Global Womens Health Devices Market

Market Size in USD Billion

USD

34.28 Billion

USD

62.05 Billion

2025

2033

USD

34.28 Billion

USD

62.05 Billion

2025

2033

| 2026 - 2033 | |

| USD 34.28 Billion | |

| USD 62.05 Billion | |

| % | |

|

Women’s Health Devices Market Overview

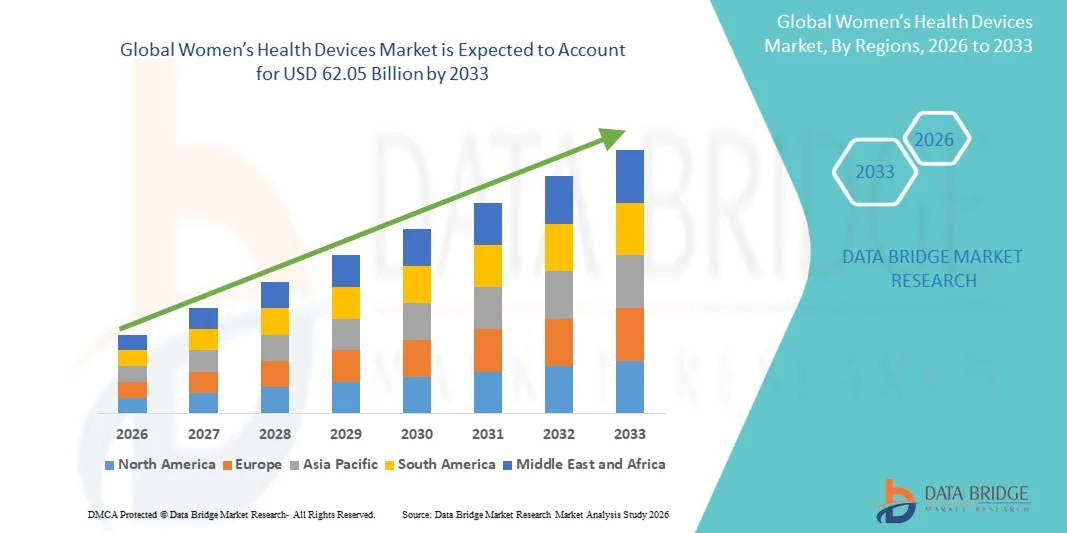

As per Data Bridge Market Research analysis The women’s health devices market was valued at USD 34.28 billion in 2025 and is projected to reach USD 62.05 billion by 2033, growing at a CAGR of 7.70% from 2026 to 2033. The market is witnessing steady growth driven by rising prevalence of gynecological disorders, increasing awareness of preventive women’s healthcare, and rapid advancements in diagnostic, surgical, and monitoring devices used across reproductive and maternal health applications.

The growing burden of conditions such as breast cancer, cervical cancer, uterine fibroids, and infertility, combined with expanding access to healthcare services in emerging economies, is accelerating the adoption of advanced women’s health devices. In addition, increasing government initiatives for maternal health, rising screening programs, and the growing shift toward minimally invasive procedures and home-based diagnostic solutions are supporting market expansion across hospitals, diagnostic centers, and ambulatory surgical settings.

Market Size & Forecast

- Global Market Value (2025): USD 34.28 Billion

- Expected Market Value (2033): USD 62.05 Billion

- Forecast CAGR (2026–2033): 7.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the global women’s health devices market with the largest revenue share of 36.92% in 2025, supported by advanced healthcare infrastructure, high screening rates for breast and cervical cancer, and strong adoption of minimally invasive gynecological procedures.

- The Diagnostic Devices segment led the market with a 39.48% share in 2025, driven by increasing demand for early disease detection, rising screening rates for breast and cervical cancer, and growing use of ultrasound and imaging systems in pregnancy monitoring.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rising female population, improving access to maternal healthcare, expanding hospital infrastructure, and growing awareness of reproductive health in countries such as India and China.

- Contraceptive Devices are the fastest-growing product type, projected to register a CAGR of 7.8%, reflecting the surge in adoption of long-acting reversible contraceptives (LARCs), increasing family planning awareness, and expanding access to reproductive health services.

- The Pregnancy & Maternal Care segment dominated the application category with a 41.02% revenue share in 2025, led by rising global birth rates in developing regions and increasing emphasis on safe pregnancy monitoring.

- Hospitals accounted for 44.21% of the market, preferred by the high patient inflow for pregnancy care, gynecological surgeries, and cancer diagnostics.

- The Cancer Care segment is the fastest-growing application category, with a CAGR of 8.1%, driven by the rising prevalence of breast, cervical, and ovarian cancers globally.

Report Scope and Women’s Health Devices Market Segmentation

|

Attributes |

Women’s Health Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Hologic, Inc. (U.S.) · GE HealthCare (U.S.) · Siemens Healthineers AG (Germany) · Koninklijke Philips N.V. (Netherlands) · FUJIFILM Holdings Corporation (Japan) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · Medtronic (Ireland) · Boston Scientific Corporation (U.S.) · CooperSurgical Inc. (U.S.) · Cook Medical LLC (U.S.) · Bayer AG (Germany) · Olympus Corporation (Japan) · BD (U.S.) · Karl Storz SE & Co. KG (Germany) · Richard Wolf GmbH (Germany) · Stryker (U.S.) · Abbott (U.S.) · Elekta AB (Sweden) · Boston Imaging (U.S.) · Natus Medical Incorporated (U.S.) |

|

Market Opportunities |

· Rising adoption of FemTech-integrated wearable and AI-based diagnostic devices · Expanding demand for minimally invasive gynecological surgical devices · Increasing government-backed women’s health screening and maternal care programs in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Women’s Health Devices Market Trends

Trend: Growth in Digital FemTech & Connected Women’s Health Devices

The women’s health devices market is increasingly shifting toward digitalization, where FemTech-driven innovations are redefining how reproductive, maternal, and preventive healthcare is delivered. Connected devices such as smart fertility trackers, wearable ovulation monitors, and AI-enabled pregnancy care systems are enabling continuous, real-time health tracking beyond traditional clinical settings. This trend is being further strengthened by the integration of mobile applications with diagnostic devices, allowing patients to monitor hormonal changes, menstrual health, pregnancy progression, and chronic gynecological conditions remotely. Healthcare providers are also leveraging cloud-based dashboards and AI analytics to interpret patient-generated data, improving early diagnosis and personalized treatment decisions.

For instance, the October 2024 expansion of AI-integrated fertility ecosystems combining wearable biosensors and predictive analytics tools reflects how FemTech is moving toward holistic, data-driven reproductive health management systems that improve patient outcomes while reducing dependency on frequent clinical visits.

Women’s Health Devices Market Dynamics

Key Market Driver: Rising Prevalence of Gynecological and Reproductive Health Disorders

A major force driving the women’s health devices market is the increasing global burden of gynecological, reproductive, and hormone-related disorders. Conditions such as breast cancer, cervical cancer, ovarian disorders, uterine fibroids, and infertility are becoming more widely diagnosed due to improved awareness and better screening infrastructure. This has significantly increased demand for advanced diagnostic imaging systems, biopsy devices, minimally invasive surgical tools, and continuous monitoring technologies used in early detection and treatment.

For instance, 2024 national-level expansion of structured breast and cervical cancer screening programs in several developing countries demonstrates how public health systems are prioritizing early detection, which directly increases the utilization of diagnostic and monitoring devices in clinical workflows.

Key Restraint/Challenge: High Cost of Advanced Women’s Health Diagnostic and Surgical Devices

Despite strong demand growth, the market faces a significant barrier in the form of high costs associated with advanced women’s health technologies. Devices such as high-resolution imaging systems, robotic-assisted gynecological surgical platforms, and integrated diagnostic suites require substantial capital investment, making them difficult to adopt in resource-constrained healthcare settings. Beyond initial purchase costs, ongoing expenses related to maintenance, software upgrades, calibration, and skilled operator training further increase the total cost of ownership.

For instance, limited deployment of advanced 3D mammography systems and robotic-assisted hysterectomy platforms in low-income regions highlights how affordability constraints continue to slow down technology diffusion, despite the clear clinical advantages offered by next-generation women’s health devices.

Key Market Opportunity: Expansion of Preventive Screening & Early Detection Programs in Women’s Healthcare

A major growth opportunity in the global women’s health devices market lies in the rapid expansion of preventive screening and early detection initiatives targeting breast cancer, cervical cancer, osteoporosis, and reproductive health disorders. Governments, NGOs, and healthcare systems are increasingly prioritizing early diagnosis to reduce long-term treatment costs and improve survival rates, which is driving large-scale deployment of diagnostic imaging systems, point-of-care testing kits, and portable screening devices. This shift toward preventive healthcare is also encouraging manufacturers to develop compact, cost-effective, and mobile diagnostic solutions suitable for both urban hospitals and rural outreach programs.

For instance, the expansion of mobile mammography units and cervical cancer screening vans in 2024 across underserved regions demonstrates how decentralized healthcare delivery models are creating strong adoption opportunities for portable women’s health devices.

Women’s Health Devices Market Scope

The women’s health devices market is segmented on the basis of product type, application, and end user.

- By Product Type

On the basis of product type, the women’s health devices market is segmented into surgical devices, diagnostic devices, contraceptive devices, labor & delivery devices, and others. The Diagnostic Devices segment dominated the market with a 39.48% share in 2025, driven by increasing demand for early disease detection, rising screening rates for breast and cervical cancer, and growing use of ultrasound and imaging systems in pregnancy monitoring. These devices are widely used across hospitals, diagnostic centers, and gynecology clinics due to their ability to provide accurate, non-invasive, and early-stage disease identification. Continuous technological advancements in imaging resolution, portable diagnostic systems, and AI-enabled interpretation tools are further strengthening adoption. Increasing awareness of preventive healthcare among women is also boosting routine diagnostic testing. Government-led screening programs and maternal health initiatives are expanding usage across both developed and emerging economies. This segment remains central to clinical decision-making in women’s healthcare pathways.

The Contraceptive Devices segment is expected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by rising adoption of long-acting reversible contraceptives (LARCs), increasing family planning awareness, and expanding access to reproductive health services. Growing focus on women’s autonomy and reproductive choice is significantly contributing to demand for IUDs and implantable devices. Government-backed population control and maternal health programs are further supporting adoption in emerging economies. Advancements in device safety, reduced side effects, and minimally invasive insertion techniques are improving acceptance rates. Increasing participation of private healthcare providers and NGOs in reproductive education is also accelerating growth. Expanding awareness campaigns in rural and semi-urban regions are further strengthening market penetration.

- By Application

On the basis of application, the market is segmented into cancer care, pregnancy & maternal care, reproductive health disorders, uterine fibroids, osteoporosis, post-menopausal care, and others. The Pregnancy & Maternal Care segment dominated the market with a 41.02% share in 2025, supported by rising global birth rates in developing regions and increasing emphasis on safe pregnancy monitoring. Growing use of fetal monitoring systems, obstetric ultrasound devices, and prenatal diagnostic tools is driving segment dominance. Hospitals and maternity clinics extensively use these devices to reduce maternal and neonatal mortality risks. Increasing awareness of antenatal care and routine pregnancy screening is further supporting demand. Government healthcare programs focused on maternal health improvement are significantly boosting device adoption. Technological advancements in non-invasive monitoring and remote fetal tracking are also enhancing clinical efficiency.

The Cancer Care segment is expected to register the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by rising prevalence of breast, cervical, and ovarian cancers globally. Expanding screening programs and early detection initiatives are increasing the use of mammography systems, biopsy devices, and imaging technologies. Awareness campaigns and national cancer prevention strategies are encouraging routine screening among women. Increasing adoption of AI-assisted imaging tools is improving diagnostic accuracy and early intervention rates. Growing healthcare investments in oncology infrastructure are further accelerating demand. Continuous innovation in minimally invasive diagnostic and surgical tools is also strengthening this segment’s growth trajectory.

- By End User

On the basis of end user, the market is segmented into hospitals, gynecology & obstetrics clinics, diagnostic centers, ambulatory surgical centers, and home care settings. The Hospitals segment dominated the market with a 44.21% share in 2025, owing to high patient inflow for pregnancy care, gynecological surgeries, and cancer diagnostics. Hospitals serve as primary centers for advanced imaging, surgical procedures, and emergency maternal care. Availability of skilled healthcare professionals and advanced infrastructure supports widespread adoption of women’s health devices. Integration of multi-specialty departments further enhances diagnostic and treatment capabilities. Government funding and insurance coverage in hospital settings are also driving higher utilization rates. Increasing hospital-based screening programs and maternal care units are strengthening this segment’s dominance globally.

The Ambulatory Surgical Centers (ASCs) segment is expected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by the growing shift toward outpatient minimally invasive procedures. ASCs offer cost-effective treatment options with shorter recovery times and reduced hospital stays. Increasing preference for day-care gynecological surgeries such as hysteroscopy and laparoscopic procedures is boosting adoption. Technological advancements in portable surgical devices are enabling complex procedures outside traditional hospital settings. Rising healthcare cost pressures are pushing patients toward outpatient care models. Expanding healthcare infrastructure in emerging economies is further accelerating ASC adoption.

Women’s Health Devices Market Regional Analysis

North America dominated the global women’s health devices market with the largest revenue share of 36.92% in 2025, supported by advanced healthcare infrastructure, high screening rates for breast and cervical cancer, and strong adoption of minimally invasive gynecological procedures. The region also benefits from well-established reimbursement systems, widespread implementation of breast and cervical cancer screening programs, and the presence of leading medical device manufacturers. Increasing prevalence of gynecological disorders and rising demand for minimally invasive procedures further strengthen market growth across hospitals, diagnostic centers, and specialty clinics. Continuous innovation in FemTech, AI-enabled diagnostics, and digital health integration continues to reinforce North America’s leadership position in the global market.

U.S. Women’s Health Devices Market Insight

The U.S. women’s health devices market is witnessing strong growth due to high healthcare spending, advanced hospital infrastructure, and widespread adoption of innovative diagnostic and surgical technologies. The country has a mature ecosystem for breast cancer screening, cervical cancer prevention, and maternal health monitoring, supported by strong insurance coverage and government-led awareness programs. Increasing prevalence of reproductive health disorders and rising demand for minimally invasive gynecological procedures are further driving device adoption. Strong presence of global medical device companies and FemTech startups is accelerating innovation in AI-enabled diagnostics and connected health solutions. In addition, growing focus on personalized medicine and digital health integration is enhancing early detection and treatment outcomes across healthcare settings.

Europe Women’s Health Devices Market Insight

Europe remains a key region in the global women’s health devices market, driven by strong public healthcare systems, structured national screening programs, and high awareness of early diagnosis for women-specific diseases. The region shows widespread adoption of breast cancer and cervical cancer screening initiatives, supported by government-led preventive healthcare policies. Growing demand for minimally invasive gynecological procedures and advanced imaging technologies is further contributing to market growth across hospitals and diagnostic centers. Increasing investments in digital health transformation and FemTech solutions are enhancing access to innovative women’s healthcare devices. Rising focus on aging population care and post-menopausal health management is also supporting sustained regional demand.

U.K. Women’s Health Devices Market Insight

The U.K. women’s health devices market is witnessing steady growth, supported by strong public health programs, increasing investment in women’s health screening, and rising adoption of advanced diagnostic technologies. Growing demand for fertility monitoring, pregnancy care solutions, and cancer screening devices is driving market expansion across healthcare facilities. Integration of AI-based diagnostic tools and digital health platforms is improving early detection and patient management efficiency. The presence of well-established healthcare infrastructure and focus on preventive care further strengthens adoption. In addition, increasing awareness of reproductive health and government-led screening initiatives are contributing to sustained market growth.

Germany Women’s Health Devices Market Insight

The Germany women’s health devices market is expanding steadily due to strong healthcare infrastructure, advanced medical research capabilities, and high adoption of precision diagnostic and surgical technologies. Hospitals and diagnostic centers are increasingly using advanced imaging systems and minimally invasive devices for gynecological and reproductive healthcare. Strong government support for early disease detection programs, particularly in breast and cervical cancer screening, is further driving demand. Continuous technological advancements in AI-assisted diagnostics and digital healthcare integration are enhancing clinical efficiency. In addition, Germany’s strong medical device manufacturing base supports innovation and market expansion.

Asia-Pacific Women’s Health Devices Market Insight

The Asia-Pacific region is expected to witness the fastest growth in the global women’s health devices market, driven by rising female population, improving healthcare infrastructure, and increasing government focus on maternal and reproductive health programs. Expanding awareness of breast cancer screening, cervical cancer prevention, and prenatal care is significantly boosting demand for diagnostic and monitoring devices. Growing healthcare investments, rising medical tourism, and increasing adoption of cost-effective medical technologies are further supporting regional expansion. The presence of large underserved populations and improving rural healthcare access are also accelerating market penetration. In addition, increasing participation of private healthcare providers is strengthening growth across emerging economies.

Japan Women’s Health Devices Market Insight

The Japan women’s health devices market is witnessing steady growth due to advanced healthcare systems, strong focus on preventive care, and rising adoption of high-precision diagnostic technologies. Increasing demand for cancer screening, fertility management, and maternal care devices is driving market expansion. The integration of AI, robotics, and digital health solutions is improving diagnostic accuracy and treatment outcomes. Japan’s aging female population is further increasing demand for post-menopausal care and chronic condition management. Continuous innovation in minimally invasive procedures and imaging technologies is also supporting market growth.

China Women’s Health Devices Market Insight

The China women’s health devices market is growing rapidly, driven by increasing urbanization, rising healthcare investments, and strong government focus on women’s health and maternal care programs. Expanding awareness of preventive screening for breast and cervical cancer is boosting demand for diagnostic devices. Rapid expansion of hospital infrastructure and increasing adoption of AI-enabled imaging and monitoring systems are further strengthening market growth. Growing medical tourism and rising presence of domestic medical device manufacturers are improving accessibility and affordability. In addition, continuous technological advancements and large population base are positioning China as a key high-growth market globally.

Women’s Health Devices Market Share

The women’s health devices industry is primarily led by well-established companies, including:

- Hologic, Inc. (U.S.)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- FUJIFILM Holdings Corporation (Japan)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- CooperSurgical Inc. (U.S.)

- Cook Medical LLC (U.S.)

- Bayer AG (Germany)

- Olympus Corporation (Japan)

- BD (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Stryker (U.S.)

- Abbott (U.S.)

- Elekta AB (Sweden)

- Boston Imaging (U.S.)

- Natus Medical Incorporated (U.S.)

Latest Developments in Women’s Health Devices Market

- In April 2025, Philips announced enhancements to its women’s health ultrasound solutions, focusing on AI-assisted imaging workflows and improved diagnostic efficiency in obstetrics and gynecology. The updates are aimed at improving workflow automation, enhancing image clarity, and supporting clinicians in early detection of fetal and reproductive health conditions. This development reflects increasing integration of AI in diagnostic imaging systems. It also reinforces Philips’ position in advancing precision imaging for women’s healthcare

- In May 2024, the U.S. Food and Drug Administration (FDA) expanded the use of HPV self-collection testing in healthcare settings using Roche’s cobas® HPV test, marking a major step forward in cervical cancer screening accessibility. This development enables women to collect samples in clinical environments, improving screening participation and early detection rates for cervical cancer. The approval reflects growing emphasis on less invasive, more accessible diagnostic methods in women’s health. It is expected to significantly improve screening coverage in underserved populations and strengthen preventive healthcare frameworks globally

- In July 2023, GE HealthCare announced advancements in its Voluson™ ultrasound portfolio, enhancing imaging performance for obstetrics and gynecology applications. The upgraded systems are designed to improve fetal imaging accuracy, streamline workflow efficiency, and support early detection of reproductive health conditions. These innovations strengthen the role of ultrasound in maternal care and gynecological diagnostics. The development highlights increasing integration of AI and automation in women’s imaging technologies

- In March 2022, Hologic announced enhancements to its Genius™ Digital Diagnostics System, integrating AI-powered tools to improve the detection of cervical cancer and other gynecological abnormalities. The system strengthens diagnostic accuracy by combining high-resolution imaging with artificial intelligence-based interpretation. This advancement supports earlier and more reliable cancer detection in women’s health screening programs. It reflects the broader industry shift toward AI-enabled diagnostic imaging solutions

- In September 2021, Medtronic expanded the clinical adoption of its Hugo™ robotic-assisted surgery (RAS) system across Europe, including applications in minimally invasive gynecological procedures. The system is designed to improve surgical precision, reduce recovery times, and enhance patient outcomes in complex procedures. This expansion highlights growing acceptance of robotic technologies in women’s health surgery. It also supports the broader transition toward minimally invasive treatment approaches in gynecology

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.