Global Viral Testing Market

Market Size in USD Billion

USD

9.29 Billion

USD

14.69 Billion

2025

2033

USD

9.29 Billion

USD

14.69 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.29 Billion | |

| USD 14.69 Billion | |

| % | |

|

Viral Testing Market Overview

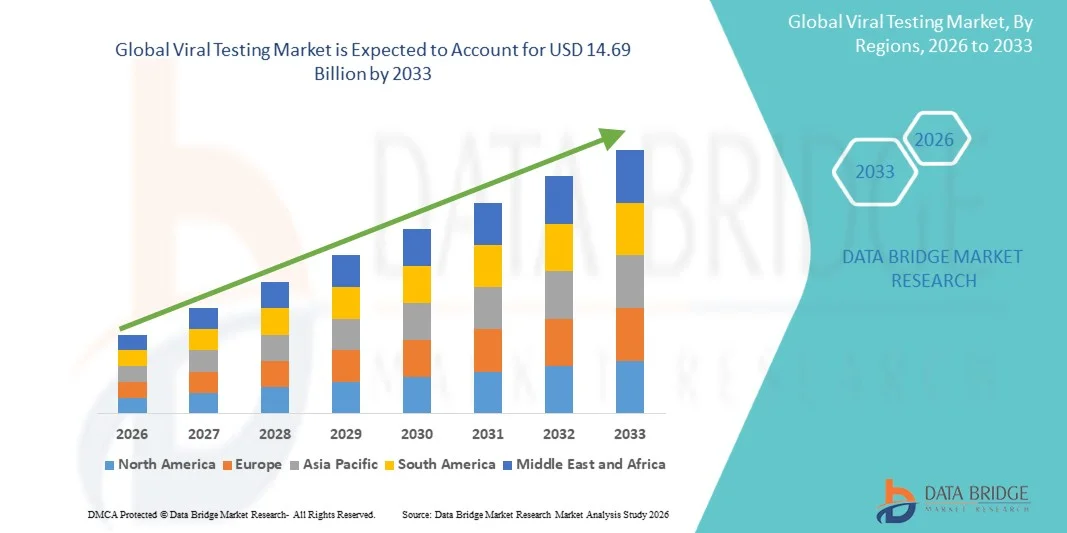

The Viral Testing Market was valued at USD 9.29 billion in 2025 and is projected to reach USD 14.69 billion by 2033, growing at a CAGR of 5.90% from 2026 to 2033. The Viral Testing Market is experiencing consistent growth driven by the rising prevalence of infectious viral diseases, increasing demand for early and accurate disease diagnosis, and continuous advancements in molecular diagnostic technologies such as PCR, RT-PCR, and next-generation sequencing (NGS). The expansion of global surveillance programs for emerging and re-emerging viral infections, including influenza, HIV, hepatitis, and novel coronaviruses, is further strengthening market demand.

The increasing frequency of viral outbreaks and pandemics, combined with stronger public health preparedness initiatives and stricter regulatory requirements for infection control, is compelling hospitals, diagnostic laboratories, and government health agencies to adopt advanced viral testing solutions. Rapid point-of-care testing, high-throughput laboratory automation, and multiplex molecular assays are increasingly replacing traditional culture-based methods, offering faster turnaround times, higher sensitivity, and improved diagnostic accuracy. Expanding applications across clinical diagnostics, blood screening, epidemiology, and research laboratories continue to support sustained market growth globally.

Key Market Trends & Insights

- North America dominated the Viral Testing Market with the largest revenue share of 38.12% in 2025, supported by advanced diagnostic infrastructure, high healthcare expenditure, strong presence of leading diagnostic companies, and widespread adoption of molecular testing technologies such as PCR, RT-PCR, and next-generation sequencing (NGS). The region also benefits from robust disease surveillance systems, high testing volumes for respiratory and blood-borne viruses, and strong government funding for infectious disease preparedness.

- The RT-PCR-Based Tests segment dominated the market with the largest revenue share of 42.18% in 2025, owing to its high sensitivity, strong specificity, and ability to detect viral genetic material at early infection stages.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.3% from 2026 to 2033, fueled by rising population density, increasing burden of infectious diseases, expanding diagnostic laboratory networks, and growing government investments in healthcare infrastructure across China, India, Japan, and Southeast Asia.

- Point-of-Care (POC) Testing is the fastest-growing testing type, projected to register a CAGR of 8.6%, driven by increasing demand for rapid, decentralized diagnostic solutions, especially in emergency care, rural healthcare settings, and outbreak response scenarios. Portable molecular devices and rapid antigen tests are significantly accelerating adoption.

- The Clinical Diagnostics segment dominates the application category with a 45.28% revenue share in 2025, led by rising hospital admissions for viral infections, increasing routine screening, and strong integration of molecular testing into standard diagnostic workflows across healthcare systems globally.

- Hospitals & Diagnostic Laboratories account for 57.94% of the market share in 2025, as they remain the primary centers for high-volume viral testing, supported by advanced laboratory infrastructure, trained professionals, and availability of automated molecular diagnostic systems.

- On-Premise Laboratory Testing dominates the deployment category with a 61.33% share in 2025, preferred due to high data security, better workflow control, and ability to handle large sample volumes in centralized diagnostic facilities.

- Cloud-Based Diagnostic Platforms are the fastest-growing segment, expected to register a CAGR of 9.1%, driven by increasing digitalization of healthcare, remote diagnostics, AI-powered test interpretation, and real-time epidemiological data sharing.

Market Size & Forecast

- Global Market Value (2025): USD 9.29 Billion

- Expected Market Value (2033): USD 14.69 Billion

- Forecast CAGR (2026–2033): 5.90%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Viral Testing Market Segmentation

|

Attributes |

Viral Testing Key Market Insights |

|

Segments Covered |

· By Test Type: Direct Fluorescent Antibody (DFA) Tests, Immunochromatographic Assays, Reverse Transcription Polymerase Chain Reaction (RT-PCR)-Based Tests, Agglutination Assays, Flow-Through Assays, Solid-Phase Assays · By Application: Influenza, Hepatitis, HIV, Measles, Rubella, Others · By End Use: Laboratories, Hospitals, Home Care Settings, Academic Institutes |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Abbott Laboratories (U.S.) |

|

Market Opportunities |

· Expansion of Molecular and RT-PCR-Based Testing · Growth in Point-of-Care (POC) and Rapid Testing Solutions · Rising Adoption of Multiplex and Syndromic Testing Panels |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Viral Testing Market Trends

Trend: Expansion of High-Throughput and Rapid Viral Testing Technologies

The Viral Testing Market is witnessing a strong shift toward high-throughput molecular diagnostics and rapid testing platforms to meet increasing global demand for early and accurate detection of viral infections. Laboratories and hospitals are increasingly adopting automated PCR and multiplex assay systems capable of processing thousands of samples per day, significantly improving diagnostic efficiency and turnaround time. For instance, during the COVID-19 pandemic, high-throughput PCR platforms such as Roche’s cobas 6800/8800 systems demonstrated the ability to process up to 3,000–4,000 tests per day per instrument, highlighting the scalability of modern viral diagnostics. The growing adoption of rapid antigen and molecular point-of-care (POC) testing devices is further transforming decentralized testing, enabling results within 15–30 minutes in emergency care and outpatient settings. Integration of AI-assisted diagnostic interpretation is also improving accuracy in viral detection and epidemiological tracking.

Viral Testing Market Dynamics

Key Market Driver: Rising Global Burden of Infectious Viral Diseases and Pandemic Preparedness Initiatives

A major driver of the Viral Testing Market is the increasing prevalence of infectious viral diseases such as influenza, HIV, hepatitis B and C, dengue, and emerging respiratory viruses. According to the World Health Organization (WHO), seasonal influenza alone affects approximately 1 billion people globally each year, including 3–5 million severe cases. In addition, the COVID-19 pandemic demonstrated the critical importance of scalable viral testing infrastructure, with over 13 billion COVID-19 tests performed globally by 2023. Governments across North America, Europe, and Asia-Pacific are now investing heavily in pandemic preparedness programs, expanding national disease surveillance networks, and strengthening laboratory capacity. The U.S. Centers for Disease Control and Prevention (CDC) and European Centre for Disease Prevention and Control (ECDC) have significantly increased funding for genomic sequencing and real-time viral monitoring systems. This growing focus on early outbreak detection and containment is driving sustained demand for advanced viral testing technologies across clinical and public health settings.

Key Restraint/Challenge: High Cost and Infrastructure Requirements of Advanced Molecular Diagnostics

Despite strong growth potential, the Viral Testing market faces a key challenge in the form of high costs associated with advanced diagnostic systems and laboratory infrastructure. Molecular testing platforms such as real-time PCR machines, next-generation sequencing (NGS) systems, and automated immunoassay analyzers require significant capital investment, often ranging from USD 25,000 to over USD 250,000 per instrument depending on configuration and throughput capacity. In addition, recurring costs related to reagents, consumables, maintenance, and skilled laboratory personnel further increase the total cost of ownership. This limits adoption in low- and middle-income countries where healthcare budgets are constrained. For example, the WHO has reported that many developing regions in Africa and parts of Southeast Asia still lack adequate access to advanced molecular diagnostic laboratories, resulting in delayed detection of viral outbreaks. Furthermore, supply chain disruptions during global health emergencies, such as shortages of PCR reagents during COVID-19, highlight operational vulnerabilities in scaling testing capacity during peak demand periods.

Key Market Opportunity: Integration of Genomic Sequencing and AI-Driven Diagnostic Platforms

The integration of next-generation sequencing (NGS), artificial intelligence (AI), and digital health technologies presents a major growth opportunity in the Viral Testing Market. Genomic sequencing is increasingly being used for real-time tracking of viral mutations, as demonstrated during the COVID-19 pandemic when platforms such as Illumina and Oxford Nanopore Technologies enabled rapid identification of new variants like Delta and Omicron within weeks of emergence. AI-powered diagnostic tools are further enhancing viral detection accuracy by analyzing large datasets from PCR and sequencing outputs, enabling faster outbreak prediction and response. Cloud-based laboratory information systems (LIS) are also facilitating real-time data sharing between hospitals, research institutions, and public health agencies. In addition, expanding investments in decentralized testing infrastructure, particularly in Asia-Pacific and Latin America, are creating significant opportunities for portable diagnostic devices and point-of-care molecular platforms. These advancements are expected to significantly improve global preparedness for future viral outbreaks while expanding access to rapid and accurate testing in underserved regions.

Viral Testing Market Scope

The Viral Testing Market is segmented on the basis of test type, application, and end use.

- By Tests

On the basis of tests, the Viral Testing Market is segmented into Direct Fluorescent Antibody (DFA) Tests, Immunochromatographic Assays, Reverse Transcription Polymerase Chain Reaction (RT-PCR)-Based Tests, Agglutination Assays, Flow-Through Assays, and Solid-Phase Assays. The RT-PCR-Based Tests segment dominated the market with the largest revenue share of 42.18% in 2025, owing to its high sensitivity, strong specificity, and ability to detect viral genetic material at early infection stages. This segment is widely adopted across hospitals, diagnostic laboratories, and reference centers for diseases such as influenza, HIV, hepatitis, and emerging viral infections. Increasing demand for molecular diagnostics, strong government-funded testing programs, and post-pandemic preparedness initiatives are further strengthening adoption. The segment benefits from continuous technological advancements in real-time PCR platforms, multiplex testing capabilities, and automation. Rising prevalence of respiratory infections and blood-borne viruses is further driving routine RT-PCR usage. Strong clinical reliability compared to conventional serological methods reinforces its dominance in the global market.

The Immunochromatographic Assays segment is expected to register the fastest CAGR of 7.4% from 2026 to 2033, driven by growing demand for rapid point-of-care testing solutions. These assays provide quick results within minutes, making them highly suitable for emergency care, home testing, and remote healthcare settings. Increasing adoption during outbreaks of influenza and COVID-like infections has significantly expanded their usage. Low cost, ease of use, and minimal requirement for laboratory infrastructure are key growth drivers. Expanding distribution of rapid diagnostic kits through retail and online pharmacies is improving accessibility. Government initiatives promoting early disease detection in rural and underserved regions are also supporting growth. Technological improvements in lateral flow assay sensitivity are enhancing diagnostic accuracy. Rising preference for decentralized healthcare testing is further accelerating demand globally.

- By Application

On the basis of application, the Viral Testing Market is segmented into Influenza, Hepatitis, HIV, Measles, Rubella, and Others. The Influenza segment dominated the market with the largest revenue share of 31.64% in 2025, due to high seasonal prevalence and recurring global outbreaks. Continuous mutation of influenza viruses necessitates frequent diagnostic testing and surveillance. Strong global monitoring programs by WHO and national health agencies further support routine influenza screening. Hospitals and laboratories conduct large-scale seasonal testing during flu peaks, increasing test volumes significantly. Co-circulation of influenza with other respiratory viruses such as RSV and SARS-like pathogens is further driving demand. Rising elderly population and immunocompromised patients contribute to higher testing rates. Availability of rapid influenza diagnostic tests also supports early detection. Public health awareness campaigns are encouraging preventive screening.

The HIV segment is expected to register the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing global screening initiatives and early diagnosis programs. Rising awareness regarding HIV transmission and prevention is boosting testing adoption. Government-funded free testing programs in developing regions are expanding access. Advancements in fourth-generation antigen/antibody combination tests are improving early detection rates. Strong demand for routine screening in high-risk populations supports segment growth. Expansion of self-testing kits is increasing patient-driven diagnostics. Integration of HIV testing into antenatal and routine health check-ups is further supporting adoption. International funding programs targeting HIV elimination are accelerating market expansion.

- By End Use

On the basis of end use, the Viral Testing Market is segmented into Laboratories, Hospitals, Home Care Settings, and Academic Institutes. The Laboratories segment dominated the market with the largest revenue share of 46.72% in 2025, due to high sample processing capacity and advanced diagnostic infrastructure. Centralized diagnostic laboratories handle large volumes of infectious disease testing efficiently. Strong adoption of RT-PCR and automated molecular platforms enhances throughput and accuracy. Laboratories benefit from economies of scale in large-scale screening programs. Increasing outsourcing of hospital diagnostic workloads to reference labs is further supporting growth. Presence of skilled laboratory professionals ensures high-quality testing output. Strong investments in high-throughput sequencing and multiplex diagnostic systems reinforce dominance. Expansion of national disease surveillance programs is further boosting demand.

The Home Care Settings segment is expected to register the fastest CAGR of 7.8% from 2026 to 2033, driven by rising adoption of rapid self-testing kits. Increasing preference for at-home diagnosis for influenza, COVID-like infections, and general viral screening is supporting growth. Convenience, privacy, and faster results are key demand drivers. Expanding availability of OTC diagnostic kits through pharmacies and e-commerce platforms is increasing accessibility. Growing geriatric population preferring home-based healthcare solutions is further boosting demand. Technological improvements in rapid antigen test accuracy are enhancing reliability. Rising healthcare decentralization and telemedicine integration are supporting home diagnostics. Government initiatives promoting self-testing during outbreaks are accelerating adoption globally.

Viral Testing Market Regional Analysis

North America dominated the Viral Testing Market and accounted for the largest revenue share of 38.12% in 2025, supported by advanced diagnostic infrastructure, high healthcare expenditure, and the strong presence of leading diagnostic companies. The region benefits from widespread adoption of molecular diagnostic technologies such as PCR, RT-PCR, and next-generation sequencing (NGS), which are extensively used for early and accurate viral detection. Robust disease surveillance systems, high testing volumes for respiratory and blood-borne infections, and strong government funding for infectious disease preparedness further strengthen market growth. In addition, well-established hospital networks, advanced laboratory automation, and rapid adoption of point-of-care testing solutions continue to reinforce North America’s leadership in the Viral Testing Market.

U.S. Viral Testing Market Insight

The U.S. Viral Testing market is witnessing strong growth driven by rising prevalence of infectious diseases, expanding adoption of molecular diagnostics, and continuous advancements in laboratory technologies. Increasing utilization of PCR and NGS-based testing platforms in hospitals, reference laboratories, and research institutes is enhancing diagnostic accuracy and turnaround time. Strong federal initiatives for pandemic preparedness and disease surveillance are further accelerating demand. In addition, the presence of major diagnostic companies and continuous innovation in rapid and multiplex testing solutions are supporting sustained market expansion across the country.

Europe Viral Testing Market Insight

The Europe Viral Testing market remains a key regional contributor, supported by strong public healthcare systems, stringent regulatory frameworks, and high awareness regarding early disease detection. Widespread use of advanced diagnostic technologies in hospitals, academic laboratories, and public health agencies is driving consistent demand. Increasing investments in infectious disease research, coupled with strong government-led screening and vaccination monitoring programs, are further supporting market growth. The region also benefits from collaborative research initiatives aimed at improving viral detection capabilities and strengthening pandemic preparedness.

U.K. Viral Testing Market Insight

The U.K. Viral Testing market is expanding steadily due to rising demand for advanced diagnostic testing and strong focus on public health surveillance. National healthcare initiatives supporting early detection of viral infections are encouraging widespread adoption of molecular and rapid testing solutions. Growing use of PCR-based diagnostics across hospitals and clinical laboratories is improving disease management outcomes. In addition, increasing investment in laboratory modernization and digital pathology systems is enhancing testing efficiency and accuracy across the country.

Germany Viral Testing Market Insight

The Germany Viral Testing market is growing steadily, driven by strong healthcare infrastructure, high laboratory automation adoption, and increasing focus on infectious disease control. German diagnostic laboratories are widely implementing PCR, RT-PCR, and multiplex assay technologies for accurate viral identification. Government support for biomedical research and strong collaboration between diagnostic companies and research institutes are further enhancing innovation in testing methodologies. Additionally, rising demand for early diagnosis and preventive healthcare is supporting sustained market expansion.

Asia-Pacific Viral Testing Market Insight

The Asia-Pacific Viral Testing market is expected to be the fastest-growing region, registering a CAGR of 8.3% from 2026 to 2033, driven by rising population density, increasing burden of infectious diseases, and expanding diagnostic laboratory networks. Rapid improvements in healthcare infrastructure across China, India, Japan, and Southeast Asia are significantly boosting testing capacity. Government investments in public health programs and infectious disease surveillance are further accelerating adoption of advanced diagnostic technologies. In addition, increasing awareness of early disease detection and growing access to affordable testing solutions are supporting strong regional market expansion.

Japan Viral Testing Market Insight

The Japan Viral Testing market is witnessing steady growth due to strong healthcare infrastructure, high adoption of advanced diagnostic technologies, and increasing focus on infectious disease monitoring. The country’s well-established laboratory systems extensively utilize molecular testing platforms such as PCR and NGS for precise viral detection. Growing emphasis on aging population healthcare management and preventive screening programs is further supporting demand. In addition, continuous innovation in automated diagnostic systems and digital laboratory solutions is improving testing efficiency and reliability.

China Viral Testing Market Insight

The China Viral Testing market is expanding rapidly, driven by a large population base, increasing prevalence of infectious diseases, and strong government investment in healthcare infrastructure. The country is witnessing rising adoption of molecular diagnostics, high-throughput testing systems, and rapid antigen testing across hospitals and laboratories. Expansion of public health surveillance programs and increasing focus on epidemic preparedness are further strengthening market demand. In addition, continuous development of domestic diagnostic manufacturing capabilities and increasing accessibility of testing services are positioning China as a major growth hub in the Viral Testing Market.

Viral Testing Market Share

The Viral Testing industry is primarily led by well-established companies, including:

- Abbott Laboratories (U.S.)

- Roche Diagnostics (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- bioMérieux SA (France)

- Becton, Dickinson and Company (U.S.)

- Danaher Corporation (U.S.)

- Siemens Healthineers AG (Germany)

- QuidelOrtho Corporation (U.S.)

- Hologic Inc. (U.S.)

- Qiagen N.V. (Germany/Netherlands)

- Sysmex Corporation (Japan)

- Fujirebio (Japan)

- Luminex Corporation (U.S.)

- Agilent Technologies Inc. (U.S.)

- PerkinElmer Inc. (U.S.)

- Trinity Biotech plc (Ireland)

- SD Biosensor Inc. (South Korea)

- Cepheid (U.S.)

- GenMark Diagnostics (U.S.)

- OraSure Technologies Inc. (U.S.)

- Chembio Diagnostics Inc. (U.S.)

- Altona Diagnostics GmbH (Germany)

- Bio-Rad Laboratories Inc. (U.S.)

- Revvity (formerly PerkinElmer Health Sciences brands) (U.S.)

- LumiraDx Ltd. (U.K.)

- Mylab Discovery Solutions Pvt. Ltd. (India)

- Molbio Diagnostics Pvt. Ltd. (India)

- Tulip Diagnostics (India)

- Arkray Inc. (Japan)

- Accula (Mesa Biotech – Thermo Fisher brand) (U.S.)

- BD MAX System (Becton Dickinson platform) (U.S.)

Latest Developments in Viral Testing Market

- In March 2021, the U.S. Food and Drug Administration (FDA) authorized multiple at-home COVID-19 rapid antigen tests, including Abbott’s BinaxNOW and Quidel’s QuickVue, enabling over-the-counter self-testing x`x`-19-related rapid test segments, reflecting sustained post-pandemic demand for fast and accessible viral detection technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.