Global Wearable Diagnostic Devices Market

Market Size in USD Billion

USD

70.00 Billion

USD

410.00 Billion

2025

2033

USD

70.00 Billion

USD

410.00 Billion

2025

2033

| 2026 - 2033 | |

| USD 70.00 Billion | |

| USD 410.00 Billion | |

| % | |

|

Wearable Diagnostic Devices Market Size

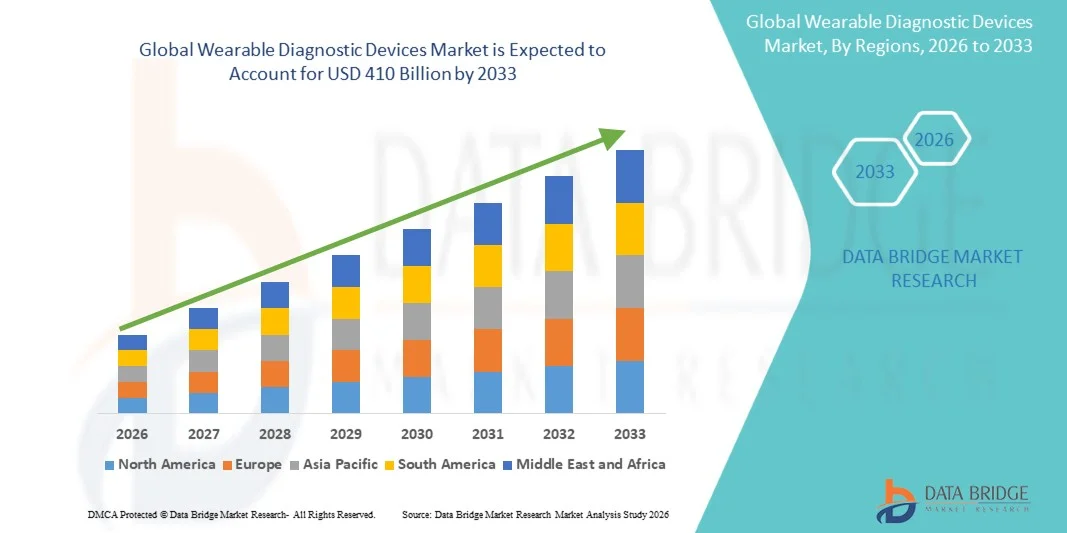

- The global wearable diagnostic devices market size was valued at USD 70 billion in 2025and is expected to reach USD 410 billion by 2033, at a CAGR of 24.7% during the forecast period

- The market growth is primarily driven by the rapid expansion of remote patient monitoring, increasing adoption of wearable medical devices, and rising burden of chronic diseases such as cardiovascular disorders, diabetes, and respiratory conditions.

- In addition, advancements in biosensor technology, artificial intelligence (AI)-enabled diagnostics, and IoT-based healthcare ecosystems are significantly transforming disease detection, monitoring, and preventive care, thereby accelerating global market adoption.

Wearable Diagnostic Devices Market Analysis

- Digital diagnostics refers to the use of connected devices, smart sensors, and AI-powered platforms to continuously monitor physiological parameters, enabling real-time disease detection, early intervention, and personalized healthcare delivery.

- The growing shift toward preventive healthcare and decentralized care models is significantly increasing the adoption of wearable diagnostic devices across hospitals, homecare settings, and individual consumers.

- Rising demand for remote patient monitoring solutions is being fueled by aging populations, increasing healthcare costs, and the need to reduce hospital readmissions for chronic disease patients.

- North America dominated the digital diagnostics market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, strong digital health adoption, and widespread use of wearable monitoring technologies.

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, registering a CAGR of approximately 27%, driven by rapid urbanization, expanding digital health infrastructure, and increasing healthcare investments in countries such as China and India.

- The vital signs monitoring devices segment dominated the market with the largest revenue share of approximately 34.6% in 2025, driven by their widespread use for continuous monitoring of essential physiological parameters such as heart rate, blood pressure, temperature, and oxygen saturation across hospitals, clinics, and homecare settings. These devices are widely adopted due to their ease of use, non-invasive nature, and strong clinical utility in both preventive and emergency care.

Report Scope and Wearable Diagnostic Devices Market Segmentation

|

Attributes |

Wearable diagnostic devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of AI-powered predictive diagnostics for early disease detection and risk stratification · Rising adoption of wearable biosensors for continuous health monitoring in non-clinical environments |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Wearable Diagnostic Devices Market Trends

“Shift Toward AI-Enabled, Connected, and Preventive Healthcare Ecosystems”

- A major trend in the global digital diagnostics market is the transition toward AI-integrated wearable devices that provide continuous health monitoring and predictive insights, enabling earlier detection of health risks and more proactive disease management.

- Devices such as smartwatches and biosensor patches are increasingly capable of detecting early signs of arrhythmias, sleep disorders, and metabolic abnormalities, supporting continuous and non-invasive monitoring of key physiological parameters.

- Integration of cloud computing and IoT enables seamless transmission of patient data to healthcare providers, improving real-time decision-making, remote patient monitoring, and reducing emergency interventions through timely alerts and interventions.

- Growing consumer adoption of fitness and health tracking devices is blurring the line between medical diagnostics and consumer wellness technologies, as more users rely on wearable devices for both preventive healthcare and lifestyle management.

- Increasing use of AI-driven analytics platforms is enhancing diagnostic accuracy and enabling personalized treatment recommendations based on continuous data collection and advanced pattern recognition.

- Demand for non-invasive and minimally disruptive monitoring solutions is rapidly increasing across both clinical and homecare environments, driven by patient preference for comfort, convenience, and long-term health tracking.

Wearable Diagnostic Devices Market Dynamics

Driver

“Rising Burden of Chronic Diseases and Expansion of Remote Monitoring Ecosystems”

- The increasing prevalence of chronic diseases such as cardiovascular disorders, diabetes, and neurological conditions is a major driver of the digital diagnostics market, as these conditions require continuous monitoring and timely intervention to prevent complications and improve patient outcomes.

- Healthcare systems are increasingly adopting remote monitoring solutions to reduce hospital burden, optimize resource utilization, and improve long-term disease management outcomes through continuous patient data tracking and early clinical response.

- For instance, wearable cardiac monitors and continuous glucose monitoring devices are being widely deployed for real-time patient tracking and early intervention, enabling healthcare providers to detect abnormalities faster and adjust treatment plans proactively.

- Rising healthcare costs and shortage of clinical infrastructure are accelerating the shift toward home-based diagnostics and telehealth platforms, allowing patients to receive quality care outside traditional hospital settings while reducing overall system pressure.

- Government initiatives promoting digital health infrastructure and telemedicine adoption are further supporting market expansion globally by encouraging integration of connected health technologies into mainstream healthcare delivery systems.

Restraint/Challenge

“Data Privacy Concerns and Device Accuracy Limitations”

- Concerns regarding patient data security and privacy in cloud-connected diagnostic systems remain a significant challenge for market growth, as increasing volumes of sensitive health data are transmitted and stored across digital platforms.

- Variability in device accuracy and potential inconsistencies in biosensor readings can affect clinical decision-making reliability, particularly when wearable devices are used for continuous or long-term patient monitoring outside clinical settings.

- High costs associated with advanced AI-enabled diagnostic wearables limit adoption in price-sensitive regions, restricting access to advanced digital health technologies in low- and middle-income markets.

- Lack of standardized regulatory frameworks for digital health devices creates delays in product approvals and commercialization, as manufacturers must navigate varying compliance requirements across different regions.

- Limited digital literacy among elderly populations can hinder effective adoption of remote monitoring technologies, reducing the potential benefits of home-based diagnostics and continuous health tracking solutions.

Wearable diagnostic devices Market Scope

The market is segmented on the basis of product, technology, application, and end user.

- By Product

On the basis of product, the global wearable diagnostic devices market is segmented into vital signs monitoring devices, cardiac monitoring devices, sleep monitoring devices, neuromonitoring devices, fetal & obstetric monitoring devices, and activity & fitness monitoring devices. The vital signs monitoring devices segment dominated the market with the largest revenue share of approximately 34.6% in 2025, driven by their widespread use for continuous monitoring of essential physiological parameters such as heart rate, blood pressure, temperature, and oxygen saturation across hospitals, clinics, and homecare settings. These devices are widely adopted due to their ease of use, non-invasive nature, and strong clinical utility in both preventive and emergency care.

The cardiac monitoring devices segment is expected to witness the fastest growth during the forecast period, fueled by the rising prevalence of cardiovascular diseases, increasing adoption of remote cardiac monitoring solutions, and growing demand for early detection of arrhythmias and heart-related complications. Continuous innovation in ECG patches, wearable Holter monitors, and real-time cardiac alert systems is further expanding this segment’s adoption across both clinical and homecare environments.

- By Technology

On the basis of technology, the market is segmented into biosensors-based wearables, wireless communication (Bluetooth, IoT-enabled devices), AI-integrated diagnostic wearables, and cloud-connected monitoring systems. The biosensors-based wearables segment dominated the market in 2025 due to their critical role in capturing real-time physiological signals with high accuracy and enabling continuous health tracking in compact, patient-friendly devices.

The AI-integrated diagnostic wearables segment is expected to register the fastest growth during the forecast period, driven by increasing demand for predictive healthcare, automated anomaly detection, and personalized health insights. Integration of AI algorithms with wearable devices is significantly enhancing diagnostic accuracy and enabling early intervention for chronic and acute conditions.

- By Application

On the basis of application, the market is segmented into remote patient monitoring, home healthcare, sports & fitness monitoring, and chronic disease management. The remote patient monitoring segment dominated the market in 2025, supported by the growing need for continuous health tracking outside hospital settings, increasing chronic disease burden, and rising adoption of telehealth platforms.

The chronic disease management segment is expected to witness the fastest growth during the forecast period, driven by the increasing prevalence of diabetes, cardiovascular diseases, and respiratory disorders requiring long-term monitoring and timely intervention. Wearable diagnostic devices are playing a critical role in improving treatment adherence and reducing hospital readmissions.

- By End User

On the basis of end user, the market is segmented into hospitals & clinics, home care settings, ambulatory care centers, and individual consumers. The hospitals & clinics segment dominated the market in 2025 due to high adoption of wearable diagnostic devices for continuous patient monitoring, post-operative care, and critical condition management. Strong clinical integration and physician-led monitoring protocols further support this dominance.

The home care settings segment is expected to witness the fastest growth during the forecast period, driven by increasing patient preference for at-home healthcare, rising geriatric population, and growing availability of user-friendly wearable diagnostic devices. Expanding telehealth services and remote monitoring infrastructure are further accelerating adoption in this segment.

Wearable Diagnostic Devices Market Regional Analysis

- North America dominated the digital diagnostics market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, strong digital health adoption, and widespread use of wearable monitoring technologies.

- The region benefits from a high concentration of leading medical device and digital health companies, which continuously drive innovation in AI-powered diagnostics, remote patient monitoring systems, and connected healthcare ecosystems, accelerating early adoption across clinical and consumer segments.

- Favorable reimbursement frameworks and strong government support for telehealth and remote patient monitoring programs are further enhancing the adoption of digital diagnostic solutions, particularly for chronic disease management and post-acute care monitoring.

U.S. Wearable Diagnostic Devices Market Insight

The U.S. wearable diagnostic devices market is highly advanced and is driven by strong adoption of digital health technologies, high healthcare spending, and widespread use of smart wearables for chronic disease management and preventive care. The presence of leading companies such as Apple Inc., Fitbit (Google), and Medtronic further accelerates innovation in AI-enabled monitoring devices. Increasing prevalence of cardiovascular diseases, diabetes, and obesity is also fueling demand for continuous monitoring solutions, while strong reimbursement frameworks and regulatory support are enabling rapid commercialization of advanced wearable diagnostic technologies.

Europe Wearable Diagnostic Devices Market Insight

The Europe wearable diagnostic devices market is expanding steadily, supported by growing emphasis on preventive healthcare, aging population, and increasing government initiatives for digital health adoption. Countries such as France, Italy, and the Nordics are increasingly integrating wearable monitoring systems into national healthcare programs. Strong regulatory frameworks from the European Medicines Agency (EMA) ensure high device safety and quality standards, while rising adoption of remote patient monitoring solutions is improving chronic disease management across the region.

U.K. Wearable Diagnostic Devices Market Insight

The U.K. wearable diagnostic devices market is witnessing strong growth due to the National Health Service (NHS) initiatives promoting digital health and remote patient monitoring. Increasing use of wearable devices for cardiac monitoring, diabetes management, and elderly care is driving adoption across healthcare systems. The country is also investing in AI-driven healthcare solutions and telemedicine platforms, which is further supporting the integration of wearable diagnostic technologies into routine clinical workflows.

Germany Wearable Diagnostic Devices Market Insight

Germany represents one of the most advanced markets in Europe for wearable diagnostic devices, driven by strong healthcare infrastructure, high technological adoption, and focus on precision medicine. The country is increasingly using wearable devices for cardiovascular monitoring and post-operative care. Supportive government policies for digital healthcare transformation and collaborations between medtech companies and research institutions are accelerating innovation and adoption of advanced biosensor-based diagnostic wearables.

Asia-Pacific Wearable Diagnostic Devices Market Insight

The Asia-Pacific wearable diagnostic devices market is the fastest-growing globally, fueled by rising healthcare awareness, increasing chronic disease burden, and rapid digital transformation in healthcare systems. Countries such as China, India, Japan, and South Korea are investing heavily in smart healthcare infrastructure and affordable wearable technologies. Expanding middle-class population and increasing smartphone penetration are also driving adoption of connected health devices for fitness tracking, chronic disease monitoring, and preventive healthcare.

Japan Wearable Diagnostic Devices Market Insight

Japan’s wearable diagnostic devices market is driven by its aging population, advanced healthcare system, and strong adoption of robotics and sensor technologies. Wearable devices are widely used for elderly care, cardiovascular monitoring, and mobility tracking. The country’s focus on precision healthcare and integration of IoT-based medical devices into hospitals and homecare settings is further enhancing adoption of advanced diagnostic wearables.

India Wearable Diagnostic Devices Market Insight

India’s wearable diagnostic devices market is growing rapidly due to increasing prevalence of chronic diseases, rising healthcare awareness, and expanding digital health ecosystem. Affordable fitness trackers and health monitoring wearables are gaining popularity among urban consumers. Government initiatives promoting telemedicine and digital health platforms, along with growing smartphone penetration, are supporting widespread adoption of wearable diagnostic solutions for preventive and remote healthcare monitoring.

Wearable Diagnostic Devices Market Share

The Wearable diagnostic devices industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Philips (Netherlands)

- GE HealthCare (U.S.)

- Siemens Healthineers (Germany)

- Abbott Laboratories (U.S.)

- Samsung Electronics (South Korea)

- Apple Inc. (U.S.)

- iRhythm Technologies (U.S.)

- BioTelemetry (Philips BioTel) (U.S.)

- Masimo (U.S.)

- AliveCor (U.S.)

- Dexcom (U.S.)

What are the Recent Developments in Global Wearable Diagnostic Devices Market?

- In May 2026, Samsung Electronics demonstrated a breakthrough in wearable preventive diagnostics using its Galaxy Watch platform, where an AI-powered algorithm developed with Chung-Ang University Hospital successfully predicted vasovagal syncope (fainting episodes) up to 5 minutes in advance using heart rate variability data, marking a major step toward predictive wearable healthcare.

- In January 2026, Medtronic received FDA clearance for its MiniMed Go™ Smart MDI system integrating the Instinct continuous glucose monitoring sensor (developed with Abbott), enabling real-time wearable-based insulin dosing insights and strengthening its AI-driven chronic disease monitoring ecosystem.

- In September 2025, Philips expanded its patient monitoring portfolio through a strategic partnership with Medtronic to integrate advanced wearable-enabled monitoring technologies, including pulse oximetry, capnography, and brain monitoring systems, enhancing hospital-to-home continuous diagnostics capabilities.

- In November 2025, Medtronic reported clinical advancements in its cardiac wearable diagnostics ecosystem, including real-world performance results for its Aurora EV-ICD system and OmniaSecure defibrillation lead, reinforcing its leadership in implantable and wearable cardiac monitoring technologies.

- In December 2025, academic and industry research highlighted new wearable AI diagnostic models such as Samsung Galaxy Watch-based “SweetDeep,” which achieved over 82% accuracy in non-invasive diabetes screening using real-world physiological data, demonstrating rapid progress in consumer wearable-based disease detection.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.