Global Zero Waste Packaged Foods Market

Market Size in USD Billion

USD

1.98 Billion

USD

5.51 Billion

2025

2033

USD

1.98 Billion

USD

5.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.98 Billion | |

| USD 5.51 Billion | |

| % | |

|

Zero-Waste Packaged Foods Market Size

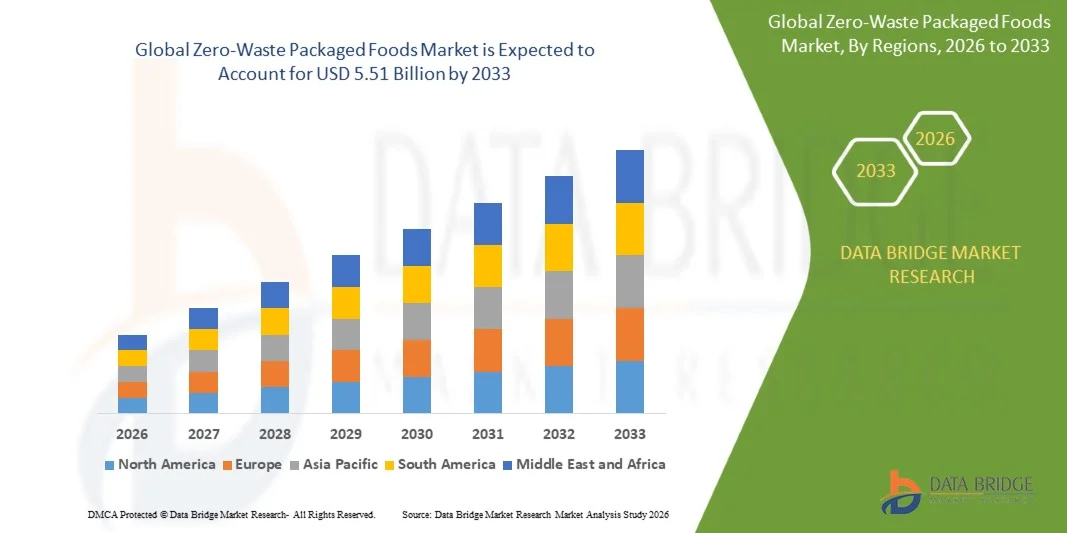

- As per Data Bridge Market Research Analysis the global zero-waste packaged foods market size was valued at USD 1.98 billion in 2025 and is expected to reach USD 5.51 billion by 2033, at a CAGR of 13.65% during the forecast period

- The market growth is largely fueled by the increasing consumer awareness regarding environmental sustainability and the rising shift toward reducing food and packaging waste, leading to greater adoption of eco-friendly packaging solutions across both retail and food service sectors

- Furthermore, growing demand for sustainable, reusable, and biodegradable food packaging solutions among environmentally conscious consumers is establishing zero-waste packaged foods as a preferred choice. These converging factors are accelerating the adoption of zero-waste practices, thereby significantly boosting the market growth

Market Size & Forecast

- Global Market Value (2025): USD 1.98 billion

- Expected Market Value (2033): USD 5.51 billion

- Forecast CAGR (2026–2033): 13.65%

Zero-Waste Packaged Foods Market Analysis

- Zero-waste packaged foods refer to food products that are produced, distributed, and consumed with minimal environmental impact through the elimination or reduction of packaging waste, often utilizing reusable, recyclable, or compostable materials. These solutions integrate sustainable sourcing, eco-friendly packaging, and circular consumption models across the food value chain

- The escalating demand for zero-waste packaged foods is primarily fueled by increasing regulatory pressure on plastic usage, rising adoption of bulk and refill-based retail systems, and growing consumer preference for environmentally responsible consumption patterns

- Asia-Pacific dominated the zero-waste packaged foods market with a share of 47.3% in 2025, due to rising environmental awareness, increasing urban population, and strong demand for sustainable food consumption practices across emerging economies

- North America is expected to be the fastest growing region in the zero-waste packaged foods market during the forecast period due to increasing demand for sustainable food packaging, rising environmental awareness, and strong presence of eco-conscious consumers

- Paper and cardboard segment dominated the market with a market share of 77.4% in 2025, due to its wide availability, low cost, and strong recyclability profile. It is extensively used for dry food products, bakery items, and takeaway packaging due to its lightweight structure and ease of customization. Retailers prefer paper-based packaging as it aligns with sustainability targets and regulatory restrictions on plastics

Report Scope and Zero-Waste Packaged Foods Market Segmentation

|

Attributes |

Zero-Waste Packaged Foods Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Zero-Waste Packaged Foods Market Trends

Growing Adoption of Sustainable and Circular Packaging Solutions

- A significant trend in the zero-waste packaged foods market is the increasing adoption of sustainable and circular packaging systems, driven by rising environmental concerns and the need to minimize food and packaging waste across the value chain. This shift is encouraging companies to redesign packaging with reusable, recyclable, and compostable materials while promoting closed-loop consumption models

- For instance, Notpla Limited has developed seaweed-based packaging solutions used by food service providers to replace single-use plastics. These innovations support biodegradability and reduce environmental impact while maintaining product safety and usability in real-world applications

- The growing expansion of refill and bulk purchasing models is transforming traditional food retail systems by reducing dependency on disposable packaging. Consumers are increasingly opting for zero-waste grocery formats that allow reuse of containers and controlled purchasing quantities

- Food manufacturers are integrating circular design principles into packaging development, focusing on material reduction and lifecycle optimization. This is leading to innovations in lightweight, compostable, and reusable packaging formats that align with sustainability goals

- The rising collaboration between packaging companies and food brands is accelerating the commercialization of eco-friendly materials suitable for various food applications. These partnerships are strengthening supply chains and enhancing the scalability of zero-waste packaging solutions

- The market is witnessing a structural transition toward sustainable consumption patterns where packaging is designed to minimize environmental footprint while maintaining functionality. This trend is reinforcing the long-term shift toward circular economy practices and supporting steady growth of the zero-waste packaged foods market

Zero-Waste Packaged Foods Market Dynamics

Driver

Rising Consumer Demand for Eco-Friendly and Waste-Reducing Food Products

- The increasing consumer preference for environmentally responsible products is driving demand for zero-waste packaged foods, as individuals seek to reduce their ecological footprint through conscious purchasing decisions. This shift is encouraging food companies to adopt sustainable packaging and production practices to align with evolving consumer expectations

- For instance, TerraCycle has partnered with major food brands to introduce reusable packaging platforms through its Loop initiative. These systems enable consumers to purchase products in returnable containers, significantly reducing single-use packaging waste and supporting circular consumption models

- The growing awareness of plastic pollution and its environmental impact is influencing purchasing behavior across both developed and emerging markets. Consumers are prioritizing products with minimal or biodegradable packaging, which is accelerating demand for zero-waste alternatives

- Retailers and food service providers are responding by expanding sustainable product offerings and integrating refill-based systems into their operations. This is enhancing accessibility and visibility of zero-waste packaged foods across multiple distribution channels

- The continuous alignment of consumer values with environmental sustainability is strengthening demand for zero-waste packaged foods. This evolving preference is playing a crucial role in driving long-term market expansion and encouraging widespread adoption of waste-reducing practices

Restraint/Challenge

High Cost and Limited Scalability of Sustainable Packaging Infrastructure

- The zero-waste packaged foods market faces challenges due to the high cost associated with sustainable packaging materials and the limited scalability of eco-friendly infrastructure. Advanced materials such as biopolymers and compostable packaging often require higher production costs compared to conventional plastics, impacting overall pricing

- For instance, Xampla Ltd. develops plant-protein-based biodegradable packaging, which involves complex processing techniques and specialized resources. These factors increase production expenses and limit large-scale adoption across cost-sensitive markets

- The lack of widespread composting and recycling infrastructure in many regions restricts the effective disposal and processing of sustainable packaging materials. This creates challenges in achieving the intended environmental benefits of zero-waste solutions

- Small and medium-sized enterprises often face financial and operational barriers in transitioning to sustainable packaging systems due to high initial investment requirements. This slows down adoption across fragmented market segments

- The ongoing challenge of achieving cost-effective scalability while maintaining environmental benefits is impacting market expansion. These constraints are compelling industry participants to invest in innovation and infrastructure development to overcome barriers and support long-term growth

Zero-Waste Packaged Foods Market Scope

The market is segmented on the basis of product type, packaging material, and distribution channel.

• By Product Type

On the basis of type, the Zero-Waste Packaged Foods market is segmented into Upcycled Snacks, Zero-Waste Grocery, Plant-Based Alternatives, Ready-to-Eat Meals, and Liquid/Refillables. The Zero-Waste Grocery segment dominated the largest market revenue share in 2025, driven by increasing consumer preference for bulk purchasing and packaging-free essentials such as grains, nuts, and spices. Retailers and sustainable grocery chains are expanding refill stations and dispenser-based models, reducing dependence on single-use packaging. Growing environmental awareness among consumers is further encouraging adoption of reusable containers and store-based refill systems. Strong government support for plastic reduction policies is also reinforcing demand across urban retail formats.

The Ready-to-Eat Meals segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for convenience-oriented sustainable food options. Consumers are increasingly seeking packaged meals that combine ease of consumption with compostable or biodegradable packaging solutions. Food service providers and delivery platforms are actively shifting toward eco-friendly meal packaging to align with sustainability commitments. Urban lifestyles and time-constrained consumers are accelerating adoption of these solutions across metro cities. Innovation in compostable trays and plant-based packaging materials is further supporting rapid expansion of this segment.

• By Packaging Material

On the basis of packaging material, the market is segmented into Paper and Cardboard, Biopolymers (PLA), Glass Packaging, Metal Packaging, and Edible Packaging. The Paper and Cardboard segment dominated the largest market revenue share of 77.4% in 2025, driven by its wide availability, low cost, and strong recyclability profile. It is extensively used for dry food products, bakery items, and takeaway packaging due to its lightweight structure and ease of customization. Retailers prefer paper-based packaging as it aligns with sustainability targets and regulatory restrictions on plastics. Increasing consumer preference for biodegradable packaging formats is further strengthening its dominance. Established recycling infrastructure also supports large-scale adoption across global supply chains.

The Biopolymers (PLA) segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for fully compostable packaging derived from renewable resources. Food manufacturers are adopting PLA-based solutions to reduce dependence on fossil-fuel-based plastics. Its ability to decompose under industrial composting conditions makes it highly suitable for sustainable food packaging applications. Advancements in material strength and heat resistance are expanding its use in both retail and food service sectors. Rising investments in bio-based material innovation are further accelerating market penetration.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Retail/Grocery Stores, Restaurants & Food Service, and Online Delivery Services. The Retail/Grocery Stores segment dominated the largest market revenue share in 2025, driven by the rapid expansion of sustainable retail formats offering bulk and package-free products. Consumers prefer in-store refill systems that allow direct control over packaging reduction and product quantity. Supermarkets and specialty organic stores are increasingly integrating zero-waste sections to attract environmentally conscious buyers. Strong visibility and accessibility of eco-friendly packaged foods in retail outlets further support segment dominance. Government-led plastic reduction initiatives are also encouraging retailers to adopt sustainable packaging systems.

The Online Delivery Services segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rapid expansion of food delivery platforms adopting sustainable packaging solutions. Increasing demand for home delivery of eco-friendly meals is pushing brands to adopt compostable and reusable packaging formats. Digital ordering convenience combined with sustainability preferences is accelerating online channel penetration. Food aggregators are partnering with eco-packaging providers to reduce environmental impact. Growing urbanization and smartphone penetration are further supporting strong growth in this segment.

Zero-Waste Packaged Foods Market Regional Analysis

- Asia-Pacific dominated the zero-waste packaged foods market with the largest revenue share of 47.3% in 2025, driven by rising environmental awareness, increasing urban population, and strong demand for sustainable food consumption practices across emerging economies

- The region’s expanding retail infrastructure, rapid growth of zero-waste stores, and increasing adoption of eco-friendly packaging solutions are accelerating market expansion

- Government initiatives to reduce plastic waste, growing middle-class population, and increasing preference for bulk and refill-based grocery models are contributing to higher adoption across the region

China Zero-Waste Packaged Foods Market Insight

China held the largest share in the Asia-Pacific zero-waste packaged foods market in 2025, owing to its large consumer base and strong government regulations focused on reducing plastic waste. The country is witnessing increasing adoption of sustainable retail formats, including bulk stores and refill stations in urban areas. Rapid expansion of e-commerce platforms integrating eco-friendly packaging and strong domestic manufacturing capabilities are further driving market growth.

India Zero-Waste Packaged Foods Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rising environmental consciousness, increasing government initiatives such as plastic ban, and growing demand for sustainable food products. The expansion of organic and zero-waste retail stores, along with increasing urbanization and disposable income, is supporting adoption. In addition, startups focusing on refill-based delivery models and eco-friendly packaging innovations are contributing to market expansion.

Europe Zero-Waste Packaged Foods Market Insight

The Europe zero-waste packaged foods market is expanding steadily, supported by stringent environmental regulations, strong consumer awareness regarding sustainability, and widespread adoption of circular economy practices. The region emphasizes reducing food and packaging waste through innovative solutions and policy frameworks. Increasing investments in biodegradable packaging and zero-waste retail chains are further driving market growth.

Germany Zero-Waste Packaged Foods Market Insight

Germany’s zero-waste packaged foods market is driven by its advanced recycling infrastructure, strong regulatory environment, and high consumer preference for sustainable products. The country has a well-established network of zero-waste stores and bulk supermarkets promoting packaging-free consumption. Continuous innovation in eco-friendly packaging materials and strong industry participation are supporting steady market expansion.

U.K. Zero-Waste Packaged Foods Market Insight

The U.K. market is supported by increasing consumer awareness regarding plastic reduction, strong presence of sustainable food brands, and growing adoption of refill and reuse models. Government policies promoting reduced packaging waste and rising investments in sustainable retail formats are driving demand. Expansion of online zero-waste delivery services is further strengthening the market position.

North America Zero-Waste Packaged Foods Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for sustainable food packaging, rising environmental awareness, and strong presence of eco-conscious consumers. Growth in zero-waste grocery stores and increasing adoption of compostable packaging solutions are boosting market expansion. In addition, technological advancements in packaging materials and increasing corporate sustainability commitments are supporting growth.

U.S. Zero-Waste Packaged Foods Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by high consumer awareness, strong demand for organic and sustainable food products, and the presence of established zero-waste retail chains. The country is witnessing increasing adoption of refill-based shopping models and eco-friendly packaging solutions. Strong innovation ecosystem and active participation from food brands in sustainability initiatives are further strengthening market growth

Zero-Waste Packaged Foods Market Share

The zero-waste packaged foods industry is primarily led by well-established companies, including:

- Tetra Pak (Switzerland)

- Notpla Limited (U.K.)

- Xampla Ltd. (U.K.)

- Eco-Products Inc. (U.S.)

- Sri Avani EcoLife Private Limited (India)

- Evoware (Indonesia)

- Biome Bioplastics (U.K.)

- Mondi (U.K.)

- DS Smith (U.K.)

- Futamura Group (Japan)

- Misfits Market (U.S.)

- Fresh Prep Foods (Canada)

- Loliware (U.S.)

- Lifepack (Indonesia)

- Zero Impack (India)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Zero Waste Packaged Foods Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Zero Waste Packaged Foods Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Zero Waste Packaged Foods Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.