Global Zero Liquid Discharge System Market

Market Size in USD Billion

USD

7.12 Billion

USD

12.36 Billion

2024

2032

USD

7.12 Billion

USD

12.36 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 7.12 Billion |

Market Size (Forecast Year) |

USD 12.36 Billion |

CAGR |

% |

Major Markets Players |

|

Zero liquid discharge Market Size

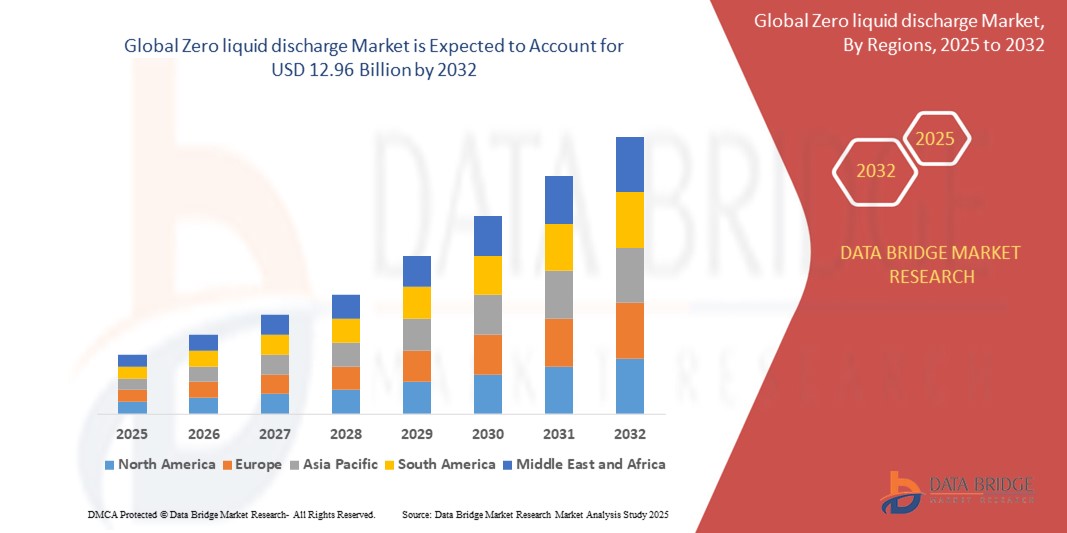

- The Global Zero liquid discharge Market size was valued at USD 7.12 Billion in 2024 and is expected to reach USD 12.96 Billion by 2032, at a CAGR of 7.77% during the forecast period

- Market growth is primarily driven by increasing environmental regulations, growing concerns over industrial wastewater discharge, and the rising need for water reuse and resource recovery, especially in water-stressed regions

- Additionally, advancements in membrane technologies, crystallizers, and thermal systems, along with the integration of automation and digital monitoring, are contributing to the expansion of the market. These trends collectively underscore a strong outlook for the global ZLD market.

Zero liquid discharge Market Analysis

- Zero Liquid Discharge (ZLD) is a wastewater management approach that ensures that no liquid waste leaves the system, making it vital for industries under pressure to meet stringent discharge regulations. It is increasingly adopted in power generation, chemicals, pharmaceuticals, food & beverage, and textile industries

- The rising demand for ZLD systems is fueled by increasing industrialization, tightening environmental norms (e.g., by EPA, EU directives, and CPCB in India), and a growing emphasis on corporate sustainability goals

- Asia-Pacific dominates the Global ZLD Market, with the largest revenue share in 2025, due to strong industrial activity, government initiatives for pollution control, and growing ZLD mandates in China and India

- North America is expected to be the fastest-growing region, driven by strict regulatory frameworks, technological innovation, and the adoption of water recycling systems in key industries like oil & gas and pharmaceuticals

- The chemical & petrochemical segment is anticipated to lead the ZLD market with a significant market share, supported by high wastewater generation, complex effluents, and the necessity of meeting compliance standards

Report Scope and Zero liquid discharge Market Segmentation

|

Attributes |

Zero liquid discharge Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Zero liquid discharge Market Trends

“Circular Economy and Industrial Water Reuse Shape Market Evolution”

- A major trend in the Global Zero Liquid Discharge Market is the rising adoption of circular economy principles, with industries increasingly focusing on waste minimization, resource recovery, and recycling of wastewater, driven by water scarcity and stricter discharge norms

- Integration of smart monitoring and control systems—including IoT-based sensors, SCADA, and AI-driven analytics—is enhancing system efficiency, real-time data collection, and process automation in ZLD operations

- Modular and skid-mounted ZLD systems are gaining popularity, especially in remote industrial locations and smaller facilities, due to their ease of installation, scalability, and lower capital investment

- There is a growing trend towards hybrid ZLD systems that combine thermal and membrane-based processes to optimize energy usage and reduce operational costs. This is particularly relevant in energy-intensive industries like power generation and chemicals

- The shift toward renewable-powered and energy-efficient ZLD systems, including solar-assisted evaporators and low-pressure membrane systems, is growing, aligned with broader decarbonization and sustainability goals of global industries

Zero liquid discharge Market Dynamics

Driver

“Stricter Environmental Regulations and Industrial Water Reuse Mandates”

- One of the key drivers for the Global ZLD Market is the tightening of wastewater discharge regulations by environmental authorities such as the EPA (USA), Central Pollution Control Board (India), and EU Water Framework Directive, mandating zero or minimal liquid effluent release

- Industries such as chemicals, textiles, oil & gas, and pharmaceuticals are under increased pressure to comply with ZLD norms, especially in water-stressed and industrialized regions

- Water reuse and recycling have become core strategies for sustainable industrial operations, not only for regulatory compliance but also for cost-saving and ESG reporting

- Government incentives, funding for water treatment infrastructure, and public-private partnerships (PPPs) in emerging markets are further accelerating ZLD adoption

Restraint/Challenge

“High Capital and Operating Costs of ZLD Systems”

- A significant restraint in the ZLD market is the high initial capital expenditure (CapEx) required for system installation, especially for thermal ZLD processes involving evaporators and crystallizers

- Operating expenses (OpEx), particularly energy consumption, maintenance of membranes and components, and brine management, remain substantial, deterring small and mid-sized industries from adoption

- Technical complexity, including scaling, fouling, and corrosion in system components, can reduce efficiency and require skilled personnel and advanced pre-treatment methods

- The lack of standardized regulatory frameworks across countries adds complexity to implementation, necessitating region-specific customization, which increases costs and deployment time

Zero liquid discharge Market Scope

The market is segmented on the basis of system, process, technology and end user.

- By System

On the basis of system, the zero liquid discharge system market is segmented into conventional and hybrid. The Hybrid ZLD segment dominates the largest market revenue share of 44.2% in 2025, owing to its ability to combine membrane and thermal technologies for higher efficiency and cost-effectiveness. Hybrid systems are increasingly preferred in industries that require scalable and energy-optimized solutions.

The Conventional ZLD segment continues to be adopted in legacy infrastructure, but is witnessing slower growth due to higher energy consumption and limited flexibility compared to hybrid solutions.

- By Process

On the basis of process, the market is segmented into pretreatment process, filtration process, evaporation process and crystallization process. The Evaporation Process segment is expected to lead in market share in 2025, as it plays a critical role in concentrating wastewater before final crystallization, particularly in high-salinity streams.

The Crystallization Process is projected to witness the fastest CAGR from 2025 to 2032, driven by increasing demand for total solute recovery and compliance with stringent ZLD mandates across high-pollution industries such as chemicals and mining.

- By Technology

On the basis of technology, the zero liquid discharge system market is segmented into reverse osmosis (RO), ultrafiltration (UF) and evaporation and crystallization. The Evaporation & Crystallization segment holds the largest revenue share in 2025, due to its essential role in achieving near-complete liquid waste elimination. It is especially vital in industries with complex or high-contaminant wastewater.

Reverse Osmosis (RO) is expected to experience strong growth owing to increasing demand for energy-efficient pre-concentration of effluent streams. RO is commonly integrated into hybrid systems to reduce the load on thermal components.

- By End User

On the basis of end user market is segmented into energy and power, chemicals and petrochemicals, food and beverages, textiles, pharmaceuticals, semiconductors and electronics and others. The Energy & Power sector leads the market in 2025, owing to the large volume of wastewater generated in thermal power plants and regulatory pressures for water reuse and zero discharge.

The Semiconductors & Electronics segment is projected to witness the fastest growth rate from 2025 to 2032, supported by the increasing number of manufacturing facilities in Asia-Pacific and the critical requirement for ultrapure water recycling in chip production processes.

Zero liquid discharge Market Regional Analysis

- Asia-Pacific dominates the Global Zero Liquid Discharge Market with the largest revenue share of 37.9% in 2024, driven by rapid industrialization, increased urbanization, and stringent environmental regulations across major economies such as China, India, and Japan

- The region’s expanding manufacturing base—especially in industries such as textiles, chemicals, power, and semiconductors—is increasing demand for ZLD systems to manage rising wastewater volumes

- Governments in Asia-Pacific are actively promoting water reuse and pollution control through regulatory frameworks, such as India’s Central Pollution Control Board mandates and China’s Water Ten Plan

- The presence of numerous local and international solution providers, growing investment in infrastructure, and the adoption of hybrid ZLD systems for cost and energy optimization are contributing to robust market growth in the region

U.S. Zero Liquid Discharge Market Insight

The U.S. Zero Liquid Discharge market captured the largest revenue share of over 68.2% within North America in 2025, driven by strict discharge regulations by the Environmental Protection Agency (EPA), rising concerns over water scarcity, and strong demand from industries such as oil & gas, pharmaceuticals, and power generation. The adoption of advanced ZLD technologies is bolstered by industrial water reuse initiatives and increasing focus on ESG (Environmental, Social, and Governance) compliance. Investment in energy-efficient and modular ZLD systems is rising, particularly in regions facing water stress, such as California and Texas.

Europe Zero Liquid Discharge Market Insight

The Europe Zero Liquid Discharge market is projected to grow at a stable CAGR throughout the forecast period, supported by stringent EU directives such as the Water Framework Directive and increasing industrial focus on circular water economy practices. Countries like Germany, France, and Italy are investing heavily in water reuse technologies to combat resource scarcity and meet sustainability goals. The region's mature industrial base and high environmental awareness drive adoption of cutting-edge ZLD technologies, including crystallizers, membrane systems, and low-energy evaporators.

U.K. Zero Liquid Discharge Market Insight

The U.K. Zero Liquid Discharge market is anticipated to grow at a robust CAGR during the forecast period due to increasing demand for water recovery and compliance with national environmental policies post-Brexit. Industries such as food & beverage, pharmaceuticals, and chemicals are investing in sustainable water management solutions. Technological partnerships and government incentives for water efficiency in manufacturing are accelerating ZLD system installations across industrial estates.

Germany Zero Liquid Discharge Market Insight

The Germany Zero Liquid Discharge market is expected to witness steady growth, driven by the country's leadership in environmental regulation and innovation in industrial water treatment. Adoption is strong in sectors like chemicals, automotive, and manufacturing, where water reuse and waste minimization are strategic priorities. The market also benefits from Germany’s advanced engineering capabilities and emphasis on energy-efficient and compact ZLD systems.

Asia-Pacific Zero Liquid Discharge Market Insight

The Asia-Pacific ZLD market is poised to grow at the fastest CAGR of over 9.2% in 2025, supported by growing environmental awareness and government mandates for wastewater management in industrial hotspots. The expansion of manufacturing and energy sectors in China, India, and Southeast Asia is creating strong demand for high-capacity and cost-effective ZLD systems. Local governments are increasingly offering subsidies and policy support for zero-discharge compliance, especially in highly polluting industries like textiles and chemicals.

Japan Zero Liquid Discharge Market Insight

The Japan ZLD market is gaining momentum as the country pushes for sustainable industrial practices and advanced wastewater recycling technologies. Adoption is driven by the need for ultrapure water in the electronics and semiconductor industries, where water quality directly affects product output. Japan’s engineering expertise and commitment to compact, energy-saving technologies are fostering growth in hybrid ZLD solutions tailored to urban and space-constrained industrial zones.

China Zero Liquid Discharge Market Insight

The China ZLD market accounted for the largest market share in Asia-Pacific in 2025, supported by aggressive government actions to curb water pollution and upgrade industrial water management infrastructure. Enforcement of zero-discharge norms in the textile, coal-to-chemical, and pharmaceutical sectors is a major growth driver. Rapid urbanization and strong capital investment in environmental tech are enabling faster deployment of large-scale ZLD systems, particularly in Eastern and Northern China.

Zero liquid discharge Market Share

The Zero liquid discharge industry is primarily led by well-established companies, including:

- Veolia Water Technologies (France)

- GE Water & Process Technologies / SUEZ (France)

- Aquatech International LLC (United States)

- Thermax Limited (India)

- GEA Group AG (Germany)

- Alfa Laval (Sweden)

- Doosan Enpure (United Kingdom)

- IDE Technologies (Israel)

- Praj Industries (India)

- Aqua Engineering GmbH (Austria)

- Saltworks Technologies Inc. (Canada)

- WesTech Engineering, LLC (United States)

- Triveni Engineering & Industries Ltd. (India)

- Oasys Water (United States)

Latest Developments in Global Zero liquid discharge Market

- In April 2024, Veolia Water Technologies announced the launch of its next-generation modular ZLD system, SIRION™ Advanced ZLD, designed for rapid deployment in chemical and textile industries. The system features integrated AI for real-time optimization of water recovery and energy usage

- In February 2024, IDE Technologies partnered with a leading Indian chemical manufacturer to deploy its advanced MAXH2O Desalter ZLD technology, enabling higher recovery rates and reduced sludge volumes. The collaboration supports stricter compliance with India’s industrial discharge regulations

- In November 2023, Aquatech International LLC unveiled a new thermal ZLD system using Low Energy Evaporation Technology (LEET) aimed at reducing energy consumption by up to 40%. The solution targets power plants and large industrial clusters in water-stressed regions

- In September 2023, Thermax Limited inaugurated a new ZLD R&D and demonstration facility in Pune, India, to enhance system testing, customer training, and the development of cost-effective hybrid ZLD solutions for the Asia-Pacific market

- In July 2023, Saltworks Technologies Inc. introduced an upgraded version of its FlexEDR™ and SaltMaker™ modular ZLD platforms, incorporating predictive maintenance and machine learning algorithms to reduce downtime and optimize throughput

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Zero Liquid Discharge System Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Zero Liquid Discharge System Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Zero Liquid Discharge System Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.