Global Virtual Specialty Consultation Networks Market

Market Size in USD Billion

USD

1.68 Billion

USD

7.03 Billion

2025

2033

USD

1.68 Billion

USD

7.03 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 1.68 Billion |

Market Size (Forecast Year) |

USD 7.03 Billion |

CAGR |

% |

Major Markets Players |

|

Virtual Specialty Consultation Networks Market Size

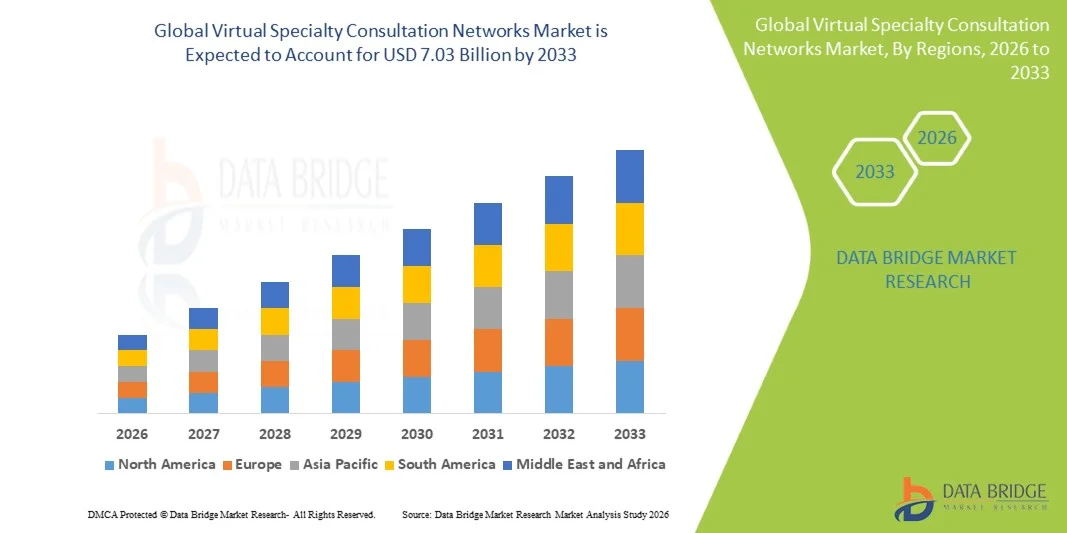

- The global virtual specialty consultation networks market size was valued at USD 1.68 billion in 2025 and is expected to reach USD 7.03 billion by 2033, at a CAGR of 19.60% during the forecast period

- The market growth is largely fueled by the increasing adoption of telemedicine and digital healthcare solutions, along with technological advancements in virtual consultation platforms, AI-enabled tools, and remote monitoring systems, leading to improved access to specialty care across both urban and rural healthcare settings

- Furthermore, rising demand from patients and healthcare providers for secure, user-friendly, and integrated virtual care solutions is establishing Virtual Specialty Consultation Networks as a preferred method for accessing specialist care and managing chronic conditions. These converging factors are accelerating the uptake of virtual consultation services, thereby significantly boosting the industry's growth

Virtual Specialty Consultation Networks Market Analysis

- Virtual Specialty Consultation Networks, providing secure and efficient access to specialist care remotely, are increasingly vital components of modern healthcare delivery systems in both urban and rural settings due to their enhanced convenience, real-time interaction capabilities, and seamless integration with electronic health records and digital health platforms

- The escalating demand for virtual consultation networks is primarily fueled by the widespread adoption of telemedicine technologies, growing need for accessible specialty care, and increasing patient preference for remote healthcare services

- North America dominated the virtual specialty consultation networks market with the largest revenue share of approximately 40% in 2025, driven by advanced healthcare infrastructure, high digital health adoption, strong presence of key market players, and the U.S. experiencing substantial growth in virtual specialty consultations, supported by innovations in AI, telehealth platforms, and integrated care solutions

- Asia-Pacific is expected to be the fastest-growing region in the virtual specialty consultation networks market during the forecast period due to increasing healthcare digitization, rising patient awareness, expanding telemedicine adoption, and growing healthcare expenditure in countries such as China, India, and Japan

- The Cloud-Based Networks segment dominated the largest market revenue share of 51.2% in 2025, due to scalability, cost-effectiveness, and remote accessibility advantages

Report Scope and Virtual Specialty Consultation Networks Market Segmentation

|

Attributes |

Virtual Specialty Consultation Networks Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Virtual Specialty Consultation Networks Market Trends

“Growing Need Due to Rising Prevalence of Complex Medical Cases”

- The rising incidence of chronic, rare, and multi-morbid medical conditions is fueling demand for virtual specialty consultation networks, as patients seek timely access to expert care beyond their immediate geographical area

- For instance, in 2025, the Mayo Clinic’s virtual rheumatology program allowed patients with rare autoimmune disorders in rural areas to consult top specialists without traveling hundreds of miles

- Population studies in North America and Europe show a steady increase in patients with autoimmune disorders, cardiovascular diseases, and genetic conditions, highlighting the necessity for remote specialist access

- For instance, Mount Sinai Health System implemented a virtual cardiology network to manage heart failure patients across multiple states, resulting in improved follow-up adherence and reduced hospital readmissions

- The growing awareness among patients and caregivers about available specialty expertise is increasing adoption of virtual platforms, as they provide convenience and faster consultation compared to traditional referrals

- Hospitals and clinics are leveraging virtual networks to optimize physician workloads, reduce patient wait times, and ensure continuous care, especially for those in remote or underserved areas

- An instance is Cleveland Clinic’s virtual oncology network, which coordinates multiple specialists for patients undergoing chemotherapy, improving care efficiency

Virtual Specialty Consultation Networks Market Dynamics

Driver

“Increasing Integration of Multidisciplinary Care and Collaborative Networks”

- Virtual specialty consultation networks are increasingly facilitating real-time collaboration among multiple healthcare providers, improving diagnostic accuracy and treatment outcomes for complex cases

- For instance, the Stanford Health Care virtual tumor board connects oncologists, radiologists, and pathologists across different hospitals to discuss complex cancer cases in real-time

- Platforms are now integrating electronic health records (EHR), lab results, and imaging systems, allowing specialists from cardiology, neurology, oncology, and rheumatology to review patient data simultaneously

- For instance, Intermountain Healthcare’s integrated EHR platform enables neurologists and cardiologists to jointly review patient imaging and lab results before virtual consultations

- Healthcare systems are adopting hybrid care models where initial consultations, follow-ups, and patient monitoring are managed virtually, while critical procedures or interventions occur in person

- An instance is Johns Hopkins Medicine, where post-surgical follow-ups for high-risk patients are conducted via virtual visits, while surgeries are performed on-site

- The trend of integrating virtual consultation networks with patient management platforms enables continuous care coordination, ensuring that patients receive consistent treatment across multiple providers

Restraint/Challenge

“Concerns Regarding Data Security, Interoperability, and High Setup Costs”

- With sensitive patient data being transmitted and stored digitally, cybersecurity and data privacy remain major concerns, with providers required to comply with regulations such as HIPAA in the U.S. and GDPR in Europe

- For instance, in 2024, a small-scale ransomware attack in a European virtual consultation platform temporarily blocked access to patient records, highlighting the critical need for secure systems

- Interoperability challenges between existing hospital IT systems and virtual consultation platforms can create inefficiencies, potentially limiting the seamless sharing of patient information

- For instance, a multi-hospital network in India faced delays integrating lab data with its virtual specialty platform due to incompatible software systems, slowing patient care

- The cost of implementing and maintaining virtual networks—including software licensing, secure cloud storage, and training personnel—can be a barrier for smaller clinics and healthcare providers in developing regions

- Patients’ trust in virtual consultation platforms is influenced by perceived risks around confidentiality and data breaches, which can slow adoption in certain markets

- An instance is a survey conducted in 2025 among elderly patients in the U.S., showing that 32% hesitated to use virtual consultation services due to data privacy concerns

Virtual Specialty Consultation Networks Market Scope

The market is segmented on the basis of service type, platform, and network type.

• By Service Type

On the basis of service type, the Virtual Specialty Consultation Networks market is segmented into Teleconsultation Services, Remote Patient Monitoring, Digital Health Platforms & Integration Services, and Others. The Teleconsultation Services segment dominated the largest market revenue share of 46.5% in 2025, driven by widespread adoption of virtual doctor visits, convenience for patients, and integration with insurance reimbursement programs. Hospitals, specialty clinics, and outpatient centers increasingly adopt teleconsultation to extend care access, particularly in remote or underserved regions. The segment benefits from high patient engagement, improved adherence to therapy, and real-time communication with physicians. Expansion of digital health policies, government incentives, and pandemic-driven adoption further reinforce market dominance. Integration with electronic health records ensures continuity of care and streamlined workflow. Hospitals leverage teleconsultation for chronic disease management and follow-ups, reducing readmission rates. Partnerships with insurance providers and technology vendors enhance accessibility. Continuous innovation in teleconsultation platforms supports quality care. Patient education campaigns and professional training increase adoption. Teleconsultation reduces travel and healthcare costs for patients. Development of specialty-focused virtual programs improves patient outcomes.

The Remote Patient Monitoring segment is expected to witness the fastest CAGR of 18.2% from 2026 to 2033, driven by the increasing prevalence of chronic diseases, rising demand for continuous monitoring, and adoption of wearable devices. Remote monitoring allows real-time tracking of patient vitals, medication adherence, and early detection of complications. Integration with AI-powered analytics improves predictive care and personalized interventions. Telehealth platforms, mobile apps, and cloud-based dashboards enhance user experience for patients and clinicians. Expansion in home healthcare and outpatient services supports rapid adoption. Insurance coverage and government incentives further encourage uptake. Clinical guidelines increasingly recommend remote monitoring for chronic disease management. Adoption is boosted by patient convenience, reduced hospital visits, and enhanced data collection. Healthcare providers benefit from operational efficiency and improved patient outcomes. Partnerships between technology vendors and healthcare institutions drive growth. Data security and compliance with regulations strengthen trust. Emerging markets are gradually adopting remote monitoring solutions.

• By Platform

On the basis of platform, the market is segmented into Video Conferencing Platforms, AI-Enabled Virtual Consultation Tools, Mobile & Web Applications, and Others. The Video Conferencing Platforms segment held the largest market revenue share of 44.8% in 2025, driven by its ability to provide seamless, real-time interactions between patients and specialists. Hospitals and outpatient centers integrate video platforms for routine consultations, follow-ups, and specialty care. Video conferencing improves diagnostic accuracy and patient engagement. High-quality audiovisual solutions, reliability, and compatibility with electronic health records enhance adoption. Professional training and IT support ensure smooth platform operation. The segment benefits from strong regulatory support and reimbursement frameworks. Integration with digital health platforms improves workflow efficiency. Telehealth adoption accelerated during COVID-19 and continues to maintain growth momentum. Patient preference for face-to-face virtual interactions sustains usage. Remote consultations reduce travel and operational costs. Collaboration with technology vendors ensures platform scalability. Video conferencing supports multi-specialty consultations and team-based care models.

The AI-Enabled Virtual Consultation Tools segment is expected to witness the fastest CAGR of 17.5% from 2026 to 2033, driven by increasing demand for intelligent decision support, symptom triaging, and predictive analytics. AI tools assist physicians in diagnosis, personalized treatment plans, and prioritizing patient needs. Integration with teleconsultation platforms enhances efficiency and clinical outcomes. Hospitals and specialty clinics leverage AI to optimize resource allocation and reduce wait times. Cloud-based deployment allows rapid scaling and real-time updates. Continuous algorithm improvements and machine learning capabilities strengthen adoption. AI tools enable patient self-management through chatbots and virtual assistants. Emerging markets are increasingly investing in AI-driven health solutions. Regulatory approvals and data privacy compliance foster trust. Training programs for clinicians improve AI utilization. Partnerships with software vendors accelerate deployment. AI-enabled platforms support integration with wearable devices and remote monitoring tools.

• By Network Type

On the basis of network type, the market is segmented into Cloud-Based Networks, On-Premise Networks, Hybrid Networks, and Others. The Cloud-Based Networks segment dominated the largest market revenue share of 51.2% in 2025, due to scalability, cost-effectiveness, and remote accessibility advantages. Cloud networks allow multiple stakeholders—hospitals, clinics, patients—to access and share data securely from any location. Integration with mobile apps and teleconsultation platforms ensures seamless workflows. Cloud solutions reduce IT maintenance costs and improve system reliability. Adoption is supported by regulatory compliance frameworks, cybersecurity measures, and encrypted data storage. Hospitals and specialty clinics leverage cloud networks for real-time collaboration and virtual consultations. The segment benefits from continuous software updates and AI integration. Patient satisfaction improves due to convenience and reduced wait times. Cloud networks support multi-specialty networks and large-scale patient data analytics. Vendor partnerships enhance service reliability and customer support. Expansion in emerging markets is accelerating due to affordable cloud infrastructure. Professional training ensures smooth implementation and adoption.

The Hybrid Networks segment is expected to witness the fastest CAGR of 16.8% from 2026 to 2033, driven by organizations seeking flexibility, combining cloud scalability with on-premise security. Hybrid networks are particularly preferred by large hospitals and research centers with sensitive patient data. Adoption is fueled by cybersecurity concerns, regulatory compliance, and customizable IT solutions. Hybrid systems facilitate interoperability between legacy hospital systems and modern telehealth platforms. Integration with AI-enabled tools and mobile applications improves operational efficiency. Healthcare providers benefit from centralized data management and distributed accessibility. Training programs enhance clinician adoption. Remote monitoring, virtual consultations, and clinical trial management are streamlined. Emerging markets gradually adopt hybrid solutions for specialty networks. Vendor support and scalable architecture drive growth. Hospitals gain operational resilience and redundancy. Patient trust increases due to enhanced data security. Partnerships with technology vendors accelerate implementation.

Virtual Specialty Consultation Networks Market Regional Analysis

- North America dominated the virtual specialty consultation networks market with the largest revenue share of approximately 40% in 2025, driven by advanced healthcare infrastructure, high digital health adoption, and a strong presence of key market players. The U.S. is experiencing substantial growth in virtual specialty consultations, supported by innovations in AI, telehealth platforms, and integrated care solutions

- High patient awareness, widespread smartphone and internet penetration, and growing adoption of remote healthcare technologies are further supporting market expansion. For instance, institutions like the Cleveland Clinic and Mayo Clinic have scaled virtual cardiology and rheumatology consultations, connecting patients in remote areas to top specialists

- The demand for personalized healthcare solutions, combined with government support for telemedicine reimbursement policies, is fueling adoption. Strategic collaborations between hospitals, insurers, and digital health startups are promoting integrated care models, improving patient outcomes and increasing reliance on virtual specialty networks

U.S. Virtual Specialty Consultation Networks Market Insight

The U.S. virtual specialty consultation networks market captured the largest revenue share of 81% in 2025 within North America, fueled by the rapid uptake of connected health devices and telehealth adoption. For instance, Mayo Clinic’s virtual rheumatology platform enables patients across rural regions to consult specialists for autoimmune disorders without traveling long distances. AI-enabled platforms are used to predict patient risks and monitor chronic conditions in real-time, enhancing the efficiency of virtual specialty consultations. For example, Cleveland Clinic’s tele-cardiology service uses AI-assisted triage to prioritize urgent cases and improve patient outcomes. Rising patient awareness of digital health tools, coupled with favorable insurance coverage for telemedicine, is increasing the frequency of virtual consultations.

Europe Virtual Specialty Consultation Networks Market Insight

The Europe virtual specialty consultation networks market is projected to expand at a substantial CAGR during the forecast period, primarily driven by stringent healthcare regulations, increasing patient demand for specialty care, and rising digital health adoption. Countries such as Germany and France are integrating telehealth platforms with national EHR systems, improving access to specialists and enabling coordinated care for chronic and complex conditions.

U.K. Virtual Specialty Consultation Networks Market Insight

The U.K. virtual specialty consultation networks market is expected to grow steadily, supported by NHS digital transformation programs, robust telemedicine infrastructure, and rising patient preference for remote specialty consultations. The focus on chronic disease management and preventive care is further encouraging adoption.

Germany Virtual Specialty Consultation Networks Market Insight

Germany virtual specialty consultation networks market is witnessing considerable growth, fueled by high digital literacy, a well-developed healthcare system, and widespread adoption of innovative telehealth technologies. Hospitals are leveraging virtual specialty networks to optimize resources and provide timely care for patients across urban and rural regions.

Asia-Pacific Virtual Specialty Consultation Networks Market Insight

The Asia-Pacific virtual specialty consultation networks market region is poised to grow at the fastest CAGR during 2026–2033, driven by increasing healthcare digitization, rising patient awareness, expanding telemedicine adoption, and growing healthcare expenditure in China, India, and Japan. Government initiatives promoting digital health, rising internet penetration, and growing urban populations are accelerating adoption.

Japan Virtual Specialty Consultation Networks Market Insight

Japan’s virtual specialty consultation networks market high-tech culture, aging population, and demand for convenient healthcare are driving adoption. Integration of IoT and remote monitoring devices with telehealth platforms is improving care delivery for chronic and geriatric patients.

China Virtual Specialty Consultation Networks Market Insight

China virtual specialty consultation networks market accounted for the largest revenue share in the Asia-Pacific region in 2025 due to rapid digitalization, urbanization, and strong government support for telemedicine. Domestic providers are expanding virtual specialty networks, offering affordable access to medical experts with integrated AI platforms enhancing triage and consultation efficiency.

Virtual Specialty Consultation Networks Market Share

The Virtual Specialty Consultation Networks industry is primarily led by well-established companies, including:

- Teladoc Health (U.S.)

- Amwell (U.S.)

- MDLIVE (U.S.)

- Doctor On Demand (U.S.)

- KRY (Sweden)

- Babylon Health (U.K.)

- Ping An Good Doctor (China)

- AliHealth (China)

- WeDoctor (China)

- HealthTap (U.S.)

- 1mg Telemedicine (India)

- Practo (India)

- Maple (Canada)

- CloudMD (Canada)

- MyDoc (Singapore)

- Ada Health (Germany)

- Push Doctor (U.K.)

- Hims & Hers Health (U.S.)

Latest Developments in Global Virtual Specialty Consultation Networks Market

- In October 2024, India’s telecom experts emphasized how 5G deployment combined with AI is bridging healthcare gaps, enabling telemedicine hubs to connect remote patients with specialists for real‑time diagnostics and virtual care across multiple clinical domains, marking a significant acceleration in virtual specialty consultation networks in emerging markets

- In January 2025, under Project Charaka, telehealth kiosks equipped for vital testing, virtual consultations, and diagnostics were launched in India, integrating with the Ayushman Bharat Digital Mission to deepen national telehealth penetration and specialist access for underserved populations

- In April 2025, Saudi Arabia launched Seha Virtual Hospital, a digital care model leveraging AI‑driven diagnosis, e‑ICU services, and wearable integration to extend specialist consultation capabilities nationwide — a major national growth milestone in virtual specialty care infrastructure

- In March 2025, Teladoc Health launched an advanced AI‑triaged virtual primary care service integrating predictive algorithms for early detection and automated care routing, expanding specialist virtual support including chronic disease and mental health management across North America and Europe

- In November 2025, the tele‑consulting services market was reported to be rapidly expanding — with global tele‑consulting services valued at over USD 31 billion in 2024 and projected to reach USD 118.50 billion by 2032, driven by increased chronic disease management, specialist virtual consultations, and broader digital care adoption

- In July 2025, industry analysis highlighted substantial growth in the global telehealth and virtual care industry, with the broader telehealth market estimated at over USD 123 billion in 2024 and rapidly expanding due to rising adoption of virtual consultations across cardiology, behavioral health, radiology, and other specialties

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.