Global Viral Hepatitis And Retrovirus Diagnostic Tests Market

Market Size in USD Billion

USD

4.78 Billion

USD

9.18 Billion

2025

2033

USD

4.78 Billion

USD

9.18 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.78 Billion | |

| USD 9.18 Billion | |

| % | |

|

Viral Hepatitis and Retrovirus Diagnostic Tests Market Size

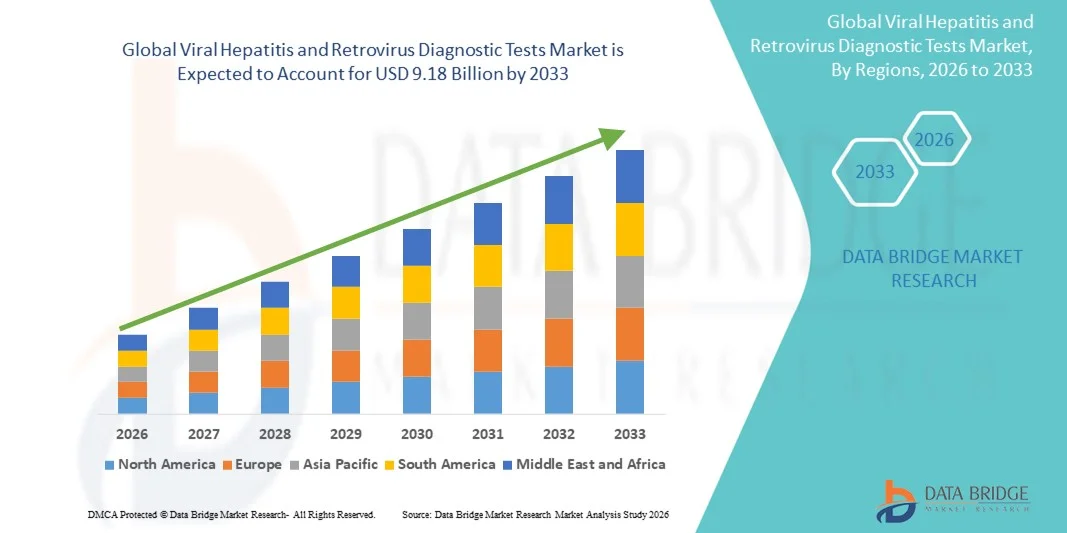

- The global viral hepatitis and retrovirus diagnostic tests market size was valued at USD 4.78 billion in 2025 and is expected to reach USD 9.18 billion by 2033, at a CAGR of 8.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of viral infections, advancements in molecular diagnostics, and technological progress in laboratory testing, leading to improved accuracy and faster detection in both clinical and point-of-care settings

- Furthermore, rising demand for early diagnosis, effective disease management, and widespread screening programs is accelerating the uptake of Viral Hepatitis and Retrovirus Diagnostic Tests solutions, thereby significantly boosting the industry's growth

Viral Hepatitis and Retrovirus Diagnostic Tests Market Analysis

- Viral Hepatitis and Retrovirus Diagnostic Tests, including ELISA, PCR, rapid diagnostic tests, and molecular assays, are increasingly vital components of modern healthcare due to their ability to enable early detection, accurate diagnosis, and effective disease management in both clinical and point-of-care settings

- The escalating demand for Viral Hepatitis and Retrovirus Diagnostic Tests is primarily fueled by the rising prevalence of hepatitis B, hepatitis C, and HIV infections, growing awareness about early diagnosis, and increasing adoption of advanced molecular and rapid testing technologies

- North America dominated the viral hepatitis and retrovirus diagnostic tests market with the largest revenue share of 39.5% in 2025, supported by advanced healthcare infrastructure, high adoption of diagnostic technologies, strong government-led screening programs, and the presence of leading diagnostic companies, with the U.S. experiencing substantial growth due to increased testing initiatives and early diagnosis campaigns

- Asia-Pacific is expected to be the fastest growing region in the viral hepatitis and retrovirus diagnostic tests market during the forecast period due to rising healthcare expenditure, growing population, increasing prevalence of viral infections, and improving access to advanced diagnostic technologies in countries such as China, India, and Japan

- The Chronic Hepatitis segment accounted for the largest market revenue share of 58.3% in 2025, driven by the rising prevalence of chronic hepatitis B and C infections globally

Report Scope and Viral Hepatitis and Retrovirus Diagnostic Tests Market Segmentation

|

Attributes |

Viral Hepatitis and Retrovirus Diagnostic Tests Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Roche Diagnostics (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Viral Hepatitis and Retrovirus Diagnostic Tests Market Trends

Growing Need Due to Rising Prevalence of Viral Infections and Early Diagnosis

- The increasing prevalence of viral infections, including hepatitis B, hepatitis C, and retroviral infections, coupled with the rising demand for early and accurate diagnosis, is a significant driver for the heightened adoption of advanced diagnostic tests

- For instance, in April 2025, Abbott Laboratories announced the launch of a next-generation viral hepatitis diagnostic panel capable of simultaneously detecting multiple viral strains with higher sensitivity and shorter turnaround time. Such strategies by key companies are expected to drive the Viral Hepatitis and Retrovirus Diagnostic Tests industry growth in the forecast period

- As healthcare providers become more focused on early detection and timely intervention, modern diagnostic tests offer rapid results, quantitative viral load measurements, and improved specificity, providing a compelling alternative to traditional methods

- Furthermore, increasing awareness about blood-borne infections, screening programs, and preventive healthcare initiatives are making diagnostic testing an essential part of clinical practice, ensuring early intervention and improved patient outcomes

- The convenience of multiplex testing, point-of-care diagnostics, and integration with hospital information systems are key factors propelling the adoption of Viral Hepatitis and Retrovirus Diagnostic Tests in both clinical and laboratory settings. The growing trend towards comprehensive screening in high-risk populations and routine checkups further contributes to market growth

Viral Hepatitis and Retrovirus Diagnostic Tests Market Dynamics

Driver

Advancements in Multiplex Testing and Point-of-Care Diagnostics

- A major and accelerating trend in the global viral hepatitis and retrovirus diagnostic tests market is the development and adoption of multiplex testing platforms and point-of-care diagnostic solutions. These innovations allow simultaneous detection of multiple viral strains or biomarkers in a single test, improving efficiency and reducing turnaround time

- For instance, in March 2024, Bio-Rad Laboratories launched a novel multiplex assay capable of detecting hepatitis B, C, and HIV antibodies in a single sample, offering rapid and accurate results for high-risk populations

- Modern point-of-care diagnostic devices are designed for use in clinics, small laboratories, and remote healthcare facilities, providing rapid results without the need for centralized labs. This trend is enhancing access to timely diagnosis in underserved and rural regions

- Integration of automated sample processing and digital reporting in new diagnostic systems is improving workflow efficiency, minimizing human error, and supporting faster clinical decision-making

- Healthcare providers are increasingly adopting non-invasive and minimally invasive testing options, such as saliva- or finger-prick-based assays, which improve patient compliance and broaden screening programs

- The rising demand for early detection, particularly among high-risk groups such as immunocompromised patients, pregnant women, and healthcare workers, is further fueling the adoption of advanced diagnostic solutions. Continuous improvements in sensitivity, specificity, and throughput of diagnostic platforms are creating opportunities for widespread clinical adoption, particularly in hospitals and specialized clinics

- Growing collaboration between diagnostic companies and public health authorities for mass screening and epidemiological studies is also shaping the market, as large-scale testing programs are critical for controlling viral infections

Restraint/Challenge

Concerns Regarding High Costs and Limited Accessibility in Developing Regions

- The relatively high cost of advanced viral hepatitis and retrovirus diagnostic tests poses a significant challenge to broader market penetration, particularly in price-sensitive regions. Many advanced molecular and serological assays require sophisticated instruments and trained personnel, increasing the overall expense of testing

- For instance, high-cost PCR-based viral load tests remain inaccessible to smaller clinics and remote healthcare centers, limiting adoption despite clinical benefits

- Addressing these challenges through the development of cost-effective, portable, and easy-to-use diagnostic solutions is crucial for expanding market reach. Companies such as Roche Diagnostics and Siemens Healthineers are emphasizing the development of modular and affordable testing platforms to target smaller healthcare facilities and emerging markets

- Furthermore, lack of awareness and limited laboratory infrastructure in certain regions can hinder timely testing and accurate diagnosis, reducing overall adoption rates

- While prices for some rapid and immunoassay-based tests have gradually decreased, the perceived premium for high-precision molecular diagnostics can still deter widespread usage, especially in low-resource settings

- Overcoming these challenges through government initiatives, subsidies, public-private partnerships, and increased availability of affordable diagnostic kits will be vital for sustained market growth

Viral Hepatitis and Retrovirus Diagnostic Tests Market Scope

The market is segmented on the basis of type, product type, end-users, and distribution channel.

- By Type

On the basis of type, the Viral Hepatitis and Retrovirus Diagnostic Tests market is segmented into Retrovirus Diagnostic Tests and Viral Hepatitis Diagnostic Tests. The Viral Hepatitis Diagnostic Tests segment dominated the largest market revenue share of 55.4% in 2025, driven by the increasing prevalence of hepatitis infections globally and the need for timely diagnosis. Hospitals and diagnostic centers prefer viral hepatitis tests for routine screening, patient monitoring, and early intervention strategies. Government-led vaccination and screening programs further reinforce demand for these tests. The adoption of highly sensitive assays for hepatitis B, C, and E supports their large market share. Rising awareness among patients and healthcare providers about liver-related complications also boosts testing frequency. In addition, viral hepatitis tests are widely used in prenatal care, blood donation screening, and occupational health programs, contributing to their dominance. Technological advancements in automated and high-throughput testing enhance workflow efficiency, making viral hepatitis diagnostics a preferred choice in laboratories. Furthermore, increasing focus on early detection and preventive healthcare in emerging markets supports the expansion of this segment. The segment’s dominance is also reinforced by partnerships between diagnostic companies and public health authorities to ensure large-scale testing availability.

The Retrovirus Diagnostic Tests segment is expected to witness the fastest CAGR of 14.1% from 2026 to 2033, due to rising awareness about retroviral infections such as HIV and HTLV. Increasing adoption of rapid point-of-care testing in clinics and mobile testing units accelerates growth. Enhanced government funding and global initiatives for retroviral screening programs further drive the segment. Rising incidences of retroviral infections in emerging economies increase testing demand. Innovative assay kits that reduce turnaround time and improve sensitivity are creating additional growth opportunities. Growing integration of portable devices and simplified sample collection methods increases patient compliance. Expanding HIV treatment programs and pre-exposure prophylaxis monitoring also contribute to segment growth. Telehealth and decentralized testing models support wider accessibility, particularly in remote regions. As public health focus intensifies on early detection and prevention of retroviral infections, the segment is poised to maintain robust growth throughout the forecast period.

- By Product Type

On the basis of product type, the market is segmented into Chronic Hepatitis and Acute Hepatitis. The Chronic Hepatitis segment accounted for the largest market revenue share of 58.3% in 2025, driven by the rising prevalence of chronic hepatitis B and C infections globally. Chronic hepatitis tests are essential for ongoing patient management, monitoring viral load, and assessing treatment efficacy. Hospitals and specialized clinics prefer these tests for their high accuracy and sensitivity. Government screening programs for chronic infections and liver disease monitoring contribute to high demand. Increased awareness of long-term complications, including cirrhosis and hepatocellular carcinoma, fuels adoption. Laboratories utilize automated platforms for consistent testing of chronic cases, enhancing workflow efficiency. The growing aging population in many regions also increases the pool of patients requiring chronic hepatitis monitoring. Furthermore, the development of multiplex assays capable of detecting multiple chronic viral strains reinforces the segment’s dominance. Public and private health initiatives to ensure early intervention in chronic hepatitis cases further support large market share.

The Acute Hepatitis segment is expected to witness the fastest CAGR of 13.7% from 2026 to 2033, fueled by rising outbreaks of hepatitis A and E in developing countries. Rapid diagnostic tests for acute hepatitis enable timely clinical decisions and containment of disease spread. Point-of-care devices in clinics and emergency departments enhance early detection and reduce hospital burden. Increasing travel and migration patterns heighten the risk of acute infections, expanding the need for testing. Health authorities are promoting vaccination programs and outbreak monitoring, supporting growth. Innovations in sample collection and rapid turnaround further accelerate adoption. Rising public health awareness campaigns and routine screening in high-risk populations, such as food handlers and travelers, also drive the segment.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The Hospital segment dominated the largest market revenue share of 62.8% in 2025, driven by the concentration of advanced diagnostic facilities and high patient volumes. Hospitals utilize comprehensive testing panels for inpatient and outpatient care, including routine screenings, disease monitoring, and preoperative assessments. Integration of automated laboratory equipment in hospitals improves throughput and efficiency. Government regulations often mandate hepatitis and retrovirus testing in hospital settings, reinforcing the segment’s dominance. Hospitals also benefit from centralized procurement, ensuring bulk availability and consistent supply of diagnostic kits. Increasing prevalence of viral infections among hospitalized patients supports demand. Collaborations between hospitals and diagnostic manufacturers facilitate access to advanced testing technologies. Specialized infectious disease departments further contribute to consistent testing requirements. In addition, hospitals play a key role in epidemiological studies and public health reporting, driving large-scale testing.

The Clinic segment is expected to witness the fastest CAGR of 9.5% from 2026 to 2033, due to growing outpatient visits and early diagnosis trends. Clinics provide easy access and shorter waiting times. Rising awareness encourages people to seek early consultation. Expansion of specialized diagnostic clinics supports this growth. The adoption of portable point-of-care devices in clinics also increases demand. Improved healthcare access in suburban and rural areas further drives this segment. Mobile testing units and telemedicine collaborations expand reach. Clinics’ convenience and patient-centric approach make them preferred locations for regular screening and follow-up care. Rising investment in primary care facilities further supports growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 59.1% in 2025, as hospitals procure diagnostic kits in bulk for inpatient and critical care applications. Centralized procurement, compliance with regulatory standards, and high consumption volumes reinforce segment leadership. Hospitals prefer direct procurement from manufacturers or authorized distributors to ensure reliability and quality. The high-volume usage of diagnostic kits for routine and specialized testing supports dominance. Strategic partnerships between hospitals and suppliers ensure uninterrupted supply.

The Online Pharmacy segment is expected to witness the fastest CAGR of 13.2% from 2026 to 2033, due to the growth in digital healthcare and e-commerce penetration. Online platforms offer convenience, rapid access to diagnostic kits, and doorstep delivery services. Rising smartphone usage and internet penetration support this trend. Increased preference for remote purchasing, subscription models, and competitive pricing further accelerates growth. Digital marketing campaigns and telehealth integrations boost consumer trust. Online sales enable access for patients in remote or underserved areas. Growth in home-based testing and self-collection kits also contributes to this segment’s rapid expansion

Viral Hepatitis and Retrovirus Diagnostic Tests Market Regional Analysis

- North America dominated the viral hepatitis and retrovirus diagnostic tests market with the largest revenue share of 39.5% in 2025

- Supported by advanced healthcare infrastructure, high adoption of diagnostic technologies, strong government-led screening programs, and the presence of leading diagnostic companies, with the U.S. experiencing substantial growth due to increased testing initiatives and early diagnosis campaigns.

- This widespread adoption is further supported by high disposable incomes, technologically advanced laboratories, and growing awareness about the importance of early detection of viral infections, establishing North America as a key revenue-generating region for the market

U.S. Viral Hepatitis and Retrovirus Diagnostic Tests Market Insight

The U.S. viral hepatitis and retrovirus diagnostic tests market captured the largest revenue share within North America in 2025, fueled by increasing government screening initiatives, rising prevalence of viral infections such as hepatitis B, hepatitis C, and HIV, and the expanding adoption of advanced diagnostic technologies, including rapid and point-of-care testing. Moreover, the growing focus on early diagnosis and preventive healthcare is significantly contributing to market expansion.

Europe Viral Hepatitis and Retrovirus Diagnostic Tests Market Insight

The Europe viral hepatitis and retrovirus diagnostic tests market is projected to expand at a substantial CAGR throughout the forecast period, driven by rising awareness of viral infections, government-supported vaccination and screening programs, and advancements in diagnostic technology adoption across clinical laboratories and hospitals. The region is experiencing significant growth in both private and public healthcare settings.

U.K. Viral Hepatitis and Retrovirus Diagnostic Tests Market Insight

The U.K. viral hepatitis and retrovirus diagnostic tests market is anticipated to grow at a noteworthy CAGR during the forecast period due to national health programs targeting hepatitis and retrovirus screening, increased healthcare funding, and technological advancements in diagnostic procedures. The growing prevalence of chronic viral infections is further encouraging adoption of advanced diagnostic tests.

Germany Viral Hepatitis and Retrovirus Diagnostic Tests Market Insight

The Germany viral hepatitis and retrovirus diagnostic tests market is expected to expand at a considerable CAGR during the forecast period, fueled by the government’s focus on preventive healthcare, increasing awareness about early detection of viral infections, and the integration of automated and rapid diagnostic technologies in hospitals and clinics.

Asia-Pacific Viral Hepatitis and Retrovirus Diagnostic Tests Market Insight

The Asia-Pacific viral hepatitis and retrovirus diagnostic tests market is poised to grow at the fastest CAGR during the forecast period, driven by rising healthcare expenditure, growing population, increasing prevalence of viral infections, and improving access to advanced diagnostic technologies in countries such as China, India, and Japan. The region is also benefiting from expanding healthcare infrastructure and government-led screening initiatives.

Japan Viral Hepatitis and Retrovirus Diagnostic Tests Market Insight

The Japan viral hepatitis and retrovirus diagnostic tests market is witnessing growth due to rising awareness of viral infections, increasing demand for early diagnosis, and adoption of high-precision diagnostic technologies in hospitals and clinics. The aging population and preventive healthcare initiatives are also supporting market expansion.

China Viral Hepatitis and Retrovirus Diagnostic Tests Market Insight

China viral hepatitis and retrovirus diagnostic tests market accounted for a significant revenue share in Asia-Pacific in 2025, attributed to the large population, increasing prevalence of viral infections, government-backed screening programs, and the expanding adoption of point-of-care and laboratory-based diagnostic technologies. The market is further supported by the growing focus on early detection and management of chronic viral infections.

Viral Hepatitis and Retrovirus Diagnostic Tests Market Share

The Viral Hepatitis and Retrovirus Diagnostic Tests industry is primarily led by well-established companies, including:

• Roche Diagnostics (Switzerland)

• Abbott (U.S.)

• Sanofi S.A. (France)

• Cepheid Inc. (U.S.)

• Siemens Healthineers (Germany)

• Becton, Dickinson and Company (U.S.)

• Thermo Fisher Scientific (U.S.)

• Ortho Clinical Diagnostics (U.S.)

• Qiagen N.V. (Netherlands)

• Bio-Rad Laboratories (U.S.)

• Hologic, Inc. (U.S.)

• Alere Inc. (U.S.)

• Nephron Pharmaceuticals (U.S.)

• PerkinElmer, Inc. (U.S.)

• BD Life Sciences (U.S.)

• Trinity Biotech plc (Ireland)

• Microlife Corporation (Switzerland)

• Johnson & Johnson (U.S.)

• Fujirebio Inc. (Japan)

Latest Developments in Global Viral Hepatitis and Retrovirus Diagnostic Tests Market

- In July 2024, the World Health Organization (WHO) prequalified the first-ever hepatitis C virus (HCV) self‑test, the OraQuick HCV self-test by OraSure Technologies, marking a significant step toward broader access to HCV diagnosis. This self‑test allows lay users to test themselves for HCV antibodies, supporting decentralized testing efforts and helping accelerate global elimination goals

- In June 2024, the U.S. Food and Drug Administration (FDA) granted marketing authorization to Cepheid for its Xpert HCV test on the GeneXpert Xpress system — this is the first HCV RNA test that can be run in CLIA-waived, point‑of‑care settings using a finger‑stick blood sample, offering results in about an hour

- In November 2023, Roche Diagnostics expanded its viral hepatitis diagnostics portfolio by launching the Elecsys HBeAg quant immunoassay, which measures both the presence and quantity of the hepatitis B e-antigen (HBeAg). This helps clinicians more accurately diagnose and monitor HBV infection and disease activity

- In November 2023, Roche also announced the launch of two automated serology tests for hepatitis E virus (HEV): Elecsys Anti-HEV IgM and IgG. These assays allow for rapid detection of acute and past HEV infections and were aligned with the inclusion of HEV testing in the WHO’s 2023 Essential Diagnostics List

- In July 2023, Roche Diagnostics India introduced the Elecsys HCV Duo immunoassay — a dual antigen‑antibody test that detects both the HCV core antigen (marker of active infection) and anti-HCV antibodies in a single run, allowing earlier diagnosis of HCV compared to antibody-only tests

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.