Global Vaping Illness Market

Market Size in USD Billion

USD

45.74 Billion

USD

67.06 Billion

2025

2033

USD

45.74 Billion

USD

67.06 Billion

2025

2033

| 2026 - 2033 | |

| USD 45.74 Billion | |

| USD 67.06 Billion | |

| % | |

|

Vaping Illness Market Overview

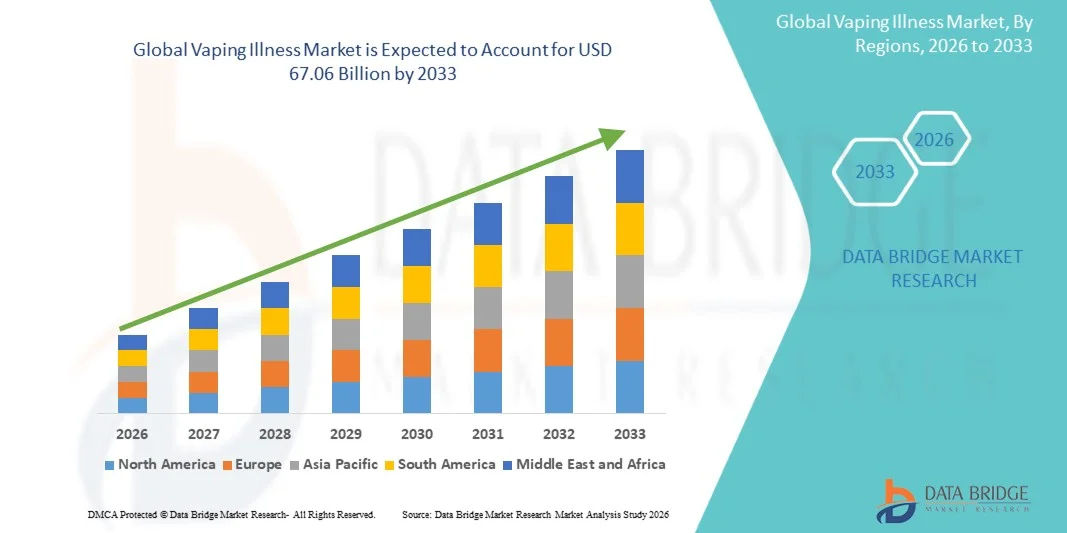

The global Vaping Illness market was valued at USD 45.74 billion in 2025 and is projected to reach USD 67.06 billion by 2033, growing at a CAGR of 4.90% from 2026 to 2033. The Global Vaping Illness market is experiencing steady growth driven by the rising incidence of e-cigarette or vaping-associated lung injuries (EVALI), increasing awareness of respiratory health risks linked to nicotine and THC vaping products, and expanding clinical focus on early diagnosis and respiratory care management. Growing usage of e-cigarettes among adolescents and young adults, combined with the long-term pulmonary complications associated with vaping-related chemical exposure, is further accelerating demand for diagnostic, emergency care, and long-term respiratory treatment solutions.

The increasing prevalence of vaping-related respiratory disorders, coupled with stricter government regulations on e-cigarette products, flavored vaping substances, and youth access restrictions, is compelling healthcare systems, regulatory authorities, and public health organizations to strengthen surveillance, screening, and treatment frameworks. Hospitals and emergency care centers are increasingly managing acute lung injury cases linked to vaping, while public health campaigns and policy interventions are focusing on prevention, awareness, and cessation support programs. This combination of rising clinical burden and regulatory action is shaping the global vaping illness treatment and management landscape.

Key Market Trends & Insights

- North America dominated the global Vaping Illness market with the largest revenue share of 36.28% in 2025, supported by advanced respiratory care infrastructure, high awareness of e-cigarette or vaping-associated lung injury (EVALI), and strong availability of critical care and emergency treatment facilities.

- The Corticosteroids segment led the market with a 44.62% share in 2025, driven by their widespread clinical use in reducing lung inflammation, managing acute respiratory distress, and improving recovery outcomes in severe vaping-related lung injury cases.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by increasing vaping adoption awareness, improving healthcare infrastructure, rising respiratory disease burden, and expanding diagnostic capabilities across China, India, and Japan.

- The Computed Tomography (CT) Scan segment is the fastest-growing diagnostic type, projected to register a CAGR of 7.1%, reflecting rising reliance on high-resolution imaging for early detection of vaping-related lung damage and pulmonary complications.

- The Shortness of Breath segment dominates the symptoms category with a 42.15% revenue share in 2025, driven by its high prevalence as the primary clinical presentation in vaping-induced respiratory distress cases.

- The Intravenous segment accounts for 57.88% of the market, preferred in hospital and emergency settings for rapid drug delivery in acute and severe vaping-related lung injury cases.

- The Hospital segment dominates the end-user category with a 48.93% revenue share in 2025, supported by high patient inflow for emergency respiratory care, availability of intensive care units, and advanced diagnostic imaging facilities.

- The Hospital Pharmacy segment is the fastest-growing distribution channel with a CAGR of 6.9%, driven by increasing inpatient treatments, critical care drug availability, and strict clinical supervision requirements for vaping illness management.

- The Injection segment dominated the market with a share of 63.18% in 2025, due to its rapid therapeutic action in emergency and critical care settings. Intravenous corticosteroids and supportive medications are widely administered in hospitalized EVALI patients.

Market Size & Forecast

- Global Market Value (2025): USD 45.74 Billion

- Expected Market Value (2033): USD 67.06 Billion

- Forecast CAGR (2026–2033): 4.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Global Vaping Illness Market Segmentation

|

Attributes |

Vaping Illness Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Johnson & Johnson (U.S.) |

|

Market Opportunities |

· Rising adoption of AI-driven respiratory diagnostics presents · Expansion of advanced imaging technologies such as CT scan, digital X-ray, and AI-assisted radiology platforms · Growing demand for targeted therapeutic development |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Vaping Illness Market Trends

Trend: Rising Incidence of EVALI Cases and Strengthening Public Health Surveillance

Healthcare providers are increasingly witnessing cases of EVALI, particularly among young adults and adolescents, driving stronger surveillance and early detection initiatives across hospitals and emergency care settings. According to the U.S. Centers for Disease Control and Prevention (CDC), thousands of hospitalizations related to vaping-associated lung injury were reported during the peak outbreak period in 2019–2021, highlighting the urgent need for improved diagnostic protocols. Hospitals are adopting standardized respiratory assessment pathways and toxic exposure screening tools to quickly identify vaping-related lung damage. In addition, rising awareness campaigns led by public health agencies are improving early symptom recognition such as shortness of breath, chest pain, and cough, enabling faster clinical intervention and reducing severe respiratory complications.

Global Vaping Illness Market Dynamics

Key Market Driver: Increasing Awareness and Advancements in Respiratory Diagnostics

The growing awareness of vaping-associated lung injury and improvements in respiratory diagnostic technologies are significantly driving market demand for early detection and treatment solutions. Advanced imaging techniques such as chest CT scans and digital X-rays are being widely used to identify lung inflammation patterns associated with EVALI, improving diagnostic accuracy in emergency departments. For instance, clinical reports from major U.S. hospitals indicate that early CT imaging has improved detection rates of vaping-related lung damage in acute respiratory cases. Pharmaceutical companies and healthcare providers are also investing in corticosteroid-based treatment protocols and supportive respiratory therapies to manage inflammation and improve patient recovery outcomes. Expanding public health monitoring systems and increased reporting of vaping-related respiratory complications are further strengthening market growth.

Key Restraint/Challenge: Diagnostic Complexity and Limited Long-Term Clinical Data

A major challenge in the EVALI market is the difficulty in diagnosing vaping-associated lung injury due to overlapping symptoms with other respiratory diseases such as pneumonia, influenza, and COVID-19. The absence of a single definitive biomarker often leads to delayed or misdiagnosis, impacting treatment outcomes. In addition, limited long-term clinical data on the progression and recurrence of EVALI restricts the development of standardized treatment guidelines. In many developing regions, lack of awareness among primary healthcare providers and limited access to advanced imaging systems further complicate early diagnosis. These factors collectively hinder consistent clinical management and slow down the adoption of specialized treatment pathways.

Key Market Opportunity: Expansion of AI-Based Respiratory Diagnostics and Toxicology Research

The increasing adoption of artificial intelligence in medical imaging and respiratory disease diagnostics presents a significant opportunity for the EVALI market. AI-enabled CT scan interpretation systems are improving the speed and accuracy of lung injury detection by identifying subtle inflammation patterns that may be missed in conventional imaging analysis. Research institutions in the U.S., Europe, and Asia-Pacific are actively developing predictive models to assess vaping-related lung damage progression and patient risk scoring. For instance, AI-assisted radiology tools deployed in large hospital networks are reducing diagnostic turnaround time in acute respiratory cases. Growing investment in toxicology research, combined with rising collaboration between healthcare technology companies and academic institutions, is expected to accelerate innovation in vaping-related lung injury detection and treatment strategies globally.

Global Vaping Illness Market Scope

The Vaping Illness market is segmented on the basis of Treatment, Diagnosis, Symptoms, Dosage, Route of Administration, End-Users, and Distribution Channel.

- By Treatment

On the basis of treatment, the global Vaping Illness market is segmented into antibiotics, antivirals, corticosteroids, and others. The Corticosteroids segment dominated the market with a share of 46.82% in 2025, owing to its strong clinical effectiveness in reducing lung inflammation and improving respiratory outcomes in severe EVALI cases. These therapies are widely used in hospital emergency departments and intensive care units for rapid symptom control. The Antibiotics segment is also widely adopted to manage secondary bacterial infections associated with vaping-related lung injury. The Antivirals segment is used in cases with suspected viral co-infections, particularly in immunocompromised patients. Increasing hospital adoption of combination therapy approaches is further strengthening treatment effectiveness. Rising awareness among pulmonologists and emergency physicians is supporting early therapeutic intervention. Corticosteroid-based protocols are increasingly standardized in clinical guidelines across developed healthcare systems. Growing availability of generic formulations is improving affordability and access in emerging markets. Expanding hospital formularies are further supporting treatment penetration. The Others segment includes supportive oxygen therapy and bronchodilators used in severe respiratory distress cases. Increasing clinical research is optimizing dosage strategies for improved outcomes. The Corticosteroids segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by rising adoption in acute care management and improved clinical response rates.

The Antivirals segment is expected to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing identification of viral co-infections in vaping-related lung injury cases. Rising diagnostic precision in hospital laboratories is enabling better differentiation between viral and chemical lung damage. Growing use of broad-spectrum antiviral therapies in emergency care settings is improving patient stabilization. Expanding hospital preparedness for mixed respiratory conditions is supporting adoption. Increasing research into viral inflammatory triggers linked to vaping exposure is strengthening clinical relevance. Pharmaceutical companies are developing targeted antiviral formulations for respiratory complications. Rising ICU admissions are increasing demand for supportive antiviral therapy. Improved awareness among pulmonologists is accelerating early prescription. Expanding healthcare infrastructure in Asia-Pacific is boosting accessibility. Integration of antiviral protocols into respiratory care guidelines is supporting standardized treatment. Growing clinical trials on combination therapy are further enhancing adoption. Increasing government funding for respiratory disease management is supporting market expansion.

- By Diagnosis

On the basis of diagnosis, the global Vaping Illness market is segmented into computed tomography (CT) scan, chest X-ray, and others. The Computed Tomography (CT) Scan segment dominated the market with a share of 52.14% in 2025, due to its high accuracy in detecting lung inflammation patterns and ground-glass opacities associated with EVALI. CT imaging is widely preferred in emergency and critical care settings for rapid diagnosis and treatment planning. The Chest X-Ray segment remains a first-line diagnostic tool due to its cost-effectiveness and wide availability in hospitals and clinics. Increasing use of radiology departments in emergency screening is supporting early disease detection. Advanced imaging protocols are improving differentiation between vaping-related lung injury and infectious respiratory diseases. The integration of AI-based imaging analysis is enhancing diagnostic precision and reducing interpretation time. Hospitals in the U.S. and Europe are increasingly deploying digital imaging systems for faster workflows. Rising investments in diagnostic infrastructure are improving access in emerging regions. Portable imaging systems are gaining traction in rural and remote healthcare facilities. The Others segment includes bronchoscopy and laboratory-based toxicology tests. Growing clinical dependence on CT imaging for severe respiratory cases is strengthening market adoption. The CT Scan segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by increasing demand for high-resolution lung imaging.

The Chest X-Ray segment is expected to witness the fastest CAGR of 6.7% from 2026 to 2033, driven by its cost-effectiveness and widespread availability across primary healthcare centers. Increasing use of portable X-ray devices in emergency and rural settings is improving early diagnosis rates. Rising patient inflow in outpatient departments is supporting high adoption. Growing government initiatives to strengthen basic diagnostic infrastructure in developing countries is boosting demand. Integration of digital radiography systems is improving image clarity and diagnostic accuracy. Increasing awareness among general physicians is accelerating early screening adoption. Expanding emergency care facilities is supporting rapid imaging requirements. Chest X-ray remains the first-line diagnostic tool in suspected respiratory toxicity cases. Rising insurance coverage for basic imaging procedures is improving accessibility. Continuous technological upgrades in imaging equipment are enhancing efficiency. Expanding healthcare access in Asia-Pacific is driving strong adoption.

- By Symptoms

On the basis of symptoms, the global Vaping Illness market is segmented into shortness of breath, cough, fever and chills, diarrhea, vomiting, headache, rapid heartbeat, dizziness, chest pain, and others. The Shortness of Breath segment dominated the market with a share of 38.27% in 2025, as it is the most commonly reported and clinically significant symptom of EVALI patients. This symptom frequently leads to emergency hospital admissions and immediate respiratory evaluation. Cough and chest pain are also widely reported in moderate to severe cases, contributing to early clinical suspicion. Fever and chills are often associated with inflammatory response and secondary infections. Gastrointestinal symptoms such as diarrhea and vomiting are increasingly recognized in clinical studies. Neurological symptoms like headache and dizziness are observed in severe toxicity cases. Rapid heartbeat is commonly linked with hypoxia and respiratory distress. Hospitals are implementing symptom-based triage systems for faster diagnosis. Increasing public awareness of vaping-related risks is improving early reporting of symptoms. Emergency departments are using standardized respiratory screening protocols. The Others segment includes fatigue and generalized weakness. The Shortness of Breath segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by rising incidence of acute respiratory complications linked to vaping exposure.

The Chest Pain segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing recognition of cardiovascular and pleuritic complications associated with vaping-related lung injury. Growing emergency admissions with overlapping cardiac and respiratory symptoms are boosting clinical attention. Improved diagnostic differentiation between cardiac and pulmonary causes is enhancing reporting accuracy. Rising awareness among patients is leading to earlier hospital visits. Increasing use of ECG and imaging co-evaluation is improving detection rates. Expansion of emergency cardiac care units is supporting faster intervention. Clinical studies linking vaping exposure to chest discomfort are increasing awareness. Growing adolescent and young adult patient populations are driving symptom reporting. Hospitals are adopting integrated cardiopulmonary evaluation protocols. Rising healthcare literacy is improving early symptom recognition. Expanding emergency healthcare infrastructure is supporting rapid diagnosis. Increasing research on vaping-induced inflammatory pain responses is strengthening market growth.

- By Dosage

On the basis of dosage, the global Vaping Illness market is segmented into injection, tablets, and others. The Injection segment dominated the market with a share of 63.18% in 2025, due to its rapid therapeutic action in emergency and critical care settings. Intravenous corticosteroids and supportive medications are widely administered in hospitalized EVALI patients. Tablets are primarily used in mild and recovering cases for continued outpatient treatment. Injectable formulations ensure faster drug bioavailability in severe respiratory distress conditions. Hospitals are increasingly adopting standardized injection-based treatment protocols. Emergency departments rely on injectable therapies for immediate symptom control. Rising ICU admissions for vaping-related lung injury are supporting injectable drug demand. Pharmaceutical companies are expanding parenteral drug production capacities. Improved hospital infrastructure is enabling wider adoption of intravenous therapies. The Others segment includes nebulized therapies used for respiratory support. Clinical guidelines increasingly recommend injection-based corticosteroid therapy for severe cases. The Injection segment is expected to witness the fastest CAGR of 7.0% from 2026 to 2033, driven by rising acute care treatment demand.

The Tablets segment is expected to witness the fastest CAGR of 6.6% from 2026 to 2033, driven by increasing preference for outpatient and home-based treatment management. Rising healthcare cost optimization is encouraging oral therapy adoption in mild cases. Expanding availability of prescription medications in retail and online pharmacies is improving access. Growing patient preference for non-invasive treatment options is supporting demand. Increasing follow-up care after hospital discharge is boosting oral medication use. Improved awareness of long-term respiratory recovery protocols is strengthening adherence. Expanding telemedicine services are supporting prescription-based oral therapies. Pharmaceutical companies are developing extended-release formulations for better compliance. Rising healthcare accessibility in emerging economies is driving adoption. Growing physician preference for step-down therapy after IV treatment is supporting transition to tablets. Increasing insurance coverage for outpatient drugs is improving affordability.

- By Route of Administration

On the basis of route of administration, the global Vaping Illness market is segmented into oral, intravenous, and others. The Intravenous segment dominated the market with a share of 58.91% in 2025, owing to its rapid onset of action and high effectiveness in managing acute respiratory inflammation. IV corticosteroids are widely used in hospital and ICU settings for severe EVALI cases. The Oral segment is commonly used for mild and moderate cases requiring outpatient treatment and follow-up care. Intravenous therapy ensures controlled drug delivery and improved clinical outcomes in emergency conditions. Increasing hospitalization rates are driving demand for IV drug administration. Hospitals are standardizing IV treatment protocols for respiratory toxicity cases. Rising ICU infrastructure investments are supporting IV therapy adoption. Oral therapies are widely used in step-down care after stabilization. The Others segment includes inhalation-based supportive therapies. Clinical preference for IV administration in critical cases is strengthening market dominance. Increasing healthcare awareness is improving early intervention rates. The Intravenous segment is expected to witness the fastest CAGR of 7.3% from 2026 to 2033, driven by rising severity of respiratory complications.

The Oral segment is expected to witness the fastest CAGR of 6.5% from 2026 to 2033, driven by increasing shift toward outpatient care management and long-term recovery therapies. Rising preference for patient-friendly medication administration is supporting oral drug adoption. Expanding pharmacy distribution networks are improving drug accessibility. Growing healthcare awareness in emerging economies is boosting early-stage treatment. Increasing use of step-down therapy after hospitalization is strengthening demand. Improved adherence to oral corticosteroid regimens is enhancing outcomes. Expanding telehealth consultations are supporting prescription of oral medications. Pharmaceutical innovation in oral formulations is improving bioavailability. Rising healthcare cost pressure is encouraging home-based care. Increasing physician preference for non-invasive treatment options is supporting adoption. Expanding insurance coverage for oral drugs is improving affordability. Growing focus on chronic respiratory management is strengthening market penetration.

- By End-Users

On the basis of end-users, the global Vaping Illness market is segmented into clinic, hospital, and others. The Hospital segment dominated the market with a share of 66.42% in 2025, due to high patient admissions for severe respiratory complications requiring emergency and ICU care. Hospitals are equipped with advanced imaging, respiratory support systems, and critical care infrastructure essential for EVALI treatment. Clinics are primarily involved in early diagnosis and mild case management. Increasing referrals from primary care centers are driving hospital admissions. Specialized pulmonary care units are improving treatment outcomes. Hospitals are integrating AI-based diagnostic systems for faster decision-making. Rising healthcare expenditure is supporting hospital infrastructure expansion. Emergency departments play a key role in initial patient stabilization. The Others segment includes outpatient care centers and telemedicine services. Growing awareness is improving early detection and hospital referrals. Strong hospital networks in developed countries are enhancing treatment access. The Hospital segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by increasing severity of respiratory cases.

The Clinic segment is expected to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by rising preference for early diagnosis and outpatient respiratory care. Increasing accessibility of diagnostic tools in primary care centers is improving early detection rates. Growing awareness among general physicians is supporting timely identification of symptoms. Expanding outpatient healthcare infrastructure in emerging markets is boosting clinic-based treatment. Rising adoption of telemedicine and digital consultations is improving accessibility. Clinics are increasingly acting as first-line screening centers for respiratory toxicity. Improved referral systems are strengthening hospital connectivity. Growing focus on cost-effective care is driving outpatient management. Increasing government support for primary healthcare is enhancing capacity. Expanding insurance coverage for outpatient consultations is improving affordability. Rising patient preference for non-hospital care is supporting clinic growth.

- By Distribution Channel

On the basis of distribution channel, the global Vaping Illness market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market with a share of 57.63% in 2025, due to direct drug dispensing for inpatient and emergency treatments. Hospital pharmacies ensure immediate availability of corticosteroids, antibiotics, and supportive respiratory medications. Retail pharmacies are widely used for outpatient prescription fulfillment and follow-up therapies. Online pharmacies are gaining traction due to increasing digital healthcare adoption. Hospitals maintain strict drug inventory systems for critical care medications. Rising hospitalization rates for EVALI are strengthening hospital pharmacy demand. Integration of electronic prescription systems is improving efficiency. Retail pharmacies support long-term medication adherence after discharge. Regulatory frameworks ensure controlled dispensing of respiratory drugs. The Others segment includes specialty pharmacy services for chronic respiratory care. Increasing digitalization is supporting online pharmacy growth in developed regions. The Hospital Pharmacy segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by rising inpatient treatment demand.

The Online Pharmacy segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by rapid digital healthcare adoption and increasing preference for home delivery of prescription medications. Growing penetration of e-pharmacy platforms is improving drug accessibility in urban and semi-urban regions. Rising telemedicine consultations are directly boosting online prescription fulfillment. Expanding smartphone usage is enabling easier access to digital pharmacy services. Increasing convenience of doorstep delivery is supporting patient adoption. Regulatory support for online drug distribution is strengthening market expansion. Integration of digital payment systems is improving transaction efficiency. Growing awareness of digital health ecosystems is accelerating adoption. Expanding logistics networks are improving delivery timelines. Rising chronic respiratory follow-up treatments are boosting repeat orders. Increasing investment by pharmacy tech startups is enhancing platform capabilities. Continuous innovation in digital healthcare infrastructure is supporting long-term growth.

Global Vaping Illness Market Regional Analysis

North America dominated the Vaping Illness market with the largest revenue share of 36.28% in 2025, supported by advanced respiratory care infrastructure, strong public health surveillance systems, and high incidence of e-cigarette or vaping-associated lung injury (EVALI) cases during peak outbreak years. The region benefits from well-established emergency care networks, widespread availability of advanced diagnostic tools such as CT scans and chest X-rays, and structured clinical treatment protocols for acute respiratory failure. Increasing awareness campaigns by health authorities and continuous monitoring of vaping-related respiratory conditions further strengthen North America’s leadership in the global market.

U.S. Vaping Illness Market Insight

The U.S. Vaping Illness market is witnessing strong growth due to rising incidence of EVALI cases, particularly among adolescents and young adults, and increasing adoption of standardized respiratory diagnostic and toxicology screening protocols in hospitals. The country’s advanced healthcare infrastructure, strong deployment of emergency surveillance systems by the CDC, and growing use of corticosteroid-based treatment approaches are driving market expansion. In addition, public health awareness campaigns focusing on symptoms such as shortness of breath, chest pain, and cough are improving early diagnosis and clinical intervention rates across healthcare facilities.

Europe Vaping Illness Market Insight

The Europe Vaping Illness market remains a major contributor to global revenue, driven by strengthening respiratory disease surveillance systems, rising awareness of vaping-associated lung injuries, and growing adoption of advanced diagnostic imaging technologies. Hospitals and emergency care centers across the region are increasingly using CT scans and chest X-rays for rapid identification of lung inflammation patterns. Furthermore, expanding public health initiatives and regulatory frameworks aimed at controlling vaping product safety are supporting early detection and improving patient outcomes.

U.K. Vaping Illness Market Insight

The U.K. Vaping Illness market is experiencing steady growth, supported by increasing awareness of vaping-related respiratory risks and strong reliance on NHS emergency care systems for acute lung injury management. Hospitals are adopting standardized clinical pathways for diagnosing suspected EVALI cases, including imaging-based assessment and corticosteroid treatment protocols. In addition, rising public health campaigns and tobacco control initiatives are improving early symptom recognition and encouraging timely medical consultation.

Germany Vaping Illness Market Insight

The Germany Vaping Illness market is expanding steadily due to strong healthcare infrastructure, high diagnostic accuracy in respiratory disease management, and increasing use of advanced imaging technologies in hospital settings. Medical institutions are leveraging CT scans and X-ray diagnostics to differentiate vaping-associated lung injury from other respiratory conditions. Moreover, growing clinical research activity and improved emergency care readiness are enhancing early detection and treatment effectiveness across the country.

Asia-Pacific Vaping Illness Market Insight

The Asia-Pacific Vaping Illness market is expected to witness rapid growth, driven by increasing awareness of vaping-related health risks, rising respiratory disease burden, and improving healthcare infrastructure across China, India, and Japan. Expanding access to diagnostic imaging, growing hospital capacity, and strengthening public health surveillance systems are supporting regional market expansion. In addition, rising government initiatives focused on respiratory health awareness are improving early detection and treatment adoption.

Japan Vaping Illness Market Insight

The Japan Vaping Illness market is witnessing consistent growth due to advanced healthcare infrastructure, strong diagnostic capabilities, and increasing emphasis on early detection of respiratory conditions. Hospitals are increasingly utilizing CT imaging and structured clinical evaluation protocols to identify vaping-associated lung injury. Moreover, high awareness of respiratory health risks and strong preventive healthcare systems are supporting stable market development.

China Vaping Illness Market Insight

The China Vaping Illness market is growing rapidly, driven by increasing respiratory health awareness, expanding hospital infrastructure, and rising adoption of advanced diagnostic technologies such as CT scans and digital X-rays. Strengthening public health surveillance systems and improving access to emergency respiratory care are further supporting early diagnosis and treatment. In addition, growing government focus on respiratory disease management and healthcare modernization is positioning China as one of the fastest-growing markets for Vaping Illness globally.

Global Vaping Illness Market Share

The Vaping Illness industry is primarily led by well-established companies, including:

- Johnson & Johnson (U.S.)

- Pfizer Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Novartis AG (Switzerland)

- Sanofi S.A. (France)

- AstraZeneca plc (U.K.)

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Boehringer Ingelheim (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- BD (Becton, Dickinson and Company) (U.S.)

- Abbott Laboratories (U.S.)

- Hologic, Inc. (U.S.)

- Fresenius Medical Care (Germany)

- GE HealthCare Technologies Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Roche Holding AG (Switzerland)

- Danaher Corporation (U.S.)

- 3M Health Care (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Cipla Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Aurobindo Pharma Ltd. (India)

- Boston Scientific Corporation (U.S.)

- Medtronic plc (Ireland)

- ResMed Inc. (U.S.)

- Philips Healthcare (Netherlands)

- Cook Medical (U.S.)

- Olympus Corporation (Japan)

- Stryker Corporation (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Eli Lilly and Company (U.S.)

- Biogen Inc. (U.S.)

Latest Developments in Global Vaping Illness Market

- In February 2021, the U.S. Centers for Disease Control and Prevention (CDC) reaffirmed its updated surveillance findings on e-cigarette or vaping product use-associated lung injury (EVALI), confirming that vitamin E acetate remained strongly linked to the 2019–2020 outbreak. The update highlighted ongoing clinical monitoring of hospitalized patients and emphasized that THC-containing products were the primary drivers of severe lung injury cases, strengthening regulatory focus on illicit vaping product contamination and safety enforcement in the U.S.

- In August 2021, CDC health communications continued post-outbreak guidance for clinicians, reinforcing standardized treatment protocols for vaping-related lung injury, including corticosteroid use and respiratory support in severe cases. The guidance also stressed early identification of symptoms such as shortness of breath, chest pain, and cough to reduce progression to respiratory failure and intensive care admission

- In February 2024, the CDC officially updated its emergency response documentation on EVALI, noting that while the major outbreak peaked in 2019–2020, syndromic surveillance systems were still being used to monitor new vaping-associated respiratory illness patterns across U.S. emergency departments. This update reinforced long-term surveillance infrastructure for detecting emerging respiratory hazards linked to vaping product use

- In May 2024, a peer-reviewed clinical analysis published in pulmonology research reports indicated that hospitalizations related to e-cigarette or vaping-associated lung injury (EVALI) remained clinically significant even after the formal CDC outbreak reporting phase ended. The study highlighted continued cases requiring oxygen therapy and intensive care, suggesting lingering public health burden despite reduced national outbreak levels

- In April 2024, pediatric respiratory medicine studies documented ongoing diagnostic evolution of vaping-associated lung injury, showing that imaging technologies such as CT scans and chest radiographs remain critical tools for identifying vaping-induced lung damage in adolescents and young adults. The study reinforced the persistence of vaping-related respiratory complications in clinical settings beyond the initial outbreak period

- In July 2025, medical journal analyses of public health communication trends reported that EVALI remains a reference case for vaping-related harm awareness campaigns, with sustained increases in public search behavior and health system education initiatives even years after the outbreak peak. The research emphasized that media coverage played a major role in shaping public awareness and vaping cessation behavior globally

- In January 2026, CDC-linked surveillance publications reiterated that e-cigarette or vaping-associated lung injury continues to be monitored through syndromic emergency data systems, highlighting that although the outbreak is no longer expanding, health authorities maintain active preparedness systems for detecting new vaping-related respiratory injury clusters in real time

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.