Global Zinc Chemicals Market

Market Size in USD Billion

USD

10.25 Billion

USD

15.24 Billion

2024

2032

USD

10.25 Billion

USD

15.24 Billion

2024

2032

| 2025 - 2032 | |

| USD 10.25 Billion | |

| USD 15.24 Billion | |

| % | |

|

Zinc Chemicals Market Size

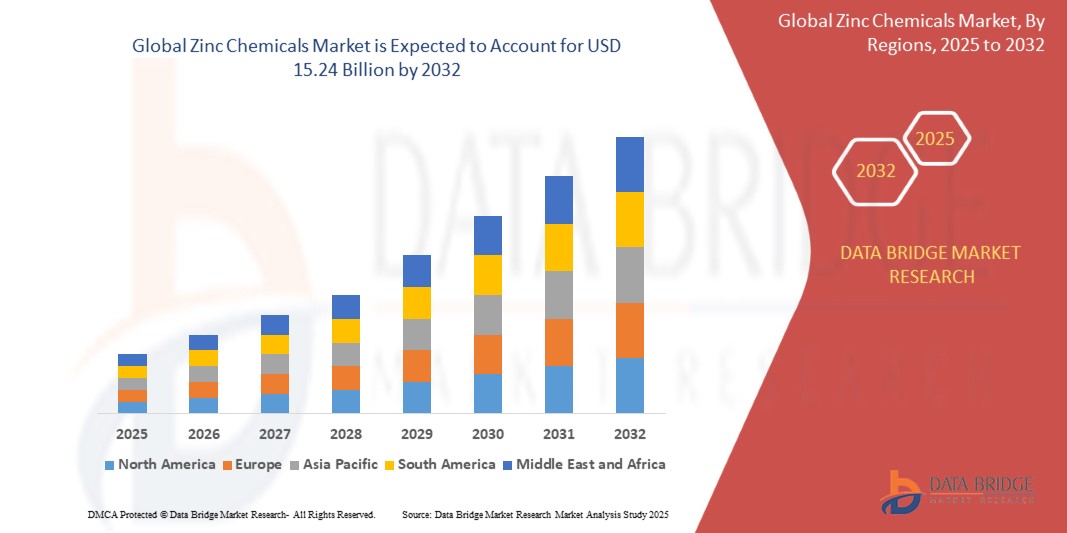

- The global zinc chemicals market was valued at USD 10.25 billion in 2024 and is expected to reach USD 15.24 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 5.08%, primarily driven by the rising demand across diverse industrial applications

- This growth is fueled by increasing usage of zinc chemicals in rubber compounding, ceramics, glass manufacturing, agriculture, and paints & coatings. The growing need for zinc-based fertilizers to enhance crop productivity in agriculture is significantly boosting the market

Zinc Chemicals Market Analysis

- Zinc chemicals are essential compounds widely used in various industrial applications, including rubber manufacturing, agriculture, pharmaceuticals, ceramics, and paints & coatings. These chemicals play vital roles such as vulcanization accelerators, fertilizers, catalysts, and corrosion inhibitors

- The demand for zinc chemicals is significantly driven by the expansion of the rubber and tire industry, increasing agricultural needs, and the growing focus on sustainable crop yield. Over half of the global demand is attributed to zinc oxide and zinc sulfate, which are heavily used in rubber processing and agricultural fertilizers, respectively

- The Asia Pacific region stands out as one of the dominant regions for zinc chemicals, led by robust industrial growth in China and India, coupled with increasing investments in infrastructure, manufacturing, and agriculture

- For instance, In 2023, EverZinc expanded its zinc oxide production capacity in Asia to meet the rising demand from the tire and fertilizer industries. Regional initiatives promoting sustainable agriculture and precision farming are also boosting the use of zinc-based micronutrients

- Globally, zinc oxide ranks as the most widely used zinc chemical, followed by zinc sulfate and zinc carbonate. These compounds play a pivotal role in driving performance, efficiency, and sustainability across multiple sectors, particularly in agriculture, rubber manufacturing, and personal care products

Report Scope and Zinc Chemicals Market Segmentation

|

Attributes |

Zinc Chemicals Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Zinc Chemicals Market Trends

“Rising Demand for Eco-Friendly and High-Purity Zinc Compounds”

- One prominent trend in the global zinc chemicals market is the increasing demand for eco-friendly and high-purity zinc compounds across multiple industries

- Driven by stricter environmental regulations and growing sustainability concerns, manufacturers are shifting toward cleaner production methods and environmentally safe formulations. This includes the use of low-impurity zinc oxides and sulfates that meet safety and regulatory standards for use in food, pharmaceutical, and cosmetic applications

- For instance, In 2023, Zochem launched a new line of high-purity zinc oxide products tailored for personal care and pharmaceutical applications, addressing the rising demand for safer and cleaner ingredients

- The push for sustainable agriculture is also contributing to this trend, with increased usage of zinc-based micronutrient fertilizers that improve soil health and crop yield without causing environmental harm

- This trend is reshaping the competitive landscape of the zinc chemicals market, as companies invest in innovation and cleaner technologies to meet end-user demands while aligning with global sustainability goals

Zinc Chemicals Market Dynamics

Driver

“Growing Demand Across Rubber, and Industrial Applications”

- The rising demand for zinc chemicals across key industries such as rubber manufacturing and chemicals is significantly contributing to the growth of the global zinc chemicals market

- Zinc oxide plays a vital role in the rubber industry as a vulcanization activator, enhancing the durability and elasticity of tires and industrial rubber products. The expansion of the automotive and construction sectors is fueling the demand for rubber products, thereby boosting the zinc chemicals market

- In zinc chemicals are crucial in various industrial processes, including ceramics, paints & coatings, pharmaceuticals, and cosmetics, where zinc compounds are valued for their anti-corrosive, antimicrobial, and UV-blocking properties

- As industrialization accelerates in emerging economies, and regulatory frameworks encourage the use of environmentally safe additives, the adoption of zinc chemicals is set to rise significantly

For instance,

- In March 2024, EverZinc announced a strategic expansion of its production facilities in Europe and Asia to meet rising demand from agriculture and tire manufacturers, citing a 15% year-over-year increase in zinc oxide consumption across these segments

- In October 2023 report by the International Fertilizer Association, the adoption of zinc-enriched fertilizers has grown by over 8% annually, driven by efforts to improve soil health and food security in countries like India and Brazil

- As a result of this widespread and growing use across diverse sectors, the demand for zinc chemicals continues to rise, positioning them as critical components in modern industrial and agricultural ecosystems

Opportunity

“Growing Scope for Zinc Chemicals in Sustainable Agriculture and Health Applications”

- The increasing emphasis on sustainable agriculture and health-centric applications presents significant growth opportunities for the global zinc chemicals market

- In agriculture, zinc sulfate and zinc oxide are widely used as micronutrient fertilizers to address zinc deficiencies in soil, which can severely impact crop yield and quality. With increasing global food demand and a focus on sustainable farming practices, the need for zinc-based agricultural solutions continues to grow

- Zinc-based fertilizers, particularly zinc sulfate and zinc oxide, are increasingly adopted to address widespread zinc deficiencies in soil, which can negatively impact crop yields. This growing agricultural need—especially in developing economies—is creating a robust market for zinc chemicals as part of precision farming and micronutrient management

- Moreover, zinc compounds such as zinc oxide and zinc gluconate are witnessing rising demand in personal care, pharmaceuticals, and food supplementation, owing to their antimicrobial, anti-inflammatory, and immune-boosting properties

For instance,

- In October 2023, the International Zinc Association reported a surge in the use of zinc in micronutrient fertilizers, especially in regions like South Asia and Sub-Saharan Africa, where over 50% of soils are zinc-deficient, creating urgent demand for zinc-enriched solutions.

- In February 2024, Zochem announced its plans to diversify its zinc oxide offerings to cater to pharmaceutical and nutraceutical applications, citing a 12% growth in demand for high-purity zinc oxide in health-related sectors

- As the world increasingly turns to sustainable solutions in agriculture and preventive healthcare, zinc chemicals are positioned to play a vital role in supporting both global food security and public health initiatives. This growing intersection between sustainability and wellness is opening new, high-value markets for zinc chemical manufacturers

Restraint/Challenge

“Volatility in Raw Material Prices and Environmental Regulations”

- The global zinc chemicals market faces a significant challenge due to the volatility in raw material prices, particularly zinc metal, which directly affects the production cost and pricing stability of zinc-based compounds

- Zinc prices are heavily influenced by global supply-demand dynamics, mining output fluctuations, and geopolitical uncertainties. This unpredictability can result in inconsistent profit margins for manufacturers and may hinder long-term planning and investments

- In addition, stringent environmental regulations surrounding mining operations and chemical manufacturing pose compliance challenges. Zinc chemical production, especially zinc oxide and zinc sulfate, can generate industrial emissions and by-products, requiring investments in eco-friendly technologies and waste treatment systems

For instance,

- In September 2023, the International Lead and Zinc Study Group (ILZSG) reported an increase in zinc price volatility due to reduced mining outputs in Latin America and ongoing disruptions in global supply chains, which led to a 9% spike in average zinc prices over three months

- In June 2024, EverZinc highlighted regulatory compliance as a key operational hurdle in its annual sustainability report, citing increasing costs due to stricter EU regulations related to emissions control and waste management during zinc oxide production

- These factors collectively present challenges in maintaining consistent product pricing, achieving profitability, and complying with evolving environmental standards. For many zinc chemical producers, navigating this complex landscape is essential to remain competitive and sustainable in the global market

Zinc Chemicals Market Scope

The market is segmented on the basis product type and application

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Application |

|

Zinc Chemicals Market Regional Analysis

“Asia-Pacific is the Dominant Region in the Zinc Chemicals Market”

- Asia-Pacific dominates the global zinc chemicals market, driven by rapid industrialization, increasing demand from emerging economies, and significant growth in sectors like construction, automotive, and agriculture

- China and India hold a significant share due to their large manufacturing bases and growing construction, automotive, and agricultural industries, which are key consumers of zinc chemicals for applications like galvanization and coatings

- The region benefits from a strong presence of key zinc chemical producers and an expanding supply chain, along with favorable government policies and infrastructure investments that boost production capacity

- Furthermore, the high demand for zinc-based fertilizers, as well as its use in electronics, paints, and coatings, is driving market growth in countries like China, Japan, and India, fueling the expansion of the zinc chemicals market across the region

“Asia-Pacific is Projected to Register the Highest Growth Rate”

- The Asia-Pacific region is expected to witness the highest growth rate in the global zinc chemicals market, driven by rapid industrialization, increasing demand for zinc in manufacturing processes, and growing applications in sectors such as automotive, construction, and agriculture.

- Countries such as China, India, and Japan are emerging as key markets due to their expanding industrial base, which is heavily reliant on zinc chemicals for galvanization, coatings, and agricultural applications.

- China, with its large manufacturing sector and a significant share of global zinc consumption, continues to lead in the use of zinc chemicals, particularly in galvanization and the production of zinc oxide for the rubber and chemical industries.

- India, with its growing industrial output and infrastructure development, is witnessing an increasing demand for zinc chemicals in construction materials, batteries, and fertilizers. The government's push for industrial growth and sustainability is also contributing to the rise in zinc chemical consumption.

- Japan, with its advanced technology and strong focus on sustainable production, remains a crucial market for zinc chemicals, especially in the automotive and electronics industries, where zinc is essential for corrosion resistance and as an additive in various electronic components

Zinc Chemicals Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Weifang Longda Zinc Industry Co., Ltd. (China)

- HAKUSUI TECH. (Japan)

- RUBAMIN (India)

- Zochem, Inc. (U.S.)

- Akrochem Corporation. (U.S.)

- L. Brüggemann GmbH & Co. KG (Germany)

- EverZinc. (Belgium)

- Pan-Continental Chemical Co., Ltd. (Taiwan)

- TIB Chemicals AG (Germany)

- Rech Chemical Co.Ltd (China)

- Purity Zinc Metals (U.S.)

- Old Bridge Chemicals, Inc. (U.S.)

- Boliden Group (Sweden)

- Nyrstar Clarksville (U.S.)

Latest Developments in Global Zinc Chemicals Market

- In September 2022, Boliden Group introduced a pioneering initiative to improve zinc recycling from electronic waste. Based in Sweden, this project underscores the company's commitment to sustainability by creating a more eco-friendly supply chain for zinc chemicals. By leveraging advanced recycling technologies, Boliden aims to reduce environmental impact while meeting the growing demand for sustainable zinc production. This initiative aligns with Boliden's broader mission to promote responsible resource management and support the transition to a circular economy

- In January 2023, Nyrstar, a prominent global zinc producer, announced a major expansion of its zinc oxide production capacity at the Clarksville facility. This strategic move was aimed at addressing the growing demand from key industries, including automotive, agriculture, and construction. By enhancing its production capabilities, Nyrstar reinforced its commitment to supporting diverse industrial needs while maintaining high-quality standards. This initiative reflects the company's dedication to innovation and meeting market demands effectively

- In March 2023, Rubamin, a prominent Indian producer of zinc chemicals, announced a substantial investment to enhance its zinc oxide production capacity. This expansion aims to cater to the increasing demand from both domestic and international markets, with a particular focus on the tire and paint industries. By boosting its production capabilities, Rubamin reinforces its commitment to meeting market needs while maintaining high-quality standards. This initiative reflects the company's dedication to innovation and supporting diverse industrial applications

- In August 2023, EverZinc, a Belgian company, finalized the acquisition of a significant zinc chemicals division from a leading industrial entity. This strategic move was aimed at bolstering EverZinc's market presence in the zinc oxide and chemicals sectors. The acquisition aligns with the company's focus on delivering sustainable and high-performance products, reinforcing its commitment to innovation and environmental responsibility. EverZinc's initiative highlights its dedication to advancing the zinc industry while meeting the evolving needs of global markets

- In February 2024, Akrochem Corporation unveiled a cutting-edge line of zinc-based advanced coatings. These innovative coatings are specifically designed to enhance corrosion resistance, catering to the automotive and industrial sectors. This launch addresses the increasing demand for durable and environmentally friendly materials, reflecting Akrochem's commitment to sustainability and high-performance solutions. By introducing these advanced coatings, the company reinforces its dedication to meeting industry needs while promoting eco-conscious practices

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Zinc Chemicals Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Zinc Chemicals Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Zinc Chemicals Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.