Global Ventriculo Peritoneal Hydrocephalus Shunts Market

Market Size in USD Million

USD

412.60 Million

USD

600.37 Million

2025

2033

USD

412.60 Million

USD

600.37 Million

2025

2033

| 2026 - 2033 | |

| USD 412.60 Million | |

| USD 600.37 Million | |

| % | |

|

Ventriculo-Peritoneal Hydrocephalus Shunts Market Overview

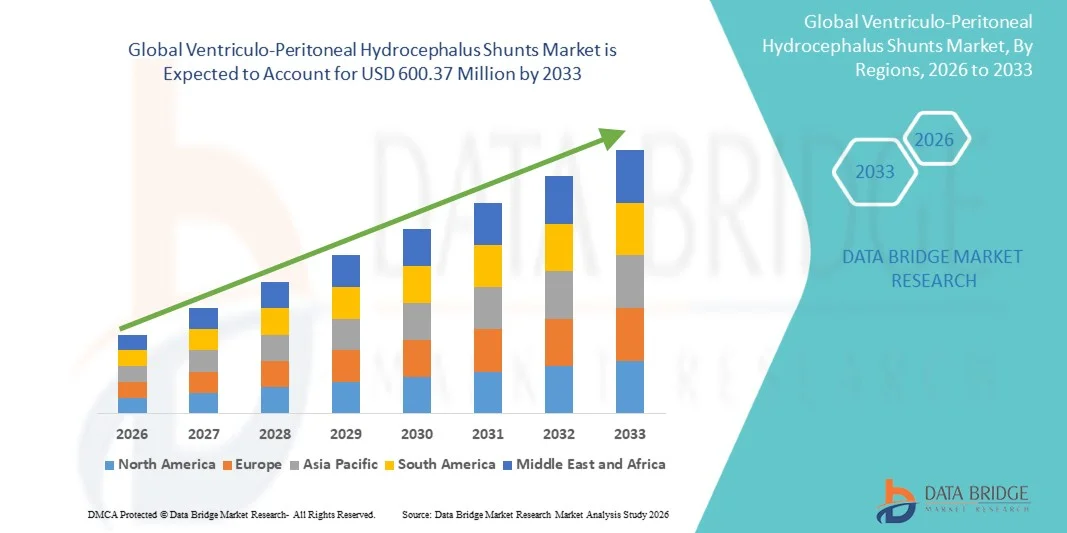

The Ventriculo-Peritoneal Hydrocephalus Shunts Market was valued at USD 412.60 Million in 2025 and is projected to reach USD 600.37 Million by 2033, growing at a CAGR of 4.80% from 2026 to 2033. The market is experiencing steady growth driven by the rising prevalence of hydrocephalus, increasing neurosurgical procedures, and growing demand for advanced cerebrospinal fluid (CSF) management solutions. Technological advancements in programmable shunt valves, anti-siphon devices, and infection-resistant catheter systems are improving treatment outcomes and enhancing long-term patient management across both pediatric and adult populations.

The increasing incidence of congenital hydrocephalus, traumatic brain injuries, brain tumors, intracranial hemorrhage, and age-related neurological disorders is driving demand for ventriculo-peritoneal hydrocephalus shunts worldwide. Healthcare providers are increasingly adopting programmable and pressure-adjustable shunt systems that allow personalized CSF drainage while reducing complications such as overdrainage and underdrainage. In addition, growing investments in neurosurgical infrastructure, expanding access to specialized neurological care, and rising awareness regarding early diagnosis and treatment of hydrocephalus are supporting market expansion. Continuous innovations in biocompatible materials, infection prevention technologies, and minimally invasive neurosurgical techniques are further accelerating the adoption of ventriculo-peritoneal hydrocephalus shunt systems across global healthcare settings.

Key Market Trends & Insights

- North America dominated the Ventriculo-Peritoneal Hydrocephalus Shunts Market with the largest revenue share of 39.12% in 2025, supported by advanced neurosurgical infrastructure, high diagnosis rates of hydrocephalus, favorable reimbursement policies, and strong adoption of programmable shunt systems across major healthcare facilities.

- The Hydrocephalus Valves segment dominated the market with a 48% revenue share in 2025, driven by their critical role in regulating cerebrospinal fluid (CSF) flow and maintaining intracranial pressure stability.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.8% from 2026 to 2033, fueled by expanding healthcare infrastructure, rising awareness of neurological disorders, increasing pediatric healthcare investments, and improving access to neurosurgical treatment across China, India, and Japan.

- The Hydrocephalus Catheters segment is projected to register the fastest growth at a CAGR of 7.5%, supported by technological advancements in infection-resistant catheter materials, increasing shunt implantation procedures, and growing demand for long-term hydrocephalus management solutions.

- The Pediatric segment dominates the age group category with a 58.64% revenue share in 2025, owing to the high prevalence of congenital hydrocephalus, neonatal brain abnormalities, and increasing early diagnosis and surgical intervention among infants and children.

- Hospitals account for 78.93% of the market in 2025, preferred due to the availability of specialized neurosurgeons, advanced diagnostic imaging systems, intensive postoperative care facilities, and comprehensive hydrocephalus treatment programs.

- The Ambulatory Surgical Centers (ASCs) segment is expected to be the fastest-growing end-user category, registering a CAGR of 7.2% from 2026 to 2033, driven by increasing demand for cost-effective surgical procedures, shorter hospital stays, technological advancements in minimally invasive neurosurgery, and expanding outpatient surgical capabilities worldwide.

Market Size & Forecast

- Global Market Value (2025): USD 412.60 Million

- Expected Market Value (2033): USD 600.37 Million

- Forecast CAGR (2026–2033): 4.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Ventriculo-Peritoneal Hydrocephalus Shunts Market Segmentation

|

Attributes |

Ventriculo-Peritoneal Hydrocephalus Shunts Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Medtronic plc (Ireland) |

|

Market Opportunities |

· Advancement in Programmable and Smart Shunt Systems · Rising Demand in Emerging Markets and Pediatric Neurosurgery Expansion · Growth in Minimally Invasive Neurosurgical Procedures and Outpatient Care Settings |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Ventriculo-Peritoneal Hydrocephalus Shunts Market Trends

Trend: Rising Adoption of Programmable and Infection-Resistant Shunt Systems

The ventriculo-peritoneal hydrocephalus shunts market is witnessing a strong shift toward programmable shunt valves and infection-resistant catheter systems designed to improve long-term patient outcomes. Modern shunt systems allow non-invasive adjustment of cerebrospinal fluid (CSF) drainage pressure, reducing the need for revision surgeries and improving clinical flexibility. According to neurosurgical clinical literature, shunt malfunction and infection rates can affect a significant proportion of patients over time, driving continuous innovation in device design. Leading hospitals and neurosurgical centers are increasingly adopting antibiotic-impregnated catheters and MRI-compatible programmable valves to reduce post-operative complications. In addition, advancements in flow-regulated and gravitational valve technologies are improving physiological CSF management, particularly in pediatric hydrocephalus cases where long-term treatment precision is critical.

Ventriculo-Peritoneal Hydrocephalus Shunts Market Dynamics

Key Market Driver: Rising Incidence of Hydrocephalus and Expanding Neurosurgical Procedures

The increasing prevalence of hydrocephalus across pediatric and adult populations is a major driver of market growth. Hydrocephalus affects an estimated 1–1.5 per 1,000 live births globally, with congenital cases being a significant contributor to pediatric neurosurgical volume. In adults, conditions such as traumatic brain injury, intracranial hemorrhage, brain tumors, and normal pressure hydrocephalus are contributing to rising surgical interventions. According to the Hydrocephalus Association, hundreds of thousands of shunt surgeries are performed globally each year, highlighting the sustained clinical demand for ventriculo-peritoneal shunting systems. Expanding access to neurosurgical care, improving diagnostic imaging capabilities (CT and MRI), and increasing awareness of neurological disorders are further accelerating early diagnosis and treatment adoption. In addition, growing healthcare investments and expansion of tertiary care hospitals in emerging economies are improving patient access to life-saving neurosurgical procedures.

Key Restraint/Challenge: Shunt Malfunction, Infection Risks, and Revision Surgeries

A significant challenge in the ventriculo-peritoneal hydrocephalus shunts market is the risk of long-term complications associated with shunt implantation. Shunt failure rates remain clinically relevant, with studies indicating that a considerable percentage of patients may require revision surgery within the first few years due to blockage, infection, or mechanical failure. Infection remains one of the most serious complications, often requiring shunt removal and prolonged antibiotic treatment. In pediatric patients, the lifetime risk of multiple revisions further increases clinical burden and healthcare costs. In addition, challenges such as overdrainage, underdrainage, and catheter migration continue to impact treatment outcomes. Variability in surgical expertise across regions and limited access to specialized neurosurgical care in low-resource settings further restrict optimal patient management. These factors collectively increase treatment complexity and pose ongoing challenges for market expansion despite technological improvements.

Key Market Opportunity: Advancements in Smart Shunt Technologies and Digital Neurological Monitoring

The development of next-generation “smart” hydrocephalus shunt systems presents a major market opportunity. Emerging technologies include pressure-sensing valves, externally programmable systems, and integrated monitoring solutions designed to provide real-time insights into CSF flow dynamics. Research institutions and medical device companies are actively exploring sensor-based shunts capable of detecting early signs of blockage or malfunction, potentially reducing emergency interventions. In parallel, the integration of digital health platforms and AI-assisted diagnostic tools is enabling improved post-operative monitoring and personalized treatment planning. For example, tele-neurosurgery follow-ups and cloud-based patient tracking systems are being explored to improve long-term shunt management outcomes. Increasing healthcare digitization, rising investment in neurotechnology startups, and growing demand for precision neurosurgery in North America, Europe, and Asia-Pacific are expected to significantly expand innovation opportunities in this market over the forecast period.

Ventriculo-Peritoneal Hydrocephalus Shunts Market Scope

The Ventriculo-Peritoneal Hydrocephalus Shunts market is segmented on the basis of product type, age group, and end-user.

- By Product Type

On the basis of product type, the Ventriculo-Peritoneal Hydrocephalus Shunts Market is segmented into hydrocephalus valves and hydrocephalus catheters. The Hydrocephalus Valves segment dominated the market with a 63.48% revenue share in 2025, driven by their critical role in regulating cerebrospinal fluid (CSF) flow and maintaining intracranial pressure stability. Increasing adoption of programmable valves allows clinicians to non-invasively adjust drainage settings, reducing the risk of overdrainage and underdrainage complications. Advanced valve technologies such as gravitational valves and anti-siphon mechanisms are improving long-term treatment outcomes. Rising preference for MRI-compatible and infection-resistant valve systems is further strengthening clinical adoption. Continuous innovation by leading manufacturers in precision flow-control systems is supporting surgical efficiency. Growing pediatric neurosurgery volumes are also contributing significantly to demand. Expanding use in normal pressure hydrocephalus (NPH) cases among elderly populations is reinforcing segment leadership. Hospitals increasingly prefer advanced valve systems due to better post-operative management outcomes. Improved durability and reduced revision surgery rates are further boosting adoption. Overall, technological advancement and clinical reliability are driving dominance of this segment.

The Hydrocephalus Catheters segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by innovations in biocompatible and infection-resistant materials. Increasing focus on reducing shunt infection rates is supporting demand for advanced catheter coatings. Enhanced flexibility and durability of modern catheters are improving surgical success rates. Rising neurosurgical procedures globally are further accelerating segment expansion. Growth in pediatric hydrocephalus cases is significantly boosting catheter demand. Technological improvements in catheter design are enabling better CSF drainage efficiency. Increasing adoption in revision surgeries is also contributing to growth. Expanding healthcare infrastructure in emerging economies is improving accessibility. Continuous R&D in antimicrobial catheter materials is strengthening market penetration. Higher survival rates in neonatal care are increasing long-term shunt usage. Overall, innovation and rising clinical need are fueling rapid growth.

- By Age Group

On the basis of age group, the market is segmented into pediatric and adult populations. The Pediatric segment dominated the market with a 58.64% revenue share in 2025, due to the high incidence of congenital hydrocephalus and neural tube defects. Early diagnosis through neonatal screening programs is increasing surgical intervention rates. Pediatric patients often require long-term shunt dependency, driving sustained demand. Hospitals are adopting child-specific programmable shunt systems for improved outcomes. Increasing awareness of pediatric neurological disorders is supporting early treatment adoption. Government initiatives for child healthcare are strengthening access to neurosurgical care. Advances in minimally invasive pediatric neurosurgery are improving survival rates. Rising birth-related complications in developing regions are contributing to segment dominance. Continuous monitoring requirements increase device utilization over time. Improved neonatal ICU infrastructure is supporting early intervention. Overall, high disease burden in infants ensures strong pediatric dominance.

The Adult segment is projected to register the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by rising cases of traumatic brain injuries and brain tumors. Increasing prevalence of normal pressure hydrocephalus (NPH) among the elderly is a key growth factor. Aging global population is significantly expanding patient pool. Improved diagnostic imaging (MRI and CT) is enabling earlier detection. Increasing stroke and intracranial hemorrhage cases are driving demand for shunt implantation. Greater awareness of adult hydrocephalus is improving treatment rates. Expanding neurology departments in hospitals is supporting surgical volumes. Rising geriatric healthcare expenditure is boosting adoption. Better post-operative care systems are improving survival outcomes. Increasing insurance coverage for neurosurgical procedures is further supporting growth. Overall, demographic aging and improved diagnosis are accelerating expansion.

- By End-User

On the basis of end-user, the market is segmented into hospitals and ambulatory surgical centers. The Hospitals segment dominated the market with a 78.93% revenue share in 2025, owing to availability of advanced neurosurgical infrastructure and skilled specialists. Hospitals are equipped with ICU support required for post-operative hydrocephalus care. High patient inflow and emergency neurosurgical cases drive dominance. Availability of advanced imaging systems supports accurate diagnosis and treatment planning. Hospitals handle complex and revision shunt surgeries more efficiently. Strong presence of multidisciplinary neurology teams enhances treatment success. Government funding and public healthcare systems support hospital dominance. Increasing adoption of programmable shunt systems is concentrated in hospital settings. Better infection control infrastructure improves surgical outcomes. Hospitals remain primary centers for pediatric neurosurgery procedures. Overall, comprehensive care facilities ensure strong market leadership.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by rising demand for cost-effective outpatient neurosurgical procedures. Increasing preference for shorter hospital stays is supporting ASC adoption. Advances in minimally invasive shunt implantation techniques are enabling outpatient procedures. Lower procedural costs compared to hospitals are attracting patients. Improved recovery protocols are making ASCs more viable for neurosurgery. Expansion of specialized neurology outpatient centers is boosting growth. Increasing healthcare privatization in emerging markets is supporting ASC expansion. Rising focus on healthcare efficiency is driving shift toward outpatient care. Technological advancements in portable imaging and surgical tools are enabling safe procedures. Insurance providers are increasingly supporting outpatient neurosurgery coverage. Overall, cost efficiency and procedural innovation are fueling rapid growth.

Ventriculo-Peritoneal Hydrocephalus Shunts Market Regional Analysis

North America dominated the Ventriculo-Peritoneal Hydrocephalus Shunts market and accounted for the largest revenue share of 39.12% in 2025, supported by advanced neurosurgical infrastructure, high diagnosis rates of hydrocephalus, favorable reimbursement policies, and strong adoption of programmable shunt systems across major healthcare facilities. The region also benefits from the presence of leading medical device manufacturers, well-established hospital networks, and rapid adoption of minimally invasive neurosurgical procedures. Increasing prevalence of neurological disorders, rising geriatric population, and strong clinical preference for advanced cerebrospinal fluid (CSF) management solutions continue to reinforce North America’s dominance in the global market.

U.S. Ventriculo-Peritoneal Hydrocephalus Shunts Market Insight

The U.S. Ventriculo-Peritoneal Hydrocephalus Shunts market is witnessing steady growth due to a high burden of hydrocephalus cases, strong healthcare expenditure, and widespread availability of advanced neurosurgical care. The country’s robust medical device ecosystem, coupled with rapid adoption of programmable and adjustable shunt technologies, is driving demand across hospitals and specialized neurology centers. In addition, favorable insurance coverage, increasing neonatal intensive care admissions, and ongoing clinical advancements in hydrocephalus management are further supporting market expansion.

Europe Ventriculo-Peritoneal Hydrocephalus Shunts Market Insight

The Europe Ventriculo-Peritoneal Hydrocephalus Shunts market remains a key regional contributor, driven by strong public healthcare systems, early diagnosis programs, and high awareness of neurological disorders. Countries across the region are increasingly adopting advanced cerebrospinal fluid management devices to improve surgical outcomes and reduce revision rates. Growing investments in neurosurgical research, combined with structured reimbursement frameworks and expanding access to specialized care, continue to support steady market growth across Europe.

U.K. Ventriculo-Peritoneal Hydrocephalus Shunts Market Insight

The U.K. Ventriculo-Peritoneal Hydrocephalus Shunts market is growing steadily, supported by the National Health Service (NHS) infrastructure and increasing adoption of advanced neurosurgical devices. Rising cases of hydrocephalus, particularly in pediatric populations, along with improved diagnostic capabilities, are driving demand. Furthermore, the country’s focus on clinical innovation, evidence-based treatment pathways, and integration of programmable shunt systems is strengthening overall market adoption.

Germany Ventriculo-Peritoneal Hydrocephalus Shunts Market Insight

The Germany Ventriculo-Peritoneal Hydrocephalus Shunts market is expanding due to its advanced hospital infrastructure, strong neurosurgical expertise, and high adoption of technologically advanced implantable devices. Increasing emphasis on precision medicine, combined with strong research and development in neurological care, is supporting market growth. In addition, favorable healthcare reimbursement systems and growing geriatric population are further accelerating demand for hydrocephalus shunt procedures.

Asia-Pacific Ventriculo-Peritoneal Hydrocephalus Shunts Market Insight

The Asia-Pacific Ventriculo-Peritoneal Hydrocephalus Shunts market is expected to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by expanding healthcare infrastructure, rising awareness of neurological disorders, and increasing investments in pediatric neurosurgical care. Improving access to advanced medical technologies, growing healthcare expenditure, and expansion of specialized neurology centers across emerging economies are further supporting regional growth. In addition, government initiatives aimed at strengthening early diagnosis and treatment of hydrocephalus are accelerating adoption across the region.

Japan Ventriculo-Peritoneal Hydrocephalus Shunts Market Insight

The Japan Ventriculo-Peritoneal Hydrocephalus Shunts market is witnessing steady growth due to its highly developed healthcare system, aging population, and strong focus on advanced neurosurgical procedures. Increasing use of programmable shunt systems and precision-based surgical approaches is enhancing treatment outcomes. Moreover, continuous advancements in medical device technologies and strong hospital infrastructure are contributing to sustained market expansion.

China Ventriculo-Peritoneal Hydrocephalus Shunts Market Insight

The China Ventriculo-Peritoneal Hydrocephalus Shunts market is growing rapidly, supported by expanding healthcare infrastructure, rising awareness of neurological diseases, and increasing government investments in specialized medical care. The growing pediatric patient pool, improving access to neurosurgical procedures in tier-2 and tier-3 cities, and rapid modernization of hospitals are significantly boosting demand. In addition, strong domestic medical device manufacturing capabilities and increasing adoption of advanced shunt technologies are positioning China as one of the fastest-growing markets globally.

Ventriculo-Peritoneal Hydrocephalus Shunts Market Share

The Ventriculo-Peritoneal Hydrocephalus Shunts industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- B. Braun Melsungen AG (Germany)

- Integra LifeSciences Holdings Corporation (U.S.)

- Johnson & Johnson (DePuy Synthes) (U.S.)

- Sophysa S.A. (France)

- Spiegelberg GmbH & Co. KG (Germany)

- Möller Medical GmbH (Germany)

- Christoph Miethke GmbH & Co. KG (Germany)

- Natus Medical Incorporated (U.S.)

- HLL Lifecare Limited (India)

- Delta Surgical Ltd. (U.K.)

- Kaneka Corporation (Japan)

- Tokibo Co., Ltd. (Japan)

- Spiegelberg GmbH (Germany)

- Aesculap, Inc. (U.S.)

- Terumo Corporation (Japan)

- LivaNova PLC (U.K.)

- Braun & Company (Europe)

- Jiangsu Huida Medical Instruments (China)

- MicroPort Scientific Corporation (China)

- Stryker Corporation (U.S.)

- Renishaw plc (U.K.)

- Neuromedex GmbH (Germany)

- G. Surgiwear Ltd. (India)

- Surtex Instruments Ltd. (U.K.)

- Vygon SA (France)

- Cook Medical (U.S.)

- Boston Scientific Corporation (U.S.)

- Paul Hartmann AG (Germany)

- Teleflex Incorporated (U.S.)

- Alcon Inc. (Switzerland)

- Olympus Corporation (Japan)

Latest Developments in Ventriculo-Peritoneal Hydrocephalus Shunts Market

- In March 2021, Medtronic continued global clinical expansion of its Strata adjustable valve shunt system, a widely used programmable cerebrospinal fluid (CSF) diversion device for hydrocephalus management. The system’s magnetic adjustability feature enabled non-invasive pressure setting modifications, improving post-surgical flexibility and reducing revision procedures. Increased adoption across pediatric neurosurgery centers in North America and Europe highlighted the growing shift toward programmable VP shunt technologies in chronic hydrocephalus care

- In July 2021, Integra LifeSciences strengthened the global clinical footprint of its Codman Hakim programmable valve system, one of the most established hydrocephalus shunt platforms. Hospitals increasingly adopted the system for its adjustable pressure control mechanism and compatibility with neuroimaging workflows. The development reinforced the market transition toward precision-based cerebrospinal fluid management solutions in both adult and pediatric neurosurgical procedures

- In February 2022, B. Braun (Aesculap) expanded the clinical adoption of its proGAV and proSA gravitational valve systems, designed to reduce overdrainage complications in VP shunt therapy. The systems gained increased usage in European neurosurgical centers due to their dual-regulation mechanism combining adjustable opening pressure and gravitational compensation. This period also saw broader clinical acceptance of anti-siphon technologies in hydrocephalus treatment protocols

- In October 2022, Miethke (B. Braun company) advanced its gravitational shunt technology portfolio with expanded use of its proGAV 2.0 valve system across complex hydrocephalus cases. The device’s improved MRI compatibility and enhanced pressure stability contributed to wider adoption in tertiary neurosurgical hospitals. Clinical studies during this period increasingly focused on reducing shunt failure rates and improving long-term patient outcomes

- In June 2023, Medtronic reinforced its neurosurgical portfolio by supporting increased adoption of programmable CSF shunt systems integrated with improved pressure calibration mechanisms. The Strata platform continued to be widely used in hydrocephalus management due to its non-invasive adjustability and strong clinical outcomes data. Hospitals globally emphasized programmable valve systems as a standard of care in managing both normal pressure hydrocephalus and pediatric cases

- In September 2023, Integra LifeSciences expanded clinical utilization of its Codman Hakim programmable shunt system with increased emphasis on MRI safety improvements and long-term implant reliability. Neurosurgical centers adopted standardized hydrocephalus treatment protocols incorporating programmable VP shunts to reduce revision surgeries and improve cerebrospinal fluid regulation accuracy

- In April 2024, B. Braun and Miethke continued strengthening adoption of gravitational-assisted VP shunt technologies across Europe and Asia-Pacific markets. The proGAV and proSA systems were increasingly used in combination for complex hydrocephalus management cases, especially in patients requiring dynamic pressure adaptation. This period also saw rising clinical focus on minimizing overdrainage and improving patient quality-of-life outcomes

- In November 2024, academic and clinical neurosurgery centers across Europe and North America expanded research into next-generation smart hydrocephalus shunt systems, focusing on integrating pressure sensors and digital monitoring capabilities. Early-stage experimental systems aimed to provide real-time intracranial pressure feedback, marking a shift toward connected neurosurgical implants and predictive post-operative care

- In March 2025, the hydrocephalus shunt market continued its transition toward digitally assisted neurosurgical care systems, with research institutions and medical device manufacturers exploring AI-supported monitoring and programmable valve optimization. Although still largely in clinical research phases, these developments indicate a long-term shift toward smart, data-driven cerebrospinal fluid management solutions aimed at reducing complications and improving surgical precision

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.