Global Vegf A Inhibitors Market

Market Size in USD Billion

USD

10.49 Billion

USD

17.02 Billion

2024

2032

USD

10.49 Billion

USD

17.02 Billion

2024

2032

| 2025 - 2032 | |

| USD 10.49 Billion | |

| USD 17.02 Billion | |

| % | |

|

Global VEGF-A Inhibitors Market Analysis

VEGF-A Inhibitors is a rapidly growing segment within the broader oncology and drug development landscape, driven by the increasing recognition of vascular endothelial growth factor-C (VEGF-C) as a key factor in the development of lymphatic vessels and the progression of various cancers. VEGF-C plays a critical role in the lymphangiogenesis process, contributing to tumor growth, metastasis, and resistance to therapies. As such, VEGF-C inhibitors are being explored as a promising therapeutic approach for treating cancers like breast cancer, melanoma, and non-small cell lung cancer (NSCLC), where lymphatic spread is a significant concern.

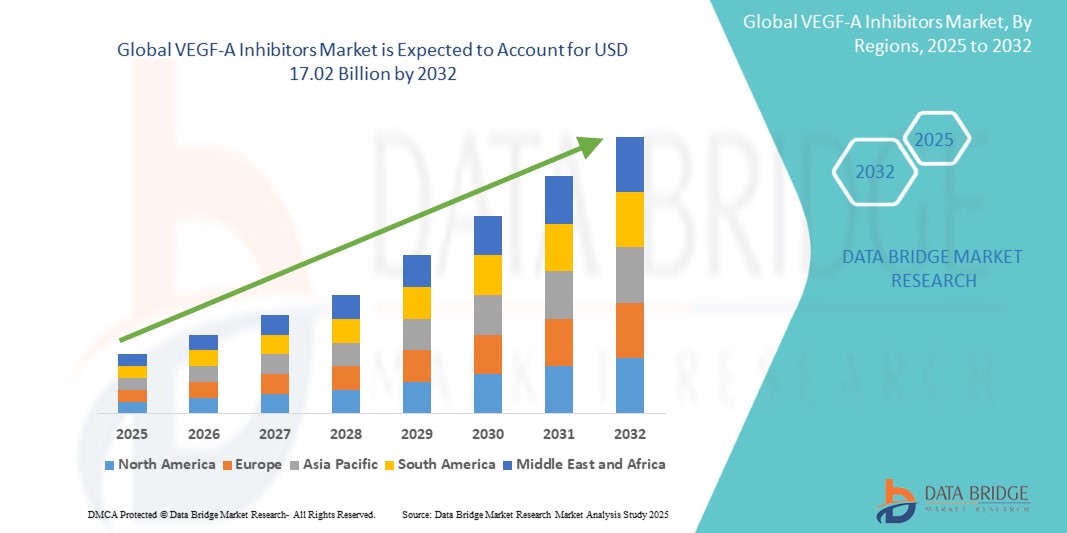

Global VEGF-A Inhibitors Market Size

Global VEGF-A inhibitors market size was valued at USD 10.49 billion in 2024 and is projected to reach USD 17.02 billion by 2032, with a CAGR of 6.2% during the forecast period of 2025 to 2032. In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework.

Global VEGF-A Inhibitors Market Trends

“Shift Toward Non-invasive Solutions”

The shift toward non-invasive solutions in the VEGF-A inhibitors market is becoming more noticeable as patients increasingly opt for procedures that involve less risk and faster recovery times. Endoscopic procedures and gastric balloons are gaining popularity due to their minimally invasive nature, offering effective weight loss results with no need for surgical incisions. These methods are seen as appealing alternatives to traditional bariatric surgeries like gastric bypass or sleeve gastrectomy, which involve more complex operations and longer recovery periods.

Non-surgical options are often associated with lower complication rates, fewer hospital stays, and quicker returns to normal activities. This trend reflects a growing preference for treatments that prioritize convenience and safety, particularly for patients hesitant about undergoing more invasive procedures. As awareness about these options spreads, more individuals are choosing non-invasive treatments to manage obesity effectively.

Report Scope and Global VEGF-A Inhibitors Market Segmentation

|

Attributes |

Global Bariatric Medical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

U.S., Canada, Mexico, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, Rest of Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, Rest of Asia-Pacific, Saudi Arabia, U.A.E., South Africa, Egypt, Israel, Rest of Middle East and Africa, Brazil, Argentina, Rest of South America |

|

Key Market Players |

Roche/Genentech (Switzerland/U.S.), Regeneron Pharmaceuticals (U.S.), Novartis AG (Switzerland), Pfizer Inc. (U.S.), Eli Lilly and Company (U.S.), Bayer AG (Germany), Amgen (U.S.), Biocon (India), Samsung Bioepis (South Korea), and Alcon (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Global VEGF-A Inhibitors Market Definition

VEGF-A inhibitors are therapies that block vascular endothelial growth factor A (VEGF-A), a protein critical for angiogenesis and vascular permeability. They prevent VEGF-A from binding to its receptors, thereby disrupting abnormal blood vessel growth. These inhibitors are used to treat conditions like cancer, where they suppress tumor blood supply, and ophthalmological diseases such as age-related macular degeneration (AMD) and diabetic retinopathy. Common examples include Bevacizumab (Avastin), Ranibizumab (Lucentis), and Aflibercept (Eylea), providing effective solutions for diseases driven by abnormal vascular activity.

Global VEGF-A Inhibitors Market Dynamics

Drivers

- Rising Incidence of VEGF-Driven Diseases

Rising incidence of VEGF-driven diseases is a significant factor driving the demand for VEGF inhibitors. Globally, the prevalence of diseases such as cancer and age-related macular degeneration (AMD), which are heavily influenced by VEGF-driven mechanisms, is increasing at an alarming rate. According to the World Health Organization (WHO), cancer remains one of the leading causes of death worldwide, with over 18 million new cases reported in 2020. Many of these cancers, including colorectal cancer and non-small cell lung cancer (NSCLC), involve abnormal VEGF activity, making VEGF inhibitors crucial in their treatment. Similarly, AMD, a leading cause of vision loss, is particularly common among the aging population and affects millions globally. In the United States, the prevalence of AMD is projected to double by 2050 as the population continues to age. This growing burden of VEGF-driven diseases underscores the rising demand for effective therapies, positioning VEGF inhibitors as essential tools in managing these conditions and improving patient outcomes.

- Innovative Drug Developments

Innovative drug developments are transforming the landscape of anti-VEGF therapies, with two key advancements standing out: biosimilars and combination therapies. The introduction of biosimilars, such as Mvasi, a biosimilar of Bevacizumab, has significantly improved the accessibility of anti-VEGF treatments, particularly in low- and middle-income countries. These cost-effective alternatives offer similar efficacy to branded biologics at a reduced price, enabling broader patient access. Alongside biosimilars, combination therapies are enhancing treatment outcomes, particularly in oncology. For instance, combining Bevacizumab with chemotherapy has demonstrated improved survival rates in patients with cancers such as colorectal and non-small cell lung cancer. These therapies work synergistically, with anti-VEGF agents inhibiting blood vessel growth that fuels tumors, while chemotherapy directly targets cancer cells. Together, these innovative approaches are expanding the reach and effectiveness of anti-VEGF treatments, addressing unmet medical needs and improving patient outcomes worldwide.

- Expanding Indications for Anti-VEGF Therapies

The scope of anti-VEGF therapies is expanding beyond their traditional applications in ophthalmology and oncology, paving the way for their use in treating a broader range of diseases. In ophthalmology, anti-VEGF agents have become the gold standard for managing conditions like age-related macular degeneration (AMD) and diabetic macular edema (DME). These therapies prevent abnormal blood vessel growth in the retina, reducing the risk of vision loss and significantly improving patients' quality of life. The market for anti-VEGF treatments in ophthalmology is witnessing rapid growth, driven by the increasing prevalence of these conditions, particularly among aging populations. In oncology, anti-VEGF therapies, especially Bevacizumab (Avastin), play a crucial role in managing cancers like colorectal cancer, non-small cell lung cancer, and renal cell carcinoma. Bevacizumab alone generated over $7 billion in global sales in 2020, highlighting its widespread adoption and effectiveness. Additionally, research is exploring the potential of anti-VEGF therapies in addressing other conditions, such as cardiovascular diseases and certain inflammatory disorders, further broadening their therapeutic applications and market potential.

Opportunities

- Emerging Markets

Emerging markets, particularly in the Asia-Pacific region, are experiencing remarkable growth in the healthcare sector, driving increased adoption of VEGF inhibitors. This growth is fueled by substantial investments in healthcare infrastructure, improved access to advanced treatments, and rising awareness of VEGF-related conditions. The healthcare market in the region is projected to grow at a CAGR of 8.3% from 2021 to 2028, reflecting this positive trajectory. Middle-income countries within Asia-Pacific are increasingly adopting therapies like Bevacizumab and Ranibizumab, as these treatments become more accessible to a broader patient base. Enhanced healthcare access and government initiatives to improve disease awareness and early diagnosis further support this trend. As the prevalence of VEGF-driven diseases such as cancers and ophthalmologic conditions rises in these regions, the demand for cost-effective and effective treatment options is expected to accelerate, solidifying the role of Asia-Pacific as a key growth hub for VEGF inhibitors.

- Advancements in Personalized Medicine

Advancements in personalized medicine are significantly enhancing the efficacy of VEGF inhibitors, particularly in oncology. The shift towards biomarker-driven therapies is at the forefront of this transformation, allowing for the customization of treatments based on individual patient profiles. By identifying genetic markers that indicate which patients will benefit most from treatments like Bevacizumab, clinicians can optimize therapy, improving outcomes while minimizing potential side effects. This precision medicine approach ensures that patients receive the most effective treatment for their specific condition, avoiding unnecessary treatments that may cause harm or be ineffective. Moreover, precision medicine is expanding the use of VEGF-A inhibitors beyond oncology, as these therapies are now being explored for a range of other diseases, including cardiovascular conditions and certain inflammatory disorders. As research continues, the ability to tailor VEGF-A inhibitors to specific disease profiles promises to offer more effective and targeted therapies, further broadening their scope and improving overall patient care.

Restraints/Challenges

- High Therapy Costs

High therapy costs associated with branded biologics like Bevacizumab (Avastin) and Eylea remain a significant barrier to the widespread accessibility of VEGF inhibitors. These biologic treatments, while highly effective, come with premium pricing, making them unaffordable for many patients, particularly in lower-income regions. For instance, the cost of a monthly treatment cycle for Bevacizumab can exceed $10,000, a price point that puts a strain on patients who may not have sufficient insurance coverage or financial resources to afford ongoing treatments. This high cost is also a major concern for healthcare systems, especially in countries with budget constraints and limited resources for sustainable healthcare spending. As the demand for anti-VEGF therapies rises, healthcare providers and governments are increasingly facing the challenge of balancing cost-effectiveness with access to life-saving treatments. The financial burden of these therapies highlights the need for alternative solutions, such as biosimilars or cost-reduction strategies, to improve accessibility without compromising patient care.

- Stringent Regulatory Pathways

Stringent regulatory pathways present a significant challenge for the approval of both new VEGF inhibitors and biosimilars. Regulatory agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have rigorous standards in place to ensure the safety and efficacy of these therapies. However, the thorough review process can be lengthy and complex, often taking several years to complete. This extended timeline can delay the entry of new treatments into the market, limiting timely access for patients who need them. Furthermore, the biosimilar approval process, which is designed to ensure that biosimilars are highly similar to existing biologics, adds additional layers of testing and regulatory scrutiny. As a result, the costs for companies involved in developing these drugs increase, as they must invest significant resources in meeting these regulatory requirements. These challenges not only delay the availability of more affordable treatments but also increase the financial burden on both companies and healthcare systems, ultimately impacting the overall accessibility of VEGF inhibitors for patients in need.

This market report provides details of new recent developments, trade regulations, import-export analysis, production analysis, value chain optimization, market share, impact of domestic and localized market players, analyses opportunities in terms of emerging revenue pockets, changes in market regulations, strategic market growth analysis, market size, category market growths, application niches and dominance, product approvals, product launches, geographic expansions, technological innovations in the market. To gain more info on the market contact Data Bridge Market Research for an Analyst Brief, our team will help you take an informed market decision to achieve market growth.

Global VEGF-A Inhibitors Market Scope

The market is segmented on the basis of drug class, therapeutic application, route of administration, and end-user. The growth amongst these segments will help you analyze meagre growth segments in the industries and provide the users with a valuable market overview and market insights to help them make strategic decisions for identifying core market applications.

Drug Class

- Anti-VEGF Monoclonal Antibodies

- VEGF-A Inhibitors

- Small Molecule Inhibitors

Therapeutic Application

- Oncology

- Ophthalmology

- Other Disorders

Route of Administration

- Intravenous

- Intravitreal

- Oral

End-User

- Hospitals

- Specialty Clinics

- Research Institutions

- Pharmaceutical and Biopharmaceutical Companies

Global VEGF-A Inhibitors Market Regional Analysis

The market is analyzed and market size insights and trends are provided by country, drug class, therapeutic application, route of administration, and end-user as referenced above.

The countries covered in the market are U.S., Canada, Mexico, Germany, France, U.K., Netherlands, Switzerland, Belgium, Russia, Italy, Spain, Turkey, rest of Europe, China, Japan, India, South Korea, Singapore, Malaysia, Australia, Thailand, Indonesia, Philippines, rest of Asia-Pacific, Saudi Arabia, U.A.E., South Africa, Egypt, Israel, rest of Middle East and Africa, Brazil, Argentina, and rest of South America.

North America is expected to dominate the market due to its advanced healthcare infrastructure, high levels of research and development (R&D) investments, and robust demand for targeted therapies. The region is home to some of the world's largest pharmaceutical and biotech companies, driving the innovation and commercialization of cutting-edge treatments. Significant investments in R&D ensure the continuous development of novel therapies, with a particular focus on precision medicine and biologics that target specific molecular pathways. The increasing demand for personalized medicine, which aims to deliver tailored therapies to patients based on genetic and molecular profiles, is a major trend in North America.

Asia-Pacific is expected to be the fastest growing due to combination of increasing healthcare investments, rising disease prevalence, and the rapid expansion of the biotech sector in countries such as China, India, and other Southeast Asian nations. As governments in the region ramp up efforts to improve healthcare infrastructure, more people are gaining access to advanced medical treatments and therapies. In particular, countries like China and India are making significant strides in building their healthcare systems and are becoming major players in the global biotech market.

The country section of the report also provides individual market impacting factors and changes in regulation in the market domestically that impacts the current and future trends of the market. Data points like down-stream and upstream value chain analysis, technical trends and porter's five forces analysis, case studies are some of the pointers used to forecast the market scenario for individual countries. Also, the presence and availability of global brands and their challenges faced due to large or scarce competition from local and domestic brands, impact of domestic tariffs and trade routes are considered while providing forecast analysis of the country data.

Global VEGF-A Inhibitors Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

Global VEGF-A Inhibitors Market Leaders Operating in the Market Are:

- Roche/Genentech (Switzerland/U.S.)

- Regeneron Pharmaceuticals (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- Amgen (U.S.)

- Biocon (India)

- Samsung Bioepis (South Korea)

- Alcon (Switzerland)

Latest Developments in Global VEGF-A Inhibitors Market

- In March 2021, Pfizer Inc. received FDA approval for a supplemental New Drug Application (sNDA) for LORBRENA (lorlatinib), expanding its indication to include first-line treatment for patients with anaplastic lymphoma kinase (ALK)-positive metastatic non-small cell lung cancer (NSCLC)

- On November 2023, the U.S. Food and Drug Administration (FDA) approved Augtyro (repotrectinib) for the treatment of adult patients with locally advanced or metastatic ROS1-positive non-small cell lung cancer (NSCLC)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.