Global Wilson Disease Market

Market Size in USD Million

USD

599.98 Million

USD

1,007.98 Million

2024

2032

USD

599.98 Million

USD

1,007.98 Million

2024

2032

| 2025 - 2032 | |

| USD 599.98 Million | |

| USD 1,007.98 Million | |

| % | |

|

Wilson Disease Market Size

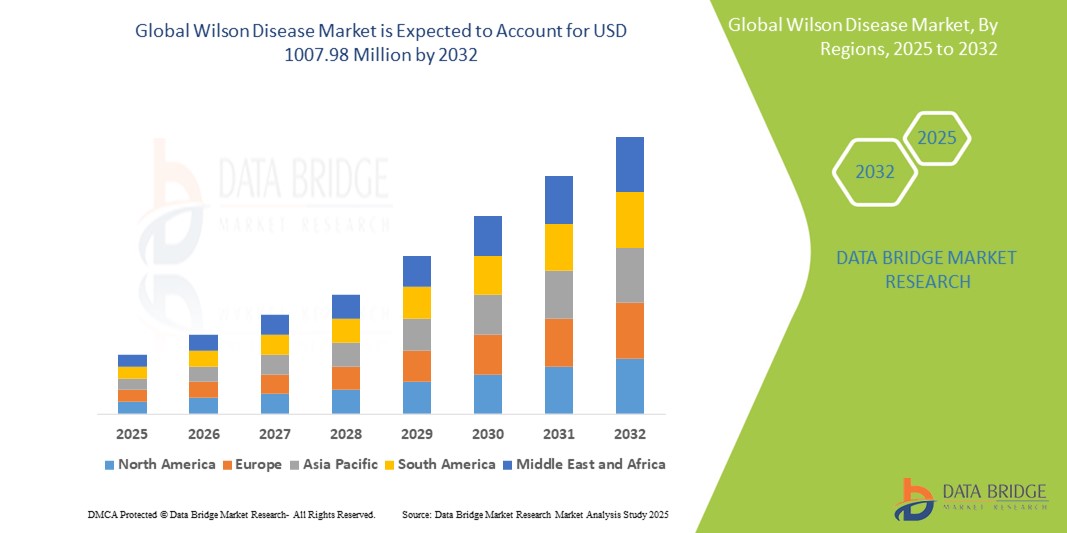

- The global Wilson Disease market size was valued at USD 599.98 million in 2024 and is expected to reach USD 1007.98 million by 2032, at a CAGR of 6.70% during the forecast period

- The market growth is largely fueled by the growing awareness and technological advancements in the diagnosis and treatment of Wilson disease, leading to increased early detection and management in both clinical and homecare settings. Furthermore, the availability of advanced diagnostic tools such as genetic testing, blood and urine analysis, and liver biopsies is enhancing the ability of healthcare providers to identify the condition accurately and promptly, contributing to improved patient outcomes and supporting the overall expansion of the market.

- Furthermore, rising patient and healthcare provider demand for effective, user-friendly, and accessible treatment solutions is establishing pharmacological therapy and supportive care as the preferred management options for Wilson disease. These converging factors are accelerating the adoption of specialized medications and expanding access through diverse distribution channels such as hospital and retail pharmacies, thereby significantly boosting the industry's growth.

Wilson Disease Market Analysis

- Wilson disease, a rare genetic disorder marked by copper accumulation in tissues, is increasingly becoming a focal point in both clinical and diagnostic settings due to its progressive nature, need for early detection, and availability of targeted therapeutic options. Enhanced screening programs, advanced testing technologies such as genetic testing and liver biopsy, and improved clinical awareness are contributing to greater identification and treatment efforts across healthcare systems globally.

- The escalating demand for Wilson disease management is primarily fueled by the rising prevalence of rare genetic disorders, increased government support for rare disease treatment, and a growing preference for non-invasive diagnostic and long-term pharmacological interventions. Patients and healthcare professionals alike are prioritizing early diagnosis and consistent treatment, driving the uptake of specialized medications and monitoring solutions.

- North America dominates the Wilson disease market with the largest revenue share of 40.01% in 2025, characterized by advanced medical infrastructure, strong patient advocacy, and a robust presence of pharmaceutical companies focusing on rare and metabolic disorders, with the U.S. experiencing substantial growth in diagnosis rates and treatment accessibility, particularly in specialized liver and genetic clinics, supported by innovation from both established firms and emerging biotech companies.

- Asia-Pacific is expected to be the fastest growing region in the Wilson disease market during the forecast period due to increasing healthcare investments, better awareness of rare genetic conditions, and expanded access to diagnostic services. Improvements in public health education and regional clinical trials are further supporting the region's rapid growth trajectory.

- The medication segment is expected to dominate the Wilson disease market with a market share of 43.2% in 2025, driven by its efficacy in managing copper levels, preference for oral administration, and long-term benefits in disease control. Chelating agents and zinc-based therapies remain the cornerstone of treatment, supported by ongoing research and the development of novel therapeutic formulations.

Report Scope and Wilson Disease Market Segmentation

|

Attributes |

Wilson Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Wilson Disease Market Trends

“Enhanced Disease Management Through Advanced Diagnostics and Personalized Therapy”

- A significant and accelerating trend in the global Wilson disease market is the deepening integration of advanced diagnostic technologies and personalized treatment strategies. This combination is significantly enhancing early diagnosis and tailored therapy approaches for improved patient outcomes.

- For instance, genetic testing and biochemical assays are now routinely combined to confirm Wilson disease diagnosis with greater accuracy. Similarly, personalized chelation therapies are being developed to better suit individual patient profiles, improving effectiveness and minimizing side effects.

- Advanced diagnostics enable features such as monitoring copper levels and treatment adherence in real time, allowing healthcare providers to optimize therapeutic regimens. Digital health tools are being used to deliver these capabilities, supporting better disease control and management.

- Moreover, integration with electronic health records and rare disease registries facilitates centralized management of patient data, promoting coordinated care among specialists such as hepatologists, neurologists, and genetic counselors.

- This trend toward more precise, integrated, and patient-centric management is reshaping expectations for Wilson disease treatment. Pharmaceutical companies and healthcare providers are increasingly focusing on innovations that combine diagnostics with personalized therapy to enhance quality of life.

- The demand for such advanced diagnostic and therapeutic solutions is growing rapidly across both developed and emerging markets, driven by increased disease awareness, improved healthcare infrastructure, and patient preference for more effective, individualized care.

Wilson Disease Market Dynamics

Driver

“Growing Need Due to Rising Awareness and Advancements in Rare Disease Management”

- The increasing prevalence of awareness about Wilson disease among patients and healthcare providers, coupled with advancements in diagnostic methods and treatment options, is a significant driver for the heightened demand for Wilson disease therapies.

- For instance, in April 2024, some pharmaceutical companies announced developments in genetic testing and biomarker identification to improve early diagnosis and personalized treatment approaches. Such strategies by key companies are expected to drive Wilson disease market growth in the forecast period.

- As patients and clinicians become more aware of the progressive nature of Wilson disease and the importance of early intervention, treatments now offer advanced features such as personalized chelation therapies, liver function monitoring, and improved safety profiles, providing a compelling upgrade over traditional treatment methods.

- Furthermore, the growing availability of diagnostic tools and the desire for integrated care pathways are making Wilson disease management an essential part of rare disease treatment ecosystems, offering seamless coordination between specialists, laboratories, and healthcare providers.

- The convenience of oral medication regimens, regular biochemical monitoring, and remote patient management through digital health platforms are key factors propelling the adoption of Wilson disease treatments in both developed and emerging healthcare markets.

- The trend towards patient-centric care models and the increasing availability of user-friendly treatment options further contribute to the market’s growth, encouraging early diagnosis and improved long-term outcomes for Wilson disease patients.

Restraint/Challenge

“Concerns Regarding Diagnostic Limitations and High Treatment Costs”

- Concerns surrounding limitations in diagnostic accuracy and delayed detection of Wilson disease pose a significant challenge to broader market penetration. As diagnosis relies on complex biochemical tests and genetic analysis, misdiagnosis or late diagnosis remain common, raising anxieties among patients and healthcare providers about treatment effectiveness and disease progression.

- For instance, inconsistent access to advanced diagnostic tools in certain regions has made some clinicians hesitant to fully adopt newer testing protocols, impacting early intervention strategies.

- Addressing these diagnostic challenges through improved testing standards, wider availability of genetic screening, and enhanced clinician training is crucial for building confidence in Wilson disease management. Companies such as Amneal Pharmaceuticals and Teva emphasize the development of comprehensive diagnostic support alongside therapies to reassure healthcare providers and patients. Additionally, the relatively high cost of long-term chelation therapy and liver transplantation can be a barrier to treatment adoption for price-sensitive patients, particularly in developing regions or among uninsured populations. While some generic medications have become more affordable, advanced treatments and ongoing monitoring often come with a higher financial burden.

- While treatment costs are gradually decreasing due to generic drug availability and healthcare subsidies, the perceived expense of lifelong management can still hinder widespread adoption, especially for those without immediate access to specialized care.

- Overcoming these challenges through improved diagnostic technologies, patient education on disease management, and development of cost-effective therapies will be vital for sustained market growth.

Wilson Disease Market Scope

The market is segmented on the basis of test type, treatment, route of administration, end-users, and distribution channel.

- By Test Type

On the basis of test type, the Wilson disease market is segmented into blood and urine test, eye exam, biopsy, genetic testing, and others. The blood and urine test segment dominates the largest market revenue share of 43.2% in 2025, driven by its established role in initial diagnosis and ongoing monitoring of copper levels in patients. Healthcare professionals often prioritize these tests due to their accessibility, cost-effectiveness, and ability to provide quick indicators of copper metabolism. The market also sees strong demand for blood and urine tests due to their routine usage in primary screening and the availability of standardized protocols enhancing diagnostic accuracy and clinical efficiency.

The genetic testing segment is anticipated to witness the fastest growth rate of 21.7% from 2025 to 2032, fueled by increasing awareness of early detection and family screening. Genetic tests offer definitive confirmation of Wilson disease by identifying mutations in the ATP7B gene, making them critical in at-risk populations and for asymptomatic individuals. The expanding use of genetic counseling and the integration of next-generation sequencing in clinical settings also contribute to the rising adoption of genetic testing as a key component in comprehensive disease management strategies.

- By Route of Administration

On the basis of route of administration, the Wilson disease market is segmented into oral, parenteral, and others. The oral segment held the largest market revenue share in 2025, driven by the widespread preference for oral chelating agents such as penicillamine and trientine due to their ease of administration and patient compliance. Oral therapies are often the first line of treatment for long-term management of Wilson disease, offering convenient dosing and effective control of copper accumulation, making them a popular choice in both hospital and homecare settings.

The parenteral segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the growing adoption of intravenous zinc or chelating formulations in acute cases or in patients who are non-responsive to oral therapies. Parenteral administration is particularly valued for its rapid bioavailability and is often used in hospital settings for intensive management. The increasing availability of advanced injectable formulations and supportive care infrastructure is further propelling growth in this segment.

By End Users

On the basis of end-users, the Wilson disease market is segmented into hospitals, homecare, specialty clinics, and others. The hospital segment held the largest market revenue share in 2025, driven by the need for specialized care, diagnostic procedures, and the administration of chelation therapy under clinical supervision. Hospitals are often the primary point of care for initial diagnosis and management of Wilson disease, particularly during acute phases requiring intensive monitoring and treatment, which contributes to their dominance in this segment.

The homecare segment is expected to witness the fastest CAGR from 2025 to 2032, favored for its convenience and cost-effectiveness, especially for patients on long-term maintenance therapy. With oral medications being a cornerstone of Wilson disease treatment, many patients are managed outside clinical settings once stabilized. Increasing awareness, supportive care infrastructure, and the availability of patient-friendly drug formulations are fueling the growth of this segment.

By Application

On the basis of application, the Wilson Disease market is segmented into commercial, residential, industrial, government institution, and others. The residential segment accounted for the largest market revenue share in 2024, driven by the increasing adoption of smart home ecosystems, rising awareness about home security, and the convenience of remote locking/unlocking. Real estate developments and the boom in short-term rentals also encourage adoption.

The commercial segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the growing need for centralized security, employee access control, and audit trails. Businesses benefit from keyless solutions that can be managed remotely, offering flexibility for multiple users and locations.

By Distribution Channel

On the basis of distribution channel, the Wilson disease market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment accounted for the largest market revenue share in 2024, driven by the direct procurement of prescription medications during inpatient treatment and post-diagnosis care. These settings ensure patients receive the necessary chelating agents and supportive drugs under medical supervision, especially during the initiation or modification of therapy.

The online pharmacy segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing digital adoption, improved access to specialty medicines, and convenience for chronic care patients. With the growing trend of telemedicine and homecare, patients and caregivers increasingly rely on online platforms to refill long-term prescriptions, track deliveries, and access discounted pricing for Wilson disease medications.

Wilson Disease Market Regional Analysis

- North America dominates the Wilson disease market with the largest revenue share of 40.01% in 2024, driven by a growing prevalence of genetic disorders and increased awareness about rare liver diseases.

- Patients in the region benefit from early diagnostic capabilities, access to specialized healthcare providers, and availability of FDA-approved treatment options such as chelating agents and zinc salts.

- This widespread adoption is further supported by high healthcare expenditure, strong presence of pharmaceutical companies, and government support for orphan drug development, establishing North America as a key contributor to the diagnosis and treatment of Wilson disease

U.S. Wilson Disease Market Insight

The U.S. Wilson disease market captured the largest revenue share of 81% within North America in 2025, fueled by increased diagnosis rates and growing awareness of rare genetic disorders. Patients and healthcare providers are increasingly prioritizing early intervention through effective chelation therapies and zinc-based treatments. The rising preference for personalized treatment plans, combined with robust demand for novel therapeutic options and improved drug formulations, further propels the Wilson disease treatment market. Moreover, ongoing research advancements and the integration of genetic testing technologies are significantly contributing to the market's expansion

Europe Wilson Disease Market Insight

The European Wilson disease market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing diagnosis rates and the growing emphasis on early disease management. The rise in awareness about rare genetic disorders, coupled with advancements in diagnostic technologies, is fostering the adoption of effective treatment regimens. European healthcare systems are also focused on improving patient outcomes through access to novel therapies and personalized care plans. The region is experiencing significant growth across hospital, specialty clinic, and homecare settings, with Wilson disease treatments being integrated into both established protocols and emerging therapeutic options.

U.K. Wilson Disease Market Insight

The U.K. Wilson disease market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of the disease and the demand for effective management options. Additionally, concerns regarding early diagnosis and long-term complications are encouraging healthcare providers and patients to seek advanced therapeutic solutions. The U.K.’s focus on rare disease research, alongside its well-established healthcare infrastructure and access to innovative treatments, is expected to continue to stimulate market growth.

Germany Wilson Disease Market Insight

The Germany Wilson disease market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of the disease and the demand for advanced, patient-centric therapeutic solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on medical innovation and research, promotes the adoption of novel treatments, particularly in specialized clinics and hospitals. The integration of multidisciplinary care approaches is also becoming increasingly prevalent, with a strong focus on early diagnosis and effective disease management aligning with local healthcare priorities and patient expectations.

Asia-Pacific Wilson Disease Market Insight

Asia-Pacific Wilson disease market is poised to grow at the fastest CAGR of over 24% in 2025, driven by increasing healthcare infrastructure development, rising disposable incomes, and advancements in medical research in countries such as China, Japan, and India. The region's growing focus on rare disease awareness, supported by government initiatives promoting healthcare access and digital health solutions, is driving the adoption of advanced Wilson disease treatments. Furthermore, as APAC emerges as a manufacturing and research hub for pharmaceuticals and biotechnologies, the affordability and accessibility of Wilson disease therapies are expanding to a wider patient base.

Japan Wilson Disease Market Insight

The Japan Wilson disease market is gaining momentum due to the country’s advanced healthcare infrastructure, increasing rare disease awareness, and demand for innovative therapies. The Japanese market places significant emphasis on early diagnosis and effective management, and the adoption of advanced Wilson disease treatments is driven by the growing number of specialized healthcare facilities and research initiatives. The integration of Wilson disease management with digital health platforms and personalized medicine is fueling growth. Moreover, Japan's aging population is likely to spur demand for easier-to-administer, effective treatment options in both hospital and outpatient settings.

China Wilson Disease Market Insight

The China Wilson disease market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's expanding healthcare infrastructure, growing awareness of rare diseases, and increasing rates of medical innovation adoption. China stands as one of the largest markets for rare disease therapies, and Wilson disease treatments are becoming increasingly accessible in hospitals, specialty clinics, and research centers. The push towards improving rare disease diagnosis and treatment, alongside the availability of affordable therapeutic options and strong domestic pharmaceutical manufacturers, are key factors propelling the market in China

Wilson Disease Market Share

The Wilson Disease industry is primarily led by well-established companies, including:

- Amneal Pharmaceuticals LLC (U.S.)

- Meda Pharmaceuticals (U.S.)

- Teva Pharmaceuticals Industries Ltd. (Israel)

- Taj Pharmaceutical Limited (India)

- Ipsen Pharma (France)

- TSUMURA & CO. (Japan)

- Trientine Pharmaceuticals (U.S.)

- Waylivra (Akcea Therapeutics) (U.S.)

- Orphalan SA (France)

- Wilson Therapeutics AB (Sweden)

- Viatris Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Bausch Health Companies Inc. (Canada)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Recordati Rare Diseases (Italy)

- Alexion Pharmaceuticals, Inc. (U.S.)

- Univar Solutions Inc. (U.S.)

- Cymabay Therapeutics (U.S.)

- Apotex Inc. (Canada)

Latest Developments in Global Wilson Disease Market

- In January 2025, Eton Pharmaceuticals announced the acquisition of Galzin (zinc acetate), a drug approved by the FDA for the maintenance treatment of Wilson’s disease. This acquisition underscores Eton's commitment to addressing rare diseases and enhancing patient access to essential therapies. The company plans to commence marketing Galzin in the U.S. in the first quarter of 2025

- In October 2024, Monopar Therapeutics announced an exclusive global licensing agreement with Alexion, AstraZeneca Rare Disease, for ALXN-1840 (bis-choline tetrathiomolybdate), a Phase 3 drug candidate for Wilson’s disease. Monopar will oversee all future development and commercialization efforts, aiming to bring this promising therapy to patients worldwide

- In October 2024, Ultragenyx Pharmaceutical reported encouraging outcomes from Stage 1 of the Phase 1/2/3 Cyprus2+ study of UX701, an investigational gene therapy for Wilson’s disease. The therapy demonstrated significant clinical activity and improved copper metabolism, with several patients discontinuing standard-of-care treatments across all three dose cohorts. A new cohort with a higher dose and optimized immunomodulation will be added to enhance efficacy.

- In June 2024, Vivet Therapeutics presented interim results from its Phase 1/2 GATEWAY trial at the EASL Congress 2024 in Milan, Italy. The trial is evaluating the safety, pharmacodynamics, and effectiveness of VTX-801, Vivet’s leading treatment candidate for Wilson’s disease. These findings highlight the potential of VTX-801 as a novel therapeutic option for patients

- In September 2023, UC Davis Health researchers administered the first-ever gene therapy for a patient with Wilson’s disease as part of the CYPRUS2+ clinical trial. The trial displayed positive results for UX701, an investigational gene therapy treatment, marking a significant milestone in the treatment of this rare genetic disorder

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.