Global Vertiports Market

Market Size in USD Million

USD

630.00 Million

USD

17,300.23 Million

2024

2032

USD

630.00 Million

USD

17,300.23 Million

2024

2032

| 2025 - 2032 | |

| USD 630.00 Million | |

| USD 17,300.23 Million | |

| % | |

|

Vertiports Market Size

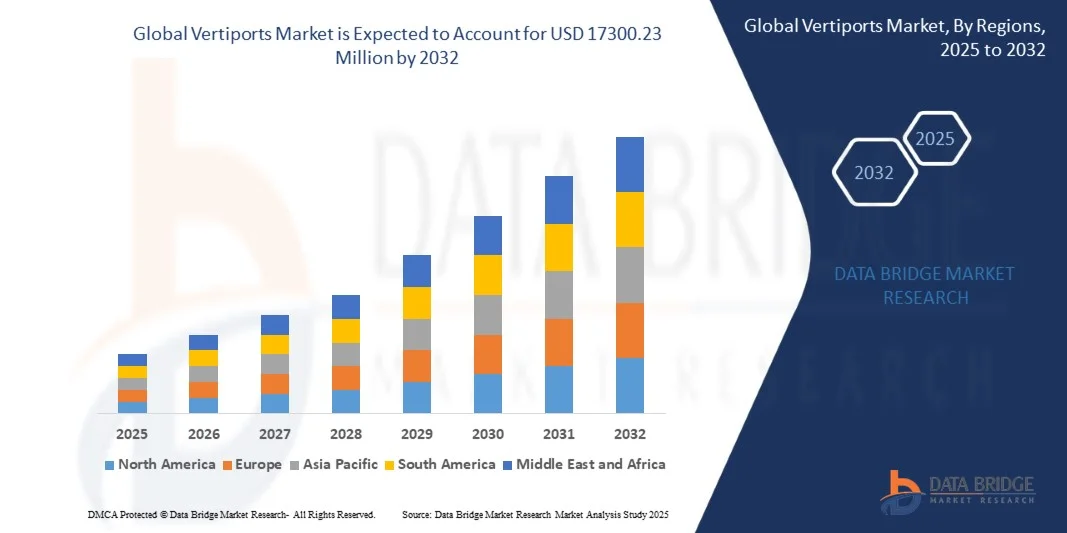

- The global vertiports market size was valued at USD 630 million in 2024 and is expected to reach USD 17300.23 million by 2032, at a CAGR of 51.30% during the forecast period

- The vertiports market growth is largely fueled by the increasing development and deployment of urban air mobility (UAM) solutions, which are driving demand for dedicated infrastructure to support electric vertical take-off and landing (eVTOL) aircraft operations in urban and regional areas

- Furthermore, rising investments from both private and government stakeholders in smart transportation, sustainability initiatives, and air traffic management systems are accelerating the establishment of vertiports, thereby significantly boosting the industry's growth

Vertiports Market Analysis

- Vertiports are specialized facilities designed to support eVTOL aircraft operations, including take-off, landing, charging, maintenance, and passenger handling. These infrastructures integrate advanced air traffic control and ground support systems, enabling safe, efficient, and scalable urban air mobility operations

- The escalating demand for vertiports is primarily fueled by the rapid adoption of eVTOL aircraft, growing urban congestion challenges, and a global push toward sustainable and time-efficient transportation solutions

- North America dominated the vertiports market in 2024, due to early adoption of urban air mobility (UAM) solutions, supportive regulatory frameworks, and significant investments in infrastructure

- Asia-Pacific is expected to be the fastest growing region in the vertiports market during the forecast period due to rapid urbanization, rising disposable incomes, and increasing government focus on smart city and UAM initiatives in countries such as China, Japan, and India

- Urban vertiports segment dominated the market with a market share of 53.5% in 2024, due to the high concentration of population, business districts, and transportation hubs in cities. Urban vertiports cater to dense passenger demand, integrate with mass transit systems, and facilitate first- and last-mile connectivity, making them a core focus for urban air mobility planners. The growing need for congestion reduction, coupled with supportive regulatory frameworks in major cities, further strengthens their market position

Report Scope and Vertiports Market Segmentation

|

Attributes |

Vertiports Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Vertiports Market Trends

“Rising Use of eVTOL Aircraft for Urban Air Mobility”

- A significant trend driving the vertiports market is the increasing use of electric vertical take-off and landing (eVTOL) aircraft for urban air mobility, as cities explore new solutions to address congestion and sustainability challenges. Vertiports are emerging as critical infrastructure to support these aircraft, offering safe, efficient, and dedicated hubs for passenger boarding and cargo transfers within urban and suburban areas

- For instance, Lilium has partnered with Ferrovial to develop a network of vertiports across Europe, designed to accommodate eVTOL jets for intercity and urban routes. Similarly, Archer Aviation and United Airlines have announced plans to establish vertiport facilities in major U.S. cities, showcasing how collaborations between eVTOL manufacturers and transport companies are shaping the urban mobility ecosystem

- The push for zero-emission, electrically powered air taxis is accelerating demand for vertiports equipped with advanced charging and maintenance facilities. These hubs must handle frequent take-offs and landings and also serve as energy distribution points, enabling fast charging and operational turnaround for high-frequency flights

- Urban planners and smart city developers are integrating vertiports into transport networks in alignment with multimodal connectivity. By linking eVTOL hubs to railways, airports, and bus systems, cities aim to create seamless transport nodes that enhance commuter efficiency and reduce reliance on conventional vehicles

- The growing role of vertiports is also reshaping airport infrastructure, as major airports explore dedicated areas to integrate eVTOL operations alongside conventional flights. Such modifications allow for greater flexibility in handling passenger volumes and help maintain aviation competitiveness under evolving travel patterns

- The deployment of vertiports designed for eVTOL mobility represents a transformative shift in transportation, firmly establishing them as foundational infrastructure for the future of urban and regional connectivity. Their widespread adoption underscores the convergence of sustainable aviation technologies, smart city initiatives, and consumer demand for faster and greener transport solutions

Vertiports Market Dynamics

Driver

“Investments in Smart and Sustainable Transport Infrastructure”

- The global push toward smart, connected, and sustainable transportation is driving increased investments into vertiport facilities, as governments and private stakeholders prioritize carbon-neutral solutions for future mobility. The focus on reducing emissions and creating faster travel alternatives aligns well with the development of vertiport networks to complement existing urban transport systems

- For instance, Ferrovial announced investments exceeding USD 1 billion to develop a network of vertiports across key U.S. and European cities, in partnership with eVTOL manufacturers such as Lilium and Vertical Aerospace. These investments highlight how large-scale funding is supporting the establishment of vertiport infrastructure at a commercial scale

- The integration of renewable energy into vertiport development, such as solar panels and energy storage systems, further enhances sustainability goals. Designers are including green roofs, modular construction methods, and energy-efficient facilities to ensure compliance with smart city and environmental policies

- Governments and public agencies are actively supporting vertiport infrastructure through pilot projects, grants, and urban transport innovation programs. Such initiatives complement investments from private stakeholders, ensuring funding pools are diversified to accelerate the rollout of operational networks

- As the transition towards next-generation transport becomes more urgent, sustained investments in smart and sustainable vertiport facilities will be a decisive driver. These developments are critical for scaling eVTOL operations and enabling their integration into wider city and regional transit ecosystems worldwide

Restraint/Challenge

“High Costs and Regulatory Barriers for Vertiport Development”

- The development of vertiports faces significant challenges related to high infrastructure costs and regulatory complexity. Building advanced landing facilities with safety compliance, energy distribution, and connectivity features requires considerable upfront investment, which acts as a barrier for both public agencies and private developers

- For instance, Skyports Infrastructure has reported substantial cost challenges in developing vertiport test facilities in London and Singapore, reflecting the scale of financial and regulatory hurdles in bringing such projects to operational readiness. These difficulties underscore the reliance on stable funding models and favorable policies to ensure long-term viability

- Regulatory frameworks for urban air mobility remain under development in many regions, complicating the approval and certification of vertiport facilities. Aviation authorities such as the FAA and EASA are still defining safety standards for air taxi corridors, charging systems, and passenger handling, delaying large-scale deployment

- Land acquisition and zoning approvals add to the barriers, as suitable locations for vertiports within crowded urban environments are limited and subject to competing commercial uses. Negotiating urban layouts while ensuring connectivity with other transit modes requires careful urban planning and extended approval timelines

- To overcome these barriers, coordinated efforts between private companies, government agencies, and aviation regulators are necessary to reduce costs and streamline approvals. The long-term success of vertiport networks will rely on effective regulatory clarity, collaborative funding initiatives, and design innovations that balance safety, affordability, and scalability for widespread adoption

Vertiports Market Scope

The market is segmented on the basis of solution, location, type, landscape, and topology.

• By Solution

On the basis of solution, the vertiports market is segmented into terminal gates, landing pads, ground support equipment, charging stations, ground control stations, and others. The terminal gates segment dominated the market in 2024, capturing the largest revenue share due to their critical role in passenger handling, boarding management, and integration with urban air mobility operations. Terminal gates are essential for ensuring efficient passenger flow and providing robust safety and operational protocols, making them a central investment focus for vertiport developers. Their capacity to support high-frequency eVTOL operations and seamless integration with ground transport systems further drives demand.

The landing pads segment is expected to witness the fastest growth rate from 2025 to 2032, propelled by the rapid expansion of eVTOL fleets and increased deployment in urban and regional hubs. Landing pads are crucial for safe takeoffs and landings, particularly in congested cityscapes, and their modular design allows for scalable deployment across diverse locations. Technological advancements in automated landing systems and safety monitoring also enhance the attractiveness of this segment to vertiport operators.

• By Location

On the basis of location, the vertiports market is segmented into ground-based, rooftop/elevated, and floating. The ground-based segment dominated the market in 2024, driven by its lower construction complexity and cost-effectiveness compared with elevated or floating vertiports. Ground-based vertiports offer easy accessibility for passengers, vehicles, and support services, making them suitable for high-traffic urban and suburban locations. Their ability to accommodate larger fleets and integrate with existing transport infrastructure further reinforces their market dominance.

Rooftop/elevated vertiports are projected to witness the fastest growth from 2025 to 2032, fueled by increasing urban density and the need to optimize airspace usage. Elevated vertiports maximize space efficiency in city centers, reduce land acquisition challenges, and provide direct connectivity to commercial and residential buildings. Advances in structural design, safety protocols, and vertiport automation make rooftop installations increasingly viable and attractive for eVTOL operations.

• By Type

On the basis of type, the vertiports market is segmented into vertihubs, vertibases, and vertipads. Vertihubs dominated the market in 2024, accounting for the largest revenue share due to their comprehensive infrastructure, which supports passenger terminals, vehicle maintenance, charging stations, and integrated ground transport links. These hubs act as central nodes for urban air mobility networks, enabling efficient scheduling, fleet management, and passenger services. Their multifunctionality and ability to handle high-capacity operations make vertihubs a critical investment for city planners and eVTOL operators.

Vertibases are expected to witness the fastest growth from 2025 to 2032, driven by demand for distributed, smaller-scale operations supporting short-haul routes. Vertibases provide flexible landing and takeoff options, require lower capital expenditure, and can be rapidly deployed in suburban and regional locations. Their strategic importance in enabling feeder services to major hubs and supporting localized air mobility expansion underpins their rapid adoption.

• By Landscape

On the basis of landscape, the vertiports market is segmented into urban vertiports and regional vertiports. Urban vertiports dominated the market in 2024, holding the largest revenue share of 53.5% due to the high concentration of population, business districts, and transportation hubs in cities. Urban vertiports cater to dense passenger demand, integrate with mass transit systems, and facilitate first- and last-mile connectivity, making them a core focus for urban air mobility planners. The growing need for congestion reduction, coupled with supportive regulatory frameworks in major cities, further strengthens their market position.

Regional vertiports are anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing interest in intercity eVTOL services and the expansion of tourism and cargo operations in suburban and less densely populated areas. Regional vertiports bridge city hubs with peripheral locations, enabling longer routes and enhancing network reach. Their comparatively lower land costs and scalable infrastructure options contribute to accelerated market adoption.

• By Topology

On the basis of topology, the vertiports market is segmented into single, linear, satellite, and pier configurations. The single configuration segment dominated the market in 2024, driven by its simplicity, lower construction costs, and ease of operational management. Single topologies are widely deployed in initial urban air mobility projects and provide a straightforward solution for takeoff, landing, and charging operations without complex layouts. Their adaptability and minimal spatial footprint make them the preferred choice for early-stage vertiport developments.

The linear configuration segment is expected to witness the fastest growth from 2025 to 2032, fueled by the expansion of vertiport networks along urban corridors and transport arteries. Linear topologies facilitate sequential landing and takeoff operations, maximize throughput, and integrate effectively with automated traffic management systems. Their operational efficiency and compatibility with growing fleet sizes make them increasingly attractive for urban air mobility operators.

Vertiports Market Regional Analysis

- North America dominated the vertiports market with the largest revenue share in 2024, driven by early adoption of urban air mobility (UAM) solutions, supportive regulatory frameworks, and significant investments in infrastructure

- The U.S. and Canada are leading the deployment of eVTOL operations, with a focus on integrating vertiports into existing transportation networks. The region’s technologically advanced population, high disposable incomes, and emphasis on smart city initiatives further support vertiport adoption

- In addition, partnerships between government bodies and private operators are accelerating the development of UAM ecosystems, establishing North America as a key hub for vertiport growth

U.S. Vertiports Market Insight

The U.S. vertiports market captured the largest revenue share in North America in 2024, fueled by rapid urbanization, growing demand for efficient urban mobility solutions, and early-stage commercialization of eVTOL aircraft. Public-private collaborations, advanced air traffic management systems, and government-backed pilot projects are driving the deployment of terminal gates, landing pads, and charging stations. The increasing focus on reducing urban congestion and carbon emissions, coupled with investments in smart vertiport infrastructure, is further propelling market growth.

Europe Vertiports Market Insight

The Europe vertiports market is projected to expand at a significant CAGR during the forecast period, primarily driven by government initiatives promoting sustainable mobility, urban congestion challenges, and increasing investments in eVTOL infrastructure. Countries such as Germany, France, and the U.K. are focusing on integrating vertiports into public transport hubs and city centers. Rising urbanization, technological adoption, and demand for eco-friendly transport solutions are fostering market growth. European operators are prioritizing vertiport designs that optimize safety, accessibility, and passenger throughput.

U.K. Vertiports Market Insight

The U.K. vertiports market is expected to grow at a notable CAGR over the forecast period, driven by increasing urban congestion and government support for urban air mobility initiatives. The trend of integrating vertiports with transportation networks in cities such as London, Manchester, and Birmingham is encouraging the adoption of UAM infrastructure. Technological advancements in eVTOL operations, combined with growing interest from logistics, passenger transport, and emergency response services, are further accelerating market development in the region.

Germany Vertiports Market Insight

The Germany vertiports market is anticipated to expand at a considerable CAGR during the forecast period, fueled by the country’s strong focus on technological innovation, environmental sustainability, and urban mobility modernization. Investments in smart city projects, eVTOL test programs, and regulatory support for UAM infrastructure promote the deployment of vertihubs, vertibases, and landing pads. The integration of vertiports with multi-modal transport hubs, emphasis on safety standards, and adoption of automated management systems are key factors driving growth in Germany.

Asia-Pacific Vertiports Market Insight

The Asia-Pacific vertiports market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by rapid urbanization, rising disposable incomes, and increasing government focus on smart city and UAM initiatives in countries such as China, Japan, and India. The expansion of regional and urban vertiports, combined with the growing domestic manufacturing of eVTOL aircraft, supports accessibility and affordability. Rising interest in air taxi services, emergency medical transport, and logistics solutions further contributes to market adoption.

Japan Vertiports Market Insight

The Japan vertiports market is gaining momentum due to the country’s advanced technological ecosystem, high urban density, and demand for efficient, safe, and automated transport solutions. Growth is driven by eVTOL integration into smart cities, the development of rooftop and elevated vertiports, and government-supported pilot programs. The focus on passenger convenience, real-time monitoring systems, and safety compliance encourages both commercial and residential adoption. Aging populations and urban mobility challenges are also accelerating demand for easily accessible vertiports.

China Vertiports Market Insight

The China vertiports market accounted for the largest revenue share in Asia-Pacific in 2024, driven by strong government support for smart city and urban air mobility projects, rapid urbanization, and the growing eVTOL ecosystem. Large-scale investments in terminal gates, charging stations, and landing pads are facilitating the rollout of vertiport infrastructure across metropolitan and regional cities. The availability of domestic eVTOL manufacturers, coupled with increasing consumer and commercial adoption of urban air mobility solutions, is propelling market growth.

Vertiports Market Share

The vertiports industry is primarily led by well-established companies, including:

- Skyports Limited (U.K.)

- Urban-Air Port Ltd. (U.K.)

- Volocopter (Germany)

- Lilium GmbH (Germany)

- NEOM (Saudi Arabia)

- Ferrovial (Netherlands)

- Groupe ADP (France)

- Hyundai Motor Group (South Korea)

- ARUP (U.K.)

- Eve Air Mobility (Brazil)

- Joby Aviation (U.S.)

- Archer Aviation (U.S.)

Latest Developments in Vertiports Market

- In June 2023, Groupe ADP signed a Memorandum of Understanding (MoU) with AutoFlight to test Prosperity 1 eVTOL flights at Pontoise Airport during the Paris Olympic Games 2024. This initiative is poised to significantly advance the European vertiports market by demonstrating operational feasibility and building early consumer awareness. By developing five new vertiports in the Paris region, Groupe ADP is setting a benchmark for urban air mobility infrastructure, which is likely to stimulate investments, accelerate adoption, and enhance the overall eVTOL ecosystem in the region

- In June 2023, UrbanV S.p.A. and Lilium partnered to advance infrastructure for Advanced Air Mobility (AAM), focusing on the construction of vertiport networks to support Lilium aircraft and clients. This collaboration is expected to strengthen the regional vertiports market in Italy and the French Riviera by enabling commercial eVTOL operations. The strategic development of vertiports facilitates scalable network deployment, improves operational efficiency, and encourages other operators to invest in similar infrastructure, thereby expanding market reach and adoption potential

- In June 2023, Lilium and UrbanV S.p.A. joined forces for the advancement of AAM infrastructure, with an emphasis on creating vertiport networks to support Lilium aircraft and clients in Italy and the French Riviera. The partnership is projected to positively impact the European vertiports market by accelerating the operational readiness of eVTOL services, demonstrating practical commercial applications, and providing a model for integrated urban and regional air mobility solutions. This initiative may also drive further investments in related vertiport and eVTOL infrastructure across other potential markets

- In March 2023, Ferrovial and Eve Air Mobility collaborated to ensure the safe and reliable operation of vertiports and eVTOLs. The deployment of Eve Air Mobility’s software to enable communication between vertiports and aircraft is expected to enhance operational efficiency and safety standards in the vertiports market. This partnership underscores the importance of integrated software solutions for eVTOL management, positioning the European vertiports market for scalable, automated operations and boosting investor confidence in urban air mobility infrastructure

- In February 2023, Skyports Infrastructure and Dubai’s Road and Transport Authority (RTA) partnered to create a vertiport network in Dubai for a 2026 launch, including proposals for future infrastructure development. With four vertiports planned at Dubai International Airport, Palm Jumeirah, Dubai Downtown, and Dubai Marina, this initiative is expected to significantly strengthen the Middle East vertiports market. It demonstrates a clear commitment to integrating urban air mobility into existing transport networks, enhancing commercial and passenger access, and attracting investments in regional eVTOL services

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.