Global Uterine Carcinosarcoma Market

Market Size in USD Billion

USD

25.72 Billion

USD

42.56 Billion

2025

2033

USD

25.72 Billion

USD

42.56 Billion

2025

2033

| 2026 - 2033 | |

| USD 25.72 Billion | |

| USD 42.56 Billion | |

| % | |

|

Uterine Carcinosarcoma Market Overview

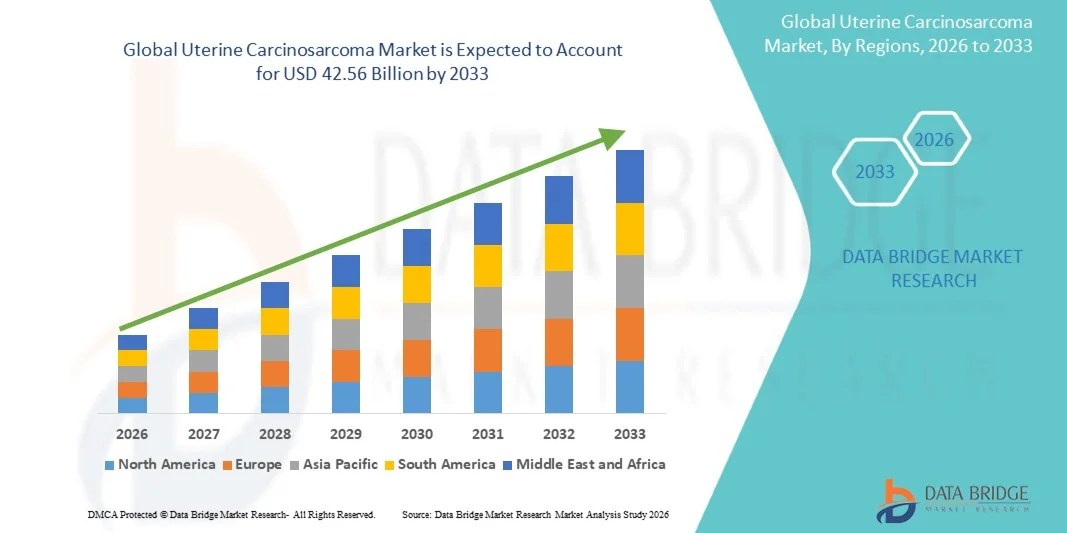

The Uterine Carcinosarcoma Market was valued at USD 25.72 billion in 2025 and is projected to reach USD 42.56 billion by 2033, growing at a CAGR of 6.50% from 2026 to 2033. The market is witnessing steady growth driven by increasing incidence of rare and aggressive uterine cancers, improved diagnostic accuracy through advanced imaging and molecular testing, and rising awareness regarding early oncological screening and personalized treatment approaches.

The growing burden of gynecologic malignancies, along with advancements in multimodal treatment strategies including surgery, chemotherapy, and targeted therapy, is driving demand for more effective therapeutic solutions. In addition, expanding oncology research pipelines and increased clinical trial activity focused on rare endometrial cancers are supporting market development. Healthcare systems are also emphasizing precision medicine and biomarker-based therapies, further contributing to the adoption of advanced treatment protocols in uterine carcinosarcoma management.

Key Market Trends & Insights

- North America dominated the Uterine Carcinosarcoma Market with the largest revenue share of 38.6% in 2025, supported by advanced oncology infrastructure, high diagnosis rates, and strong presence of specialized cancer centers.

- The Homologous Carcinosarcoma segment led the market with a 62.4% share in 2025, driven by its higher clinical prevalence and more frequent diagnosis in uterine malignancy cases.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.9% from 2026 to 2033, fueled by rising gynecologic cancer burden, improving diagnostic access, and expanding oncology treatment infrastructure in emerging economies.

- Heterologous Carcinosarcoma are the fastest-growing type, projected to register a CAGR of 7.6%, reflecting the surge in improved diagnostic capabilities and rising awareness of rare tumor variants.

- The Chemotherapy segment dominated the treatment type category with a 46.2% revenue share in 2025, led by its position as the standard first-line and adjuvant treatment for most patients.

- Intravenous accounted for 71.8% of the market, preferred by hospitals and oncology specialists due to its ability to deliver high-potency chemotherapy and immunotherapy agents directly into the bloodstream

- The Oral segment is the fastest-growing route of administration category, with a CAGR of 6.9%, driven by the increasing development of oral targeted therapies and supportive care drugs.

Market Size & Forecast

- Global Market Value (2025): USD 25.72 Billion

- Expected Market Value (2033): USD 42.56 Billion

- Forecast CAGR (2026–2033): 6.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Uterine Carcinosarcoma Market Segmentation

|

Attributes |

Uterine Carcinosarcoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Merck & Co., Inc. (U.S.) · Bristol-Myers Squibb Company (U.S.) · AstraZeneca (U.K.) · Pfizer Inc. (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · Novartis AG (Switzerland) · Eli Lilly and Company (U.S.) · AbbVie Inc. (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Amgen Inc. (U.S.) · GSK plc (U.K.) · Sanofi (France) · Bayer AG (Germany) · Takeda Pharmaceutical Company Limited (Japan) · Astellas Pharma Inc. (Japan) · Daiichi Sankyo Company, Limited (Japan) · Seagen Inc. (U.S.) · Exelixis, Inc. (U.S.) · Clovis Oncology, Inc. (U.S.) · BeiGene Ltd. (China) |

|

Market Opportunities |

· Rising adoption of precision oncology and biomarker-driven therapies · Expanding clinical trial activity for rare gynecologic cancers · Increasing integration of molecular diagnostics in routine cancer profiling |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Uterine Carcinosarcoma Market Trends

Trend: Rising Adoption of Precision Oncology and Molecular Profiling

Hospitals and cancer centers are increasingly adopting molecular profiling and genomic testing to better classify uterine carcinosarcoma subtypes and guide personalized treatment decisions. This shift toward precision oncology is improving early detection accuracy and enabling more targeted therapy selection, particularly in advanced and recurrent cases. The integration of next-generation sequencing (NGS) and biomarker-based testing is also supporting clinical trial enrollment and expanding research into rare uterine malignancies, while multidisciplinary tumor boards are using integrated data to refine treatment pathways. For instance, comprehensive genomic profiling is now being incorporated into endometrial cancer management protocols in leading oncology institutes

Uterine Carcinosarcoma Market Dynamics

Key Market Driver: Increasing Focus on Advanced Gynecologic Cancer Treatment

The rising incidence of aggressive uterine cancers and growing awareness among clinicians is driving demand for advanced treatment options such as combination chemotherapy, immunotherapy, and targeted therapy approaches. Healthcare systems are increasingly prioritizing early diagnosis and multimodal treatment strategies to improve survival outcomes in rare and high-risk gynecologic malignancies. Pharmaceutical companies are also expanding oncology pipelines focused on rare uterine tumors, supported by increasing regulatory incentives for orphan cancer drugs. For instance, ongoing clinical studies evaluating immune checkpoint inhibitors in uterine carcinosarcoma patients highlight this growing treatment focus.

Key Restraint/Challenge: Limited Early Diagnosis and High Treatment Complexity

A major challenge in the uterine carcinosarcoma market is the difficulty in achieving early and accurate diagnosis due to its rarity and overlapping histological features with other endometrial cancers. Delayed detection often results in advanced-stage diagnosis, which significantly limits treatment effectiveness and survival outcomes. In addition, complex multimodal treatment regimens involving surgery, chemotherapy, and radiation increase patient burden and healthcare costs. For instance, many cases are still diagnosed post-hysterectomy following non-specific symptom presentation, reflecting diagnostic limitations in routine clinical settings.

Key Market Opportunity: Expansion of Immunotherapy and Clinical Research Programs

The growing adoption of immunotherapy and expansion of clinical research initiatives presents a strong opportunity for market growth in uterine carcinosarcoma treatment. Pharmaceutical companies and research institutions are increasingly focusing on rare tumor-specific trials, enabling access to novel drug combinations and personalized treatment strategies. The development of global clinical trial networks and collaborative oncology research platforms is further accelerating drug development for rare gynecologic cancers. For instance, multi-center trials evaluating PD-1 and PD-L1 inhibitors in advanced endometrial malignancies are expanding therapeutic possibilities for this patient population.

Uterine Carcinosarcoma Market Scope

The uterine carcinosarcoma market is segmented on the basis of type, treatment type, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Uterine Carcinosarcoma Market is segmented into homologous carcinosarcoma and heterologous carcinosarcoma. The Homologous Carcinosarcoma segment dominated the market with a 62.4% share in 2025, owing to its higher clinical prevalence and more frequent diagnosis in uterine malignancy cases. This subtype is more commonly encountered in endometrial cancer progression, leading to greater focus in clinical research and treatment protocols. Improved histopathological techniques and molecular diagnostics are enhancing detection accuracy for this type. It is also more responsive to standard chemotherapy regimens compared to heterologous forms, supporting its clinical dominance. Increasing hospital-based case identification and cancer registry reporting further strengthen its market share. Overall, its higher incidence rate and established treatment pathways drive segment leadership.

The Heterologous Carcinosarcoma segment is expected to register the fastest growth with a CAGR of 7.6% from 2026 to 2033, driven by improved diagnostic capabilities and rising awareness of rare tumor variants. This subtype is increasingly being identified through advanced molecular profiling and immunohistochemistry testing. Growing research interest in aggressive and treatment-resistant tumors is supporting clinical trial expansion. It often requires more complex treatment approaches, which is driving innovation in targeted and combination therapies. Increasing investment in rare cancer research is further accelerating segment growth. In addition, enhanced pathology reporting standards are improving detection rates globally.

- By Treatment Type

On the basis of treatment type, the Uterine Carcinosarcoma Market is segmented into chemotherapy, immunotherapy, targeted therapy, hormone therapy, and brachytherapy. The Chemotherapy segment dominated the market with a 46.2% share in 2025, due to its position as the standard first-line and adjuvant treatment for most patients. Platinum-based combination regimens remain widely used in clinical practice. Hospitals rely heavily on chemotherapy due to established treatment guidelines and availability across healthcare systems. It is often combined with surgery to improve survival outcomes in advanced cases. Strong reimbursement support in developed markets further sustains its dominance. Despite toxicity concerns, its proven efficacy in aggressive tumors reinforces its widespread use.

The Immunotherapy segment is expected to grow the fastest with a CAGR of 8.3% from 2026 to 2033, driven by increasing clinical trials evaluating immune checkpoint inhibitors in rare gynecologic cancers. Advancements in PD-1/PD-L1 inhibitors are expanding treatment possibilities for refractory cases. Combination therapies involving immunotherapy and chemotherapy are gaining traction in oncology pipelines. Rising focus on precision medicine is accelerating adoption in specialized cancer centers. Regulatory incentives for orphan oncology drugs are further boosting development activity. Expanding biomarker-based patient selection is improving treatment effectiveness and uptake.

- By Route of Administration

On the basis of route of administration, the Uterine Carcinosarcoma Market is segmented into oral, intravenous, and others. The Intravenous segment dominated the market with a 71.8% share in 2025, as most chemotherapy and immunotherapy agents are administered through IV infusion. This route ensures rapid drug delivery and controlled dosing in hospital settings. Oncology treatment protocols for uterine carcinosarcoma heavily rely on IV-based combination regimens. Hospital infrastructure is well-equipped for infusion-based cancer therapies, supporting its dominance. IV administration also allows close monitoring of adverse effects in high-risk patients. The severity of the disease further reinforces the need for controlled hospital-based treatment delivery.

The Oral segment is expected to grow the fastest with a CAGR of 6.9% from 2026 to 2033, driven by increasing development of oral targeted therapies and supportive care drugs. Oral administration improves patient convenience and reduces hospital dependency. Advances in drug formulation are enabling better bioavailability of oncology drugs. Rising adoption of outpatient cancer care models is supporting segment growth. Patients with long-term maintenance therapy increasingly prefer oral medications. Expanding pipeline of oral kinase inhibitors is further accelerating adoption.

- By End-Users

On the basis of end-users, the Uterine Carcinosarcoma Market is segmented into hospitals, homecare, specialty centres, and others. The Hospitals segment dominated the market with a 64.5% share in 2025, due to the availability of advanced oncology infrastructure and multidisciplinary treatment teams. Most surgeries, chemotherapy, and radiation therapies are performed in hospital settings. Hospitals also serve as primary centers for cancer diagnosis and staging. High patient inflow and strong reimbursement frameworks support segment dominance. Integration of diagnostic and therapeutic services enhances treatment efficiency. Complex disease management requirements further reinforce hospital preference.

The Specialty Centres segment is expected to grow the fastest with a CAGR of 7.8% from 2026 to 2033, driven by rising demand for specialized oncology care. These centres offer focused expertise in rare and aggressive cancers such as uterine carcinosarcoma. Increasing adoption of precision medicine and clinical trial participation is boosting their role. Patients prefer specialty centres for advanced treatment options and improved outcomes. Growing investments in cancer-specific healthcare infrastructure are further supporting expansion. Collaboration with pharmaceutical companies for research programs is also accelerating growth.

- By Distribution Channel

On the basis of distribution channel, the Uterine Carcinosarcoma Market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The Hospital Pharmacy segment dominated the market with a 68.9% share in 2025, as most oncology drugs are dispensed directly within hospital treatment settings. High-cost chemotherapy and immunotherapy drugs are typically administered under strict medical supervision. Hospital pharmacies ensure controlled storage, dosing accuracy, and compliance with treatment protocols. Strong integration with inpatient and outpatient oncology departments supports dominance. Emergency access to critical cancer medications further strengthens this channel. Institutional procurement systems also reinforce its leading position.

The Online Pharmacy segment is expected to grow the fastest with a CAGR of 8.1% from 2026 to 2033, driven by increasing digitalization of healthcare services. Growing adoption of tele-oncology and home-based supportive care is supporting demand. Patients prefer convenient drug delivery and refill options for maintenance therapies. Expansion of regulated e-pharmacy platforms is improving accessibility and safety. Rising penetration of digital health ecosystems is further accelerating growth. However, strict regulatory frameworks still limit full-scale adoption in oncology drugs.

Uterine Carcinosarcoma Market Regional Analysis

North America dominated the Uterine Carcinosarcoma Market with the largest revenue share of 38.6% in 2025, supported by advanced oncology infrastructure, high diagnosis rates, and strong presence of specialized cancer centers. The region also benefits from widespread adoption of precision medicine approaches, strong clinical trial activity for rare uterine cancers, and high accessibility to advanced diagnostic tools such as molecular and genetic testing. Increasing focus on immunotherapy-based treatment strategies and well-established reimbursement systems continues to strengthen North America’s leadership position in the global market.

U.S. Uterine Carcinosarcoma Market Insight

The U.S. uterine carcinosarcoma market is witnessing steady growth due to rising incidence of aggressive endometrial cancers, strong adoption of advanced oncology diagnostics, and increasing availability of precision medicine-based treatment options. The country’s well-established healthcare infrastructure, along with widespread use of molecular profiling, immunotherapy, and targeted therapy, is driving demand across hospitals and specialty cancer centers. In addition, strong clinical trial activity focused on rare gynecologic cancers and high awareness regarding early cancer detection are accelerating market expansion in the U.S.

Europe Uterine Carcinosarcoma Market Insight

The Europe uterine carcinosarcoma market remains a significant contributor to global revenue, driven by strong public healthcare systems, increasing cancer screening programs, and growing adoption of advanced treatment protocols. The widespread use of multidisciplinary oncology care and expanding access to biomarker-based diagnostics are supporting market growth across the region. Increasing investment in rare cancer research, coupled with rising adoption of immunotherapy and targeted therapies, continues to strengthen Europe’s position in the Uterine Carcinosarcoma Market.

U.K. Uterine Carcinosarcoma Market Insight

The U.K. uterine carcinosarcoma market is experiencing steady growth, supported by rising focus on gynecologic cancer awareness, expanding NHS cancer care programs, and increasing adoption of precision oncology approaches. Growing utilization of genomic testing and advanced imaging technologies is improving early diagnosis and treatment planning. Furthermore, participation in international clinical trials and strong research collaboration networks are enhancing access to innovative therapies, positioning the U.K. as an important contributor in rare uterine cancer management.

Germany Uterine Carcinosarcoma Market Insight

The Germany uterine carcinosarcoma market is expanding steadily due to the country’s advanced healthcare infrastructure, strong oncology research ecosystem, and increasing adoption of personalized cancer treatment strategies. Leading cancer centers are actively integrating molecular diagnostics and multimodal treatment approaches for rare uterine malignancies. Continuous advancements in immunotherapy research, along with strong government support for oncology innovation and clinical studies, are further driving market growth in Germany.

Asia-Pacific Uterine Carcinosarcoma Market Insight

The Asia-Pacific uterine carcinosarcoma market is expected to witness rapid growth, driven by increasing gynecologic cancer burden, improving healthcare infrastructure, and rising adoption of advanced oncology diagnostics across countries such as China, India, and Japan. Growing awareness regarding early cancer detection, expanding access to specialized treatment centers, and increasing investments in precision medicine are supporting regional market expansion. In addition, rising clinical research activity and improving availability of immunotherapy-based treatments are accelerating growth across the region.

Japan Uterine Carcinosarcoma Market Insight

The Japan uterine carcinosarcoma market is witnessing consistent growth due to strong emphasis on advanced cancer research, high adoption of molecular diagnostics, and increasing use of precision oncology approaches. Leading hospitals and research institutes are actively integrating genomic testing and targeted therapies into treatment protocols for rare gynecologic cancers. Moreover, Japan’s strong focus on innovation in immunotherapy and structured cancer care systems is further supporting market development.

China Uterine Carcinosarcoma Market Insight

The China uterine carcinosarcoma market is growing rapidly, driven by rising incidence of gynecologic cancers, expanding oncology infrastructure, and increasing adoption of advanced diagnostic and treatment technologies. Government initiatives to improve cancer screening programs and strengthen hospital capabilities are boosting early detection rates. In addition, growing investments in immunotherapy research, expanding clinical trials, and increasing accessibility to precision medicine are positioning China as one of the fastest-growing markets for uterine carcinosarcoma globally.

Uterine Carcinosarcoma Market Share

The uterine carcinosarcoma industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Eli Lilly and Company (U.S.)

- AbbVie Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Amgen Inc. (U.S.)

- GSK plc (U.K.)

- Sanofi (France)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Astellas Pharma Inc. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Seagen Inc. (U.S.)

- Exelixis, Inc. (U.S.)

- Clovis Oncology, Inc. (U.S.)

- BeiGene Ltd. (China)

Latest Developments in Uterine Carcinosarcoma Market

- In March 2026, early-stage clinical research programs reported encouraging outcomes from combination immunotherapy trials involving pembrolizumab in recurrent gynecologic cancers, including endometrial malignancies. Phase I data showed durable responses in heavily pretreated patients, supporting continued exploration of immune-based combination regimens for rare uterine cancers such as carcinosarcoma, where treatment options remain limited and survival outcomes remain poor

- In May 2025, Journal of Clinical Oncology presented data on pembrolizumab plus lenvatinib in advanced or recurrent uterine carcinosarcoma, showing clinical activity in a rare cancer population with historically poor prognosis. The study reported objective responses and progression control in a subset of patients, reinforcing the potential of combination immunotherapy in treatment-resistant uterine malignancies and supporting ongoing clinical trial expansion

- In October 2024, Gynecologic Oncology Reports published clinical evidence on the combination of lenvatinib and pembrolizumab in patients with uterine carcinosarcoma, highlighting real-world effectiveness in heavily pre-treated cases. The study demonstrated measurable tumor response and manageable safety profiles, supporting the expanding role of immune checkpoint inhibitor combinations in rare and aggressive uterine cancers with limited treatment options

- In June 2024, U.S. FDA, a leading regulatory authority in oncology therapeutics, approved pembrolizumab (Keytruda) in combination with chemotherapy (carboplatin and paclitaxel) for primary advanced or recurrent endometrial carcinoma, which includes uterine carcinosarcoma patients under broader clinical practice guidelines. The approval was based on the KEYNOTE-868/NRG-GY018 Phase III trial demonstrating significant progression-free survival improvement across MMR subgroups, marking a major shift toward immunotherapy-based first-line treatment strategies in aggressive uterine cancers

- In June 2024, multiple international oncology associations highlighted expanded adoption of PD-1 inhibitor-based regimens in endometrial cancers following FDA approval updates. Clinical trial results from KEYNOTE-868 showed significant reduction in risk of disease progression or death, accelerating integration of immunotherapy into standard treatment pathways that also encompass uterine carcinosarcoma management due to overlapping treatment protocols in advanced uterine malignancies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.