Global Urogynecologic Surgical Mesh Implants Market

Market Size in USD Billion

USD

2.32 Billion

USD

3.45 Billion

2024

2032

USD

2.32 Billion

USD

3.45 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.32 Billion | |

| USD 3.45 Billion | |

| % | |

|

Urogynecologic Surgical Mesh Implants Market Size

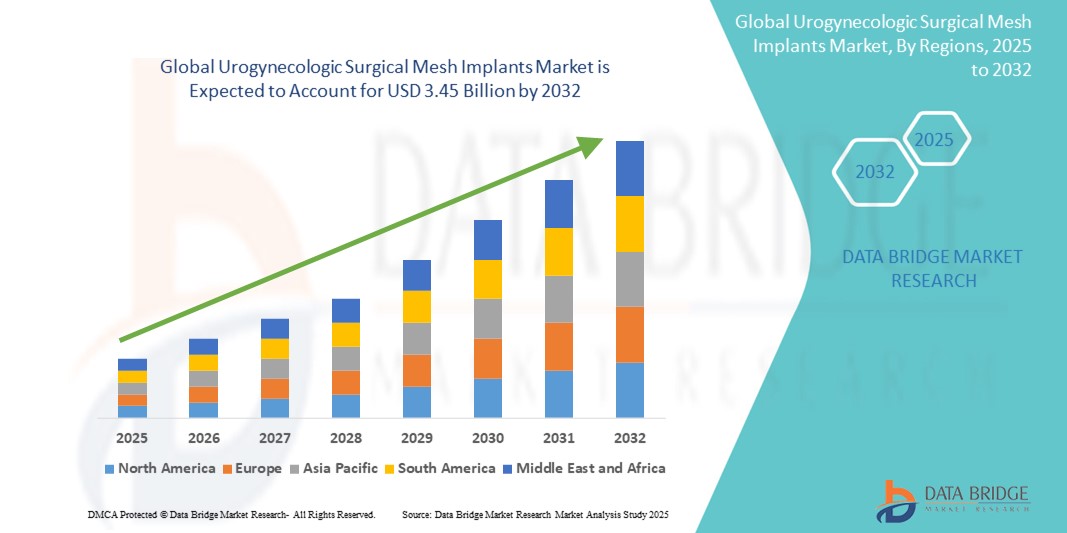

- The global urogynecologic surgical mesh implants market size was valued at USD 2.32 billion in 2024 and is expected to reach USD 3.45 billion by 2032, at a CAGR of 5.10% during the forecast period

- The market growth is largely fueled by the growing adoption of minimally invasive procedures and technological progress in biocompatible materials, leading to increased innovation in pelvic floor reconstruction techniques across hospital and ambulatory settings

- Furthermore, rising patient awareness regarding pelvic organ prolapse (POP) and stress urinary incontinence (SUI), coupled with the growing demand for effective, durable treatment options, is establishing urogynecologic surgical mesh implants as a preferred therapeutic choice. These converging factors are accelerating the uptake of urogynecologic surgical mesh implants, thereby significantly boosting the industry's growth

Urogynecologic Surgical Mesh Implants Market Analysis

- Urogynecologic surgical mesh implants, used to treat pelvic organ prolapse (POP) and stress urinary incontinence (SUI), are increasingly recognized as essential tools in gynecologic and urologic surgeries. These implants offer structural support to weakened pelvic tissues, significantly improving patient outcomes and quality of life. Their growing adoption is driven by advancements in minimally invasive surgical techniques and increased awareness of women’s pelvic health disorders

- The rising prevalence of pelvic floor disorders, particularly among aging populations and postmenopausal women, is a key driver for the urogynecologic surgical mesh implants market. In addition, enhanced materials such as lightweight, biocompatible mesh products and improved surgical approaches have minimized complications, further encouraging adoption

- North America dominated the urogynecologic surgical mesh implants market with the largest revenue share of 41.6% in 2024, attributed to the region's well-established healthcare infrastructure, favorable reimbursement policies, and high awareness of pelvic floor disorders. In the U.S., there is significant demand for minimally invasive procedures, with gynecologists and urogynecologists increasingly adopting mesh implants for faster recovery and improved long-term support

- Asia-Pacific is projected to be the fastest-growing region in the urogynecologic surgical mesh implants market with a CAGR of 9.8% during the forecast period of 2025 to 2032, owing to rising healthcare expenditure, increasing awareness about women’s health, and expanding access to gynecologic care. Countries like China, India, and Japan are seeing a notable rise in the number of urogynecologic surgeries, driven by an aging female population and urbanization

- The non-absorbable surgical mesh segment dominated the urogynecologic surgical mesh implants market with a revenue share of 48.6% in 2024, driven by its long-term durability and widespread use in pelvic organ prolapse (POP) and stress urinary incontinence (SUI) surgeries. These meshes offer strong and lasting support, making them the preferred choice in recurrent prolapse cases

Report Scope and Urogynecologic Surgical Mesh Implants Market Segmentation

|

Attributes |

Urogynecologic Surgical Mesh Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Urogynecologic Surgical Mesh Implants Market Trends

“Growing Preference for Minimally Invasive and Patient-Centric Solutions”

- A significant and accelerating trend in the global urogynecologic surgical mesh implants market is the increasing demand for minimally invasive surgical interventions for pelvic organ prolapse (POP) and stress urinary incontinence (SUI), especially among the aging female population

- Technological advances have led to the development of lightweight, biocompatible, and patient-specific mesh implants that improve clinical outcomes while reducing the risk of complications such as erosion or infection. Companies are increasingly focusing on mesh designs that mimic natural tissue behavior and facilitate faster recovery post-surgery

- For instance, Boston Scientific has developed the Solyx Single-Incision Sling System, which enables efficient treatment of SUI through a less invasive approach, reducing operative time and postoperative discomfort. Likewise, Medtronic’s synthetic mesh offerings are optimized for minimally invasive procedures and are gaining popularity across both developed and emerging healthcare systems

- Surgeons and healthcare providers are increasingly adopting urogynecologic mesh implants due to their ability to provide long-lasting anatomical support, especially in patients with recurrent prolapse or multiple vaginal deliveries. The rising awareness about pelvic health among women and improved diagnostics are further supporting this shift

- In addition, increased regulatory oversight in the U.S. and Europe, following safety concerns in earlier years, has driven manufacturers to enhance product safety, conduct long-term clinical trials, and provide surgeon training programs. This proactive approach is helping rebuild trust in mesh procedures, ultimately supporting market recovery and expansion

- The demand for urogynecologic surgical mesh implants is growing rapidly across hospital settings and specialty clinics, as healthcare systems globally continue to emphasize efficient, cost-effective, and patient-tailored pelvic floor solutions

Urogynecologic Surgical Mesh Implants Market Dynamics

Driver

“Growing Need Due to Increasing Pelvic Floor Disorders and Aging Population”

- The growing global prevalence of pelvic floor disorders (PFDs), such as stress urinary incontinence (SUI) and pelvic organ prolapse (POP), is significantly driving demand for urogynecologic surgical mesh implants, especially among postmenopausal and elderly women. These conditions are increasingly recognized and treated, leading to a surge in surgical interventions utilizing mesh implants

- For instance, according to the National Institutes of Health (NIH), up to 50% of women over the age of 50 are affected by some form of pelvic floor dysfunction, highlighting a massive patient base for surgical mesh treatments. As awareness grows and more women seek treatment, demand for durable and minimally invasive solutions like surgical mesh continues to rise

- Moreover, the aging global population is a key factor, with the World Health Organization (WHO) projecting that the number of people aged 60 years and above will double by 2050. With aging being a major risk factor for PFDs, healthcare systems worldwide are increasingly adopting urogynecologic mesh implants as standard treatment tools to improve quality of life and restore normal function

- Technological advancements, such as the development of lightweight, biocompatible, and partially absorbable meshes, as well as the shift toward laparoscopic and robotic-assisted procedures, are improving clinical outcomes and reducing complications, thereby supporting market growth

Restraint/Challenge

“Litigation and Safety Concerns Impacting Adoption”

- A major restraint in the urogynecologic surgical mesh implants market is the lingering safety and litigation concerns surrounding mesh-related complications such as erosion, infection, chronic pain, and mesh shrinkage. Past controversies, especially in the U.S. and Europe, have led to stricter regulatory scrutiny and public distrust

- For instance, the FDA reclassified transvaginal mesh devices for POP as high-risk (Class III) in 2016, and subsequently ordered the halt of sales in 2019 due to insufficient safety data from manufacturers. This significantly impacted market confidence and led to the withdrawal of many products

- Despite these challenges, manufacturers are actively working to address safety issues by developing next-generation meshes with improved materials, enhanced pore structures, and validated long-term safety data. The focus has shifted toward transabdominal approaches, which are considered safer than traditional transvaginal methods

- High litigation costs and regulatory hurdles remain a challenge for market expansion, particularly in North America and Europe. In addition, in many developing countries, limited access to trained urogynecologic surgeons and high procedure costs restrict the adoption of advanced mesh implants

- Overcoming these hurdles will require greater investment in clinical research, surgeon training, and regulatory transparency. Increasing public awareness about newer, safer alternatives and their long-term benefits will be critical for market recovery and growth

Urogynecologic Surgical Mesh Implants Market Scope

The market is segmented into four notable segments based on type, application, end user, and sales channel.

- By Type

On the basis of type, the urogynecologic surgical mesh implants market is segmented into non-absorbable surgical mesh, absorbable surgical mesh, and others. The non-absorbable surgical mesh segment dominated the largest market revenue share of 48.6% in 2024, driven by its long-term durability and widespread use in pelvic organ prolapse (POP) and stress urinary incontinence (SUI) surgeries. These meshes offer strong and lasting support, making them the preferred choice in recurrent prolapse cases.

The absorbable surgical mesh segment is expected to witness the fastest CAGR of 6.8% from 2025 to 2032, as advancements in biodegradable materials and innovations in tissue-regenerative mesh implants make them suitable for short-term support and reduce complications associated with long-term implantation.

- By Application

On the basis of application, the urogynecologic surgical mesh implants market is segmented into hernia repair, traumatic or surgical wounds, abdominal wall reconstruction, and facial surgery. The hernia repair segment held the largest market share of 41.3% in 2024, owing to the high incidence of hernia cases and the growing adoption of mesh implants as a standard treatment.

The abdominal wall reconstruction segment is projected to grow at the fastest CAGR of 7.1% during the forecast period, driven by increasing surgical interventions for complex abdominal procedures and the growing prevalence of obesity-related conditions requiring mesh-supported reconstruction.

- By End User

On the basis of end user, the urogynecologic surgical mesh implants market is segmented into hospitals, ambulatory surgical centers, clinics, and others. The hospital segment accounted for the largest market revenue share of 52.9% in 2024, supported by advanced infrastructure, skilled surgeons, and access to high-end mesh implant procedures.

Ambulatory surgical centers are expected to register the highest CAGR of 6.9% from 2025 to 2032, due to a shift towards outpatient care, shorter recovery times, and the cost-effectiveness of performing minimally invasive urogynecologic procedures in these settings.

- By Sales Channel

On the basis of sales channel, the urogynecologic surgical mesh implants market is segmented into direct channel and distribution channel. The direct channel segment dominated the market with a revenue share of 57.4% in 2024, as major manufacturers prioritize direct sales to hospitals and surgical centers for better control over pricing and product support.

The distribution channel segment is anticipated to grow at the fastest CAGR of 5.6% during the forecast period, fueled by expanding global supply chains and increasing penetration of mesh implant products in emerging markets through third-party distributors and e-commerce platforms.

Urogynecologic Surgical Mesh Implants Market Regional Analysis

- North America dominated the urogynecologic surgical mesh implants market with the largest revenue share of 41.6% in 2024, driven by the rising prevalence of pelvic organ prolapse (POP) and stress urinary incontinence (SUI) among women, alongside growing awareness about available surgical treatment options

- The region benefits from favorable reimbursement policies, widespread access to advanced surgical care, and the strong presence of key industry players such as Boston Scientific, Coloplast, and Becton, Dickinson and Company

- Ongoing innovations in mesh material—focusing on biocompatibility and reduced complication rates—are further supporting adoption in both academic and private hospital settings across the region

U.S. Urogynecologic Surgical Mesh Implants Market Insight

The U.S. urogynecologic surgical mesh implants market captured the largest revenue share of 61% in 2024 within North America, driven by a high incidence of pelvic floor disorders and the availability of experienced urogynecologic surgeons. Further, increasing insurance coverage, demand for minimally invasive procedures, and FDA-approved transabdominal mesh systems for sacrocolpopexy contribute to widespread adoption. R&D investments by U.S.-based companies to develop next-generation partially absorbable mesh devices have strengthened market leadership.

Europe Urogynecologic Surgical Mesh Implants Market Insight

The Europe urogynecologic surgical mesh implants market is projected to expand at a notable CAGR of over 5.3% during the forecast period, supported by an aging female population and increasing surgical volumes for POP and SUI. Regulatory scrutiny following previous mesh-related complications has led to a shift toward safer transabdominal and laparoscopic mesh procedures. Countries like Germany, the U.K., and France are investing in improving women’s health services, boosting the adoption of regulated surgical mesh products.

U.K. Urogynecologic Surgical Mesh Implants Market Insight

The U.K. urogynecologic surgical mesh implants market is anticipated to grow at a CAGR of 5.9% during the forecast period, driven by growing demand for pelvic reconstructive surgeries and rising awareness of post-childbirth incontinence treatments. NHS reforms and updated NICE guidelines promoting informed consent and safer alternatives have increased procedural transparency and patient uptake. The market is also seeing growth in public-private partnerships for women’s health infrastructure.

Germany Urogynecologic Surgical Mesh Implants Market Insight

The Germany urogynecologic surgical mesh implants market is expected to expand at a CAGR of 6.1%, owing to strong healthcare infrastructure, government-funded hospital systems, and early adoption of laparoscopic and robotic surgical technologies. Emphasis on clinical trials, biomaterial innovation, and surgeon-led quality assurance programs further accelerates market penetration.

Asia-Pacific Urogynecologic Surgical Mesh Implants Market Insight

The Asia-Pacific urogynecologic surgical mesh implants market is projected to grow at the fastest CAGR of 9.8% from 2025 to 2032, driven by increasing awareness of pelvic health, improved diagnostic capabilities, and expanded surgical access in countries like China, Japan, and India. Government initiatives in women's healthcare and expansion of hospital infrastructure are playing key roles. Manufacturing cost advantages and local production by players such as Hangzhou Kangji Medical contribute to regional affordability and access.

Japan Urogynecologic Surgical Mesh Implants Market Insight

The Japan urogynecologic surgical mesh implants market is gaining momentum due to a rapidly aging population, with over 28% of the population above 65 years, and increased cases of POP. The market is shaped by strong surgical skill development, conservative regulatory oversight, and rising demand for minimally invasive, patient-friendly mesh products tailored to elderly patients.

China Urogynecologic Surgical Mesh Implants Market Insight

The China urogynecologic surgical mesh implants market accounted for the largest revenue share in the Asia-Pacific region in 2024, supported by an expanding healthcare infrastructure and growing awareness of women’s pelvic health. A rapidly growing middle class, government investment in surgical innovation, and the presence of domestic mesh producers have improved access to affordable treatments. The country's shift toward urbanized, hospital-based care is enabling quicker diagnosis and elective POP surgeries, enhancing market performance.

Urogynecologic Surgical Mesh Implants Market Share

The urogynecologic surgical mesh implants industry is primarily led by well-established companies, including:

- W. L. Gore & Associates, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- Mölnlycke Health Care AB (Sweden)

- Medical Devices Business Services, Inc. (U.S.)

- BD (Becton, Dickinson and Company) (U.S.)

- Medtronic (Ireland)

- LifeCell International Pvt. Ltd. (India)

- B. Braun SE (Germany)

- Betatech Medical (Turkey)

- Atrium Medical Corporation (U.S.)

Latest Developments in Global Urogynecologic Surgical Mesh Implants Market

- In April 2024, the U.S. FDA completed its evaluation of “522 studies” on stress urinary incontinence mini-slings, confirming comparable effectiveness and safety to traditional mid‑urethral slings over a 36-month follow‑up period. This milestone underscores ongoing regulatory scrutiny aimed at ensuring mesh safety and boosting patient confidence

- In April 2019, the FDA has enforced a ban on surgical mesh for transvaginal repair of pelvic organ prolapse. Following a 2016 device reclassification to Class III (high-risk), major manufacturers such as Boston Scientific, Coloplast, and Ethicon ceased distribution in the U.S. due to concerns over safety and efficacy

- In January 2024, the FDA continues to monitor and analyze adverse event reports and postmarket data for urogynecologic surgical mesh. Its epidemiological reviews and literature assessments ensure ongoing benefits outweigh risks

- In April, 2019 marks the official FDA mandate requiring manufacturers to stop selling all mesh devices for transvaginal POP repair, following an advisory committee’s recommendation. Data demonstrated increased risks of mesh exposure and erosion compared to native tissue repair

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.