Global Wind Power Market

Market Size in USD Billion

USD

73.91 Billion

USD

111.72 Billion

2024

2032

USD

73.91 Billion

USD

111.72 Billion

2024

2032

| 2025 - 2032 | |

| USD 73.91 Billion | |

| USD 111.72 Billion | |

| % | |

|

Wind Power Market Size

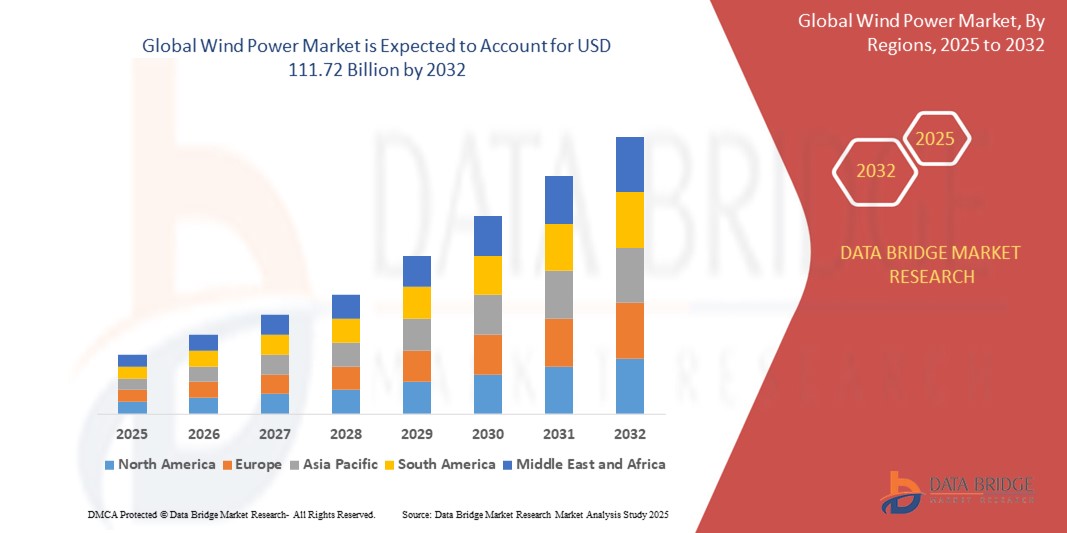

- The global wind power market size was valued at USD 73.91 billion in 2024 and is expected to reach USD 111.72 billion by 2032, at a CAGR of 5.30% during the forecast period

- The market growth is primarily driven by increasing global demand for renewable energy, supportive government policies promoting clean energy, and technological advancements in wind turbine efficiency and capacity

- Rising awareness of climate change and the need for sustainable energy solutions, coupled with declining costs of wind power installations, are accelerating the adoption of wind energy across utility, commercial, industrial, and residential applications

Wind Power Market Analysis

- Wind power, a cornerstone of renewable energy, is increasingly vital for meeting global energy demands due to its scalability, cost-effectiveness, and minimal environmental impact compared to fossil fuels

- The market is propelled by growing investments in renewable energy infrastructure, advancements in turbine technology, and the expansion of offshore wind farms, which offer higher energy yields

- Asia-Pacific dominated the wind power market with the largest revenue share of 42.5% in 2024, driven by extensive wind energy projects in China and India, supportive government incentives, and rapid industrialization

- North America is expected to be the fastest-growing region during the forecast period, fueled by increasing investments in offshore wind projects, particularly in the U.S., and favorable regulatory frameworks promoting renewable energy adoption

- The >12 MW segment dominated the largest market revenue share of 28.5% in 2024, driven by the increasing demand for high-capacity turbines, particularly in offshore wind farms, which maximize energy output and improve project economics

Report Scope and Wind Power Market Segmentation

|

Attributes |

Wind Power Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Wind Power Market Trends

“Increasing Integration of AI and Big Data Analytics”

- The global wind power market is experiencing a significant trend toward integrating Artificial Intelligence (AI) and Big Data analytics to enhance operational efficiency

- These technologies enable advanced data processing and analysis, providing deeper insights into turbine performance, wind patterns, and predictive maintenance needs

- AI-powered wind energy solutions facilitate proactive problem-solving by identifying potential issues before they lead to costly repairs or turbine downtime

- For instances, companies are developing AI-driven platforms that analyze wind patterns to optimize turbine orientation or predict maintenance schedules based on real-time environmental and operational data

- This trend is enhancing the value proposition of wind power systems, making them more efficient and attractive to utility companies, commercial entities, and investors

- AI algorithms can analyze vast datasets, including wind speed, turbine stress, energy output fluctuations, and grid integration patterns, to maximize energy production and reduce operational costs

Wind Power Market Dynamics

Driver

“Rising Demand for Renewable Energy and Grid Stability”

- Increasing global demand for renewable energy sources, driven by climate change concerns and the need to reduce carbon emissions, is a major driver for the wind power market

- Wind power systems enhance grid stability by providing clean, sustainable energy through features such as advanced forecasting, energy storage integration, and grid-compatible electrical systems

- Government mandates and renewable energy targets, particularly in regions such as Europe with ambitious net-zero goals, are contributing to the widespread adoption of wind power

- The proliferation of IoT and advancements in 5G technology are enabling faster data transmission and lower latency, supporting more sophisticated wind farm management and real-time energy optimization

- Wind turbine manufacturers and energy providers are increasingly incorporating advanced control systems as standard features to meet regulatory requirements and enhance system reliability

Restraint/Challenge

“High Initial Costs and Regulatory Complexities”

- The substantial initial investment required for wind turbine manufacturing, installation, and grid integration can be a significant barrier, particularly in emerging markets

- Developing large-scale wind farms, both onshore and offshore, involves complex and costly processes, including site acquisition, permitting, and infrastructure development

- Environmental and community concerns, such as land use conflicts or opposition to turbine installations due to aesthetic or ecological impacts, pose significant challenges

- The fragmented regulatory landscape across countries, with varying standards for environmental impact assessments, grid integration, and community engagement, complicates operations for international developers

- These factors can deter investment and limit market expansion, particularly in regions with stringent regulations or high sensitivity to environmental and community concerns

Wind Power market Scope

The market is segmented on the basis of rating, location, component, and application.

- By Rating

On the basis of rating, the global wind power market is segmented into ≤ 2 MW, >2≤ 5 MW, >5≤ 8 MW, >8≤10 MW, >10≤ 12 MW, and >12 MW. The >12 MW segment dominated the largest market revenue share of 28.5% in 2024, driven by the increasing demand for high-capacity turbines, particularly in offshore wind farms, which maximize energy output and improve project economics. These ultra-large turbines, such as GE's Haliade-X (14 MW) and Siemens Gamesa’s SG 14-222 DD, reduce the number of installations needed, lowering costs and environmental impact.

The >10≤ 12 MW segment is expected to witness the fastest growth rate of 12.5% from 2025 to 2032, fueled by advancements in turbine technology and their suitability for large-scale offshore projects. The trend toward larger turbines enhances energy capture efficiency, making them ideal for regions with strong wind conditions.

- By Location

On the basis of location, the global wind power market is segmented into onshore and offshore. The onshore segment dominated with a revenue share of 75.5% in 2024, owing to its cost-effectiveness, simpler installation processes, and established grid infrastructure. Countries such as China, the U.S., and India heavily invest in onshore wind to meet renewable energy targets, with China’s Jiuquan Wind Power Base being a prime instances.

The offshore segment is anticipated to experience the fastest growth rate of 13.6% from 2025 to 2032, driven by higher and more consistent wind speeds, enabling greater energy yields. Technological advancements, such as floating wind turbines, are expanding offshore projects to deeper waters, supported by government policies in Europe and Asia-Pacific.

- By Component

On the basis of component, the global wind power market is segmented into turbine, support structure, electrical infrastructure, and others. The turbine segment held the largest market revenue share of 40% in 2024, as turbines are the core technology for harnessing wind power. Innovations in turbine design, such as larger rotor diameters and lightweight materials, enhance energy capture and efficiency, driving segment dominance.

The electrical infrastructure segment is expected to witness the fastest growth rate of 14% from 2025 to 2032, propelled by the increasing need for efficient energy transmission and grid integration. Advancements in high-voltage direct current (HVDC) systems and dynamic cables for offshore projects are key growth drivers, particularly for large-scale wind farms.

- By Application

On the basis of application, the global wind power market is segmented into utility, commercial, industrial, and residential. The utility segment dominated with a revenue share of 47% in 2024, driven by large-scale wind farms feeding electricity into power grids. Utility-scale projects benefit from economies of scale, making them cost-effective for meeting renewable energy targets in countries such as China and the U.S.

The industrial segment is anticipated to grow at the fastest rate of 12.7% from 2025 to 2032, fueled by rising demand for renewable energy among industrial players seeking to reduce carbon footprints and operational costs. Industries such as manufacturing and mining are increasingly adopting wind energy to power operations sustainably.

Wind Power Market Regional Analysis

- Asia-Pacific dominated the wind power market with the largest revenue share of 42.5% in 2024, driven by extensive wind energy projects in China and India, supportive government incentives, and rapid industrialization

- Consumers and industries prioritize wind power for its sustainability, cost-effectiveness, and ability to reduce carbon emissions, particularly in regions with high energy demand and favorable wind conditions

- Growth is supported by advancements in turbine technology, such as larger rotor diameters and higher-capacity turbines, alongside increasing adoption in both onshore and offshore segments

Japan Wind Power Market Insight

Japan’s wind power market is expected to witness rapid growth due to strong consumer and industrial preference for high-capacity, technologically advanced turbines that enhance energy efficiency and sustainability. The presence of major wind turbine manufacturers and integration of wind power in utility-scale projects accelerate market penetration. Rising interest in offshore wind projects also contributes to growth.

China Wind Power Market Insight

China holds the largest share of the Asia-Pacific wind power market, propelled by rapid urbanization, rising energy demand, and extensive government support for renewable energy. The country’s focus on reducing reliance on fossil fuels and strong domestic manufacturing capabilities for turbines enhance market accessibility. Competitive pricing and large-scale onshore and offshore wind projects support sustained market growth.

North America Wind Power Market Insight

North America is expected to witness the fastest growth rate in the global wind power market, driven by increasing investments in renewable energy and supportive policies promoting clean energy adoption. The U.S. and Canada lead the region, with strong demand for both onshore and offshore wind projects. Advancements in turbine technology, such as >8≤10 MW and >10≤12 MW turbines, and growing corporate commitments to sustainability further accelerate market expansion. The focus on electrical infrastructure and support structures enhances grid reliability, supporting utility-scale projects.

U.S. Wind Power Market Insight

The U.S. wind power market is expected to witness significant growth, fueled by strong demand for renewable energy and supportive government policies promoting clean energy. The trend towards larger turbine capacities and increasing offshore wind projects further boosts market expansion. The integration of wind power in utility-scale projects and corporate renewable procurement complements market growth, creating a robust ecosystem.

Europe Wind Power Market Insight

The Europe wind power market is expected to witness significant growth, supported by ambitious renewable energy targets and a mature regulatory environment. Consumers and industries seek wind power solutions that enhance energy efficiency while reducing greenhouse gas emissions. The growth is prominent in both onshore and offshore installations, with countries such as Germany and the U.K. showing significant uptake due to strong policy support and technological advancements.

U.K. Wind Power Market Insight

The U.K. market for wind power is expected to witness rapid growth, driven by demand for offshore wind energy and government initiatives to lower electricity costs through regional energy pricing. Increased focus on sustainability and advancements in turbine technology encourage adoption. Evolving regulations balancing environmental goals with energy security influence market dynamics, promoting both utility and commercial applications.

Germany Wind Power Market Insight

Germany is expected to witness rapid growth in the wind power market, attributed to its advanced wind energy infrastructure and high focus on sustainability and energy efficiency. German industries and utilities prefer high-capacity turbines that maximize energy output and contribute to lower carbon emissions. The integration of wind power in both premium and large-scale projects supports sustained market growth.

Wind Power Market Share

The wind power industry is primarily led by well-established companies, including:

- ACCIONA (Spain)

- NORDEX SE (Germany)

- General Electric Company (U.S.)

- Envision Group (China)

- Goldwind (China)

- Siemens Gamesa Renewable Energy, S.A.U. (Spain)

- Suzlon Energy Limited (India)

- Vestas (Denmark)

- Sinovel Wind Group Co., Ltd. (China)

- The Wind Power (China)

- ENERCON Global GmbH (Germany)

- Mingyang Smart Energy Group Co., Ltd. (China)

- JUWI (Germany)

- Inoxwind (India)

- AEROVIDE GmbH (Germany)

What are the Recent Developments in Global Wind Power Market?

- In December 2024, Brazil's Federal Senate passed a landmark offshore wind bill, laying the foundation for rapid growth in the country's offshore wind energy sector. This legislation establishes a regulatory framework that enables the federal government to auction offshore areas for wind farm development, unlocking significant investment opportunities. With over 100 proposed projects representing more than 230 GW of potential capacity, the bill positions Brazil as a key player in the global energy transition. It is expected to drive job creation, enhance energy security, and support Brazil’s climate goals by accelerating the shift to clean, renewable power

- In November 2024, the Global Wind Energy Council (GWEC) and the Global Wind Organisation (GWO) released the Global Wind Workforce Outlook 2024–2028, projecting the need for 532,000 new wind technicians by 2028 to meet the growing global demand for onshore and offshore wind energy. Of these, 40% must be new entrants, highlighting the urgent need for workforce development, vocational training, and safety standards. This surge in demand reflects the rapid expansion of the wind industry and the critical role skilled labor will play in achieving global renewable energy and net-zero targets

- In June 2022, BP announced it would acquire a 40.5% stake and assume operatorship of the Asian Renewable Energy Hub (AREH) in Western Australia. This massive project, spanning 6,500 square kilometers, aims to develop up to 26 GW of combined solar and onshore wind capacity. The AREH is expected to produce 1.6 million tonnes of green hydrogen or 9 million tonnes of green ammonia annually, making it one of the world’s largest renewable and green hydrogen hubs. BP’s investment underscores a major shift by traditional energy companies toward large-scale renewable energy ventures

- In May 2022, Engie Brasil Energia agreed to acquire the Serra do Assuruá wind project in Bahia state from PEC Energia for approximately $50 million (BRL 265 million). This acquisition includes 24 development grants totaling 882 MW of onshore wind capacity, along with land leases, wind measurement data, and a guaranteed grid connection. The project also benefits from a preliminary environmental license and eligibility for transmission tariff reductions. This move strengthens Engie’s renewable energy portfolio in Brazil, where it already operates several major wind complexes, and aligns with its strategy to accelerate the energy transition

- In April 2022, SSE Renewables signed an agreement to acquire Siemens Gamesa Renewable Energy’s (SGRE) Southern Europe renewable energy development platform. The deal includes a 3.9 GW portfolio of onshore wind projects across Spain, France, Italy, and Greece, with potential for an additional 1 GW of co-located solar capacity. This acquisition marks SSE’s strategic entry into Southern Europe and supports its Net Zero Acceleration Programme, aiming to expand its presence in wind, solar, batteries, and hydrogen across the continent

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Wind Power Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Wind Power Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Wind Power Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.