Global Venipuncture Needles And Syringes Market

Market Size in USD Billion

USD

833.39 Billion

USD

1,234.11 Billion

2025

2033

USD

833.39 Billion

USD

1,234.11 Billion

2025

2033

| 2026 - 2033 | |

| USD 833.39 Billion | |

| USD 1,234.11 Billion | |

| % | |

|

Venipuncture Needles and Syringes Market Size

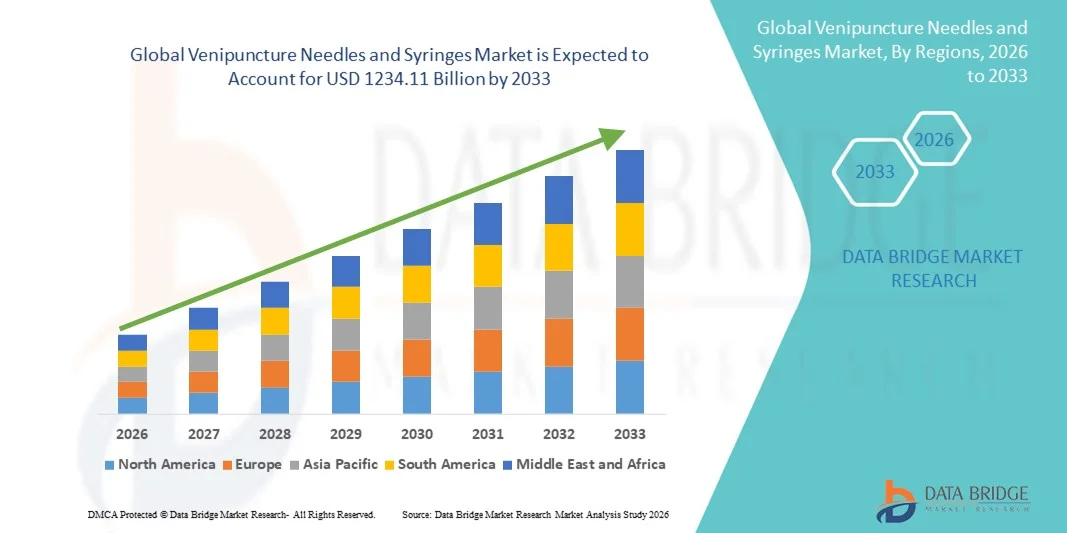

- The global venipuncture needles and syringes market size was valued at USD 833.39 billion in 2025 and is expected to reach USD 1234.11 billion by 2033, at a CAGR of 5.03% during the forecast period

- The market growth is primarily driven by the rising prevalence of chronic diseases, increasing diagnostic testing, and expanding vaccination programs worldwide. The growing volume of blood collection procedures in hospitals, diagnostic laboratories, and blood banks has significantly increased demand, with routine venipuncture procedures accounting for over 55% of total needle and syringe utilization in 2025

- Furthermore, increasing emphasis on patient safety, infection control, and the adoption of safety-engineered venipuncture devices is accelerating market expansion. Safety needles and syringes now represent approximately 48–52% of total market revenue, supported by regulatory mandates and healthcare facility protocols. These factors are collectively driving steady adoption of venipuncture needles and syringes, contributing to a market CAGR of around during the forecast period, thereby significantly boosting overall industry growth

Venipuncture Needles and Syringes Market Analysis

- Venipuncture needles and syringes are essential medical devices used for blood collection, intravenous therapy, and diagnostic testing across hospitals, clinics, and diagnostic laboratories. Their importance continues to grow due to increasing healthcare utilization, expansion of preventive diagnostics, and rising demand for minimally invasive blood sampling techniques in both public and private healthcare settings

- The escalating demand for venipuncture needles and syringes is primarily driven by the rising prevalence of chronic diseases, growing geriatric population, and increasing volume of routine blood tests and vaccination programs. In addition, heightened awareness regarding infection prevention and the shift toward safety-engineered devices are strengthening adoption, with safety venipuncture products accounting for approximately 50–55% of total market demand in 2025

- North America dominated the venipuncture needles and syringes market with the largest revenue share of approximately 41.3% in 2025, supported by advanced healthcare infrastructure, high diagnostic testing rates, strict safety regulations, and strong presence of leading medical device manufacturers. The U.S. contributed the majority share due to widespread adoption of safety needles and strong reimbursement frameworks

- Asia-Pacific is expected to be the fastest-growing region in the venipuncture needles and syringes market during the forecast period, registering a CAGR driven by increasing healthcare expenditure, expanding hospital networks, rising awareness of early disease diagnosis, and growing patient populations in countries such as China, India, and Japan

- The needles segment dominated the largest market revenue share of 58.6% in 2025, driven by their essential role in routine blood collection, diagnostic testing, and intravenous access procedures across healthcare settings

Report Scope and Venipuncture Needles and Syringes Market Segmentation

|

Attributes |

Venipuncture Needles and Syringes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Venipuncture Needles and Syringes Market Trends

Rising Adoption of Safety-Engineered and Single-Use Devices

- A prominent and accelerating trend in the global venipuncture needles and syringes market is the increasing adoption of safety-engineered and single-use devices designed to reduce needlestick injuries and prevent cross-contamination

- Healthcare providers are increasingly prioritizing occupational safety for clinicians while maintaining high standards of patient care

- Safety venipuncture needles equipped with features such as retractable needles, shielded tips, and passive safety mechanisms are gaining widespread acceptance across hospitals, diagnostic laboratories, and blood collection centers

- For instance, BD (Becton, Dickinson and Company) offers the BD Vacutainer Push Button Blood Collection Set, which incorporates a one-handed safety activation mechanism to help reduce accidental needlestick injuries after blood collection

- The growing emphasis on infection prevention and control (IPC) has further accelerated the transition toward disposable venipuncture products, particularly in high-volume settings such as pathology labs, vaccination centers, and outpatient clinics

- In addition, advancements in ergonomic design and material quality are improving ease of use, precision, and patient comfort during blood collection procedures. Manufacturers are focusing on ultra-thin wall needles and smoother bevel designs to minimize pain and improve blood flow efficiency

- This trend is fundamentally reshaping product development strategies, with leading companies investing in regulatory-compliant, safety-focused innovations to align with evolving healthcare standards and workplace safety regulations worldwide

Venipuncture Needles and Syringes Market Dynamics

Driver

Growing Demand Driven by Rising Diagnostic Testing and Chronic Disease Prevalence

- The increasing global burden of chronic diseases such as diabetes, cardiovascular disorders, cancer, and infectious diseases is a major driver of demand for venipuncture needles and syringes. These conditions require frequent blood sampling for diagnosis, treatment monitoring, and disease management

- The expanding volume of diagnostic and laboratory testing, supported by the growth of preventive healthcare and routine health screenings, is significantly boosting the consumption of venipuncture products across healthcare facilities

- For instance, the expansion of large diagnostic laboratory networks such as Quest Diagnostics and Dr. Lal PathLabs has led to a substantial increase in daily blood sample collections, directly driving demand for high-quality venipuncture needles and syringes

- Moreover, the aging global population is increasing the frequency of medical visits and laboratory investigations, reinforcing the long-term demand for venipuncture products in both inpatient and outpatient settings

- Public health screening programs, vaccination campaigns, and disease surveillance initiatives further contribute to sustained demand, particularly in government and community healthcare facilities

- The growing awareness among healthcare professionals regarding standardized blood collection practices and compliance with clinical guidelines is also supporting market growth, as facilities increasingly adopt reliable and safety-compliant venipuncture devices

Restraint/Challenge

Risk of Needlestick Injuries and Cost Pressure on Healthcare Systems

- Despite technological advancements, needlestick injuries remain a significant concern, particularly in resource-limited settings where traditional, non-safety needles are still widely used

- These injuries expose healthcare workers to bloodborne pathogens, creating safety risks and potential legal liabilities for healthcare institutions

- The higher cost of safety-engineered venipuncture needles compared to conventional devices can act as a barrier to adoption, especially for small clinics, public hospitals, and healthcare systems operating under tight budget constraints

- For instance, many government hospitals in low- and middle-income countries continue to rely on conventional needles due to procurement cost limitations, despite awareness of safer alternatives

- In developing regions, limited awareness and insufficient training regarding proper needle handling and disposal further exacerbate safety challenges, slowing the transition to advanced venipuncture solutions

- In addition, fluctuations in raw material prices and supply chain disruptions can impact manufacturing costs and product availability, creating pricing pressures for manufacturers and end users alike

- Addressing these challenges through cost-effective product designs, bulk purchasing programs, training initiatives, and supportive regulatory policies will be essential for improving adoption rates and ensuring sustained growth of the venipuncture needles and syringes market globally

Venipuncture Needles and Syringes Market Scope

The market is segmented on the basis of product, vein type, and end-user.

- By Product

On the basis of product, the Global Venipuncture Needles and Syringes market is segmented into Needles and Syringes. The needles segment dominated the largest market revenue share of 58.6% in 2025, driven by their essential role in routine blood collection, diagnostic testing, and intravenous access procedures across healthcare settings. Venipuncture needles are widely used in hospitals, diagnostic laboratories, and blood donation centers due to their precision, safety features, and compatibility with vacuum blood collection systems. Increasing prevalence of chronic diseases, rising demand for diagnostic testing, and growth in preventive health checkups have further boosted needle consumption globally. Safety-engineered needles with features such as retractable tips and needle shields have gained strong adoption to reduce needlestick injuries. Regulatory mandates promoting the use of safety needles in developed regions have also contributed to segment dominance. In addition, high procedural volumes in outpatient and inpatient settings continue to sustain consistent demand. The wide availability of multiple gauge sizes tailored for different patient populations further strengthens market penetration. Growing awareness regarding infection control and occupational safety reinforces the sustained dominance of this segment.

The syringes segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, fueled by rising demand for disposable and safety syringes in venipuncture and therapeutic applications. Increased focus on infection prevention, particularly after global health crises, has accelerated the shift toward single-use syringes. Syringes integrated with safety mechanisms are increasingly adopted in hospitals and blood banks to minimize cross-contamination risks. Expanding immunization programs and blood sampling initiatives in emerging economies further support growth. Technological advancements such as low dead-space syringes and ergonomic designs enhance usability and accuracy. Government initiatives promoting safe injection practices also play a key role. In addition, the expansion of diagnostic laboratories and home healthcare services contributes to rising syringe consumption. These factors collectively position syringes as the fastest-growing product segment during the forecast period.

- By Vein Type

On the basis of vein type, the Global Venipuncture Needles and Syringes market is segmented into Cephalic Vein, Median Cubital Vein, Basilic Vein, and Others. The median cubital vein segment accounted for the largest market revenue share of 46.3% in 2025, owing to its widespread preference among healthcare professionals for venipuncture procedures. Located centrally in the antecubital fossa, the median cubital vein is easily accessible, well-anchored, and less prone to rolling, making it ideal for blood collection. Its large size and stable positioning reduce the risk of complications such as hematoma formation and nerve injury. High success rates associated with first-attempt cannulation drive its extensive use in hospitals and diagnostic laboratories. The vein’s suitability for patients across different age groups further supports its dominance. Training protocols for phlebotomists often prioritize the median cubital vein, reinforcing its routine usage. In addition, its compatibility with standard needle gauges enhances procedural efficiency. These advantages collectively contribute to its leading position in the global market.

The basilic vein segment is projected to grow at the fastest CAGR of 9.4% from 2026 to 2033, driven by increasing use in patients with difficult venous access. Although deeper and less visible, the basilic vein is increasingly utilized when primary veins are unsuitable due to prior venipuncture or medical conditions. Rising prevalence of chronic illnesses requiring frequent blood draws has increased reliance on alternative veins. Advances in vein visualization technologies and ultrasound-guided venipuncture have improved access to the basilic vein. Growing adoption in specialized care settings and oncology units further fuels demand. Improved training and awareness among healthcare professionals also support its increased utilization. In addition, expanding geriatric populations with fragile veins contribute to segment growth. These factors position the basilic vein segment as the fastest-growing during the forecast period.

- By End-User

On the basis of end-user, the Global Venipuncture Needles and Syringes market is segmented into Hospitals, Blood Donation Camps, and Others. The hospitals segment dominated the global market with a revenue share of 61.8% in 2025, driven by high patient footfall and a large volume of diagnostic and therapeutic procedures. Hospitals are primary centers for blood collection, intravenous therapy, and disease diagnosis, resulting in consistent demand for venipuncture products. The availability of skilled healthcare professionals and advanced infrastructure further supports high procedural efficiency. Increasing hospital admissions due to chronic diseases, surgeries, and emergency care contribute significantly to consumption. Hospitals also adhere strictly to safety and regulatory standards, encouraging the use of high-quality needles and syringes. Integration of safety-engineered devices to prevent occupational hazards further boosts demand. In addition, expansion of multispecialty hospitals in emerging economies strengthens market dominance. Continuous procurement through bulk purchasing agreements also sustains revenue leadership.

The blood donation camps segment is anticipated to register the fastest CAGR of 10.1% from 2026 to 2033, driven by growing awareness about voluntary blood donation and rising demand for blood components. Government initiatives and non-profit organizations actively promote regular blood donation drives, increasing procedural volumes. Expansion of mobile blood collection units in rural and semi-urban regions further supports growth. Advances in portable and user-friendly venipuncture devices improve efficiency in camp settings. Rising trauma cases, surgical procedures, and transfusion needs globally fuel demand for donated blood. Enhanced safety protocols and disposable product usage further accelerate adoption. In addition, corporate social responsibility (CSR) initiatives and community health programs boost the frequency of donation camps. These factors collectively position blood donation camps as the fastest-growing end-user segment.

Venipuncture Needles and Syringes Market Regional Analysis

- North America dominated the venipuncture needles and syringes market, accounting for approximately 41.3% of the global revenue share in 2025

- This leadership is primarily supported by the region’s advanced healthcare infrastructure, high volume of diagnostic and therapeutic blood collection procedures, and stringent safety regulations governing the use of medical sharps. The strong presence of leading medical device manufacturers, along with continuous product innovations such as safety-engineered needles and prefilled syringes, further strengthens market growth

- In addition, high healthcare spending and widespread adoption of standardized infection control practices across hospitals, diagnostic laboratories, and blood banks continue to drive sustained demand in the region

U.S. Venipuncture Needles and Syringes Market Insight

The U.S. venipuncture needles and syringes market captured the majority share within North America in 2025, driven by the widespread adoption of safety venipuncture needles and syringes to prevent needlestick injuries and bloodborne infections. Strong reimbursement frameworks, high diagnostic testing rates, and a well-established outpatient and hospital network significantly contribute to market expansion. Increasing prevalence of chronic diseases, growing demand for routine blood tests, and compliance with Occupational Safety and Health Administration (OSHA) guidelines further support the consistent use of advanced venipuncture products across healthcare settings.

Europe Venipuncture Needles and Syringes Market Insight

The Europe venipuncture needles and syringes market is projected to grow at a steady CAGR during the forecast period, supported by strict regulatory standards related to patient safety and medical waste management. Rising demand for early disease diagnosis, increasing geriatric population, and the expansion of public healthcare systems across major European countries are driving product adoption. The growing preference for safety-engineered devices in hospitals and diagnostic laboratories is also contributing to regional market growth.

U.K. Venipuncture Needles and Syringes Market Insight

The U.K. venipuncture needles and syringes market is expected to witness notable growth during the forecast period due to increasing diagnostic testing volumes and strong emphasis on healthcare worker safety. Government-led initiatives to reduce needlestick injuries, along with high utilization of venipuncture procedures in routine health screenings and chronic disease management, are accelerating demand for advanced needles and syringes across hospitals and pathology labs.

Germany Venipuncture Needles and Syringes Market Insight

The Germany venipuncture needles and syringes market is anticipated to expand at a considerable CAGR, supported by the country’s well-developed healthcare infrastructure and focus on technological innovation in medical devices. Increasing awareness of infection prevention, coupled with rising demand for high-quality and eco-friendly disposable medical products, is encouraging the adoption of safety venipuncture devices in both inpatient and outpatient settings.

Asia-Pacific Venipuncture Needles and Syringes Market Insight

The Asia-Pacific venipuncture needles and syringes market region is expected to be the fastest-growing market for venipuncture needles and syringes during the forecast period, registering a robust CAGR. Growth is driven by increasing healthcare expenditure, expanding hospital and diagnostic laboratory networks, and rising awareness of early disease detection. Rapid urbanization, improving access to healthcare services, and large patient populations in countries such as China, India, and Japan are significantly boosting demand for blood collection devices. Additionally, the region’s emergence as a major manufacturing hub is improving product availability and affordability.

Japan Venipuncture Needles and Syringes Market Insight

The Japan venipuncture needles and syringes market is gaining steady momentum due to its advanced healthcare system, aging population, and high frequency of routine diagnostic testing. The growing need for minimally invasive and safer blood collection solutions is encouraging the adoption of safety-engineered venipuncture needles. Increased focus on patient comfort and healthcare worker safety continues to support market expansion across hospitals, clinics, and diagnostic centers.

China Venipuncture Needles and Syringes Market Insight

China venipuncture needles and syringes market accounted for the largest revenue share in the Asia-Pacific region in 2025, driven by rapid expansion of healthcare infrastructure, a growing middle-class population, and increasing government investment in public health initiatives. Rising demand for diagnostic testing, coupled with strong domestic manufacturing capabilities, is accelerating the adoption of venipuncture needles and syringes across hospitals, blood banks, and diagnostic laboratories. The push toward early diagnosis and preventive healthcare further strengthens market growth in the country.

Venipuncture Needles and Syringes Market Share

The Venipuncture Needles and Syringes industry is primarily led by well-established companies, including:

• Terumo Corporation (Japan)

• Nipro Corporation (Japan)

• Smiths Medical (U.K.)

• B. Braun S.E. (Germany)

• Greiner Bio-One International GmbH (Austria)

• Sarstedt AG & Co. KG (Germany)

• Cardinal Health (U.S.)

• Medtronic plc (Ireland)

• Vygon Group (France)

• Weigao Group Medical Polymer Co., Ltd. (China)

• Hindustan Syringes & Medical Devices Ltd. (India)

• Retractable Technologies, Inc. (U.S.)

• EXELINT International (U.S.)

• Jiangsu Jichun Medical Devices Co., Ltd. (China)

• Narang Medical Limited (India)

• Vitromed Healthcare (India)

• SungShim Medical Co., Ltd. (South Korea)

Latest Developments in Global Venipuncture Needles and Syringes Market

- In June 2021, Hindustan Syringes & Medical Devices announced the launch of its DispoJekt Safety Needle, a single-use venipuncture needle designed to significantly reduce the risk of needlestick injuries among healthcare workers. The product incorporates an integrated safety mechanism that activates immediately after blood collection, aligning with global efforts to improve occupational safety in hospitals and diagnostic laboratories. This launch strengthened the company’s position as a leading supplier of safety-engineered needles, particularly in emerging markets with increasing emphasis on infection control and safe injection practices

- In November 2023, Becton, Dickinson and Company (BD) introduced the PIVO Pro Needle-free Blood Collection Device, following U.S. FDA 510(k) clearance. The device enables blood collection directly from an existing peripheral IV catheter without the need for an additional venipuncture, reducing patient discomfort and minimizing repeated needle insertions. The launch represented a significant technological advancement in blood collection practices and supported BD’s broader “One-Stick Hospital Stay” initiative, aimed at improving patient experience while reducing complications associated with multiple needle sticks

- In March 2024, VYGON expanded its venipuncture portfolio with the launch of a next-generation safety blood collection needle system. The product was designed to enhance patient comfort through optimized needle geometry while incorporating passive safety features to prevent accidental needle exposure after use. This development reflected the growing demand from healthcare providers for devices that balance procedural efficiency, patient comfort, and staff safety

- In April 2024, BD India announced the commercial launch of the BD Vacutainer UltraTouch Push Button Blood Collection Set in the Indian market. The device features an ultra-thin wall cannula and push-button safety activation, aimed at reducing insertion pain and improving blood flow consistency during venipuncture. The launch addressed the increasing demand for premium blood collection solutions in high-volume diagnostic centers across India and reinforced BD’s focus on innovation tailored to regional healthcare needs

- In November 2024, Greiner Bio-One completed the acquisition of SIS Medical, a move that expanded its capabilities in blood collection and venipuncture device manufacturing. This acquisition allowed Greiner Bio-One to strengthen its production footprint and enhance its portfolio of needles and syringes used in diagnostic and clinical settings, supporting long-term growth in the global venipuncture consumables market

- In March 2025, Terumo Corporation entered into a strategic distribution partnership with Fisher Scientific to expand the global reach of its venipuncture needles and blood collection systems. Through Fisher Scientific’s extensive laboratory and healthcare distribution network, Terumo aimed to improve product accessibility across hospitals, diagnostic laboratories, and research institutions, particularly in North America and Europe

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.