Global Von Willebrand Disease Market

Market Size in USD Million

USD

584.62 Million

USD

931.10 Million

2024

2032

USD

584.62 Million

USD

931.10 Million

2024

2032

| 2025 - 2032 | |

| USD 584.62 Million | |

| USD 931.10 Million | |

| % | |

|

Von Willebrand Disease (Factor VIII Deficiency) Market Size

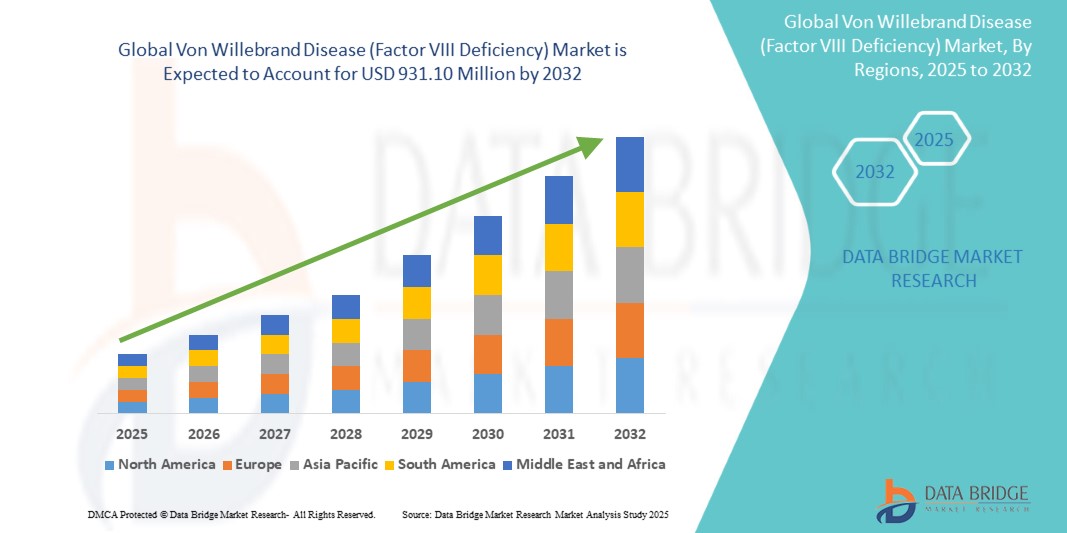

- The Global Von Willebrand Disease (Factor VIII Deficiency) Market size was valued at USD 584.62 Million in 2024 and is expected to reach USD 931.10 Million by 2032, at a CAGR of 5.99 %during the forecast period

- This growth is driven by factors such as the rising prevalence of Von Willebrand Disease, increased awareness and diagnosis rates, growing demand for targeted therapies, and advancements in genetic testing and coagulation disorder diagnostics

Von Willebrand Disease (Factor VIII Deficiency) Market Analysis

- Von Willebrand Disease (Factor VIII Deficiency) is a genetic haematological bleeding illness caused by a lack of von Willebrand factors, which are faulty clotting proteins in the blood. It produces prolonged or heavy bleeding and affects both men and women equally. Frequent and prolonged nose bleeding, easy bruising, and heavy bleeding after surgery or dental work are common signs and symptoms of Von Willebrand disease.

- The demand for Von Willebrand Disease (Factor VIII Deficiency) is significantly driven by the rising prevalence of bleeding disorders, increasing awareness through public health initiatives, and advancements in diagnostic technologies such as genetic testing and factor assays.

- North America is expected to dominate the Von Willebrand Disease (Factor VIII Deficiency) market with a share of 36.4%, attributed to advanced healthcare infrastructure, high adoption of innovative hematology diagnostics, and the strong presence of leading biopharmaceutical companies specializing in rare bleeding disorders

- Asia-Pacific is projected to be the fastest-growing region in the Von Willebrand Disease (Factor VIII Deficiency) market during the forecast period due to rapid improvements in healthcare access, growing awareness of bleeding disorders, and increasing availability of specialized treatments

- The Type 1 Von Willebrand Disease segment is expected to lead the market with a share of 34.5% owing to its higher prevalence, early diagnosis rates, and established treatment protocols. The widespread use of desmopressin and factor replacement therapies for Type 1 cases, along with clinician familiarity, supports its dominant position in the market

Report Scope and Von Willebrand Disease (Factor VIII Deficiency) Market Segmentation

|

Attributes |

Von Willebrand Disease (Factor VIII Deficiency) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Von Willebrand Disease (Factor VIII Deficiency) Market Trends

“Rising Adoption of Genetic and Molecular Diagnostics”

- One prominent trend in Von Willebrand Disease (Factor VIII Deficiency) is the rising adoption of genetic and molecular diagnostics

- This shift is driven by the need for more accurate and earlier diagnosis of inherited bleeding disorders, allowing for tailored treatment approaches and better disease management

- For instance, many specialized healthcare centers are incorporating next-generation sequencing (NGS) and multiplex PCR panels to identify mutations in the VWF gene, helping distinguish between different types of the disease and ensuring patients receive the most appropriate therapy

- This trend is significantly improving diagnostic precision, reducing misclassification of disease types, and enabling personalized treatment plans based on genetic profiles

- The Von Willebrand Disease (Factor VIII Deficiency) market is expected to benefit from continued investment in molecular diagnostics, supporting the early identification of at-risk individuals and the development of more targeted therapeutic strategies worldwide

Von Willebrand Disease (Factor VIII Deficiency) Market Dynamics

Driver

“Increasing prevalence of Von Willebrand disease (factor VIII deficiency)”

- The increasing prevalence of Von Willebrand Disease (Factor VIII Deficiency) is significantly driving demand for early diagnosis, comprehensive care, and effective long-term treatment strategies

- As awareness of inherited bleeding disorders grows, more individuals are being screened and diagnosed, especially in regions with improving healthcare access and genetic testing capabilities

- The rising number of diagnosed cases has prompted healthcare providers and policymakers to prioritize specialized hematology services and ensure availability of essential treatments like desmopressin, factor concentrates, and gene therapy research

- This growing disease burden underscores the need for robust healthcare infrastructure, patient education programs, and ongoing research to address diverse disease types and severities

- With more cases being detected across all age groups, the market is seeing increased investments in targeted therapies and comprehensive disease management approaches

For instance,

- a recent CDC report highlighted that Von Willebrand Disease is one of the most common inherited bleeding disorders, affecting up to 1% of the global population, with many cases still underdiagnosed or misclassified. This has led to increased funding for diagnostic programs and public health initiatives in countries like the U.S., U.K., and Germany

- As the prevalence continues to rise, the Von Willebrand Disease (Factor VIII Deficiency) market is expected to expand steadily, fueled by improved awareness, early intervention, and advancements in therapeutic solutions

Opportunity

“Increase in the number of research and development activities”

- The increase in research and development activities is significantly contributing to the advancement of Von Willebrand Disease (Factor VIII Deficiency) diagnostics and treatment

- Pharmaceutical companies, academic institutions, and healthcare organizations are heavily investing in R&D to discover novel therapies, improve existing treatment protocols, and develop gene-based solutions for long-term disease management

- These efforts are accelerating innovation in recombinant factor therapies, gene therapies, and precision diagnostics, aiming to reduce bleeding episodes, enhance patient quality of life, and improve treatment adherence

For instance,

- Takeda Pharmaceuticals has initiated multiple clinical trials focusing on next-generation recombinant von Willebrand factor (rVWF) therapies to improve treatment outcomes for patients with both Type 1 and Type 3 VWD, particularly those who are unresponsive to desmopressin

- The rise in R&D activities not only supports scientific breakthroughs but also opens up new opportunities for market expansion, especially as regulators prioritize orphan drug development and faster approvals for rare bleeding disorder

Restraint/Challenge

“High Cost of Treatment and Limited Access to Advanced Therapies”

- The high cost of Von Willebrand Disease (Factor VIII Deficiency) treatments presents a significant challenge for market growth, particularly in low- and middle-income countries. Advanced therapies such as recombinant von Willebrand factor and gene therapies can be prohibitively expensive, limiting patient access

- These specialized treatments often involve high production costs, cold chain logistics, and long-term clinical monitoring, which add to the financial burden on healthcare systems and patients

- Smaller hospitals and healthcare providers with limited budgets may be unable to offer the latest therapies, leading to continued reliance on older, less effective treatment options like plasma-derived concentrates or desmopressin in suboptimal cases

For instance,

- In many parts of Africa and Southeast Asia, the high cost of recombinant therapies prevents widespread adoption, forcing clinicians to depend on less advanced therapies that may not be suitable for all patients, especially those with severe or unresponsive Von Willebrand Disease

- As a result, financial constraints and disparities in healthcare access continue to hinder equitable treatment availability, posing a restraint to the global Von Willebrand Disease (Factor VIII Deficiency) market’s growth and limiting innovation uptake in under-resourced regions

Von Willebrand Disease (Factor VIII Deficiency) Market Scope

The market is segmented on the basis of type, drugs, route of administration, end-users and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Drugs |

|

|

By Route of Administration |

|

|

By End User |

|

|

By Usage |

|

In 2025, the Type 1 von Willebrand Disease is projected to dominate the market with a largest share in type segment

The Type 1 von Willebrand Disease segment is expected to dominate the Von Willebrand Disease (Factor VIII Deficiency) market with the largest share of 34.5% in 2025 due to its high prevalence, ease of diagnosis, and effective response to first-line treatments such as desmopressin. Type 1 is the most common and typically mildest form of the disease, making it more frequently identified and managed through standardized protocols. Its relatively straightforward treatment approach and widespread clinical familiarity contribute to its continued dominance. While advanced therapies are emerging for more severe types, the consistent clinical outcomes and accessibility of care for Type 1 patients reinforce its leading position in the market.

The Antihemophilic Factor/Von Willebrand Factor Complex is expected to account for the largest share during the forecast period in drugs segment

In 2025, the Antihemophilic Factor/Von Willebrand Factor Complexs segment is expected to dominate the market due to its effectiveness in treating severe cases of Von Willebrand Disease, particularly in Type 2 and Type 3 patients. These therapies offer superior treatment outcomes by restoring both factor VIII and Von Willebrand factor levels, making them essential for managing bleeding episodes in individuals with more severe forms of the disease. The increasing adoption of these complex therapies is fueled by their ability to provide long-lasting protection against bleeding and reduce the frequency of treatment. The growing demand for personalized, targeted therapies and supportive clinical evidence will continue to drive the segment’s growth.

Von Willebrand Disease (Factor VIII Deficiency) Market Regional Analysis

“North America Holds the Largest Share in the Von Willebrand Disease (Factor VIII Deficiency) Market”

- North America dominates the Von Willebrand Disease (Factor VIII Deficiency) market with a share of 36.4%, driven by advanced healthcare infrastructure, the high adoption of cutting-edge treatment options, and the strong presence of key pharmaceutical and biotechnology companies

- The U.S. holds a significant share of 78.3%, due to the widespread use of advanced therapies like antihemophilic factor/Von Willebrand factor complexes, driven by the growing demand for effective treatment of severe bleeding disorders and the high prevalence of Von Willebrand Disease.

- The presence of leading companies, such as Takeda, Bayer, and Novo Nordisk, alongside ongoing clinical advancements, continues to drive innovation in treatment options. Additionally, significant investments in research and development (R&D) ensure the continuous improvement of therapeutic options and personalized care for Von Willebrand Disease patients.

- The rising prevalence of Von Willebrand Disease and increasing demand for personalized treatment options support market growth in North America. As healthcare standards improve and more effective therapies emerge, the demand for innovative treatment solutions will solidify North America’s dominant position in the market.

“Asia-Pacific is Projected to Register the Highest CAGR in the Von Willebrand Disease (Factor VIII Deficiency) Market”

- The Asia-Pacific region is expected to witness the highest growth rate in the Von Willebrand Disease (Factor VIII Deficiency) market, driven by rapid improvements in healthcare infrastructure, increasing awareness of the disease, and rising procedure volumes

- Countries such as China, India, and Japan are emerging as key markets for Von Willebrand Disease treatment due to the rising incidence of bleeding disorders and the growing demand for advanced therapeutic options. Increased awareness and early diagnosis are driving the adoption of recombinant therapies and factor replacement treatments in these regions.

- • Japan, with its advanced medical infrastructure, remains a critical market for Von Willebrand Disease treatments. The country continues to lead in the adoption of cutting-edge factor replacement therapies, enhancing the effectiveness and safety of treatment options for patients with bleeding disorders.

- • The growing focus on healthcare improvements and comprehensive care for patients with Von Willebrand Disease is expected to drive demand for innovative treatments, positioning the APAC region as the fastest-growing market for these therapies.

Von Willebrand Disease (Factor VIII Deficiency) Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Novo Nordisk A/S (Denmark),

- Sun Pharmaceutical Industries Ltd. (Mumbai),

- Zydus Cadila (Ahmedabad), Baxter (US),

- Glenmark Pharmaceuticals Limited (India),

- Bausch Health Companies Inc. (Canada),

- Bayer AG (Germany), Mylan N.V. (US),

- Teva Pharmaceutical Industries Ltd.(Jerusalem),

- Sanofi (France), Pfizer Inc. (US),

- GlaxoSmithKline plc (UK),

- Novartis AG (Switzerland),

- F. Hoffmann-La Roche Ltd. (Switzerland),

- Merck & Co., Inc. (US),

- Allergan (Ireland),

- Cipla Inc. (US),

- Abbott (US),

- AbbVie Inc. (US),

- Merck KGaA (Germany),

- Amneal Pharmaceuticals LLC. (US),

- Boehringer Ingelheim International GmbH. (Germany)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.