Middle East And Africa Brain Cancer Diagnostic Market

Market Size in USD Million

USD

95.95 Million

USD

334.63 Million

2024

2032

USD

95.95 Million

USD

334.63 Million

2024

2032

| 2025 - 2032 | |

| USD 95.95 Million | |

| USD 334.63 Million | |

| % | |

|

Middle East and Africa Brain Cancer Diagnostic Market Size

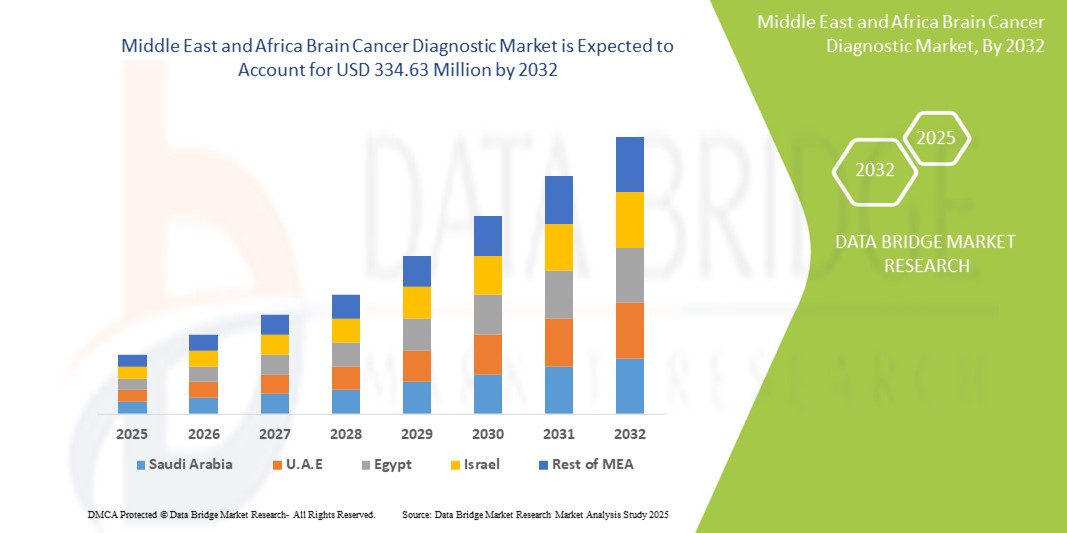

- The Middle East and Africa brain cancer diagnostic market size was valued at USD 95.95 Million in 2024 and is expected to reach USD 334.63 Million by 2032, at a CAGR of 16.90% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within advanced imaging techniques, liquid biopsies, and molecular diagnostics, leading to increased digitalization and precision in both hospital and research settings

- Furthermore, rising patient demand for accurate, minimally invasive, and integrated diagnostic solutions for early detection and monitoring is establishing brain cancer diagnostics as the modern standard of care. These converging factors are accelerating the uptake of Brain Cancer Diagnostic solutions, thereby significantly boosting the industry's growth

Middle East and Africa Brain Cancer Diagnostic Market Analysis

- The brain cancer diagnostic market is witnessing significant growth, driven by rising incidence rates of brain cancer, increasing awareness about early detection, and advancements in diagnostic technologies such as MRI, CT scans, liquid biopsies, and molecular diagnostics

- The escalating demand for accurate and non-invasive diagnostic methods is further supported by growing government healthcare initiatives, expansion of cancer screening programs, and higher investments in advanced imaging and biomarker-based diagnostics

- Saudi Arabia dominated the brain cancer diagnostic market in the Middle East & Africa with the largest revenue share of 36.8% in 2024, driven by its rapidly advancing healthcare infrastructure, government-backed cancer detection programs, and increasing availability of cutting-edge diagnostic imaging technologies across leading hospitals and cancer centers

- South Africa is projected to be the fastest-growing country in the brain cancer diagnostic market during the forecast period, supported by rising healthcare expenditure, expanding access to private and public healthcare facilities, and growing adoption of advanced diagnostic solutions to address the increasing cancer burden

- The 35–65 segment dominated the Middle East and Africa brain cancer diagnostic market revenue share of 46.1% in 2024, as brain cancers are more prevalent in this age group, making them the largest pool of diagnosed patients

Report Scope and Brain Cancer Diagnostic Market Segmentation

|

Attributes |

Brain Cancer Diagnostic Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Brain Cancer Diagnostic Market Trends

Advancements in Precision Diagnostics and Early Detection

- A significant and accelerating trend in the Middle East and Africa brain cancer diagnostic market is the growing adoption of precision diagnostics, including advanced imaging modalities, molecular profiling, and biomarker-based testing. These innovations are greatly enhancing diagnostic accuracy, enabling earlier detection of brain tumors, and improving patient management outcomes

- For instance, recent developments in liquid biopsy and next-generation sequencing (NGS) technologies have provided healthcare professionals in the region with more reliable, minimally invasive options for detecting genetic mutations and tumor biomarkers linked to brain cancers. This has led to more personalized treatment pathways and better prognosis for patients

- Advanced MRI and PET-CT systems are being increasingly deployed across hospitals and specialized cancer centers in countries such as Saudi Arabia, the UAE, and South Africa, offering high-resolution imaging and more precise evaluation of tumor progression and treatment response

- The rising availability of molecular diagnostic tests is further enabling clinicians to identify tumor subtypes, helping guide targeted therapy decisions. This is particularly important in improving survival rates and reducing recurrence by tailoring treatment strategies to individual patient needs

- The expansion of healthcare infrastructure, combined with government-backed initiatives to improve cancer screening programs in the Middle East and Africa, is facilitating broader access to diagnostic technologies. This, in turn, is reducing diagnostic delays and ensuring that more patients receive timely interventions

- Overall, the trend toward more advanced, personalized, and early diagnostic solutions is fundamentally reshaping the Brain Cancer Diagnostic market in the region. As a result, key global and regional players are increasingly investing in research collaborations and technology integration to strengthen their footprint in this rapidly evolving market

Middle East and Africa Brain Cancer Diagnostic Market Dynamics

Driver

Growing Need Due to Rising Prevalence and Early Detection Efforts

- The increasing prevalence of brain cancer cases across both developed and developing countries, coupled with the rising emphasis on early detection and diagnosis, is a significant driver of the Brain Cancer Diagnostic market. Timely identification of brain tumors is critical for improving survival rates, which has prompted healthcare systems to invest in more advanced diagnostic tools

- For instance, in April 2024, several healthcare providers in the Middle East and Africa expanded their cancer care facilities with advanced MRI and CT scanners, enabling earlier detection and improved monitoring of brain cancer patients. Such initiatives are expected to drive market growth in the forecast period

- As patients and clinicians become more aware of the importance of early diagnosis in improving treatment outcomes, there is a growing demand for innovative diagnostic solutions such as liquid biopsy, genetic profiling, and molecular imaging, which offer more accurate and less invasive alternatives compared to conventional approaches

- Furthermore, the expansion of cancer screening programs and the integration of precision diagnostics into standard care are making advanced solutions an essential component of healthcare systems. These efforts are particularly evident in urban hospitals and specialized oncology centers, where advanced tools are being deployed to streamline workflows and improve diagnostic accuracy

- The growing preference for non-invasive and patient-friendly diagnostic methods, combined with the rising healthcare expenditure and research funding, continues to propel the adoption of cutting-edge technologies in both developed and emerging economies

Restraint/Challenge

Concerns Regarding High Costs and Limited Accessibility

- Despite the growing demand, the high cost of advanced brain cancer diagnostic systems remains a significant barrier to widespread adoption. MRI, PET-CT, and next-generation sequencing tests are often associated with substantial expenses, making them less accessible to patients in lower-income regions. This cost factor can delay timely diagnosis and treatment initiation

- In addition, disparities in healthcare infrastructure, particularly in rural and underserved areas, limit access to advanced diagnostic tools. While major hospitals and urban cancer centers are adopting these technologies, smaller clinics and healthcare facilities often lack the resources to implement them

- Another challenge lies in the shortage of skilled professionals trained to operate advanced imaging and molecular diagnostic systems. Without sufficient expertise, diagnostic accuracy may be compromised, further affecting patient outcomes

- Although government and private initiatives are gradually addressing these issues by expanding reimbursement policies and funding cancer programs, financial constraints and uneven distribution of resources still hinder broader adoption

- Overcoming these challenges through increased healthcare investments, training programs for medical professionals, and the development of cost-effective diagnostic technologies will be essential to ensure equitable access and sustain long-term market growth

Middle East and Africa Brain Cancer Diagnostic Market Scope

The market is segmented on the basis of test type, cancer type, age group, and end user

- By Test Type

On the basis of test type, the brain cancer diagnostic market is segmented into imaging test, biopsy, lumbar puncture, molecular testing, electroencephalography, and others. The imaging test segment dominated the market revenue share of 42.8% in 2024, owing to its widespread use as the first-line diagnostic approach for brain cancer. MRI and CT scans are routinely employed in hospitals and diagnostic centers across the Middle East and Africa, providing precise structural information and enabling early detection of tumors. Accessibility of imaging devices through government hospitals and private diagnostic centers ensures broad usage, while advancements in imaging resolution continue to improve diagnostic accuracy. The segment also benefits from insurance coverage, well-trained radiologists, and integration with digital health systems. Routine monitoring of patients undergoing treatment further strengthens demand. Partnerships between hospitals and imaging service providers also expand utilization across urban and semi-urban regions.

The molecular testing segment is expected to witness the fastest growth with a CAGR of 7.6% from 2025 to 2032, driven by the increasing adoption of precision medicine and biomarker-based diagnostics. Molecular testing allows identification of genetic mutations, tumor markers, and treatment-specific pathways, making it vital for personalized therapy. Rising clinical research initiatives in the region are boosting awareness of genomic testing for brain cancers. Hospitals and research institutes are investing in molecular diagnostic platforms to improve patient outcomes. Growing collaborations with global diagnostic companies are making these technologies more accessible. Improved affordability, coupled with a rising emphasis on early detection, supports expansion. Educational programs for physicians on the benefits of molecular testing are further encouraging adoption. The segment is expected to transform the diagnostic landscape, aligning with global advancements in oncology care.

- By Cancer Type

On the basis of cancer type, the brain cancer diagnostic market is segmented into acoustic neuroma, astrocytomas, glioblastoma multiforme, meningiomas, oligodendroglioma, and others. The glioblastoma multiforme segment dominated the market in 2024 with a 38.5% revenue share, due to its aggressive nature and high prevalence compared to other brain cancers. Patients with glioblastoma typically require multiple diagnostic procedures, including imaging, biopsy, and molecular profiling, driving sustained demand. Hospitals and specialty clinics prioritize early and accurate diagnosis for glioblastoma given its poor prognosis. The complexity of the disease necessitates advanced diagnostics, which strengthens reliance on both imaging and molecular testing solutions. Government cancer registries and awareness initiatives often emphasize glioblastoma, further reinforcing market leadership. Continuous research studies and clinical trials focusing on this cancer type expand diagnostic applications. Urban centers report higher diagnosis rates, boosting utilization of advanced diagnostic services.

The astrocytomas segment is expected to witness the fastest growth with a CAGR of 6.9% from 2025 to 2032, supported by increasing recognition of low- and high-grade variants. Astrocytomas often present in younger populations, leading to rising diagnosis in both pediatric and adult cases. Improved awareness among healthcare professionals regarding the disease spectrum is driving early detection. Diagnostic advancements such as MRI spectroscopy and biopsy refinement are expanding adoption. Hospitals and diagnostic centers are enhancing infrastructure to accommodate specialized testing for astrocytomas. Patient advocacy groups and educational campaigns are also raising visibility of this cancer type. Insurance coverage is broadening for advanced diagnostic tests associated with astrocytomas. Ongoing clinical research further strengthens the case for timely and precise diagnosis, fueling robust growth.

- By Age Group

On the basis of age group, the brain cancer diagnostic market is segmented into below 21, 21–34, 35–65, and 65 and above. The 35–65 segment dominated the market revenue share of 46.1% in 2024, as brain cancers are more prevalent in this age group, making them the largest pool of diagnosed patients. Hospitals and specialty clinics frequently report higher diagnostic demand among this group, supported by higher healthcare-seeking behavior and regular checkups. Imaging and biopsy procedures are commonly performed for suspected cases, with insurance coverage often extending to this age range. Urban centers particularly see greater adoption of advanced diagnostic technologies among middle-aged patients. Pharmaceutical trials and diagnostic innovations also prioritize this demographic. Patient compliance with regular monitoring further reinforces demand. Employers and government health programs contribute to early detection efforts.

The below 21 segment is expected to witness the fastest growth with a CAGR of 7.2% from 2025 to 2032, fueled by increasing recognition of pediatric brain tumors and the need for early intervention. Pediatric cases are receiving growing attention from both hospitals and research institutes in the Middle East and Africa. Diagnostic centers are introducing specialized pediatric imaging protocols and minimally invasive testing approaches. Awareness campaigns targeting parents and caregivers are improving early detection rates. Pediatric oncologists are expanding their diagnostic capabilities with molecular and genetic testing. Insurance policies are increasingly covering pediatric diagnostic services, enhancing access. Clinical trials targeting childhood brain cancers are also increasing, encouraging uptake of advanced diagnostic methods. The growing demand for child-friendly diagnostic solutions supports rapid segment growth.

- By End User

On the basis of end user, the brain cancer diagnostic market is segmented into hospitals, specialty clinics, diagnostic centers & research institutes, ambulatory surgical centers, and others. The hospitals segment dominated the market with a 52.4% revenue share in 2024, due to the availability of comprehensive diagnostic infrastructure and high patient inflow. Hospitals serve as primary points for both initial diagnosis and advanced testing procedures, including imaging, biopsy, and molecular diagnostics. Government hospitals across the Middle East and Africa provide subsidized or free diagnostic services, ensuring high accessibility. Private hospitals complement with advanced equipment and specialized staff, offering premium services. The integration of diagnostic and treatment pathways within hospital systems drives efficiency and patient compliance. Hospitals also engage in collaborative clinical research, further reinforcing their leadership position. Urban and semi-urban hospital networks ensure widespread coverage.

The specialty clinics segment is expected to witness the fastest growth with a CAGR of 6.7% from 2025 to 2032, as the number of neurology- and oncology-focused clinics expands across the region. Specialty clinics provide quicker access to targeted diagnostic services, offering personalized care and faster turnaround times. Patients increasingly prefer specialty clinics for convenience and specialized expertise. The adoption of advanced imaging, biopsy, and molecular testing is particularly strong in these settings. Investment from private healthcare providers is boosting infrastructure in urban areas. Partnerships with hospitals and research institutions further enhance diagnostic offerings. Awareness campaigns are encouraging patients to seek early consultation at specialty clinics. Insurance coverage for diagnostic procedures in such facilities is improving, supporting wider adoption. This growing ecosystem positions specialty clinics as a high-growth segment.

Middle East and Africa Brain Cancer Diagnostic Market Regional Analysis

- The Middle East & Africa brain cancer diagnostic market is experiencing steady growth, supported by a combination of rising cancer prevalence, significant improvements in healthcare infrastructure, and proactive government-led initiatives that prioritize early detection and advanced treatment

- The availability of sophisticated imaging technologies, coupled with increasing collaborations with international diagnostic companies, has enabled hospitals and cancer centers in the region to expand their diagnostic capabilities

- Moreover, heightened awareness regarding the importance of early cancer detection and the growing number of trained oncologists and radiologists are further contributing to the expansion of the market across both developed and developing nations within the region

Saudi Arabia Brain Cancer Diagnostic Market Insight

The Saudi Arabia brain cancer diagnostic market accounted for the largest share of the Middle East & Africa brain cancer diagnostic market, securing 36.8% of the regional revenue. The country’s dominance is largely driven by its rapidly advancing healthcare infrastructure and sustained government investment under the Vision 2030 initiative, which has prioritized oncology services as a critical area of development. Leading hospitals and specialized cancer centers in Riyadh, Jeddah, and Dammam are equipped with cutting-edge diagnostic modalities, including MRI, CT, PET-CT, and molecular testing platforms, which are widely utilized for accurate detection and monitoring of brain tumors. National screening programs and awareness campaigns have also played a pivotal role in encouraging early diagnosis, improving survival rates, and reducing the overall disease burden. Furthermore, Saudi Arabia has been expanding its adoption of precision diagnostics, with an increasing emphasis on molecular and genetic profiling to support personalized medicine. This continuous focus on advanced technologies and government-backed strategies has firmly positioned the country as the regional hub for cancer diagnostics.

South Africa Brain Cancer Diagnostic Market Insight

The South Africa brain cancer diagnostic market, on the other hand, is projected to be the fastest-growing market for brain cancer diagnostics in the Middle East & Africa during the forecast period. This growth trajectory is underpinned by rising healthcare expenditure, greater investments in oncology services, and the government’s ongoing efforts to expand access to advanced diagnostic solutions across both public and private healthcare sectors. The country has been actively addressing disparities in cancer care by establishing new diagnostic laboratories and strengthening collaborations with global diagnostic providers, thereby improving accessibility to technologies such as molecular imaging, next-generation sequencing (NGS), and liquid biopsy. These innovations are enabling earlier and more precise identification of brain tumors, which is essential in managing the growing cancer burden in the country. South Africa’s commitment to upgrading its healthcare infrastructure and the rising demand for advanced diagnostic solutions have created a dynamic environment for market growth, positioning the country as an emerging leader in brain cancer diagnostics within the region.

Middle East and Africa Brain Cancer Diagnostic Market Share

The brain cancer diagnostic industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- NIHON KOHDEN CORPORATION (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Neusoft Corporation (China)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- BD (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Canon Medical Systems (Japan)

- Hitachi, Ltd. (Japan)

- Biocept, Inc. (U.S.)

- MinFound Medical Systems Co. (China)

Latest Developments in Middle East and Africa Brain Cancer Diagnostic Market

- In June 2021, the AED 700 million Neuro Spinal Hospital and Radiosurgery Centre opened in Dubai Science Park, featuring 114 beds and advanced technologies such as CyberKnife radiosurgery, AI-powered diagnostic solutions, and smart patient care systems. This launch marked a significant milestone in enhancing access to world-class neurosurgical and oncology care in the UAE

- In February 2023, GE HealthCare advanced its imaging portfolio in the region with the availability of the SIGNA PET/MR AIR system, which integrates high-resolution MRI with time-of-flight PET technology. The system enhances neuroimaging precision for detecting and managing brain tumors, enabling clinicians to perform detailed, simultaneous molecular and anatomical assessments

- In January 2024, Siemens Healthineers showcased its latest diagnostic and imaging innovations at Arab Health 2024 in Dubai, highlighting AI-augmented MRI and CT solutions designed to accelerate neuro-oncology workflows. These technologies were introduced to support earlier detection and better treatment planning for brain cancers, reinforcing the company’s commitment to advancing cancer diagnostics in the MEA region

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.