Global Vinyls Market

Market Size in USD Billion

USD

75.33 Billion

USD

124.20 Billion

2024

2032

USD

75.33 Billion

USD

124.20 Billion

2024

2032

| 2025 - 2032 | |

| USD 75.33 Billion | |

| USD 124.20 Billion | |

| % | |

|

Vinyls Market Size

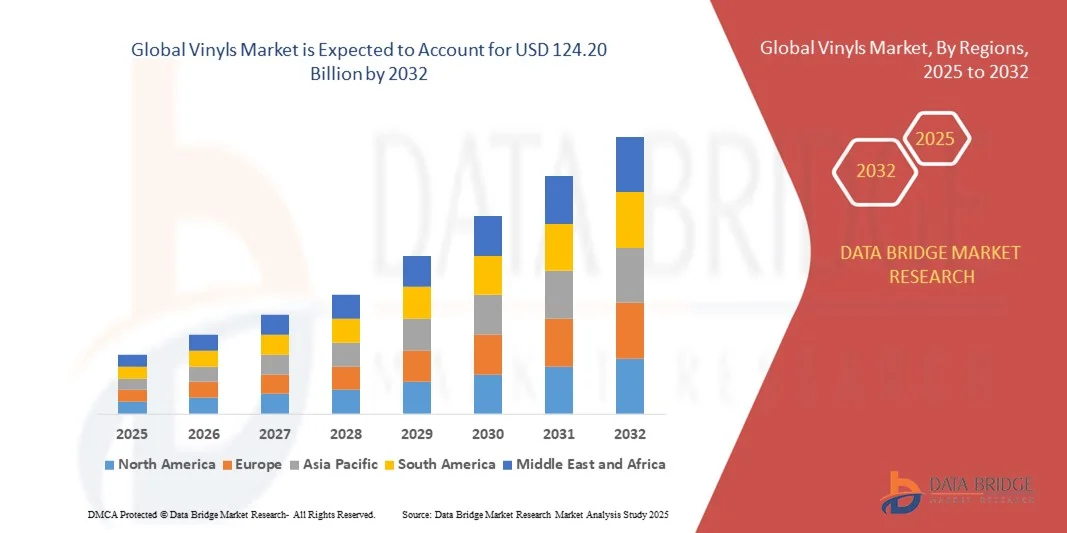

- The global vinyls market size was valued at USD 75.33 billion in 2024 and is expected to reach USD 124.20 billion by 2032, at a CAGR of 6.45% during the forecast period

- The market growth is largely fuelled by the rising demand for vinyl-based products in construction, automotive, packaging, and consumer goods, owing to their durability, cost-effectiveness, and versatility

- Increasing industrialization, urbanization, and infrastructure development in emerging economies are further driving the adoption of vinyl products across multiple end-use sectors

Vinyls Market Analysis

- Rising awareness of environmentally friendly and recyclable vinyl materials is encouraging manufacturers to innovate and meet regulatory standards, enhancing market acceptance globally

- The expansion of end-use industries, including building & construction, automotive, and electronics, is fueling demand for specialty vinyls with improved properties such as flame retardancy, chemical resistance, and flexibility

- North America dominated the vinyls market with the largest revenue share of 38.5% in 2024, driven by increasing demand for construction materials, automotive components, and packaging solutions, as well as rising awareness of durable and lightweight materials

- Asia-Pacific region is expected to witness the highest growth rate in the global vinyls market, driven by increasing construction activities, expanding automotive sectors, and rising packaging requirements in countries such as China, India, and Japan. Technological advancements, coupled with government initiatives promoting industrial growth and urban development, are accelerating adoption

- The Vinyl Chloride segment held the largest market revenue share in 2024, driven by its extensive use in construction materials, pipes, and packaging solutions. Vinyl Chloride offers excellent durability, chemical resistance, and cost-effectiveness, making it a preferred choice across multiple industrial applications

Report Scope and Vinyls Market Segmentation

|

Attributes |

Vinyls Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Vinyls Market Trends

Increasing Adoption of Vinyls Across Construction, Automotive, and Packaging Industries

- The growing utilization of vinyls in construction materials, automotive components, and packaging solutions is transforming the market by enhancing durability, flexibility, and cost-efficiency. Vinyls’ resistance to moisture, chemicals, and UV exposure is driving widespread adoption across end-use sectors. Furthermore, innovations in vinyl formulations are enabling tailored applications for specialty construction projects, automotive interiors, and industrial packaging, reinforcing their versatility

- Rising demand for lightweight and versatile materials in emerging economies is accelerating market growth, particularly where rapid urbanization and industrialization drive the need for efficient building and packaging solutions. Manufacturers are integrating vinyls to meet functional and aesthetic requirements. In addition, the growing trend of prefabricated and modular construction methods is further fueling vinyl adoption due to its ease of handling and cost-effectiveness

- The ease of processing, recyclability, and compatibility with composite materials makes vinyls attractive for routine industrial applications, providing cost-effective performance enhancement without compromising quality. Vinyls are increasingly used in pipes, flooring, and flexible packaging products. Enhanced formulations that combine vinyls with additives for flame retardancy, UV protection, or color stability are driving greater adoption across diverse industrial segments

- For instance, in 2023, several European and North American construction and packaging companies reported improved product performance and consumer satisfaction after switching to high-grade vinyls, highlighting its impact on market differentiation and growth. The adoption of these high-quality materials also helped manufacturers reduce maintenance costs and extend product lifecycle, reinforcing the economic advantages for end users

- While vinyl adoption is increasing across industries, market expansion depends on continued innovation, regulatory compliance, and sustainable sourcing. Companies must focus on high-quality formulations, environmental standards, and optimized manufacturing processes to fully capitalize on demand. The push for eco-friendly and recyclable vinyl solutions is expected to create new market opportunities while aligning with global sustainability initiatives

Vinyls Market Dynamics

Driver

Rising Demand for Durable, Lightweight, and Cost-Effective Materials

- Increasing demand for flexible and robust construction materials, such as flooring, window frames, and pipes, is driving the adoption of vinyls. Their long lifespan, low maintenance requirements, and aesthetic versatility boost market uptake. The ability to produce customized shapes and colors enhances design flexibility, making vinyls highly attractive for residential, commercial, and industrial construction projects

- The automotive sector is incorporating vinyl-based materials for interior components, wiring insulation, and lightweight panels, supporting overall market expansion. Vinyls enhance vehicle durability while contributing to fuel efficiency through weight reduction. With the automotive industry focusing on sustainability and cost reduction, vinyl components provide a balance of performance and affordability, leading to increased adoption globally

- Packaging industries are using vinyls for films, wraps, and containers to improve shelf life, hygiene, and product safety. This cross-industry adoption reinforces the market trajectory. In addition, innovations in barrier properties and printable vinyl packaging are enhancing branding and consumer appeal, further accelerating demand in the food, beverage, and consumer goods sectors

- For instance, in 2022, several packaging solution providers in China and India expanded their vinyl-based product lines, significantly increasing adoption among food and consumer goods manufacturers. This expansion also allowed companies to reduce waste and energy consumption during production, highlighting the cost and environmental benefits of using advanced vinyl solutions

- While rising demand and versatile applications are fueling growth, consistent raw material supply, sustainable production, and technological innovation are essential to sustain market expansion. Companies investing in research and development for higher-performance vinyls and greener alternatives are likely to gain a competitive edge in the global market.

Restraint/Challenge

Environmental Concerns and Regulatory Constraints

- Environmental issues related to vinyl production, such as chlorine emissions and plastic waste, have led to stricter regulations, limiting production flexibility in some regions. Manufacturers face increasing pressure to adopt eco-friendly and recyclable alternatives. Public awareness and regulatory oversight are also prompting the industry to invest in cleaner production techniques and circular economy solutions

- The high cost of specialty vinyls for certain applications, such as medical and high-performance automotive components, restricts adoption among smaller manufacturers and emerging markets. Price sensitivity can limit widespread usage. In addition, the complexity of processing these specialty vinyls often requires advanced machinery and skilled labor, further increasing overall production costs

- Supply chain challenges, including raw material availability and logistics, may disrupt consistent vinyl supply, affecting production timelines and market performance. This is compounded by global fluctuations in PVC resin prices and transportation bottlenecks, impacting downstream industries and causing periodic market instability

- For instance, in 2023, several vinyl manufacturers in Europe reported production delays due to PVC resin shortages and transportation bottlenecks, impacting downstream industries and market timelines. Such disruptions also affected product launches, inventory management, and customer satisfaction, highlighting the critical need for resilient supply chains

- While technological advancements in sustainable production and recycling continue, addressing cost, environmental compliance, and supply chain challenges remains crucial. Companies must focus on scalable production, optimized sourcing, and regional regulatory alignment to unlock long-term market potential. Collaborative initiatives between manufacturers, regulators, and recyclers are also expected to create a more sustainable and stable market environment

Vinyls Market Scope

The market is segmented on the basis of types and end-user industries.

- By Types

On the basis of types, the vinyls market is segmented into Vinyl Acetate, Vinyl Alcohol, Vinyl Chloride, and Others. The Vinyl Chloride segment held the largest market revenue share in 2024, driven by its extensive use in construction materials, pipes, and packaging solutions. Vinyl Chloride offers excellent durability, chemical resistance, and cost-effectiveness, making it a preferred choice across multiple industrial applications.

The Vinyl Acetate segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by its versatility in adhesives, coatings, and paints. Vinyl Acetate is particularly favored for its strong bonding properties, ease of processing, and compatibility with composite materials, making it ideal for automotive, construction, and packaging industries.

- By End User Industries

On the basis of end-user industries, the vinyls market is segmented into Automotive, Construction, Electrical, Healthcare, and Others. The Construction segment accounted for the largest revenue share in 2024, driven by rising urbanization, infrastructure development, and the adoption of durable, lightweight, and cost-effective building materials.

The Automotive segment is projected to witness significant growth from 2025 to 2032, owing to the increasing incorporation of vinyl-based components for interiors, wiring insulation, and lightweight panels. Vinyl materials enhance vehicle durability, fuel efficiency, and design flexibility, driving demand across passenger and commercial vehicle manufacturing.

Vinyls Market Regional Analysis

- North America dominated the vinyls market with the largest revenue share of 38.5% in 2024, driven by increasing demand for construction materials, automotive components, and packaging solutions, as well as rising awareness of durable and lightweight materials

- Consumers and manufacturers in the region highly value the versatility, cost-efficiency, and performance benefits offered by vinyls, including resistance to moisture, chemicals, and UV exposure

- This widespread adoption is further supported by high industrialization, strong R&D capabilities, and a technologically advanced manufacturing base, establishing vinyls as a preferred material across multiple end-use industries

U.S. Vinyls Market Insight

The U.S. vinyls market captured the largest revenue share in North America in 2024, fueled by growing construction activity, automotive production, and packaging demand. The adoption of vinyl-based materials for lightweight and durable solutions in residential, commercial, and industrial applications continues to expand. Moreover, increasing integration of vinyl composites in automotive interiors, flexible packaging, and pipes enhances market growth. Environmental compliance and sustainable production practices are also shaping market strategies.

Europe Vinyls Market Insight

The Europe vinyls market is projected to witness significant growth from 2025 to 2032, driven by strict regulations on material performance and safety, coupled with rising demand for sustainable and durable solutions. Urbanization, construction activity, and automotive production are key factors fostering adoption. European manufacturers are increasingly using vinyls in packaging, flooring, and automotive components due to their cost-efficiency and recyclability. The market is seeing significant growth in both renovation and new-build projects.

U.K. Vinyls Market Insight

The U.K. vinyls market is projected to witness significant growth from 2025 to 2032, propelled by increased use in construction, automotive interiors, and industrial applications. Concerns regarding material longevity, maintenance costs, and energy-efficient solutions are encouraging adoption. The U.K.’s established manufacturing sector, along with e-commerce and distribution networks, supports broader market penetration.

Germany Vinyls Market Insight

The Germany vinyls market is projected to witness significant growth from 2025 to 2032, fueled by the country’s focus on high-performance materials and eco-conscious production. Germany’s industrial infrastructure, technological advancement, and emphasis on sustainability promote the adoption of vinyls in construction, automotive, and electrical applications. Integration with composite materials and innovation in manufacturing processes further drives growth.

Asia-Pacific Vinyls Market Insight

The Asia-Pacific vinyls market is projected to witness significant growth from 2025 to 2032, driven by rapid urbanization, industrialization, and rising demand for lightweight and durable materials in countries such as China, India, and Japan. Government initiatives supporting infrastructure development, smart construction, and manufacturing modernization are boosting market adoption. The region’s expanding middle class and growing packaging and automotive industries further propel vinyl consumption.

Japan Vinyls Market Insight

The Japan vinyls market is projected to witness significant growth from 2025 to 2032 due to high technological adoption, advanced manufacturing capabilities, and increasing demand for durable, lightweight, and eco-friendly materials. The integration of vinyls in automotive interiors, electronic housings, and construction materials is accelerating growth. Moreover, an aging population and industrial focus on efficiency are encouraging adoption in specialized applications.

China Vinyls Market Insight

The China vinyls market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, industrial expansion, and strong manufacturing capabilities. Vinyls are widely used in construction, automotive, packaging, and electrical applications. The government’s push towards smart cities, coupled with domestic production of vinyl components, makes China a key driver of the global vinyls market.

Vinyls Market Share

The Vinyls industry is primarily led by well-established companies, including:

- GZ VINYL (China)

- Dublin Vinyl (Ireland)

- Vinyl Chemicals (India) Ltd. (India)

- Dow (U.S.)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Wacker Chemie AG (Germany)

- LG Chem. (South Korea)

- Central Drug House (India)

- DCM Shriram (India)

- MarvelVinyls (India)

- Emerald Performance Materials (U.S.)

- Royal Dutch Shell plc (Netherlands)

- Occidental Petroleum Corporation (U.S.)

- Qatar Petrochemical Company (QAPCO) (Qatar)

- Q.P.J.S.C. (Saudi Arabia)

- M. Holland Company (U.S.)

- Teknor Apex (U.S.)

- IndianPetroChem.com (India)

- Crystal Quinone PVT LTD (India)

- A. Schulman, Inc. (U.S.)

- Exxon Mobil Corporation (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Vinyls Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Vinyls Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Vinyls Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.