Global Viral Conjunctivitis Market

Market Size in USD Million

USD

364.65 Million

USD

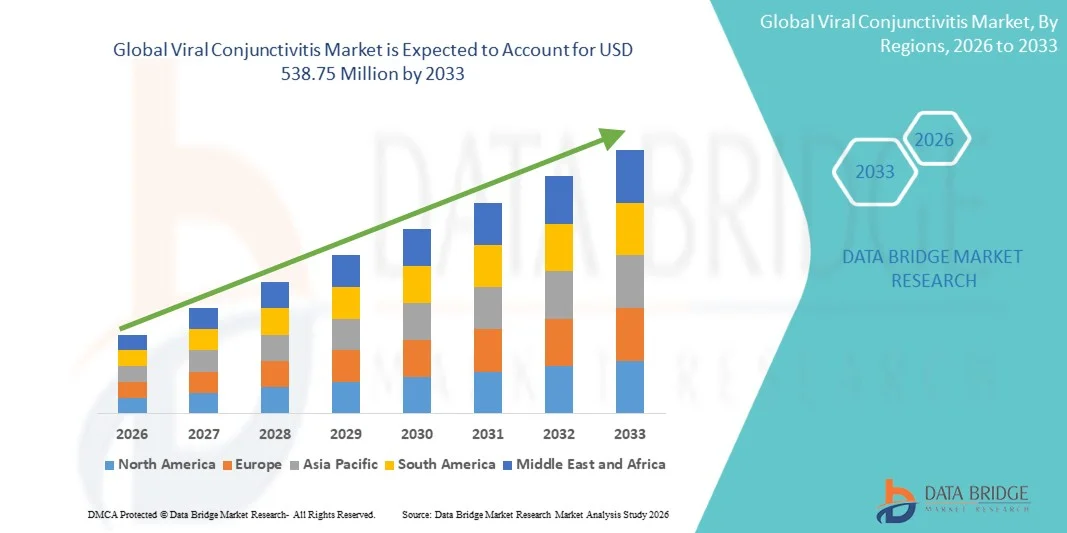

538.75 Million

2025

2033

USD

364.65 Million

USD

538.75 Million

2025

2033

| 2026 - 2033 | |

| USD 364.65 Million | |

| USD 538.75 Million | |

| % | |

|

Viral Conjunctivitis Market Size

- The global viral conjunctivitis market size was valued at USD 364.65 Million in 2025 and is expected to reach USD 538.75 Million by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of viral conjunctivitis cases worldwide, driven by seasonal outbreaks, higher population density in urban areas, and rising incidence of viral eye infections. Advances in diagnostic methods and treatment options are further supporting market expansion in both clinical and homecare settings

- Furthermore, rising demand for safe, effective, and easy-to-administer therapeutic solutions is positioning viral conjunctivitis treatments as essential interventions in ophthalmology and primary healthcare. These converging factors are accelerating the uptake of viral conjunctivitis solutions, thereby significantly boosting growth in the global viral conjunctivitis market

Viral Conjunctivitis Market Analysis

- Viral conjunctivitis treatments—including antiviral medications, supportive drops, and symptom‑relief therapies—are becoming increasingly essential in modern ophthalmic care due to the high and often seasonal incidence of viral eye infections worldwide. Increased prevalence of adenovirus‑mediated “pink eye” and heightened awareness of contagious ocular conditions are driving demand across clinical and outpatient settings

- The escalating demand for viral conjunctivitis solutions is primarily fueled by rising public health initiatives focused on eye infection management, improved access to healthcare services, and growing patient preference for effective, targeted therapeutic options that alleviate symptoms and reduce transmission

- North America dominated the viral conjunctivitis market with 33.5% of total revenue in 2025, underpinned by advanced healthcare infrastructure, strong public health awareness, and proactive treatment adoption. The U.S. remains the largest single contributor within the region due to robust diagnostic capabilities and high healthcare spending on ophthalmic conditions

- Asia‑Pacific is expected to be the fastest‑growing region during the forecast period, supported by expanding eye care services, increasing healthcare expenditure, and a large patient population seeking accessible treatment options for viral conjunctivitis

- The ocular segment dominated the largest market revenue share of 72% in 2025, driven by the direct application to the eye, fast therapeutic effect, and preference among healthcare providers for targeted treatment

Report Scope and Viral Conjunctivitis Market Segmentation

|

Attributes |

Viral Conjunctivitis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Pfizer (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Viral Conjunctivitis Market Trends

“Rising Prevalence of Viral Eye Infections and Growing Public Awareness”

- A key and accelerating trend in the global viral conjunctivitis market is the increasing prevalence of viral eye infections, including adenoviral and enteroviral conjunctivitis, which continue to affect millions of people worldwide, particularly children and the elderly

- This trend is significantly driving the demand for preventive care and targeted therapeutic interventions

- For instance, WHO reports indicate seasonal outbreaks of adenoviral conjunctivitis in schools and healthcare facilities, prompting governments and health organizations to expand public awareness campaigns and improve diagnostic and treatment accessibility

- Growing patient awareness about the importance of early diagnosis and prompt treatment is leading to higher consultation rates with ophthalmologists and optometrists, thereby expanding the market

- Educational initiatives emphasizing hygiene practices and the avoidance of viral transmission in communities are encouraging proactive preventive behaviors, which are contributing to market growth

- Furthermore, increasing health literacy and access to healthcare services in both developed and emerging regions are enabling patients to seek medical attention promptly, boosting the demand for antiviral therapies and supportive care products

Viral Conjunctivitis Market Dynamics

Driver

“Expanding Healthcare Infrastructure and Access to Ophthalmology Services”

- The expansion of healthcare infrastructure, including specialized eye care centers, clinics, and hospital-based ophthalmology departments, is a major driver for the Viral Conjunctivitis market

- For instance, countries like the U.S., Germany, and Japan have seen substantial increases in ophthalmology outpatient visits and screening programs, providing greater access to diagnosis and treatment of viral conjunctivitis

- Investments in regional healthcare facilities in Asia-Pacific and Latin America are facilitating broader market reach, particularly in semi-urban and rural populations

- Telemedicine services and online consultation platforms are increasingly being adopted, allowing remote patients to access timely care, which further supports market growth

- Rising healthcare expenditure, including insurance coverage for outpatient visits and antiviral prescriptions, is enhancing affordability and increasing patient adherence to treatment regimens

Restraint/Challenge

“High Treatment Costs and Limited Access in Developing Regions”

- Despite growing awareness and technological advancements, high costs of antiviral therapies and specialized eye care can limit adoption, especially in low-income regions. Premium-priced treatments and diagnostic kits may remain inaccessible to large population segments

- For instance, expensive PCR-based diagnostic tools are often unavailable in remote healthcare facilities in parts of Africa and Southeast Asia, restricting timely diagnosis and treatment

- Inconsistent healthcare infrastructure, limited availability of ophthalmologists, and lack of cold-chain or supply chain management for sensitive therapeutic products continue to hinder market expansion

- Vaccine hesitancy, cultural beliefs, and lack of awareness about preventive care for viral infections may further impact adoption rates, even where healthcare services are accessible

- Overcoming these challenges requires investments in affordable therapeutics, regional healthcare expansion, awareness campaigns, and streamlined distribution channels to ensure equitable access to viral conjunctivitis care worldwide

Viral Conjunctivitis Market Scope

The market is segmented on the basis of medication, product type, route of administration, end-users, and distribution channel.

• By Medication

On the basis of medication, the Viral Conjunctivitis market is segmented into lubricating eye drops, vasoconstrictor, analgesic & pain relief, antiviral, and others. The lubricating eye drops segment dominated the largest market revenue share of 39.8% in 2025, driven by their widespread availability, ease of use, and suitability for symptomatic relief of viral conjunctivitis. Hospitals, specialty clinics, and homecare providers frequently recommend lubricating drops. High patient adherence is supported by convenience and minimal side effects. Combination formulations enhance patient compliance. Brand recognition and physician recommendations reinforce adoption. Government healthcare programs and insurance coverage encourage usage. Emerging markets show increasing penetration. Public awareness campaigns highlight preventive care and early symptom management. Multiple dosage forms enhance versatility. Continuous R&D improves formulation stability. Distribution through pharmacies ensures accessibility. Patient trust and routine use sustain market dominance.

The antiviral segment is expected to witness the fastest CAGR of 11.6% from 2026 to 2033, fueled by rising prevalence of viral conjunctivitis, technological advancements in antiviral formulations, and growing awareness of treatment benefits. Hospitals and specialty clinics expand antiviral usage. Homecare adoption is increasing due to patient preference for convenient treatments. Emerging markets show strong uptake. Physician recommendation and digital health platforms boost adoption. E-commerce and online pharmacy availability improve accessibility. Combination therapies enhance efficacy. Public health campaigns drive awareness. Safety and tolerability improvements reinforce trust. Insurance coverage and reimbursement support faster adoption. Market penetration is accelerated by increasing patient education and adherence.

• By Product Type

On the basis of product type, the market is segmented into eye drops, eye ointment, liquid wipes, gel, and others. The eye drops segment dominated the largest market revenue share of 46.2% in 2025, driven by ease of administration, fast symptom relief, and broad availability in hospitals, specialty clinics, and homecare settings. Patient compliance is high due to comfort and convenience. Brand loyalty and physician preference reinforce adoption. Combination drops increase therapeutic efficiency. Emerging markets show strong growth in eye drop usage. Regulatory approvals ensure safety and quality. Marketing campaigns improve visibility. Digital health platforms promote adherence. Retail and hospital pharmacies stock eye drops extensively. Pediatric and adult patient segments support usage. Continuous formulation improvements sustain leadership.

The eye ointment segment is expected to witness the fastest CAGR of 10.9% from 2026 to 2033, driven by growing demand for long-lasting protection and adherence-friendly formulations. Hospitals, specialty clinics, and homecare providers expand adoption. Emerging markets show increasing uptake. Physician recommendation supports use. Digital health awareness campaigns encourage patient adherence. Combination ointments improve treatment efficiency. Convenience and effectiveness sustain growth. Marketing and visibility campaigns enhance awareness. Insurance coverage supports adoption. Supply through online pharmacies and retail channels improves access. Technological advancements in consistency and absorption boost preference. Patient satisfaction reinforces repeat use.

• By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, ocular, and others. The ocular segment dominated the largest market revenue share of 72% in 2025, driven by the direct application to the eye, fast therapeutic effect, and preference among healthcare providers for targeted treatment. Hospitals and specialty clinics widely administer ocular products. Homecare adoption is supported by convenience and safety. Regulatory approvals and physician trust reinforce market dominance. Emerging markets are witnessing increased ocular treatment adoption. Combination formulations improve effectiveness. Brand recognition and public awareness campaigns strengthen penetration. Patient compliance is high due to ease of use. Distribution through hospital and retail pharmacies ensures availability. Formulation stability and efficacy drive continued preference.

The oral segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, fueled by growing use of systemic antivirals and supportive medications for viral conjunctivitis. Hospitals and specialty clinics expand oral therapy adoption. Homecare convenience encourages patient preference. Emerging markets show increasing uptake. Physician recommendations and digital platforms boost awareness. Insurance coverage and reimbursement enhance adoption. Combination therapies increase efficacy. E-commerce channels improve accessibility. Safety and tolerability drive adherence. Patient education campaigns reinforce compliance. Market penetration is strengthened by global public health initiatives.

• By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the largest market revenue share of 48% in 2025, driven by institutional treatment programs, physician-administered therapy, and high patient throughput. Specialty clinics and homecare providers support outpatient administration. Public awareness campaigns strengthen adoption. Regulatory approvals and physician trust reinforce dominance. Emerging markets show increasing hospital-driven treatment. Brand recognition enhances patient trust. Supply chain efficiency ensures product availability. Digital scheduling and patient follow-up improve adherence. Combination therapies increase efficiency. Pediatric and adult segments drive adoption. Hospitals continue to be central to treatment delivery.

The homecare segment is expected to witness the fastest CAGR of 12.1% from 2026 to 2033, fueled by convenience, online pharmacy availability, telemedicine support, and patient preference for at-home treatment. Hospitals and specialty clinics show steady growth. Emerging markets show strong adoption. Digital campaigns and physician recommendations boost uptake. E-commerce penetration improves accessibility. Combination therapies enhance treatment convenience. Patient adherence and comfort reinforce growth. Marketing campaigns strengthen visibility. Needle-free and self-administered formulations increase preference. Public health initiatives promote at-home care. Homecare providers expand service offerings to meet rising demand.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 44% in 2025, driven by prescription-based demand, institutional stocking, and integration into hospital treatment programs. Specialty clinics and homecare rely on hospital pharmacy supply. Physician trust and regulatory approvals reinforce dominance. Emerging markets show strong hospital pharmacy adoption. Marketing campaigns and awareness programs improve visibility.

The online pharmacy segment is expected to witness the fastest CAGR of 12.3% from 2026 to 2033, driven by e-commerce penetration, doorstep delivery, digital marketing, and convenience. Retail and hospital pharmacies show steady growth. Consumer awareness, smartphone adoption, and online consultations accelerate adoption. Emerging markets show strong uptake. Convenience and accessibility sustain faster growth. Marketing campaigns strengthen visibility. Increasing trust in online purchases further drives adoption. Expansion of digital healthcare platforms supports long-term growth. Growth is reinforced by patient preference for home delivery and 24/7 access.

Viral Conjunctivitis Market Regional Analysis

- North America dominated the viral conjunctivitis market with the largest revenue share of 33.5% in 2025, underpinned by advanced healthcare infrastructure, strong public health awareness, and proactive treatment adoption

- The U.S. remains the largest single contributor within the region due to robust diagnostic capabilities and high healthcare spending on ophthalmic conditions

- Widespread access to eye care specialists, diagnostic laboratories, and pharmacies, combined with patient education initiatives, supports high adoption of antiviral therapies and preventive measures

U.S. Viral Conjunctivitis Market Insight

The U.S. viral conjunctivitis market accounted for the majority of North America’s revenue in 2025, driven by widespread clinical adoption of rapid diagnostic tests, antiviral eye drops, and supportive therapies. The country benefits from strong insurance coverage for ophthalmic conditions, well-established outpatient care, and advanced hospital networks, which collectively ensure early detection and treatment. Increasing patient awareness about the complications of untreated viral conjunctivitis, coupled with proactive public health campaigns, further stimulates market growth.

Europe Viral Conjunctivitis Market Insight

The Europe viral conjunctivitis market is projected to expand at a moderate CAGR during the forecast period, driven by increasing awareness of ocular hygiene and access to healthcare services. Rising urbanization, coupled with improved diagnostic infrastructure in countries such as Germany, France, and Italy, supports timely treatment. Public health initiatives and routine eye examinations are encouraging early diagnosis and treatment, particularly in schools and workplaces, contributing to steady market growth across both residential and institutional care settings.

U.K. Viral Conjunctivitis Market Insight

The U.K. viral conjunctivitis market is expected to grow at a notable CAGR during the forecast period, fueled by enhanced public awareness campaigns and preventive eye care programs. Increased visits to ophthalmologists and optometrists, combined with government-supported vaccination and hygiene programs, are promoting early detection and effective management. The adoption of antiviral treatments and over-the-counter supportive therapies continues to rise, reflecting a growing focus on eye health and preventive care.

Germany Viral Conjunctivitis Market Insight

The Germany viral conjunctivitis market is projected to grow steadily over the forecast period, supported by well-developed healthcare infrastructure, high patient literacy, and government initiatives promoting preventive eye care. The availability of advanced diagnostic laboratories and hospital networks allows for prompt identification and treatment of viral conjunctivitis. Rising public awareness and access to antiviral therapies and supportive medications contribute to increasing market penetration, particularly in urban and semi-urban populations.

Asia-Pacific Viral Conjunctivitis Market Insight

The Asia-Pacific viral conjunctivitis market is expected to grow at the fastest CAGR during the forecast period, driven by expanding eye care services, increasing healthcare expenditure, and a large patient population seeking accessible treatment options. Rapid urbanization, growing public awareness of eye health, and government initiatives aimed at improving healthcare infrastructure are fueling demand. Countries such as China, India, and Japan are witnessing increased hospital visits, improved diagnostic capabilities, and wider availability of antiviral treatments, contributing to robust regional market growth.

Japan Viral Conjunctivitis Market Insight

The Japan viral conjunctivitis market is gaining momentum due to the country’s aging population, high healthcare standards, and emphasis on preventive care. A strong network of ophthalmologists, advanced diagnostic facilities, and patient education campaigns are driving early detection and treatment adoption. Rising demand for antiviral eye drops and supportive therapies, coupled with government initiatives to manage viral outbreaks, is positively influencing market expansion.

China Viral Conjunctivitis Market Insight

The China viral conjunctivitis market accounted for the largest share in Asia-Pacific in 2025, driven by rising urbanization, a growing middle-class population, and expanding healthcare infrastructure. Increasing public awareness of eye health, coupled with improved access to diagnostic services and antiviral therapies, is promoting early treatment adoption. In addition, government programs aimed at enhancing eye care services in both urban and rural areas are facilitating greater market penetration and supporting rapid growth across the region.

Viral Conjunctivitis Market Share

The Viral Conjunctivitis industry is primarily led by well-established companies, including:

• Pfizer (U.S.)

• Novartis (Switzerland)

• Sanofi (France)

• Bausch + Lomb (U.S.)

• GSK (U.K.)

• Johnson & Johnson (U.S.)

• Santen Pharmaceutical (Japan)

• Dr. Reddy’s Laboratories (India)

• Cipla (India)

• Sun Pharma (India)

• HRA Pharma (France)

• Glenmark Pharmaceuticals (India)

• Fresenius Kabi (Germany)

• Beiersdorf (Germany)

• Shire Pharmaceuticals (Ireland)

• Amorepacific Corporation (South Korea)

• Abbott Laboratories (U.S.)

• Hoffmann-La Roche (Switzerland)

• Mylan (U.S.)

Latest Developments in Global Viral Conjunctivitis Market

- In April 2021, Okogen, Inc. announced interim analysis results from its Phase 2 RUBY clinical trial showing that its investigational antiviral candidate OKG‑0301 was safe and demonstrated a dose‑dependent antiviral effect in patients with acute adenoviral (viral) conjunctivitis, reported in a clinical press release and presented at the Association for Research in Vision and Ophthalmology conference, marking a key step in the development of a potential first‑in‑class therapy for adenoviral conjunctivitis

- In October 2023, Okogen, Inc. initiated a Phase 2b clinical trial for OKG‑0303, a fixed‑dose combination treatment targeting both viral and bacterial forms of acute infectious conjunctivitis (including adenoviral conjunctivitis), aiming to address the broad unmet need in infectious conjunctivitis therapeutics

- In July 2025, Starpharma Holdings Ltd. reported that its clinical‑stage dendrimer SPL7013 (astodrimer sodium) exhibited potent antiviral effects against adenovirus — the predominant viral agent in viral conjunctivitis — and is being advanced through further development and commercial discussions as a novel therapy candidate for viral conjunctivitis treatment

- In April 2025, interim data presented from ongoing research in the viral conjunctivitis drugs pipeline indicated clinical activity of OKG‑0301 in acute adenoviral conjunctivitis patients, and this data was highlighted at scientific forums, indicating continued progress toward later‑stage clinical evaluation

- In June 2025, iView Therapeutics, Inc. announced that the first patient was dosed in its Phase 2 clinical trial (IVIEW‑1201‑01‑AIC) evaluating IVIEW‑1201, a gel‑forming ophthalmic solution for treating acute adenoviral conjunctivitis in India, marking a key entry into region‑specific clinical research for viral conjunctivitis therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.