Global Wireless Occupancy Sensor Market

Market Size in USD Billion

USD

1.60 Billion

USD

4.20 Billion

2025

2033

USD

1.60 Billion

USD

4.20 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 1.60 Billion |

Market Size (Forecast Year) |

USD 4.20 Billion |

CAGR |

% |

Major Markets Players |

|

Wireless Occupancy Sensor Market Overview

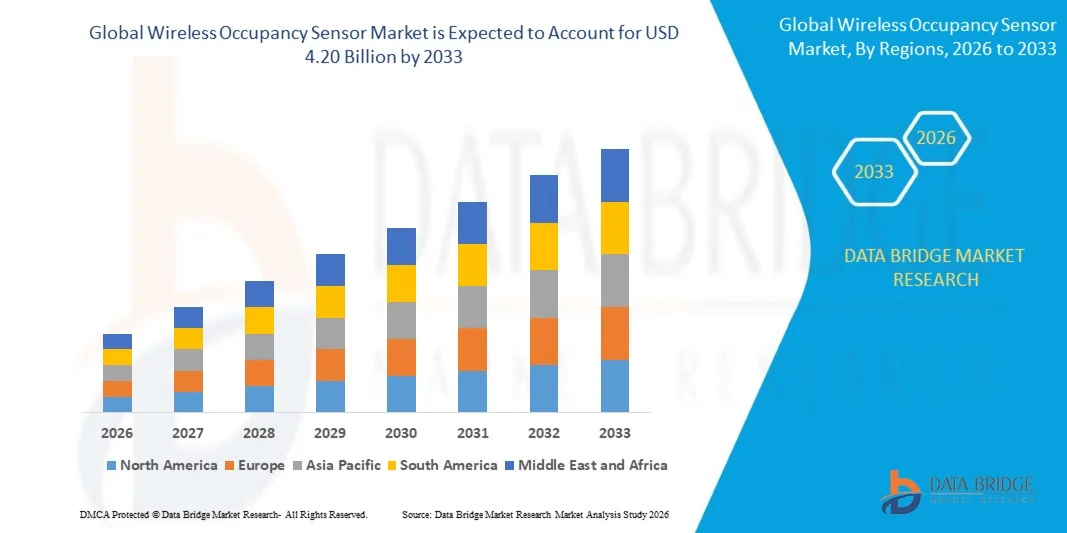

The Wireless Occupancy Sensor Market was valued at USD 1.60 billion in 2025 and is projected to reach USD 4.20 billion by 2033, growing at a CAGR of 12.85% from 2026 to 2033. The market is experiencing strong growth driven by increasing demand for energy-efficient building management solutions, rapid adoption of smart building technologies, and growing integration of wireless sensing systems across commercial, residential, and industrial facilities. Rising investments in building automation infrastructure and the expansion of Internet of Things (IoT)-enabled environments are further accelerating market development worldwide.

The growing emphasis on reducing energy consumption and complying with stringent energy-efficiency regulations is encouraging facility managers, commercial building operators, and homeowners to deploy advanced wireless occupancy sensors. These systems automatically monitor room occupancy and control lighting, heating, ventilation, air conditioning (HVAC), and other connected devices, helping organizations reduce operational costs and improve energy efficiency. Wireless occupancy sensors are increasingly replacing wired alternatives in many applications due to their simplified installation, scalability, lower maintenance requirements, and seamless integration with smart building platforms. In addition, rising adoption of connected workplaces, smart homes, and intelligent infrastructure projects is supporting market expansion across both developed and emerging economies.

Key Market Trends & Insights

- North America dominated the wireless occupancy sensor market with the largest revenue share of 36.9% in 2025, supported by widespread deployment of smart building solutions, stringent energy-efficiency regulations, advanced building automation infrastructure, and strong adoption of connected facility management technologies.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 14.2% from 2026 to 2033. Growth is driven by rapid urbanization, increasing smart city developments, expanding commercial construction activities, rising government investments in energy-efficient infrastructure, and growing adoption of connected building technologies across emerging economies.

- The Passive Infrared segment held the largest market revenue share of approximately 42.7% in 2025 driven by its low cost, high reliability, and widespread deployment across residential and commercial buildings. Passive infrared sensors detect body heat movement efficiently while consuming minimal power, making them highly suitable for lighting automation and energy management applications. Their ease of installation and compatibility with smart building systems continue to support broad adoption globally.

- The Dual Technology segment is projected to register the fastest growth at a CAGR of 14.1% from 2026 to 2033, driven by increasing demand for higher detection accuracy in offices, hospitals, educational facilities, and industrial environments. By combining passive infrared and ultrasonic technologies, these sensors significantly reduce false triggering and improve occupancy detection performance, making them increasingly preferred for advanced building automation systems.

- The Commercial Buildings segment accounted for the largest market revenue share of approximately 61.8% in 2025 driven by growing investments in smart offices, retail centers, healthcare facilities, educational institutions, and corporate campuses. Building owners are increasingly deploying occupancy-based controls to comply with energy-efficiency regulations while reducing operating expenses. The expansion of intelligent building infrastructure continues to accelerate segment growth.

- The Residential Buildings segment is expected to witness the fastest growth at a CAGR of 13.6% from 2026 to 2033 owing to increasing adoption of smart home technologies, connected lighting systems, and residential energy management solutions. Rising consumer awareness regarding electricity conservation and convenience-based automation is supporting wider sensor deployment across modern households.

- The Wireless segment dominated the market with a revenue share of approximately 67.4% in 2025 driven by simplified installation, lower infrastructure requirements, and seamless integration with IoT-enabled building management platforms. Technologies such as Zigbee, Bluetooth Low Energy, Wi-Fi, and LoRaWAN are increasingly supporting large-scale deployments across commercial and residential environments.

- The Wired segment continues to maintain stable demand in critical infrastructure and industrial facilities where highly reliable communication networks are required. However, wireless solutions are expected to continue gaining market share due to greater scalability, flexibility, and lower installation costs.

- The Indoor Operation segment accounted for the largest market revenue share of approximately 78.9% in 2025 driven by widespread implementation across offices, schools, hospitals, hotels, retail facilities, and residential buildings. Indoor occupancy monitoring plays a critical role in lighting automation, HVAC optimization, and workplace utilization management.

- The Outdoor Operation segment is projected to register the fastest growth at a CAGR of 13.9% from 2026 to 2033 due to increasing deployment in smart street lighting systems, public infrastructure, transportation hubs, parking facilities, and smart city projects. Growing urban development initiatives are supporting adoption of outdoor occupancy sensing technologies worldwide.

- The 180–360° segment held the largest market revenue share of approximately 48.6% in 2025 owing to its ability to monitor larger areas with fewer sensor installations. These sensors are extensively utilized in open office environments, conference halls, warehouses, and large commercial facilities where wide-angle coverage improves operational efficiency and reduces deployment costs.

- The 90–179° segment is expected to witness notable growth during the forecast period driven by increasing demand for targeted monitoring applications in classrooms, hospital rooms, retail spaces, and residential settings. Its balanced coverage capability makes it suitable for a wide range of occupancy detection requirements.

- The Lighting Systems segment accounted for the largest market revenue share of approximately 44.5% in 2025 driven by growing implementation of automated lighting controls to reduce electricity consumption and improve building energy performance. Occupancy-based lighting automation remains one of the most widely adopted energy-saving technologies across commercial and residential sectors.

- The HVAC Systems segment is projected to register the fastest growth at a CAGR of 14.4% from 2026 to 2033 due to increasing focus on intelligent climate control and energy-efficient building operations. Occupancy-driven HVAC management allows facilities to optimize heating and cooling usage while improving occupant comfort and reducing utility expenses.

- The Educational segment held the largest market revenue share of approximately 24.8% in 2025 driven by increasing deployment of smart classroom technologies and government-led energy efficiency initiatives across schools, universities, and academic institutions. Educational facilities are utilizing occupancy sensors to optimize lighting, HVAC systems, and space utilization while lowering operating costs.

- The Health Care segment is projected to register the fastest growth at a CAGR of 14.7% from 2026 to 2033 owing to rising adoption of intelligent patient room management systems, occupancy-based environmental controls, and smart hospital infrastructure. Healthcare facilities are increasingly leveraging occupancy sensing technologies to improve patient comfort, operational efficiency, and resource utilization while complying with modern healthcare facility standards.

Market Size & Forecast

- Global Market Value (2025): USD 1.60 Billion

- Expected Market Value (2033): USD 4.20 Billion

- Forecast CAGR (2026–2033): 12.85%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Wireless Occupancy Sensor Market Segmentation

|

Attributes |

Wireless Occupancy Sensor Key Market Insights |

|

Segments Covered |

· By Technology: Passive Infrared, Ultrasonic, Dual Technology, and Others · By Building Type: Residential Buildings and Commercial Buildings · By NetworkConnectivity: Wired and Wireless · By Operation: Indoor Operation and Outdoor Operation · By Coverage Area: Less than 89°, 90–179°, and 180–360° · By Application: Lighting Systems, HVAC Systems, Security and Surveillance Systems, and Others · By End User: Industrial, Aerospace and Defense, Health Care, Hotels, Educational, and Consumer Electronics |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Legrand North America, LLC. (U.S.) |

|

Market Opportunities |

• Rising Deployment Of Smart Building And Intelligent Infrastructure Projects • Increasing Integration Of Wireless Occupancy Sensors With IoT And Building Automation Platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Wireless Occupancy Sensor Market Trends

Trend: Increasing Adoption Of IoT-Enabled Smart Building Automation And Energy Management Systems

Growing demand for intelligent energy management, workplace optimization, and automated building operations is accelerating the adoption of wireless occupancy sensors across commercial, residential, and industrial facilities. Traditional lighting and HVAC systems often operate continuously regardless of actual occupancy, resulting in unnecessary energy consumption and higher operational costs. This is encouraging facility operators to deploy wireless sensing technologies capable of detecting occupancy patterns and automatically controlling connected systems.

In modern commercial buildings, wireless occupancy sensors are increasingly integrated with smart lighting and HVAC platforms to improve energy efficiency and occupant comfort. For instance, office buildings implementing occupancy-based lighting controls can reduce lighting energy consumption by 30–60%, according to building efficiency studies. Educational institutions, healthcare facilities, and retail establishments are also deploying wireless sensor networks to optimize space utilization while lowering electricity usage. The growing adoption of Bluetooth Low Energy (BLE), Zigbee, and LoRaWAN communication technologies is further enhancing deployment flexibility and system scalability.

The rapid expansion of smart city initiatives and green building projects is also driving market demand. In addition, organizations are increasingly utilizing occupancy analytics to improve workplace planning and resource allocation. Industry reports indicate that smart building deployments globally surpassed 45 million connected devices in commercial facilities during 2025, highlighting the growing role of wireless occupancy sensing technologies in intelligent infrastructure development.

Wireless Occupancy Sensor Market Dynamics

Key Market Driver: Rising Focus On Energy Efficiency And Building Automation

Governments, businesses, and building owners worldwide are increasingly prioritizing energy conservation and operational efficiency to reduce utility costs and achieve sustainability goals. Buildings account for a significant portion of global energy consumption, creating strong demand for technologies capable of automatically optimizing lighting, HVAC, and facility operations based on real-time occupancy conditions.

Commercial offices, educational institutions, hospitals, and industrial facilities are increasingly deploying wireless occupancy sensors to minimize energy wastage and improve building performance. For instance, occupancy-based lighting control systems installed in commercial buildings can lower lighting-related electricity consumption by up to 40–60% depending on usage patterns. Smart HVAC systems integrated with occupancy sensing technologies are also helping organizations reduce heating and cooling expenses while improving occupant comfort.

Similarly, governments across North America, Europe, and Asia-Pacific are strengthening energy-efficiency regulations and green building standards to encourage adoption of intelligent building technologies. Real-world deployments across large office campuses and public infrastructure projects during 2024 demonstrated energy savings ranging from 20–35% following integration of wireless occupancy monitoring systems into building management platforms.

Key Restraint/Challenge: Connectivity Limitations And Integration Complexities

Despite significant advantages, wireless occupancy sensor deployments can face challenges related to connectivity reliability, interoperability, and integration with existing building management systems. Large facilities often operate multiple communication protocols and legacy infrastructure, creating compatibility concerns during implementation.

In addition, wireless devices may experience signal interference from walls, machinery, electronic equipment, or network congestion, potentially affecting detection accuracy and system performance. Organizations also face challenges associated with initial configuration, calibration requirements, cybersecurity considerations, and ongoing network management. These factors can increase deployment complexity and discourage adoption among smaller facilities with limited technical resources.

Industry implementation assessments indicate that building automation projects involving multiple wireless communication standards often require additional integration services and system customization, increasing deployment costs and extending installation timelines. Concerns regarding data privacy and network security continue to remain important considerations for enterprise customers deploying connected occupancy sensing solutions.

Key Market Opportunity: Expansion Of Smart Buildings And Intelligent Workplace Infrastructure

The growing development of smart buildings, connected workplaces, and intelligent urban infrastructure presents substantial growth opportunities for wireless occupancy sensor manufacturers. Organizations increasingly require real-time occupancy intelligence to improve energy management, optimize space utilization, and enhance workplace productivity.

Building operators are increasingly integrating wireless occupancy sensors with IoT platforms, cloud-based analytics, and artificial intelligence systems to enable predictive facility management. For instance, occupancy data is being utilized to automate conference room scheduling, optimize cleaning operations, and improve employee workspace experiences in modern office environments. In healthcare facilities, occupancy monitoring systems help improve room utilization and resource allocation while supporting patient comfort initiatives.

In addition, advancements in battery technology, energy harvesting systems, and low-power wireless communication protocols are improving sensor performance and deployment flexibility. Smart office projects implemented during 2025 across North America and Europe reported workspace utilization improvements of approximately 15–25% after deploying occupancy-based analytics platforms integrated with wireless sensor networks. These developments are creating significant opportunities across commercial real estate, healthcare, education, retail, and smart city infrastructure markets.

Wireless Occupancy Sensor Market Scope

The market is segmented on the basis of technology, building type, network connectivity, operation, coverage area, application, and end user.

- By Technology

On the basis of technology, the wireless occupancy sensor market is segmented into Passive Infrared, Ultrasonic, Dual Technology, and Others. The Passive Infrared segment held the largest market revenue share of approximately 42.7% in 2025 driven by its low cost, high reliability, and widespread deployment across residential and commercial buildings. Passive infrared sensors detect body heat movement efficiently while consuming minimal power, making them highly suitable for lighting automation and energy management applications. Their ease of installation and compatibility with smart building systems continue to support broad adoption globally.

The Dual Technology segment is projected to register the fastest growth at a CAGR of 14.1% from 2026 to 2033, driven by increasing demand for higher detection accuracy in offices, hospitals, educational facilities, and industrial environments. By combining passive infrared and ultrasonic technologies, these sensors significantly reduce false triggering and improve occupancy detection performance, making them increasingly preferred for advanced building automation systems.

- By Building Type

On the basis of building type, the wireless occupancy sensor market is segmented into Residential Buildings and Commercial Buildings. The Commercial Buildings segment accounted for the largest market revenue share of approximately 61.8% in 2025 driven by growing investments in smart offices, retail centers, healthcare facilities, educational institutions, and corporate campuses. Building owners are increasingly deploying occupancy-based controls to comply with energy-efficiency regulations while reducing operating expenses. The expansion of intelligent building infrastructure continues to accelerate segment growth.

The Residential Buildings segment is expected to witness the fastest growth at a CAGR of 13.6% from 2026 to 2033 owing to increasing adoption of smart home technologies, connected lighting systems, and residential energy management solutions. Rising consumer awareness regarding electricity conservation and convenience-based automation is supporting wider sensor deployment across modern households.

- By Network Connectivity

On the basis of network connectivity, the wireless occupancy sensor market is segmented into Wired and Wireless. The Wireless segment dominated the market with a revenue share of approximately 67.4% in 2025 driven by simplified installation, lower infrastructure requirements, and seamless integration with IoT-enabled building management platforms. Technologies such as Zigbee, Bluetooth Low Energy, Wi-Fi, and LoRaWAN are increasingly supporting large-scale deployments across commercial and residential environments.

The Wired segment continues to maintain stable demand in critical infrastructure and industrial facilities where highly reliable communication networks are required. However, wireless solutions are expected to continue gaining market share due to greater scalability, flexibility, and lower installation costs.

- By Operation

On the basis of operation, the wireless occupancy sensor market is segmented into Indoor Operation and Outdoor Operation. The Indoor Operation segment accounted for the largest market revenue share of approximately 78.9% in 2025 driven by widespread implementation across offices, schools, hospitals, hotels, retail facilities, and residential buildings. Indoor occupancy monitoring plays a critical role in lighting automation, HVAC optimization, and workplace utilization management.

The Outdoor Operation segment is projected to register the fastest growth at a CAGR of 13.9% from 2026 to 2033 due to increasing deployment in smart street lighting systems, public infrastructure, transportation hubs, parking facilities, and smart city projects. Growing urban development initiatives are supporting adoption of outdoor occupancy sensing technologies worldwide.

- By Coverage Area

On the basis of coverage area, the wireless occupancy sensor market is segmented into Less than 89°, 90–179°, and 180–360°. The 180–360° segment held the largest market revenue share of approximately 48.6% in 2025 owing to its ability to monitor larger areas with fewer sensor installations. These sensors are extensively utilized in open office environments, conference halls, warehouses, and large commercial facilities where wide-angle coverage improves operational efficiency and reduces deployment costs.

The 90–179° segment is expected to witness notable growth during the forecast period driven by increasing demand for targeted monitoring applications in classrooms, hospital rooms, retail spaces, and residential settings. Its balanced coverage capability makes it suitable for a wide range of occupancy detection requirements.

- By Application

On the basis of application, the wireless occupancy sensor market is segmented into Lighting Systems, HVAC Systems, Security and Surveillance Systems, and Others. The Lighting Systems segment accounted for the largest market revenue share of approximately 44.5% in 2025 driven by growing implementation of automated lighting controls to reduce electricity consumption and improve building energy performance. Occupancy-based lighting automation remains one of the most widely adopted energy-saving technologies across commercial and residential sectors.

The HVAC Systems segment is projected to register the fastest growth at a CAGR of 14.4% from 2026 to 2033 due to increasing focus on intelligent climate control and energy-efficient building operations. Occupancy-driven HVAC management allows facilities to optimize heating and cooling usage while improving occupant comfort and reducing utility expenses.

- By End User

On the basis of end user, the wireless occupancy sensor market is segmented into Industrial, Aerospace and Defense, Health Care, Hotels, Educational, and Consumer Electronics. The Educational segment held the largest market revenue share of approximately 24.8% in 2025 driven by increasing deployment of smart classroom technologies and government-led energy efficiency initiatives across schools, universities, and academic institutions. Educational facilities are utilizing occupancy sensors to optimize lighting, HVAC systems, and space utilization while lowering operating costs.

The Health Care segment is projected to register the fastest growth at a CAGR of 14.7% from 2026 to 2033 owing to rising adoption of intelligent patient room management systems, occupancy-based environmental controls, and smart hospital infrastructure. Healthcare facilities are increasingly leveraging occupancy sensing technologies to improve patient comfort, operational efficiency, and resource utilization while complying with modern healthcare facility standards.

Wireless Occupancy Sensor Market Regional Analysis

North America Wireless Occupancy Sensor Market Insight

North America dominated the wireless occupancy sensor market with the largest revenue share in 2025, supported by widespread adoption of smart building technologies, stringent energy-efficiency regulations, and increasing investments in intelligent infrastructure. Building owners and facility managers across the region highly value wireless occupancy sensors for their ability to reduce energy consumption, automate lighting and HVAC operations, and improve workplace efficiency. The presence of advanced building automation ecosystems, high technology penetration, and growing demand for sustainable building solutions continues to strengthen market growth across commercial, residential, healthcare, and educational sectors.

U.S. Wireless Occupancy Sensor Market Insight

The U.S. wireless occupancy sensor market captured the largest revenue share in 2025 within North America, fueled by rapid adoption of IoT-enabled building management systems and growing emphasis on energy conservation. Organizations are increasingly implementing occupancy-based lighting and HVAC controls to reduce operating costs and comply with evolving energy standards. The growing deployment of smart offices, connected campuses, and intelligent commercial buildings is further propelling market expansion. Moreover, increasing investments in workplace optimization and data-driven facility management solutions continue to support industry growth across the country.

Europe Wireless Occupancy Sensor Market Insight

The Europe wireless occupancy sensor market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent sustainability regulations and increasing adoption of energy-efficient building technologies. The region's focus on reducing carbon emissions and improving building performance is accelerating deployment of occupancy-based automation systems. European building owners are increasingly integrating wireless sensors into lighting, HVAC, and security platforms to achieve operational efficiency and regulatory compliance. Growing investments in green building projects and smart city initiatives are further contributing to regional market growth.

U.K. Wireless Occupancy Sensor Market Insight

The U.K. wireless occupancy sensor market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of smart building solutions and rising emphasis on energy management. Organizations across commercial offices, educational institutions, and healthcare facilities are increasingly deploying occupancy sensing technologies to optimize space utilization and reduce electricity consumption. The country's strong commitment to sustainability targets and modernization of building infrastructure continues to support widespread sensor adoption. Growing implementation of connected workplace environments is also contributing to market expansion.

Germany Wireless Occupancy Sensor Market Insight

The Germany wireless occupancy sensor market is expected to witness the fastest growth rate from 2026 to 2033, fueled by strong demand for advanced automation technologies and energy-efficient building systems. Germany's emphasis on industrial innovation, smart manufacturing, and sustainable infrastructure development is driving deployment of intelligent occupancy monitoring solutions. Building operators are increasingly integrating wireless sensors with automated lighting and climate control systems to improve operational efficiency. The growing popularity of smart commercial buildings and environmentally responsible construction practices is further accelerating market growth.

Asia-Pacific Wireless Occupancy Sensor Market Insight

The Asia-Pacific wireless occupancy sensor market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, increasing smart city investments, and expanding adoption of connected building technologies. Governments across the region are actively promoting energy-efficient infrastructure and digital transformation initiatives, creating favorable conditions for sensor deployment. The growing construction of commercial buildings, residential complexes, educational facilities, and healthcare institutions is further driving market demand. In addition, increasing affordability of wireless technologies is enabling broader adoption across emerging economies.

Japan Wireless Occupancy Sensor Market Insight

The Japan wireless occupancy sensor market is expected to witness the fastest growth rate from 2026 to 2033 due to the country's advanced technology infrastructure, strong focus on automation, and increasing demand for intelligent energy management systems. Japanese organizations are increasingly utilizing occupancy sensors to improve operational efficiency and optimize building performance. The integration of occupancy sensing technologies with smart lighting, HVAC, and security systems is becoming increasingly common across commercial and residential applications. Moreover, Japan's commitment to energy conservation and sustainable urban development continues to support market growth.

China Wireless Occupancy Sensor Market Insight

The China wireless occupancy sensor market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's large-scale smart city initiatives, rapid urban development, and strong adoption of building automation technologies. China represents one of the largest markets for connected infrastructure and intelligent building systems, creating substantial demand for occupancy sensing solutions across commercial, industrial, and residential sectors. Government support for energy-efficient construction projects and digital transformation programs is accelerating sensor deployment nationwide. The presence of a large electronics manufacturing ecosystem and growing investments in smart buildings further contribute to market expansion in China.

Wireless Occupancy Sensor Market Share

The Wireless Occupancy Sensor industry is primarily led by well-established companies, including:

• Legrand North America, LLC. (U.S.)

• Schneider Electric SE (France)

• Eaton (Ireland)

• Johnson Controls (Ireland)

• Acuity Brands Lighting, Inc. (U.S.)

• Signify Holding (Netherlands)

• Lutron Electronics Co., Inc. (U.S.)

• Leviton Manufacturing Co., Inc. (U.S.)

• Honeywell International Inc. (U.S.)

• Hubbell Incorporated (U.S.)

• Texas Instruments Incorporated (U.S.)

• OSRAM GmbH (Germany)

• Siemens AG (Germany)

• Hager Group (Germany)

Latest Developments in Wireless Occupancy Sensor Market

- In February 2025, ABB and Samsung Electronics, Partnership/Technology Integration, announced the integration of ABB’s InSite energy management system with Samsung SmartThings platforms to create a unified building automation ecosystem. The collaboration enhances occupancy-based energy optimization, smart appliance coordination, and real-time monitoring capabilities across residential and commercial buildings. This development is expected to accelerate adoption of connected building technologies and strengthen demand for intelligent occupancy sensing solutions.

- In February 2025, Eaton Corporation, Capacity Expansion Investment, announced a USD 340 million investment to establish a new transformer manufacturing facility in Jonesville, South Carolina. The project is expected to create approximately 700 jobs while strengthening grid infrastructure needed to support increasing power requirements from smart buildings and connected facilities. The expansion reinforces energy infrastructure modernization and supports broader deployment of building automation technologies.

- In January 2025, Acuity Brands, Acquisition, completed its USD 1.215 billion acquisition of QSC, LLC to expand its intelligent building portfolio with cloud-managed audio, video, and control technologies. The integration strengthens Acuity’s Intelligent Spaces segment and improves interoperability between occupancy sensing, automation, and building management platforms. The acquisition is expected to enhance smart building capabilities and drive innovation across connected workplace environments.

- In October 2024, Schneider Electric, Strategic Investment, completed its investment in Planon Beheer B.V. to accelerate the digital transformation of commercial buildings and workplace environments. The collaboration focuses on occupancy-driven space utilization, facility optimization, and sustainability management solutions. The initiative is expected to improve operational efficiency while supporting growing demand for data-driven smart building technologies.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Wireless Occupancy Sensor Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Wireless Occupancy Sensor Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Wireless Occupancy Sensor Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.