Global Windscreen Automotive Glazing Market

Market Size in USD Billion

USD

9.11 Billion

USD

19.38 Billion

2025

2033

USD

9.11 Billion

USD

19.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.11 Billion | |

| USD 19.38 Billion | |

| % | |

|

Windscreen Automotive Glazing Market Overview

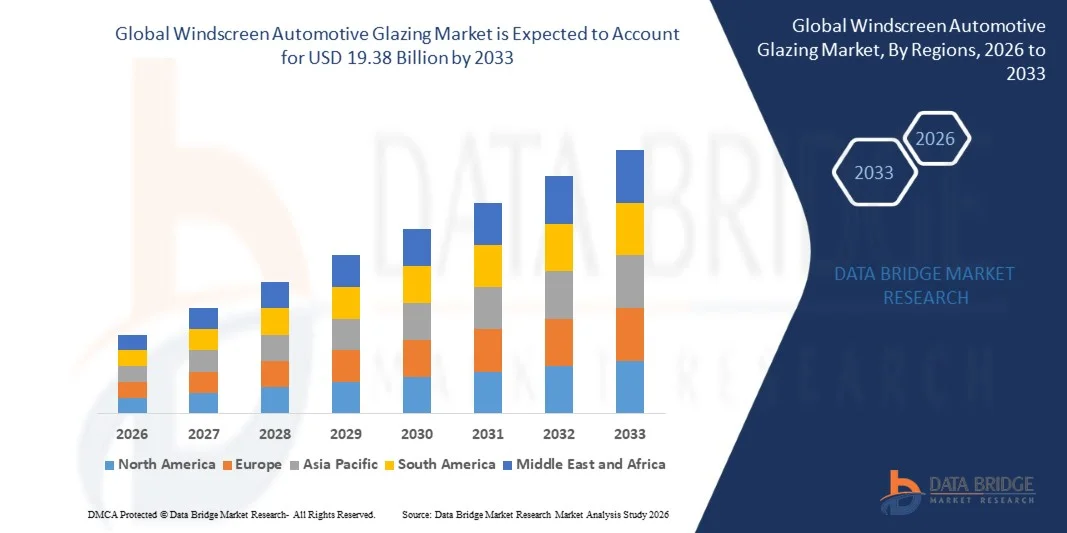

The Windscreen Automotive Glazing Market was valued at USD 9.11 Billion in 2025 and is projected to reach USD 19.38 Billion by 2033, growing at a CAGR of 9.90% from 2026 to 2033. The market is experiencing consistent growth driven by rising automotive production, increasing adoption of electric vehicles, and growing demand for advanced safety and lightweight glazing solutions across passenger and commercial vehicles. Expanding integration of laminated, acoustic, and smart windscreen technologies, along with continuous advancements in polycarbonate and high-strength glass materials, is further supporting market growth across global automotive manufacturing hubs.

The increasing focus on vehicle safety regulations, fuel efficiency improvement, and electric mobility transition is significantly accelerating demand for lightweight and high-performance windscreen glazing systems. Automakers are increasingly adopting advanced glazing solutions compatible with ADAS sensors, heads-up displays, and enhanced thermal insulation, enabling improved driving safety and passenger comfort. In addition, rising investments in EV platforms and premium vehicle segments are further strengthening the adoption of innovative automotive glazing technologies across global markets.

Key Market Trends & Insights

- Asia-Pacific dominated the Windscreen Automotive Glazing Market with the largest revenue share of 48.29% in 2025, supported by strong automotive production capacity, rapid vehicle electrification, and high demand for passenger cars, commercial vehicles, and off-highway equipment across emerging economies

- The front windshield segment led the market with a 67% share in 2025, driven by critical safety requirements, advanced driver assistance system integration, and regulatory mandates for high-performance glazing

- North America is expected to be the fastest-growing region at a CAGR of 5.9% from 2026 to 2033, fueled by increasing demand for lightweight vehicles, and strong presence of leading automotive manufacturers

- Battery Electric Vehicle (BEV) is the fastest-growing electric vehicle type, projected to register a CAGR of 18.2% from 2026 to 2033, supported by rapid electrification policies and expanding charging infrastructure

- The laminated glass segment dominated the product category with a 62% revenue share in 2025, led by superior safety performance, noise reduction capability, and regulatory compliance requirements in modern vehicles

- Construction equipment accounted for 58% of the market in 2025, preferred by rising infrastructure development, mining expansion, and increasing demand for heavy-duty machinery safety glazing

- The polycarbonate segment is the fastest-growing product category, with a CAGR of 12.6% from 2026 to 2033, driven by increasing demand for lightweight and high-strength glazing materials

Market Size & Forecast

- Global Market Value (2025): USD 9.11 Billion

- Expected Market Value (2033): USD 19.38 Billion

- Forecast CAGR (2026–2033): 9.90%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Windscreen Automotive Glazing Market Segmentation

|

Attributes |

Windscreen Automotive Glazing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Covestro AG (Germany) · Freeglass GmbH & Co. KG (Germany) · SABIC (Saudi Arabia) · Webasto Thermo & Comfort SE (Germany) · Trinseo PLC (U.S.) · Teijin Limited (Japan) · Xinyi Glass Holdings Limited (China) · AGC Inc. (Japan) · Guardian Industries Holdings (U.S.) · Nippon Sheet Glass Co., Ltd (Japan) · Fuyao Glass Industry Group Co., Ltd (China) · Saint-Gobain (France) · Sumitomo Corporation (Japan) · Evonik Industries AG (Germany) · Corning Incorporated (U.S.) · Dongguan Benson Automobile Glass Co., Ltd (China) · Şişecam (Turkey) · Vitro, S.A.B. de C.V. (Mexico) · PPG Industries, Inc. (U.S.) · Magna International Inc (Canada) |

|

Market Opportunities |

· EV Lightweight Windscreen Glazing Expansion · ADAS-Integrated Smart Glazing Systems Growth · Aftermarket and Premium Glazing Demand Increase |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Windscreen Automotive Glazing Market Trends

Trend: Lightweight Smart Glazing Adoption in EVs and Safety Systems

The Windscreen Automotive Glazing market is witnessing strong adoption of lightweight and smart glazing technologies driven by electric vehicle expansion and advanced safety integration requirements. Automakers are increasingly focusing on laminated, acoustic, and polycarbonate glazing solutions to reduce vehicle weight, improve energy efficiency, and support ADAS functionality. Integration of heads-up displays, rain sensors, and camera-based driver assistance systems is further accelerating demand for technologically advanced windscreen systems across premium and EV segments.

Companies such as AGC Inc. are advancing smart glazing solutions, including sensor-compatible and display-integrated windscreen technologies used in electric and connected vehicles to enhance safety and driving experience across global automotive platforms.

Windscreen Automotive Glazing Market Dynamics

Key Market Driver: Rising Vehicle Production and Safety Regulations

The growing global automotive production and strict vehicle safety regulations are significantly driving demand for advanced windscreen glazing solutions. Increasing emphasis on passenger safety, crash resistance, and visibility standards is pushing OEMs to adopt laminated and impact-resistant glazing materials across vehicle categories. Regulatory frameworks such as UNECE safety norms and NCAP safety rating programs are further strengthening the integration of high-performance glazing systems in modern vehicles.

Major companies such as Saint-Gobain, Pilkington, and Fuyao Glass are continuously supplying advanced laminated and acoustic windscreen solutions to global automotive manufacturers, supporting large-scale adoption across passenger cars, SUVs, and commercial vehicles.

Key Restraint/Challenge: High Cost and Complex Manufacturing of Advanced Glazing

A major challenge in the Windscreen Automotive Glazing market is the high production cost and complex manufacturing process associated with laminated, smart, and polycarbonate glazing materials. Advanced glazing systems require multi-layer processing, precision coating technologies, and integration of electronic components, which significantly increases production complexity and cost. Supply chain constraints and high capital investment in specialized manufacturing infrastructure further limit large-scale affordability in cost-sensitive markets.

Companies such as Nippon Sheet Glass Co., Ltd and Guardian Industries Holdings face ongoing challenges in balancing innovation with cost efficiency while scaling production of advanced automotive glazing solutions for mass-market applications.

Key Market Opportunity: ADAS-Integrated Smart Glazing Systems Growth

The increasing adoption of ADAS technologies presents a major growth opportunity for smart and sensor-integrated windscreen glazing systems. Demand for windshields compatible with cameras, LiDAR, and heads-up display systems is rising rapidly as vehicles become more autonomous and connected. This is driving innovation in optical-grade glass, infrared reflective coatings, and embedded sensor-compatible glazing structures across automotive platforms.

Companies such as Corning Incorporated and Saint-Gobain are actively developing advanced smart glazing technologies integrated with ADAS features, enabling improved driver assistance, enhanced safety performance, and stronger adoption across next-generation electric and autonomous vehicles.

Windscreen Automotive Glazing Market Scope

The windscreen automotive glazing market is segmented on the basis of off-highway vehicle, electric vehicle, vehicle type, product, and application.

- By Off-Highway Vehicle

On the basis of off-highway vehicle, the Windscreen Automotive Glazing Market is segmented into construction equipment and agricultural tractors. The Construction Equipment segment dominated the market with the largest share of 58% in 2025, driven by rising infrastructure development, mining expansion, and increasing demand for heavy-duty machinery safety glazing. High durability laminated windscreen adoption in excavators, loaders, and bulldozers further strengthens segment leadership. OEM integration of advanced impact-resistant glazing for operator safety enhances replacement cycles and aftermarket demand. Strong deployment across Asia-Pacific and Middle East construction corridors continues to support dominance.

The Agricultural Tractors segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by rapid farm mechanization and adoption of precision agriculture equipment. Increasing demand for enhanced visibility and UV-protected glazing in modern tractors is accelerating product penetration. Government subsidies for agricultural modernization in developing economies are further supporting adoption. Rising replacement of conventional glass with polycarbonate-based windshields improves safety and fuel efficiency in field operations.

- By Electric Vehicle

On the basis of electric vehicle, the market is segmented into battery electric vehicle, hybrid electric vehicle, and plug-in hybrid electric vehicle. The Hybrid Electric Vehicle segment dominated the market with a share of 44% in 2025, supported by strong global production volumes and balanced reliance on combustion and electric systems. Higher thermal management requirements and vibration resistance needs increase demand for advanced laminated glazing solutions. Established manufacturing base across Europe, U.S., and Asia reinforces consistent demand across OEM supply chains. Continued consumer preference for cost-effective electrification strengthens segment leadership.

The Battery Electric Vehicle segment is projected to register the fastest growth at a CAGR of 18.2% from 2026 to 2033, driven by rapid electrification policies and expanding charging infrastructure. Increasing focus on lightweight glazing materials such as advanced laminated glass and polycarbonate supports vehicle range optimization. Rising investments by automakers in premium EV platforms with panoramic windshields further accelerates adoption. Strong regulatory push toward zero-emission mobility across China, Europe, and India fuels long-term expansion.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into passenger car, light commercial vehicle, truck, and bus. The Passenger Car segment dominated the market with a share of 49% in 2025, driven by high production volumes and rising consumer demand for safety and comfort-enhancing glazing systems. Increasing integration of acoustic laminated windshields and heads-up display compatible glass strengthens product penetration. Strong OEM adoption across global automotive manufacturers supports consistent demand. Urban mobility expansion and replacement cycles further reinforce segment dominance.

The Light Commercial Vehicle segment is projected to register the fastest growth at a CAGR of 10.5% from 2026 to 2033, driven by expansion of e-commerce logistics and last-mile delivery services. Rising demand for durable and impact-resistant windshields in fleet operations enhances product adoption. Growth in shared mobility and commercial transportation networks increases replacement frequency. Advancements in lightweight glazing materials improve fuel efficiency and operational performance across fleets.

- By Product

On the basis of product, the market is segmented into laminated glass, tempered glass, and polycarbonate. The Laminated Glass segment dominated the market with a share of 62% in 2025, driven by superior safety performance, noise reduction capability, and regulatory compliance requirements in modern vehicles. Increasing integration in front windshields for impact resistance and passenger protection strengthens adoption. OEM preference for laminated solutions across passenger and commercial vehicles enhances market stability. Strong durability and crack resistance further support long lifecycle usage.

The Polycarbonate segment is projected to register the fastest growth at a CAGR of 12.6% from 2026 to 2033, driven by increasing demand for lightweight and high-strength glazing materials. Growing focus on vehicle weight reduction for improved fuel efficiency and EV range expansion supports adoption. Rising application in off-highway vehicles and premium automotive designs enhances penetration. Advancements in scratch-resistant coatings and UV stability technologies further accelerate market growth.

- By Application

On the basis of application, the market is segmented into front windshield and rear windshield. The Front Windshield segment dominated the market with a share of 67% in 2025, driven by critical safety requirements, advanced driver assistance system integration, and regulatory mandates for high-performance glazing. Increasing adoption of laminated glass for impact protection and sensor compatibility further strengthens demand. OEM focus on enhanced visibility and structural integrity reinforces segment leadership. High replacement demand across global automotive fleets sustains dominance.

The Rear Windshield segment is projected to register the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by rising demand for defogging systems and integrated electronic heating elements. Increasing use of advanced styling and aerodynamic vehicle designs is boosting adoption of high-quality rear glazing solutions. Growth in SUV and hatchback production further supports segment expansion. Continuous improvements in durability and shatter resistance technologies enhance long-term adoption across vehicle categories.

Windscreen Automotive Glazing Market Regional Analysis

Asia-Pacific dominated the windscreen automotive glazing market and accounted for the largest revenue share of 48.29% in 2025, supported by strong automotive production capacity, rapid vehicle electrification, and high demand for passenger cars, commercial vehicles, and off-highway equipment across emerging economies. The region benefits from a well-established automotive manufacturing ecosystem, cost-efficient glass production facilities, and large-scale OEM supply chains. Rising infrastructure development, expanding logistics networks, and increasing adoption of advanced safety glazing solutions such as laminated and acoustic windshields are further accelerating regional market growth. Strong penetration of EV manufacturing hubs and continuous investments in lightweight automotive materials continue to reinforce Asia-Pacific’s dominance in the global market.

China Windscreen Automotive Glazing Market Insight

China held the largest share in the Asia-Pacific Windscreen Automotive Glazing market in 2025, driven by its massive automotive production base, strong EV leadership, and extensive demand for passenger and commercial vehicles. The country benefits from a highly integrated supply chain for automotive glass manufacturing, supporting large-scale OEM and aftermarket demand. Rapid expansion of battery electric vehicles and hybrid vehicles is significantly increasing the adoption of advanced laminated and polycarbonate glazing solutions. In addition, strong government support for new energy vehicles and continuous infrastructure expansion are reinforcing China’s leadership position in the global automotive glazing ecosystem.

India Windscreen Automotive Glazing Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by rising vehicle ownership, expanding road infrastructure, and increasing demand for commercial fleets and passenger cars. Growing adoption of safety-focused automotive standards is boosting penetration of laminated windshields across mid-range and premium vehicles. Rapid expansion of the logistics, e-commerce, and agricultural mechanization sectors is further supporting demand for durable glazing solutions in LCVs and off-highway vehicles. In addition, increasing domestic automotive manufacturing investments and rising EV adoption are accelerating long-term market expansion across the country.

Europe Windscreen Automotive Glazing Market Insight

The Europe Windscreen Automotive Glazing market is expanding steadily, supported by stringent vehicle safety regulations, high EV penetration, and strong demand for premium automotive designs. The region benefits from advanced automotive engineering capabilities and strong focus on lightweight and energy-efficient materials in vehicle production. Increasing adoption of acoustic laminated windshields and ADAS-compatible glazing systems is further driving market growth. In addition, rising preference for sustainable mobility solutions and continuous innovation in electric and hybrid vehicles are strengthening regional demand for advanced windscreen glazing technologies.

Germany Windscreen Automotive Glazing Market Insight

Germany accounted for the largest share in the Europe Windscreen Automotive Glazing market in 2025, driven by its strong automotive manufacturing base and leadership in premium vehicle production. The country has a well-established OEM ecosystem that extensively integrates laminated and high-performance glazing systems in passenger cars and luxury vehicles. Rising demand for EVs and hybrid vehicles is further accelerating adoption of lightweight and thermally efficient windscreen solutions. In addition, strong R&D investments in automotive safety technologies and advanced glass materials are reinforcing Germany’s dominant market position.

U.K. Windscreen Automotive Glazing Market Insight

The U.K. market is supported by increasing adoption of electric vehicles, rising demand for advanced safety features, and growing automotive aftermarket replacement activities. Expanding usage of laminated and acoustic windshields in passenger vehicles is strengthening product penetration across OEM and repair channels. The country is also witnessing growing integration of smart glazing systems compatible with connected vehicle technologies. In addition, strong regulatory focus on vehicle safety standards and increasing consumer preference for premium automotive features are contributing to steady market growth.

North America Windscreen Automotive Glazing Market Insight

North America is projected to grow at the fastest CAGR of 5.9% from 2026 to 2033, driven by rapid EV adoption, increasing demand for lightweight vehicles, and strong presence of leading automotive manufacturers. Rising consumer preference for advanced safety features, including ADAS-integrated windshields and acoustic insulation glazing, is significantly boosting market expansion. Strong investments in electric mobility infrastructure and fleet modernization are further accelerating adoption of high-performance automotive glazing. In addition, growing replacement demand in the aftermarket segment and technological advancements in smart glass solutions are reinforcing regional growth momentum.

U.S. Windscreen Automotive Glazing Market Insight

The U.S. accounted for the largest share in the North America Windscreen Automotive Glazing market in 2025, supported by strong automotive production, high vehicle ownership rates, and extensive demand for premium SUVs, trucks, and electric vehicles. The country benefits from advanced automotive technology integration, including heads-up display-compatible and sensor-enabled windshields. Increasing focus on vehicle safety regulations and rising adoption of EV platforms are further strengthening demand for laminated and lightweight glazing solutions. In addition, strong aftermarket replacement cycles and widespread availability of advanced automotive glass products are reinforcing the U.S. leadership position in the regional market.

Windscreen Automotive Glazing Market Share

The windscreen automotive glazing industry is primarily led by well-established companies, including:

- Covestro AG (Germany)

- Freeglass GmbH & Co. KG (Germany)

- SABIC (Saudi Arabia)

- Webasto Thermo & Comfort SE (Germany)

- Trinseo PLC (U.S.)

- Teijin Limited (Japan)

- Xinyi Glass Holdings Limited (China)

- AGC Inc. (Japan)

- Guardian Industries Holdings (U.S.)

- Nippon Sheet Glass Co., Ltd (Japan)

- Fuyao Glass Industry Group Co., Ltd (China)

- Saint-Gobain (France)

- Sumitomo Corporation (Japan)

- Evonik Industries AG (Germany)

- Corning Incorporated (U.S.)

- Dongguan Benson Automobile Glass Co., Ltd (China)

- Şişecam (Turkey)

- Vitro, S.A.B. de C.V. (Mexico)

- PPG Industries, Inc. (U.S.)

- Magna International Inc (Canada)

Latest Developments in Windscreen Automotive Glazing Market

- In September 2025 Pilkington launched a new digital customer integration platform aimed at streamlining ordering, tracking, and aftersales services for automotive glazing products. This development strengthens Pilkington’s position in the global windscreens market by improving supply chain responsiveness and enhancing OEM and aftermarket customer experience. The shift toward digitalized procurement systems is expected to reduce lead times and improve operational efficiency across automotive glass distribution networks, supporting stronger client retention and competitive positioning

- In July 2025 AGC Inc. expanded its collaboration with a leading electric vehicle manufacturer to supply next-generation smart windscreen glazing integrated with sensors and display compatibility features. This partnership reinforces AGC’s presence in the rapidly growing EV segment and supports the broader industry trend of connected and intelligent vehicle components. The integration of advanced functionalities into glazing systems is expected to enhance driving safety, improve vehicle interface technologies, and strengthen AGC’s long-term OEM partnerships across global EV platforms

- In May 2025 Fuyao Glass Industry Group announced the expansion of its production capacity for lightweight laminated automotive windscreen glass to meet rising global OEM demand. This strategic expansion is significant as it enhances the company’s ability to supply high-volume vehicle manufacturers while supporting the industry’s shift toward lightweight and fuel-efficient automotive materials. The increased capacity is expected to strengthen Fuyao’s export competitiveness and reinforce its leadership position in both passenger and commercial vehicle glazing segments

- In March 2025 NSG Group introduced an upgraded line of acoustic laminated windscreen glazing designed to reduce cabin noise and improve driving comfort in premium and electric vehicles. This innovation aligns with the growing demand for enhanced in-vehicle experience and supports increasing adoption of EVs and luxury automotive models worldwide. The product launch is expected to strengthen NSG Group’s positioning in the premium glazing segment while expanding its footprint in high-value OEM contracts across Europe and Asia-Pacific

- In January 2025 Saint-Gobain introduced an upgraded lightweight laminated windscreen glazing solution engineered to improve crash resistance while reducing overall vehicle weight. This development strengthens the company’s positioning in the global automotive glazing market by directly addressing OEM demand for improved fuel efficiency and enhanced passenger safety. The innovation supports the broader industry transition toward lightweight vehicle architectures and is expected to increase adoption across both internal combustion and electric vehicle platforms, reinforcing Saint-Gobain’s competitive edge in high-performance glazing solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.