Global Welding Equipment Market

Market Size in USD Billion

USD

37.40 Billion

USD

54.42 Billion

2025

2033

USD

37.40 Billion

USD

54.42 Billion

2025

2033

| 2026 - 2033 | |

| USD 37.40 Billion | |

| USD 54.42 Billion | |

| % | |

|

Welding Equipment Market Overview

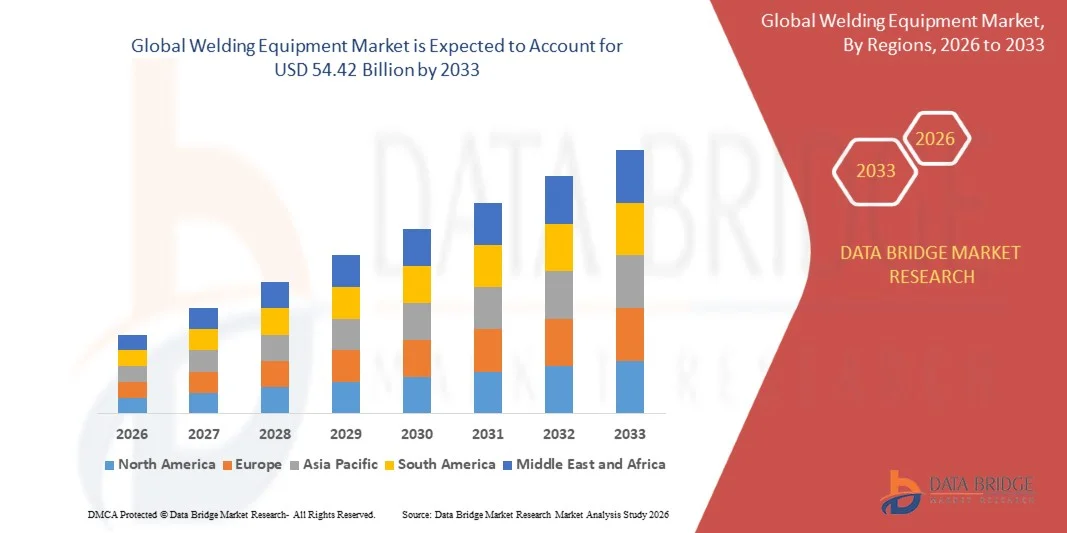

The Welding Equipment Market was valued at USD 37.40 billion in 2025 and is projected to reach USD 54.42 billion by 2033, growing at a CAGR of 4.80% from 2026 to 2033. The market is witnessing steady growth driven by increasing industrialization, rising demand from construction and infrastructure development activities, and expanding applications across automotive manufacturing, shipbuilding, and heavy engineering sectors.

The growing emphasis on automation and precision-based manufacturing is accelerating the adoption of advanced welding technologies such as robotic welding systems, laser welding, and inverter-based equipment. In addition, the rising need for efficient metal joining solutions in energy infrastructure, oil and gas projects, and repair and maintenance activities is further supporting market expansion globally.

Key Market Trends & Insights

- North America dominated the welding equipment market with the largest revenue share of 35.6% in 2025, supported by strong industrial infrastructure, advanced manufacturing capabilities, and high adoption of automation in automotive, aerospace, and energy industries.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 6.1% from 2026 to 2033. Growth is driven by rapid industrialization, expanding construction activities, strong automotive manufacturing base, and increasing investments in infrastructure development projects across emerging economies such as China, India, and Southeast Asia.

- The Arc Welding segment held the largest market revenue share of approximately 42.6% in 2025 driven by its extensive usage in construction, shipbuilding, automotive manufacturing, and heavy fabrication industries due to its versatility, strong joint formation, and cost-effectiveness across diverse metal types. Arc welding processes such as SMAW and MIG/MAG are widely adopted in both industrial and field applications where durability and structural strength are critical.

- The Resistance Welding segment is projected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033 driven by increasing adoption in automotive body assembly lines and mass production environments where high-speed, repeatable, and clean welding operations are required. Rising deployment of spot welding and seam welding technologies in electric vehicle manufacturing is further accelerating segment expansion.

- The Metal Welding segment held the largest market revenue share of approximately 71.3% in 2025 driven by its dominant use in infrastructure development, automotive production, and industrial fabrication where steel, aluminum, and alloy joining is essential for structural integrity and durability.

- The Plastic Welding segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033 driven by increasing demand in automotive lightweight components, electronics enclosures, and medical device manufacturing where precision joining of thermoplastics is required for miniaturized and high-performance applications.

- The Manual segment held the largest market revenue share of approximately 48.9% in 2025 driven by its widespread use in small-scale fabrication, repair operations, and construction activities where flexibility and lower equipment cost are key advantages.

- The Automatic segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033 driven by increasing adoption of robotic welding systems in automotive manufacturing, aerospace production, and large-scale industrial facilities aiming to improve productivity, precision, and operational efficiency.

- The Industrial segment held the largest market revenue share of approximately 78.5% in 2025 driven by strong demand from manufacturing plants, construction projects, energy infrastructure, and heavy engineering industries requiring large-scale welding operations.

- The Commercial segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033 driven by rising adoption in commercial construction, maintenance services, and small fabrication workshops supporting urban infrastructure development and repair activities.

- The Construction segment held the largest market revenue share of approximately 28.7% in 2025 driven by large-scale infrastructure projects such as bridges, buildings, metro rail systems, and industrial facilities requiring extensive welding applications for structural assembly.

- The Automotive segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033 driven by increasing adoption of robotic welding systems in electric vehicle production, lightweight vehicle structures, and high-precision assembly lines focused on improving efficiency and safety standards.

Market Size & Forecast

- Global Market Value (2025): USD 37.40 Billion

- Expected Market Value (2033): USD 54.42 Billion

- Forecast CAGR (2026–2033): 4.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Welding Equipment Market Segmentation

|

Attributes |

Welding Equipment Key Market Insights |

|

Segments Covered |

· By Process Type: Arc Welding, Braze Welding, Forge Welding, Gas Welding, Resistance Welding, Welding Consumables, and Others · By Material Type: Metal Welding, Glass Welding, Plastic Welding, and Others · By AutomationType: Automatic and Semi-Automatic, Manual · By Application: Residential, Commercial, and Industrial · By End-User: Oil & Gas, Automotive, Aviation & Shipbuilding, Power, Chemicals, Mining, Construction, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Doosan Corporation (South Korea) · Amada (India) Pvt. Ltd (India) · Makino (Japan) · JTEKT Corporation (Japan) · Georg Fischer Ltd (Switzerland) · Komatsu NTC (Japan) · Okuma Corporation (Japan) · HYUNDAI WIA CORP (South Korea) · CHIRON Group SE (Germany) · MAG IAS Gmbh (Germany) · Haas Automation, Inc (U.S.) · GROB-WERKE GmbH & CO.KG (Germany) · SPINNER machine tool factory GmbH (Germany) · YAMAZAKI Mazak Corporation (Japan) · DMG MORI (Germany) |

|

Market Opportunities |

· Expansion Of Infrastructure Development Projects · Rising Adoption Of Automated And Robotic Welding Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Welding Equipment Market Trends

Trend: Growth In Automation Adoption And Advanced Welding Technologies

Increasing demand for high-precision, efficient, and cost-effective metal joining solutions across automotive, construction, aerospace, and heavy engineering sectors is accelerating the shift toward automated welding systems. Traditional manual welding processes often face limitations in consistency, productivity, and safety, encouraging industries to adopt robotic welding, inverter-based systems, and digitally controlled welding equipment.

In modern automotive manufacturing, companies are increasingly integrating robotic welding cells into assembly lines to enhance production speed and ensure uniform weld quality, such as in body-in-white fabrication where precision and repeatability are critical for vehicle safety standards. In shipbuilding and heavy fabrication industries, automated submerged arc welding systems are being widely used to improve productivity and reduce material wastage while handling large-scale structural components.

The expansion of infrastructure development projects, including metro rail networks, bridges, and industrial plants, is further increasing demand for portable and high-efficiency welding machines capable of operating in diverse field conditions. In addition, advancements in inverter technology and hybrid welding systems are enabling lower energy consumption and improved arc stability, supporting sustainable manufacturing goals.

Welding Equipment Market Dynamics

Key Market Driver: Rising Industrialization And Infrastructure Expansion

Rapid industrialization across emerging and developed economies is significantly driving demand for welding equipment across construction, manufacturing, and energy sectors. Large-scale infrastructure projects, including transportation networks, commercial complexes, and industrial facilities, require extensive welding applications for structural fabrication and assembly.

Industries such as automotive and construction are increasingly deploying advanced welding technologies, such as MIG, TIG, and robotic welding systems, to improve productivity and ensure high-strength joint formation in critical applications. For instance in automotive manufacturing, automated welding systems are widely used in chassis and body assembly lines to meet high-volume production requirements while maintaining safety and quality standards.

Similarly, energy and oil and gas sectors rely heavily on welding equipment for pipeline construction, refinery maintenance, and offshore platform development, where durable and high-performance welding solutions are essential for operational reliability. Large infrastructure initiatives in countries such as India and China, including smart city projects and metro rail expansions, are significantly boosting equipment demand in 2025.

Key Restraint/Challenge: High Equipment Cost And Skilled Labor Shortage

The high initial cost of advanced welding systems, particularly robotic and laser welding equipment, remains a major barrier for small and medium-sized enterprises. Advanced systems require significant capital investment along with ongoing maintenance and software integration costs, limiting adoption in cost-sensitive market.

In addition, the welding industry is facing a shortage of skilled labor capable of operating and maintaining advanced automated systems. Traditional welding skills are often insufficient for modern digital and robotic equipment, creating a gap between technological advancement and workforce readiness.

Industry assessments indicate that automated welding systems can cost several times more than conventional manual equipment, with robotic welding cells often requiring substantial setup investment, which restricts adoption among smaller fabrication units and workshops in developing regions.

Key Market Opportunity: Expansion Of Smart Manufacturing And Robotic Welding Integration

The increasing shift toward Industry 4.0 and smart manufacturing is creating significant opportunities for advanced welding equipment integrated with robotics, sensors, and AI-based monitoring systems. Manufacturers are increasingly adopting connected welding solutions to improve precision, reduce defects, and enhance real-time process control.

Automotive OEMs are expanding the use of robotic welding lines in electric vehicle production, such as battery pack enclosures and lightweight aluminum body structures, to improve structural integrity and production efficiency. In aerospace manufacturing, precision laser welding systems are being adopted for complex component fabrication requiring high accuracy and minimal thermal distortion.

In addition, advancements in welding automation software and real-time monitoring systems are enabling predictive maintenance and quality assurance, reducing downtime and improving operational efficiency. Pilot smart factory implementations in 2025 across Germany and Japan have demonstrated productivity improvements of nearly 20–25% after integrating AI-enabled robotic welding systems in high-volume production environments.

Welding Equipment Market Scope

The market is segmented on the basis of process type, material type, automation type, application, and end-user.

- By Process Type

On the basis of process type, the welding equipment market is segmented into Arc Welding, Braze Welding, Forge Welding, Gas Welding, Resistance Welding, Welding Consumables, and Others. The Arc Welding segment held the largest market revenue share of approximately 42.6% in 2025 driven by its extensive usage in construction, shipbuilding, automotive manufacturing, and heavy fabrication industries due to its versatility, strong joint formation, and cost-effectiveness across diverse metal types. Arc welding processes such as SMAW and MIG/MAG are widely adopted in both industrial and field applications where durability and structural strength are critical.

The Resistance Welding segment is projected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033 driven by increasing adoption in automotive body assembly lines and mass production environments where high-speed, repeatable, and clean welding operations are required. Rising deployment of spot welding and seam welding technologies in electric vehicle manufacturing is further accelerating segment expansion.

- By Material Type

On the basis of material type, the market is segmented into Metal Welding, Glass Welding, Plastic Welding, and Others. The Metal Welding segment held the largest market revenue share of approximately 71.3% in 2025 driven by its dominant use in infrastructure development, automotive production, and industrial fabrication where steel, aluminum, and alloy joining is essential for structural integrity and durability.

The Plastic Welding segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033 driven by increasing demand in automotive lightweight components, electronics enclosures, and medical device manufacturing where precision joining of thermoplastics is required for miniaturized and high-performance applications.

- By Automation Type

On the basis of automation type, the market is segmented into Automatic, Semi-Automatic, and Manual. The Manual segment held the largest market revenue share of approximately 48.9% in 2025 driven by its widespread use in small-scale fabrication, repair operations, and construction activities where flexibility and lower equipment cost are key advantages.

The Automatic segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033 driven by increasing adoption of robotic welding systems in automotive manufacturing, aerospace production, and large-scale industrial facilities aiming to improve productivity, precision, and operational efficiency.

- By Application

On the basis of application, the market is segmented into Residential, Commercial, and Industrial. The Industrial segment held the largest market revenue share of approximately 78.5% in 2025 driven by strong demand from manufacturing plants, construction projects, energy infrastructure, and heavy engineering industries requiring large-scale welding operations.

The Commercial segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033 driven by rising adoption in commercial construction, maintenance services, and small fabrication workshops supporting urban infrastructure development and repair activities.

- By End-User

On the basis of end-user, the market is segmented into Oil & Gas, Automotive, Aviation & Shipbuilding, Power, Chemicals, Mining, Construction, and Others. The Construction segment held the largest market revenue share of approximately 28.7% in 2025 driven by large-scale infrastructure projects such as bridges, buildings, metro rail systems, and industrial facilities requiring extensive welding applications for structural assembly.

The Automotive segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033 driven by increasing adoption of robotic welding systems in electric vehicle production, lightweight vehicle structures, and high-precision assembly lines focused on improving efficiency and safety standards.

Welding Equipment Market Regional Analysis

North America Welding Equipment Market Insight

North America dominated the welding equipment market with the largest revenue share of 35.6% in 2025, supported by strong industrial infrastructure, high adoption of advanced manufacturing technologies, and robust demand from automotive, aerospace, and energy sectors. The region benefits from widespread integration of automated welding systems, strong presence of key manufacturers, and continuous investments in oil & gas pipeline development and infrastructure modernization projects. In addition, the increasing shift toward robotic welding solutions and smart factory adoption is further strengthening market growth across the region.

U.S. Welding Equipment Market Insight

The U.S. welding equipment market captured the largest revenue share in North America in 2025, driven by rapid expansion of automotive production facilities, defense manufacturing programs, and large-scale infrastructure rehabilitation projects. The country’s strong emphasis on advanced manufacturing technologies, including robotic welding cells and laser welding systems, is significantly enhancing productivity and precision in industrial operations. For instance in automotive assembly plants, automated welding lines are widely used for body frame manufacturing and electric vehicle battery enclosure fabrication. Furthermore, the presence of major OEMs and industrial equipment manufacturers continues to support market expansion.

Europe Welding Equipment Market Insight

The Europe welding equipment market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent industrial safety regulations, rising demand for energy-efficient manufacturing processes, and strong adoption of automation across automotive and aerospace sectors. The region’s focus on sustainable manufacturing and carbon reduction initiatives is encouraging the use of inverter-based welding systems and robotic welding technologies. Europe’s advanced shipbuilding industry and growing renewable energy infrastructure projects are further supporting market expansion across industrial applications.

U.K. Welding Equipment Market Insight

The U.K. welding equipment market is expected to witness steady growth from 2026 to 2033, supported by increasing investments in infrastructure development, offshore energy projects, and industrial refurbishment activities. The growing adoption of automated welding systems in construction and manufacturing sectors is improving productivity and reducing labor dependency. In addition, rising demand from aerospace manufacturing hubs and defense production facilities is further contributing to the expansion of advanced welding technologies across the country.

Germany Welding Equipment Market Insight

The Germany welding equipment market is expected to witness strong growth from 2026 to 2033, driven by the country’s leadership in industrial automation, automotive manufacturing, and precision engineering. Germany’s emphasis on Industry 4.0 adoption is accelerating the integration of robotic welding systems and digitally controlled welding equipment in production lines. For instance in automotive manufacturing plants, robotic arc welding systems are widely deployed for high-precision body assembly processes. Furthermore, strong demand from machinery manufacturing and renewable energy infrastructure is supporting sustained market development.

Asia-Pacific Welding Equipment Market Insight

The Asia-Pacific welding equipment market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, urbanization, and large-scale infrastructure development in countries such as China, India, Japan, and South Korea. The region’s expanding automotive manufacturing base, growing construction activities, and rising investments in energy and transportation infrastructure are significantly driving demand for welding equipment. In addition, increasing adoption of automated and semi-automated welding systems in manufacturing industries is further boosting regional market expansion.

Japan Welding Equipment Market Insight

The Japan welding equipment market is expected to witness steady growth from 2026 to 2033 due to the country’s advanced manufacturing ecosystem, strong robotics integration, and high demand for precision engineering solutions. Japan’s automotive and electronics industries are major consumers of automated welding systems, particularly for high-accuracy assembly and miniaturized component fabrication. For instance in automotive production facilities, robotic welding systems are extensively used to ensure consistent quality and efficiency in mass production lines. Moreover, the country’s focus on technological innovation continues to support adoption of next-generation welding technologies.

China Welding Equipment Market Insight

The China welding equipment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid industrial expansion, large-scale infrastructure projects, and strong dominance in manufacturing activities. China’s growing automotive sector, shipbuilding industry, and construction boom are key drivers of welding equipment demand across the country. For instance in major infrastructure projects such as high-speed rail networks and urban metro systems, extensive welding applications are used for structural fabrication and assembly. In addition, the presence of strong domestic manufacturers and increasing automation adoption are further accelerating market growth.

Welding Equipment Market Share

The Welding Equipment industry is primarily led by well-established companies, including:

- Doosan Corporation (South Korea)

- Amada (India) Pvt. Ltd (India)

- Makino (Japan)

- JTEKT Corporation (Japan)

- Georg Fischer Ltd (Switzerland)

- Komatsu NTC (Japan)

- Okuma Corporation (Japan)

- HYUNDAI WIA CORP (South Korea)

- CHIRON Group SE (Germany)

- MAG IAS Gmbh (Germany)

- Haas Automation, Inc (U.S.)

- GROB-WERKE GmbH & CO.KG (Germany)

- SPINNER machine tool factory GmbH (Germany)

- YAMAZAKI Mazak Corporation (Japan)

- DMG MORI (Germany)

Latest Developments in Welding Equipment Market

- In December 2025, Miller Electric Mfg. LLC introduced the Auto Elite wire drive for integration with the Auto Deltaweld system, designed to enhance automated and robotic welding lines by improving arc consistency, simplifying maintenance, and increasing uptime in high-volume production environments

- In September 2025, The Lincoln Electric Company launched the Flex Lase handheld laser welding system aimed at enabling faster and more precise welding operations, reducing heat input, minimizing material distortion, and lowering post-weld finishing requirements across fabrication, automotive, and precision manufacturing sectors

- In September 2023, ESAB introduced the Renegade Volt ES 200i battery-powered welding system in collaboration with Stanley Black & Decker, delivering up to 150A stick output on battery power and up to 200A on 230V supply, enhancing portability, flexibility, and on-site welding efficiency in remote and industrial applications

- In September 2023, Miller Electric Mfg. LLC launched the Millermatic 142 MIG Welder targeting both DIY users and professionals, offering a lightweight design and reliable arc performance that improves welding accessibility, ease of use, and productivity for small-scale fabrication tasks

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Welding Equipment Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Welding Equipment Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Welding Equipment Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.