Usher Syndrome Type 2 Treatment Market Size

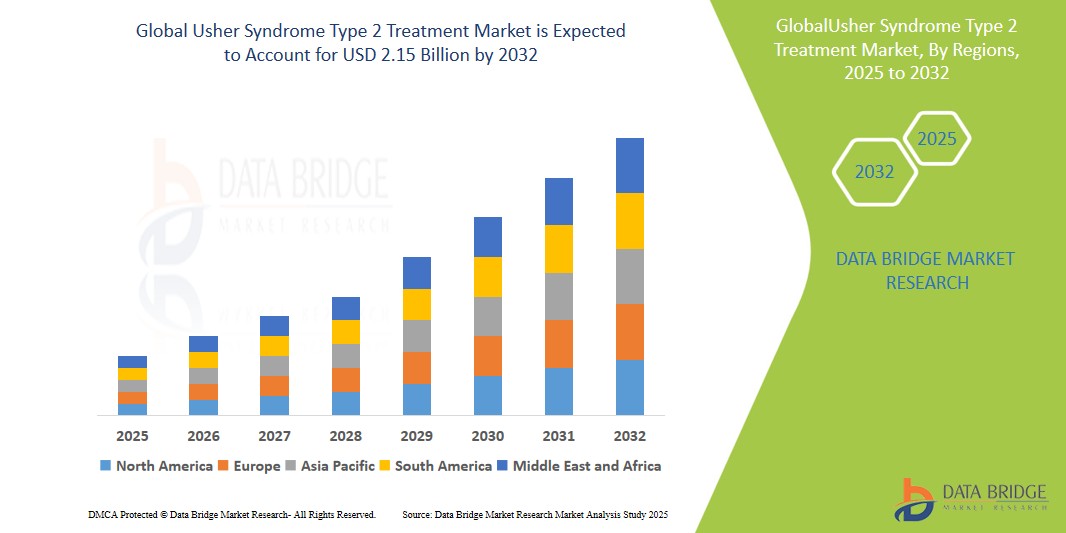

- The global usher syndrome type 2 treatment market size was valued at USD 1.35 billion in 2024 and is expected to reach USD 2.15 billion by 2032, at a CAGR of 6.0% during the forecast period

- This growth is driven by increasing awareness of genetic disorders, rising investment in gene therapy R&D, and improving diagnostic capabilities globally

Usher Syndrome Type 2 Treatment Market Analysis

- Usher Syndrome Type 2 is a genetic condition characterized by moderate to severe hearing loss and progressive vision loss due to retinitis pigmentosa. Treatment focuses on managing hearing loss, vision impairment, and emerging genetic therapies

- The market is expanding due to increasing initiatives in rare disease treatment, rapid advances in genomics, and improved newborn screening protocols

- North America dominates the usher syndrome type 2 treatment market with a market share of approximately 39.16%, driven by high diagnostic awareness, access to specialized care, and active clinical trials

- Asia-Pacific is projected to grow at the fastest pace and currently holds an estimated market share of 30.23%, due to improvements in genetic testing infrastructure and growing investment in orphan disease treatment

- The cochlear implant segment is expected to dominate with a market share of 39.2% due to greater reimbursement support and enhanced post-implant outcomes

Report Scope and Usher Syndrome Type 2 Treatment Market Segmentation

|

Attributes |

Usher Syndrome Type 2 Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Usher Syndrome Type 2 Treatment Market Trends

"Emerging Role of Gene Therapy in Treating Usher Syndrome Type 2"

- Gene therapy is increasingly recognized as a promising solution to address the genetic mutations causing Usher Syndrome Type 2, especially USH2A variants. RNA-based therapies, such as antisense oligonucleotides (AONs), and dual-vector adeno-associated virus (AAV) approaches are targeting the large USH2A gene to restore functional usherin protein, offering potential to halt or reverse vision loss.

- There is growing clinical momentum and regulatory encouragement for orphan drugs, with the FDA and EMA granting fast-track and orphan drug designations to therapies like ultevursen, accelerating approval pathways in the U.S. and Europe. Research is focusing on dual-vector strategies to overcome the large size of USH2A, which exceeds traditional AAV capacity, while CRISPR-based exon-skipping techniques are being explored for precise, long-term gene repair. Gene therapy is reshaping the treatment outlook for Usher Syndrome Type 2 by offering curative potential rather than symptomatic management, with ongoing trials signaling a shift toward disease-modifying interventions

- For Instance, In 2024, ProQR advanced its clinical-stage program, sepofarsen, which demonstrated photoreceptor preservation and functional visual gains in a Phase II trial, while its ultevursen (formerly QR-421a) progressed to the LUNA Phase 2b trial, dosing its first patient in December 2024.

- Such gene therapy’s emergence, driven by RNA therapies and dual-vector innovations, is transforming Usher Syndrome Type 2 treatment, with regulatory support and clinical advancements paving the way for curative solutions.

Usher Syndrome Type 2 Treatment Market Dynamics

Driver

" Advances in Genetic Research and Testing "

- The rise of whole-exome sequencing and low-cost genetic panels has revolutionized early detection of Usher Syndrome Type 2 mutations, enabling timely interventions like cochlear implants and genetic counseling. Collaborative genomic initiatives, such as the Foundation Fighting Blindness’s My Retina Tracker Program, are building comprehensive USH2A mutation databases to guide therapy development.

- These advancements facilitate precise diagnosis, improve treatment readiness, and prioritize gene therapy pipelines, driving demand for targeted therapies. Genetic research is accelerating the identification of novel USH2A variants, supporting personalized medicine and enhancing clinical trial recruitment for therapies like ultevursen.

- For Instance: Studies in 2023 showed that early genetic testing led to timely fitting of assistive hearing devices and informed family planning, reducing disease burden in affected families.

- Genetic research advancements, particularly in sequencing and mutation databases, are driving early detection and personalized treatment for Usher Syndrome Type 2, fueling market growth and innovation.

Opportunity

" Increasing Public and Private Funding for Rare Diseases"

- Governments and private foundations are committing significant resources to rare disease research, including Usher Syndrome Type 2, to support therapeutic development and clinical infrastructure. The Foundation Fighting Blindness’s RD Fund and other venture philanthropy initiatives are investing in promising therapies like ultevursen.

- Biotech startups focusing on vision and hearing restoration, such as Sepul Bio, have raised substantial venture capital, expediting RNA therapy trials and assistive technology development. These investments are creating opportunities for scaling treatment access, advancing dual-vector and CRISPR-based therapies, and accelerating regulatory approvals.

- For Instance,In 2023, the EU committed EUR 150 million under Horizon Europe for orphan disease therapeutics, including inherited retinal and auditory disorders, boosting trials for USH2A-targeted therapies.

- Robust funding from public and private sectors is catalyzing Usher Syndrome Type 2 research and therapy development, expanding access and driving transformative market opportunities.

Restraint/Challenge

" High Cost and Accessibility of Advanced Therapies"

- Gene therapies like ultevursen and cochlear implants are prohibitively expensive, often costing hundreds of thousands of dollars, and are not consistently covered by insurance, particularly in developing countries. Manufacturing complexities and cold chain logistics further limit availability.

- Limited awareness among general practitioners delays referrals to specialists, exacerbating diagnostic and treatment gaps, especially in rural areas. Efforts to address costs through subsidies and public-private partnerships, such as those supported by Horizon Europe, are underway but face challenges in scaling to meet global demand.

- For Instance, A 2023 report highlighted that only 20% of patients in low-income regions had access to cochlear implants due to cost and infrastructure barriers, with similar challenges for gene therapies.

- The high cost and limited accessibility of gene therapies and assistive devices pose significant challenges to the Usher Syndrome Type 2 treatment market, requiring scalable solutions to ensure equitable access.

Usher Syndrome Type 2 Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, mode of administration, distribution channel, and end user

|

Segmentation |

Sub-Segmentation |

|

|

|

By Diagnosis |

|

|

By Mode of Administration |

|

|

By End User |

|

|

By Distribution Channel

|

|

In 2025, the Cochlear Implant is projected to dominate the market with a largest share in therapy type segment

In 2025, the Cochlear Implant segment is projected to dominate the market with the highest growth rate, holding a projected share of 38.6%, driven by their proven efficacy, technological advancements, and the growing demand for effective interventions. Early cochlear implantation is particularly beneficial for USH2 patients, especially before the onset of significant visual deterioration due to retinitis pigmentosa. Timely intervention can prevent compounded sensory deficits, leading to better communication outcomes .

The Hospital segment expected to account for the largest share during the forecast period in end user market

In 2025, the hospitals are expected to account for the largest market share of 54.2% during the forecast period. Hospitals serve as primary centers for diagnosing and treating Usher Syndrome Type 2, offering a range of services including genetic testing, audiological evaluations, and advanced therapies such as gene and stem cell treatments.

Usher Syndrome Type 2 Treatment Market Regional Analysis

“North America Holds the Largest Share in the Usher Syndrome Type 2 Treatment Market”

- North America dominates the Usher Syndrome Type 2 treatment market, accounting for an estimated 39.6% of the global market share in 2025. This leadership is attributed to high diagnostic awareness, access to specialized neuro-otology and genetic services, and an active pipeline of clinical trials for gene and drug therapies.

- The United States leads the region with an estimated 32.4% market share, supported by robust regulatory frameworks, including Orphan Drug Designations, NIH-funded rare disease initiatives, and early-stage clinical research funding through the FDA and academic consortia.

- Multi-center research networks, such as the RDCRN (Rare Diseases Clinical Research Network) and Auditory Clinical Research Centers, across the U.S. and Canada are facilitating rapid patient enrollment and trial execution for therapies targeting both retinitis pigmentosa and progressive hearing loss associated with Usher Syndrome Type 2.

- National strategies aimed at inclusive newborn hearing screening, genomic mapping programs, and patient advocacy group participation (e.g., Foundation Fighting Blindness) continue to enhance early detection, genetic counseling, and therapeutic uptake, strengthening North America's dominance.

“Asia-Pacific is Projected to Register the Highest CAGR in the Usher Syndrome Type 2 Treatment Market”

- The Asia-Pacific region is projected to grow at the highest compound annual growth rate (CAGR) in the Usher Syndrome Type 2 treatment market and currently holds an estimated 18.7% market share in 2025. This expansion is fueled by rapid adoption of genetic testing, growing government subsidies for orphan and sensory disorder treatments, and cross-border collaborations in precision medicine.

- China and India are leading regional growth, driven by national newborn screening policies, integration of Usher syndrome testing in genetic panels, and collaborative gene therapy research with global institutions and biotech firms.

- Emerging biotech ecosystems in Singapore, South Korea, and Japan are investing heavily in R&D for neurogenetic and sensory impairments, boosting the pipeline for gene editing, retinal implants, and personalized cochlear therapies.

- Government-supported national health plans, the rise of urban diagnostic lab chains, and public-private partnerships for audiology and low vision rehabilitation services are enabling earlier diagnosis and broader treatment access across the region, especially in metro hospitals and academic centers.

Usher Syndrome Type 2 Treatment Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- ProQR Therapeutics N.V. (Netherlands)

- Sensorion (F rance)

- Decibel Therapeutics, Inc. (U.S.)

- Akouos, Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- MeiraGTx Holdings plc (U.K.)

- Editas Medicine (U.S.)

- Spark Therapeutics (U.S.)

- Otonomy, Inc. (U.S.)

- ReNeuron Group plc (U.K.)

- Audina Hearing Instruments Inc. (U.S.)

- Oticon Medical (Denmark)

- MED-EL (Austria)

- Cochlear Ltd (Australia)

- Advanced Bionics AG (Switzerland)

Latest Developments in Global Usher Syndrome Type 2 Treatment Market

- In January 2025, ProQR Therapeutics initiated a Phase 1/2 clinical trial named STELLAR for QR-421a, an investigational RNA-based oligonucleotide therapy. The QR-421a molecule is designed to skip exon 13 of the USH2A gene, which is one of the most common mutations associated with Usher Syndrome Type 2. Early preclinical studies demonstrated that this exon skipping approach can restore the function of the USH2A protein, potentially halting or reversing vision deterioration. The STELLAR trial is evaluating both safety and efficacy, with patients undergoing multiple dosing regimens and long-term retinal monitoring through imaging and functional vision tests.

- In September 2024, Nacuity Pharmaceuticals commenced a Phase 2 clinical trial for NACA, a chemically modified form of N-acetylcysteine (NAC), aimed at reducing oxidative stress and protecting photoreceptor cells in patients with retinitis pigmentosa linked to Usher Syndrome. The trial, which is being conducted across several international sites, is assessing NACA’s ability to slow disease progression and improve retinal function. Interim data analysis is expected by mid-2025, and a Phase 3 trial will be initiated pending positive efficacy results and regulatory consultations.

- In January 2025, the Usher Syndrome Society launched the Pipeline for Usher Syndrome Research (PUSH), a large-scale research collaboration anchored at Boston Children’s Hospital. The PUSH initiative aims to accelerate the discovery and development of novel treatments by enabling access to patient registries, biobanks, and genetic testing data. Through partnerships with academic institutions, biotech firms, and advocacy groups, PUSH will focus on genotype-phenotype correlations, mutation-specific therapies, and standardization of outcome measures for clinical trials.

- In March 2024, researchers introduced dithio-CN03, a newly synthesized small-molecule compound that targets degenerative pathways in rod photoreceptors affected by retinitis pigmentosa. Preclinical testing in animal models demonstrated that dithio-CN03 can preserve rod structure and function, potentially extending the visual field and delaying the onset of blindness in Usher Syndrome patients. The compound works by modulating oxidative stress and enhancing cellular resilience against apoptotic signals. Further development is planned through public-private funding initiatives.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.