Global Vascular Stent Market

Market Size in USD Billion

CAGR :

%

USD

9.94 Billion

USD

18.14 Billion

2025

2033

USD

9.94 Billion

USD

18.14 Billion

2025

2033

| 2026 –2033 | |

| USD 9.94 Billion | |

| USD 18.14 Billion | |

| % | |

|

Vascular Stent Market Size

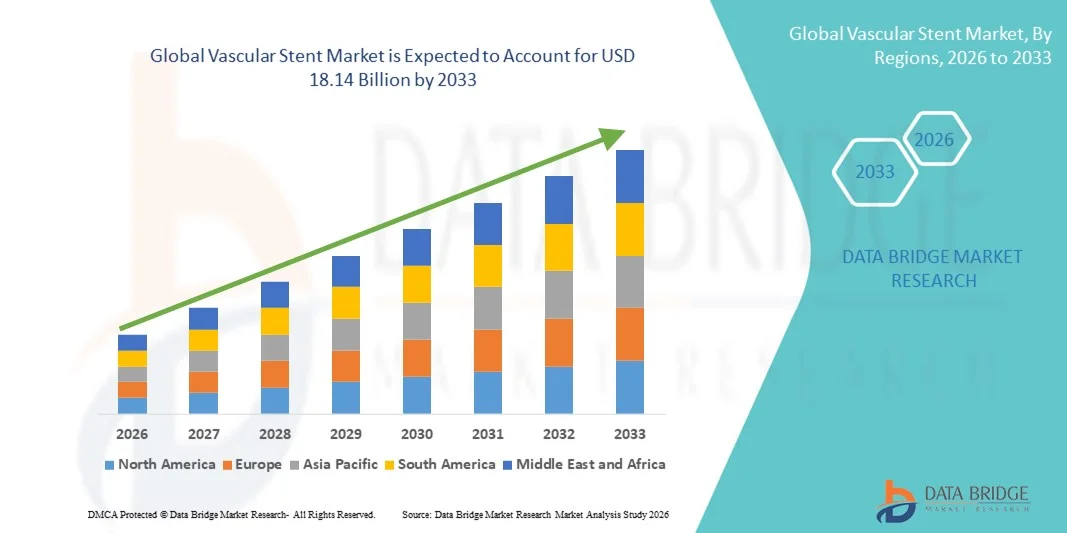

- The global vascular stent market size was valued at USD 9.94 billion in 2025 and is expected to reach USD 18.14 billion by 2033, at a CAGR of 7.81% during the forecast period

- The market growth is largely fueled by the rising prevalence of cardiovascular diseases, increasing incidence of coronary artery disorders, and continuous technological advancements in minimally invasive interventional procedures across healthcare systems worldwide

- Furthermore, growing preference for drug-eluting and bioresorbable stents, expanding geriatric population, and improving access to advanced cardiac care in emerging economies are establishing vascular stents as a critical solution in modern cardiovascular treatment. These converging factors are accelerating the adoption of vascular stent technologies, thereby significantly boosting the industry's growth

Vascular Stent Market Analysis

- Vascular stents, small mesh-like tubular devices implanted within narrowed or blocked blood vessels to restore and maintain blood flow, are increasingly vital components of modern interventional cardiology and peripheral vascular procedures in both hospital and ambulatory surgical center settings due to their effectiveness in minimally invasive treatment and improved patient recovery outcomes

- The escalating demand for vascular stents is primarily fueled by the rising prevalence of cardiovascular diseases, increasing incidence of coronary artery disease and peripheral artery disease, and growing preference for minimally invasive procedures over traditional open surgeries

- North America dominated the vascular stent market with the largest revenue share of 38.64% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative drug-eluting stents, and a strong presence of leading medical device manufacturers, with the U.S. witnessing substantial growth in interventional procedures driven by favorable reimbursement frameworks and continuous technological advancements

- Asia-Pacific is expected to be the fastest growing region in the vascular stent market during the forecast period due to expanding healthcare infrastructure, increasing healthcare expenditure, growing patient awareness, and a rapidly aging population susceptible to cardiovascular disorders

- Drug-eluting stent segment dominated the vascular stent market with a market share of 71.25% in 2025, driven by its superior efficacy in reducing restenosis rates, improved long-term clinical outcomes, and widespread clinical preference over bare-metal stents

Report Scope and Vascular Stent Market Segmentation

|

Attributes |

Vascular Stent Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Vascular Stent Market Trends

Advancements in Drug-Eluting and Bioresorbable Technologies

- A significant and accelerating trend in the global vascular stent market is the continuous innovation in drug-eluting stents (DES) and bioresorbable scaffold technologies. This fusion of advanced biomaterials and controlled drug delivery systems is significantly enhancing patient outcomes and long-term vessel patency

- For instance, next-generation drug-eluting stents developed by leading manufacturers incorporate improved polymer coatings and thinner strut designs, allowing enhanced flexibility and reduced risk of restenosis. Similarly, bioresorbable stents are engineered to gradually dissolve after restoring blood flow, offering temporary scaffolding without leaving permanent implants

- Technological integration in vascular stents enables features such as targeted drug release to prevent neointimal hyperplasia and improved biocompatibility to minimize inflammatory response. For instance, certain contemporary DES platforms utilize advanced antiproliferative agents to reduce repeat revascularization rates and can support complex lesion treatment. Furthermore, improved catheter delivery systems offer physicians greater precision and ease of deployment during minimally invasive procedures

- The seamless integration of imaging compatibility and enhanced stent architecture facilitates optimized procedural outcomes across diverse patient populations. Through advanced interventional platforms, clinicians can manage coronary and peripheral artery diseases more effectively, creating a more streamlined and outcome-focused treatment approach

- This trend towards more efficient, durable, and patient-centric stent technologies is fundamentally reshaping clinical expectations in interventional cardiology. Consequently, companies such as Abbott and Boston Scientific are developing next-generation DES platforms with improved safety profiles, enhanced radial strength, and optimized healing responses

- The demand for vascular stents offering superior efficacy, long-term safety, and compatibility with minimally invasive procedures is growing rapidly across both developed and emerging healthcare markets, as providers increasingly prioritize improved clinical outcomes and cost-effective cardiovascular care

- The integration of advanced imaging modalities such as intravascular ultrasound (IVUS) and optical coherence tomography (OCT) with stent deployment procedures is improving precision-based treatment planning and procedural success rates

Vascular Stent Market Dynamics

Driver

Growing Cardiovascular Disease Burden and Preference for Minimally Invasive Procedures

- The increasing prevalence of cardiovascular diseases among aging populations, coupled with the growing preference for minimally invasive interventional procedures, is a significant driver for the heightened demand for vascular stents

- For instance, in recent years, major medical device manufacturers have announced expanded production capacities and next-generation DES launches to address rising volumes of percutaneous coronary interventions worldwide. Such strategies by key companies are expected to drive the vascular stent industry growth in the forecast period

- As patients and healthcare providers seek faster recovery times and reduced hospital stays, vascular stents offer effective revascularization with lower procedural risks compared to traditional open-heart surgeries, providing a compelling alternative in cardiac care

- Furthermore, the expanding availability of catheterization laboratories and skilled interventional cardiologists in emerging economies is making vascular stent procedures more accessible, supporting broader adoption across diverse healthcare settings

- The clinical advantages of reduced restenosis rates, improved survival outcomes, and shorter rehabilitation periods are key factors propelling the adoption of vascular stents in both coronary and peripheral artery disease management. The growing inclusion of advanced stents in reimbursement frameworks further contributes to market growth

- Rising healthcare expenditure and government initiatives aimed at strengthening cardiovascular disease management programs are further accelerating procedural volumes across both public and private healthcare institutions

- Continuous technological collaboration between medical device manufacturers and research institutions is enhancing product innovation pipelines, supporting sustained demand for next-generation vascular stent platforms

Restraint/Challenge

Risk of Stent Thrombosis and Stringent Regulatory Requirements

- Concerns surrounding potential complications such as stent thrombosis, in-stent restenosis, and long-term adverse events pose a significant challenge to broader market expansion. As vascular stents are implantable medical devices, they require rigorous clinical validation and post-market surveillance, raising safety and efficacy considerations among regulators and clinicians

- For instance, stringent approval processes by regulatory authorities for new-generation stents have led to extended clinical trial timelines, delaying product commercialization in certain regions

- Addressing these safety concerns through enhanced biocompatible materials, optimized drug coatings, and robust clinical data is crucial for building physician and patient confidence. Companies emphasize long-term outcome studies and real-world evidence to support adoption. In addition, the relatively high cost of advanced drug-eluting and bioresorbable stents compared to bare-metal alternatives can be a barrier for healthcare systems with constrained budgets, particularly in low- and middle-income countries

- While technological advancements continue to improve safety profiles, the cost burden and regulatory complexity can still hinder widespread penetration, especially in price-sensitive healthcare markets

- Overcoming these challenges through continued clinical innovation, streamlined regulatory pathways, and cost-effective manufacturing strategies will be vital for sustained market growth

- Limited awareness and delayed diagnosis of peripheral artery disease in certain developing regions may restrict timely intervention and reduce procedural volumes

- Supply chain disruptions affecting raw materials such as cobalt-chromium and specialized polymers can impact production timelines and pricing stability in the vascular stent industry

Vascular Stent Market Scope

The market is segmented on the basis of type, product, mode of delivery, materials, and end user.

- By Type

On the basis of type, the global vascular stent market is segmented into drug-eluting stents, bare-metal stents, and bio absorbable stents. The Drug-Eluting Stents (DES) segment dominated the market with the largest revenue share of 71.25% in 2025, driven by its superior clinical efficacy in reducing restenosis rates compared to bare-metal alternatives. DES release antiproliferative drugs that prevent excessive tissue growth within arteries, significantly lowering the risk of repeat revascularization procedures. Their widespread adoption in percutaneous coronary interventions across developed healthcare systems has reinforced their leading position. In addition, continuous advancements in polymer coatings and thinner strut technologies have improved safety profiles and patient outcomes. Favorable reimbursement policies in major markets further support segment dominance. Strong physician preference and robust clinical data validating long-term effectiveness continue to strengthen the demand for drug-eluting stents globally.

The Bio absorbable Stents segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing focus on temporary scaffolding solutions that naturally dissolve after restoring vessel patency. These stents reduce long-term complications associated with permanent metallic implants and support natural vessel healing. Growing research investments and next-generation bioresorbable scaffold innovations are improving structural integrity and safety outcomes. Rising demand for advanced cardiovascular therapies among younger patient populations is further accelerating adoption. Regulatory approvals for improved bio absorbable platforms are expanding market penetration. As healthcare providers emphasize long-term patient-centric outcomes, this segment is expected to gain significant momentum during the forecast period.

- By Product

On the basis of product, the vascular stent market is segmented into coronary stents, peripheral stents, and EVAR stent grafts. The Coronary Stents segment dominated the market in 2025, primarily due to the high global prevalence of coronary artery disease and increasing volumes of percutaneous coronary interventions. Coronary stents are widely utilized in hospital catheterization laboratories for restoring blood flow in blocked coronary arteries. Technological advancements in drug-eluting coronary platforms have enhanced procedural success and reduced complication rates. The rising geriatric population, which is more susceptible to cardiac disorders, further supports demand. Established clinical guidelines recommending stent placement for specific cardiac conditions reinforce their extensive usage. Strong reimbursement frameworks in developed regions also contribute to segment dominance.

The EVAR Stent Grafts segment is expected to register the fastest growth during the forecast period, driven by the increasing incidence of abdominal aortic aneurysms and preference for minimally invasive endovascular aneurysm repair procedures. EVAR stent grafts offer reduced hospital stays and lower perioperative risks compared to open surgical repair. Continuous improvements in graft design and delivery systems are enhancing procedural precision. Expanding awareness and early diagnosis of aortic aneurysms are contributing to procedural growth. Growing adoption in emerging economies with improving vascular surgery infrastructure further supports expansion. The shift toward less invasive vascular repair solutions positions EVAR stent grafts as a rapidly expanding segment.

- By Mode of Delivery

On the basis of mode of delivery, the market is segmented into balloon-expandable stents and self-expanding stents. The Balloon-Expandable Stents segment dominated the market in 2025, owing to their high radial strength and precise placement capabilities during coronary interventions. These stents allow accurate deployment in calcified or rigid lesions, making them particularly suitable for coronary artery treatments. Their compatibility with drug-eluting technologies further enhances therapeutic effectiveness. Physicians prefer balloon-expandable systems for their predictable expansion characteristics. Technological refinements in catheter design and imaging guidance have improved procedural success rates. Extensive usage in percutaneous coronary interventions supports segment leadership.

The Self-Expanding Stents segment is projected to witness the fastest growth rate from 2026 to 2033, driven by increasing application in peripheral artery disease treatments. These stents automatically expand upon deployment, adapting well to dynamic vascular environments such as the femoral and carotid arteries. Their flexibility and fracture resistance make them suitable for tortuous vessels. Growing diagnosis of peripheral vascular disorders is fueling demand. Advancements in nitinol-based materials are enhancing durability and long-term outcomes. Expanding interventional radiology procedures globally further accelerate segment growth.

- By Materials

On the basis of materials, the vascular stent market is segmented into metallic stents and other stents. The Metallic Stents segment dominated the market in 2025, supported by their established clinical reliability and structural strength. Materials such as stainless steel, cobalt-chromium, and nitinol provide durability and optimal radial force. Metallic stents are widely used in both coronary and peripheral interventions due to their proven safety profile. Continuous innovation in alloy composition has improved flexibility and reduced strut thickness. Strong physician familiarity and long-term outcome data further reinforce their leading market position. Cost-effectiveness compared to certain advanced alternatives also contributes to dominance.

The Other Stents segment, which includes bioresorbable and polymer-based platforms, is expected to grow at the fastest pace during the forecast period. Increasing research into biodegradable materials is enhancing next-generation stent performance. These materials aim to reduce long-term inflammatory risks and eliminate permanent implants. Rising preference for innovative treatment options among healthcare providers is driving adoption. Clinical trials demonstrating improved healing responses are expanding acceptance. As technological advancements address earlier performance limitations, this segment is projected to gain substantial traction.

- By End User

On the basis of end user, the market is segmented into hospitals and cardiac centres, ambulatory surgical centres, and others. The Hospitals and Cardiac Centres segment dominated the market in 2025, attributed to the high volume of complex cardiovascular procedures performed in these facilities. Hospitals are equipped with advanced catheterization laboratories and specialized interventional cardiology teams. Availability of comprehensive post-procedural care and emergency support further strengthens their leadership. Increasing patient inflow for coronary and peripheral interventions supports consistent demand. Strong reimbursement structures in hospital settings also enhance procedural volumes. Continuous investments in advanced imaging and surgical infrastructure reinforce segment dominance.

The Ambulatory Surgical Centres segment is expected to witness the fastest growth during the forecast period, driven by the rising shift toward outpatient minimally invasive procedures. These centers offer cost-effective treatment alternatives with shorter hospital stays. Technological advancements enabling safer and quicker interventions are supporting the migration of select vascular procedures to ambulatory settings. Growing patient preference for convenient and efficient healthcare services further fuels expansion. Improved insurance coverage for outpatient cardiovascular interventions is accelerating adoption. As healthcare systems focus on cost optimization, ambulatory surgical centres are emerging as a rapidly expanding end-user segment.

Vascular Stent Market Regional Analysis

- North America dominated the vascular stent market with the largest revenue share of 38.64% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative drug-eluting stents, and a strong presence of leading medical device manufacturers

- Patients and healthcare providers in the region highly value the clinical efficacy, reduced restenosis rates, and improved recovery outcomes offered by drug-eluting and next-generation vascular stents across coronary and peripheral interventions

- This widespread adoption is further supported by favorable reimbursement frameworks, presence of leading medical device manufacturers, a well-established network of catheterization laboratories, and increasing awareness regarding early diagnosis and treatment of cardiovascular conditions, establishing vascular stents as a primary solution in modern cardiac care

U.S. Vascular Stent Market Insight

The U.S. vascular stent market captured the largest revenue share within North America in 2025, fueled by the high prevalence of coronary artery disease and the strong adoption of minimally invasive interventional cardiology procedures. Healthcare providers are increasingly prioritizing advanced drug-eluting and next-generation stent technologies to improve long-term patient outcomes. The growing aging population, combined with lifestyle-related cardiovascular risk factors, further propels the vascular stent industry. Moreover, the presence of leading medical device manufacturers and favorable reimbursement frameworks is significantly contributing to the market's expansion.

Europe Vascular Stent Market Insight

The Europe vascular stent market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the increasing burden of cardiovascular diseases and well-established public healthcare systems. The rise in early diagnosis initiatives, coupled with demand for minimally invasive procedures, is fostering the adoption of vascular stents. European healthcare providers are also focused on clinical efficacy and long-term safety outcomes. The region is experiencing significant growth across coronary and peripheral interventions, with advanced stent platforms being incorporated into both tertiary hospitals and specialized cardiac centers.

U.K. Vascular Stent Market Insight

The U.K. vascular stent market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing incidences of heart disease and strong emphasis on early interventional treatment. In addition, rising awareness regarding preventive cardiac care is encouraging both patients and clinicians to opt for minimally invasive stent procedures. The country’s structured reimbursement system and expanding catheterization laboratory infrastructure are expected to continue to stimulate market growth.

Germany Vascular Stent Market Insight

The Germany vascular stent market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing adoption of technologically advanced interventional devices and strong clinical research capabilities. Germany’s well-developed healthcare infrastructure, combined with its emphasis on medical innovation and quality standards, promotes the adoption of next-generation drug-eluting and bioresorbable stents. The integration of advanced imaging technologies with stent deployment procedures is also becoming increasingly prevalent, aligning with the country’s focus on precision-based cardiovascular care.

Asia-Pacific Vascular Stent Market Insight

The Asia-Pacific vascular stent market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising cardiovascular disease prevalence, increasing healthcare expenditure, and rapid healthcare infrastructure development in countries such as China, Japan, and India. The region's growing awareness regarding early cardiac intervention, supported by government healthcare initiatives, is driving the adoption of vascular stents. Furthermore, as APAC emerges as a major manufacturing hub for medical devices, the affordability and accessibility of vascular stent technologies are expanding to a broader patient population.

Japan Vascular Stent Market Insight

The Japan vascular stent market is gaining momentum due to the country’s aging population, advanced healthcare systems, and high demand for minimally invasive treatments. The Japanese market places a significant emphasis on precision and clinical safety, and the adoption of vascular stents is driven by increasing volumes of coronary interventions. The integration of advanced imaging and catheter-based technologies with stent procedures is fueling growth. Moreover, Japan's growing focus on managing age-related cardiovascular disorders is likely to spur demand for effective and long-term vascular treatment solutions in both public and private healthcare sectors.

India Vascular Stent Market Insight

The India vascular stent market accounted for a significant revenue share in Asia Pacific in 2025, attributed to the country's rising cardiovascular disease burden, expanding healthcare infrastructure, and increasing access to interventional cardiology services. India stands as one of the fastest-growing markets for coronary and peripheral stent procedures, with growing adoption across urban and semi-urban hospitals. The push toward strengthening cardiac care facilities and the availability of cost-effective stent options, alongside supportive regulatory reforms, are key factors propelling the market in India.

Vascular Stent Market Share

The Vascular Stent industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Cook (U.S.)

- MicroPort Scientific Corporation (China)

- B. Braun SE (Germany)

- Cardinal Health (U.S.)

- BD (U.S.)

- Biosensors International Group, Ltd. (Singapore)

- Meril Life Sciences Pvt. Ltd. (India)

- Elixir Medical Corporation (U.S.)

- Endologix LLC (U.S.)

- Lepu Medical Technology Co., Ltd. (China)

- Translumina GmbH (Germany)

- iVascular, S.L.U. (Spain)

- Otsuka Medical Devices Co., Ltd. (Japan)

- Purple MicroPort Cardiovascular Pvt. Ltd. (India)

- Sahajanand Medical Technologies Limited (India)

- Vascular Concepts Limited (India)

- Balton Sp. z o.o. (Poland)

What are the Recent Developments in Global Vascular Stent Market?

- In January 2026, Gore & Associates’ Viabahn Fortegra Venous Stent won FDA approval for treating deep venous disease in the inferior vena cava and iliofemoral veins, representing a significant expansion of venous-specific stent indications beyond traditional arterial applications

- In June 2025, InspireMD announced that the U.S. FDA granted premarket approval (PMA) for its CGuard® Prime Carotid Stent System, a next-generation mesh-covered carotid stent designed to improve safety and stroke prevention in carotid artery stenosis patients, marking a major regulatory milestone for advanced carotid stenting technology

- In May 2025, the FDA granted De Novo clearance for Reflow Medical’s Spur Peripheral Retrievable Stent System the first retrievable stent with integrated balloon dilation designed to improve lesion access and vessel compliance in below-the-knee chronic limb-threatening ischemia

- In April 2025, Terumo Neuro’s first dual-layer micromesh carotid stent received FDA PMA approval, offering physicians a new clinical option for treating carotid artery stenosis and potentially improving procedural outcomes for at-risk patients

- In April 2024, Abbott’s Esprit™ BTK Everolimus-Eluting Resorbable Scaffold received FDA approval, becoming the first drug-eluting bioresorbable scaffold approved for below-the-knee lesions in chronic limb-threatening ischemia, significantly advancing bioabsorbable stent technology in peripheral artery disease treatment

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.