro-gynecology market is segmented into direct tenders, online, retail stores, and others. The direct tenders segment is expected to hold the largest market revenue share in 2025, driven by widespread procurement of urogynecology devices by public and private hospitals through centralized purchasing systems. Large-volume purchases via tenders ensure cost efficiency and standardized product access across institutional healthcare settings. The segment’s dominance is further reinforced by government-backed healthcare schemes, growing hospital chains in emerging markets, and long-term vendor contracts that streamline device supply for pelvic floor disorder treatments.

The online segment is expected to witness the fastest CAGR from 2025 to 2032, propelled by the growing shift toward digital health platforms and e-commerce for medical supplies. Increased patient awareness, convenience in purchasing, and availability of a wide range of pelvic care products—such as pessaries and pelvic floor exercisers—are accelerating online sales. The segment is further supported by the expansion of telemedicine, digital pharmacies, and direct-to-consumer marketing strategies adopted by urogynecology device manufacturers targeting tech-savvy and remote populations.

Uro-Gynecology Market Regional Analysis

- North America is the largest market for uro-gynecology, holding a substantial revenue share in 2025 and is projected to grow at a robust CAGR of 7.8% from 2025 to 2032. The region's growth is driven by high awareness of pelvic health issues, favorable reimbursement policies, strong presence of key market players, and early adoption of innovative uro-gynecological devices and procedures

- North America benefits from advanced healthcare infrastructure, high awareness of pelvic health issues, favorable reimbursement policies, strong presence of key market players, and early adoption of innovative uro-gynecological devices and procedures

- Countries such as U.S, Canada and Mexico lead the region with large-scale adoption of lightweight materials across key industries and robust manufacturing infrastructures

U.S Uro-Gynecological Market Insight

The U.S. uro-gynecology market accounted for the largest market revenue share in the North American market in 2025, attributed to advanced healthcare infrastructure, rising prevalence of pelvic floor disorders, growing awareness, favorable reimbursement policies, and increased adoption of innovative surgical and non-surgical treatment solutions.

Europe Uro-Gynecology Market Insight

The Europe uro-gynecology market accounted for the largest market revenue share in the global market in 2025, owing to a well-established healthcare system, rising prevalence of pelvic floor disorders, growing geriatric female population, strong government support for women's health initiatives, and widespread adoption of advanced uro-gynecological treatment technologies.

Germany Uro-Gynecology Market Insight

The Germany uro-gynecology market is expected to register the fastest CAGR in the region from 2025 to 2032, driven by rising geriatric population, increasing awareness of urogynecological conditions, technological advancements in diagnostic and surgical procedures, expanding healthcare expenditure, and growing demand for minimally invasive treatment options.

U.K. Uro-Gynecology Market Insight

The U.K. uro-gynecology market is expected to register the growth in the region from 2025 to 2032, driven by increasing awareness of women’s health, rising cases of pelvic floor disorders, advancements in urogynecological treatments, supportive government initiatives, and growing adoption of minimally invasive surgical procedures.

Asia Pacific Uro-Gynecology Market Insight

The Asia Pacific uro-gynecology market is expected to register a notable CAGR from 2025 to 2032, driven by a rapidly aging population, increasing awareness of women’s health issues, rising healthcare investments, expanding access to advanced medical technologies, and growing demand for cost-effective uro-gynecological treatments in emerging economies such as China and India.

China Uro-Gynecology Market Insight

The China uro-gynecology market is expected to register a notable CAGR from 2025 to 2032, driven by a rapidly aging population, increasing healthcare investments, growing awareness of urogynecological conditions, rising demand for advanced medical technologies, and expansion of healthcare infrastructure in both urban and rural areas.

India Uro-Gynecology Market Insight

The India uro-gynecology market is expected to register a notable CAGR from 2025 to 2032, driven by increasing awareness of women's health issues, rising prevalence of pelvic floor disorders, expanding healthcare access in rural areas, growing medical tourism, and government initiatives supporting women's reproductive and urogynecological health.

Uro-Gynecology Market Share

The Uro-Gynecology industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Medtronic (Ireland)

- Cook Medical (U.S.)

- Teleflex Incorporated (U.S.)

- Coloplast (Denmark)

- Hollister Incorporated (U.S.)

- Integer Holdings Corporation (U.S.)

- Laborie (Canada)

- Convatec Group PLC (U.K.)

- Cooper Surgical, Inc. (U.S.)

- B. Braun SE (Germany)

- Caldera Medical (U.S.)

- Synkotech Biocompatible Materials SL (Spain)

- W. L. Gore & Associates, Inc. (U.S.)

- Neomedic International (Spain)

- DynaMesh (part of FEG Textiltechnik mbH) (Germany)

- Poly-Med Incorporated (U.S.)

- PROMEDON (Argentina)

- Betatech Medical (Turkey)

- Bioseal Inc (U.S.)

- pfm medical gmbh (Germany)

- American Medical Systems (Now part of Boston Scientific) (U.S.)

- Bezwada Biomedical, LLC (U.S.)

Latest Developments in Global Uro-Gynecology Market

- In January, Boston Scientific completed its acquisition of Axonics Inc.This significant move has expanded Boston Scientific's Urology and Pelvic Health business by integrating Axonics' cutting-edge sacral neuromodulation (SNM) systems, which are instrumental in treating urinary and bowel dysfunction, directly addressing conditions prevalent in urogynecology

- In February, Boston Scientific implemented management changes and restructuring initiatives that resulted in the creation of a dedicated Urology and Pelvic Health division. This strategic reorganization, which has been in place for some time, underscores Boston Scientific's focused commitment to developing and commercializing products for urinary, pelvic floor, and related women's health conditions, thereby bolstering its impact on the urogynecology field

- In April, Boston Scientific's Urology and Women's Health Division solidified its long-standing marketing alliance with Bladder Health Network, making it exclusive with a four-year agreement back on April 19, 2010. This enduring partnership continues to promote greater access to advanced diagnostic solutions, such as urodynamic testing, for female urinary incontinence and other urinary system problems, which directly supports diagnostic capabilities within the urogynecology market

- In April, Bioseal participated in the HSPA Conference 2024 in Las Vegas, showcasing its innovations and hosting CE-credit educational sessions on sterile processing and quality improvement. This engagement enhanced Bioseal’s industry visibility, strengthened customer education, and positioned the company as a thought leader in sterile processing and single-use surgical solutions

- In March 2023, Bioseal Inc. launched the BioBlue family—a range of single-use surgical instruments designed to reduce cleaning, sterilization labor, and turnaround times in sterile processing.This innovation strengthened Bioseal’s position in the OB/GYN and urogynecology markets by offering cost-effective, sterile, ready-to-use instruments that improve workflow efficiency and reduce infection risk in clinical settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.