Middle East And Africa Dengue Treatment Market

Market Size in USD Million

USD

22.84 Million

USD

125.21 Million

2024

2032

USD

22.84 Million

USD

125.21 Million

2024

2032

| 2025 - 2032 | |

| USD 22.84 Million | |

| USD 125.21 Million | |

| % | |

|

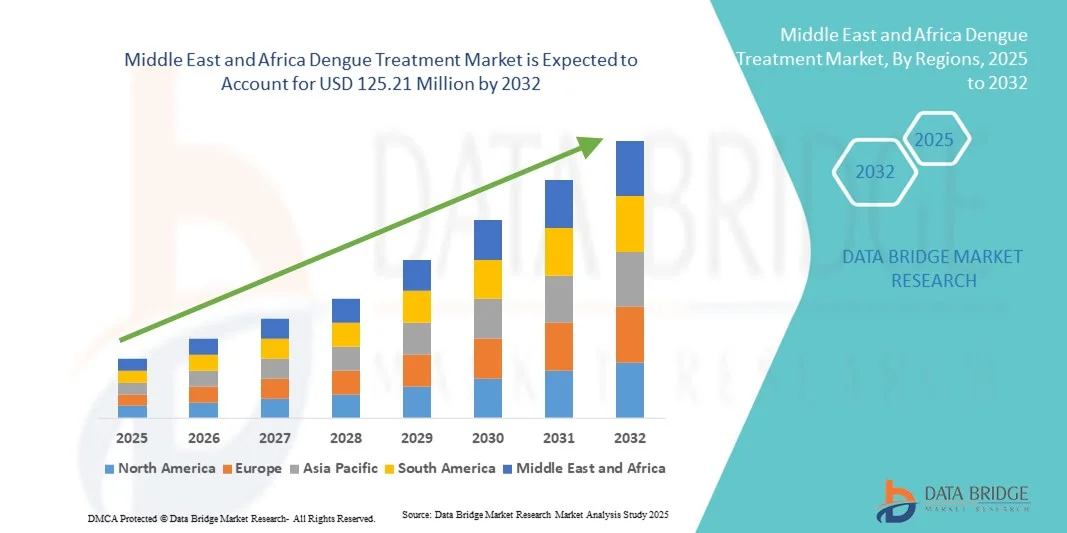

Middle East and Africa Dengue Treatment Market Size

- The Middle East and Africa dengue treatment market size was valued at USD 22.84 million in 2024 and is expected to reach USD 125.21 million by 2032, at a CAGR of 23.7% during the forecast period

- The market growth is largely fueled by the rising prevalence of dengue fever across tropical and subtropical regions, increasing the demand for effective and accessible treatment options

- Furthermore, growing government initiatives, research in antiviral therapies, and heightened public awareness are accelerating the uptake of dengue treatment solutions, thereby significantly boosting the industry's growth

Middle East and Africa Dengue Treatment Market Analysis

- The Middle East & Africa Dengue Treatment market is witnessing significant growth, driven by rising incidence of dengue fever, increasing healthcare awareness, and government initiatives aimed at improving access to effective treatment solutions

- The market growth is primarily fueled by rising public health investments, expanding healthcare infrastructure, and increasing adoption of antiviral therapies, supportive care measures, and vaccination programs across the region

- Saudi Arabia dominated the Middle East and Africa dengue treatment market with the largest revenue share of 38.5% in 2024, characterized by a high prevalence of dengue cases, strong healthcare initiatives, and well-established medical facilities, with hospitals and specialty clinics witnessing increasing demand for dengue treatment solutions

- The United Arab Emirates (UAE) is expected to be the fastest-growing country in the Middle East & Africa dengue treatment market during the forecast period due to increasing urbanization, rising healthcare access, proactive government programs, and growing investment in dengue prevention and treatment initiatives

- The Mosquito-to-Human Transmission segment dominated the Middle East and Africa dengue treatment market with the largest revenue share of 87% in 2024, as it represents the primary route of infection in endemic regions

Report Scope and Dengue Treatment Market Segmentation

|

Attributes |

Dengue Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Dengue Treatment Market Trends

Enhanced Convenience Through Advanced Therapeutics and Digital Health Integration

- A significant and accelerating trend in the Middle East and Africa dengue treatment market is the deepening integration of advanced therapeutics with digital health solutions, including patient monitoring apps, telemedicine platforms, and AI-assisted treatment guidance. This integration is enhancing patient convenience, adherence, and overall disease management

- For instance, several regional hospitals are implementing telemedicine-enabled dengue treatment programs, allowing patients to receive timely consultations, monitor symptoms remotely, and adjust medication schedules without frequent hospital visits. Similarly, some specialty clinics are leveraging AI-based systems to predict disease progression and optimize supportive care regimens

- AI integration in dengue treatment enables predictive monitoring of patient symptoms, potentially suggesting dosage adjustments or alerting physicians to early warning signs of severe dengue. For instance, certain digital platforms analyze patient vitals and historical data to provide intelligent alerts for potential complications. Furthermore, mobile-based platforms offer patients the ease of accessing treatment guidelines, appointment reminders, and medication tracking from home

- The seamless integration of dengue treatment with telemedicine and mobile health platforms facilitates centralized management of patient care. Through a single interface, physicians can monitor patient recovery, provide treatment recommendations, and adjust care plans, creating a more connected and efficient healthcare experience

- This trend toward more intelligent, patient-centric, and digitally integrated dengue treatment solutions is fundamentally reshaping expectations for disease management. Consequently, healthcare providers and pharmaceutical companies are increasingly developing AI-assisted therapies, digital care platforms, and remote monitoring tools tailored for dengue patients

- The demand for Dengue Treatment options that offer remote monitoring, digital health integration, and advanced therapeutics is growing rapidly across both hospitals and specialty clinics, as patients and providers increasingly prioritize convenience, timely intervention, and comprehensive care

Middle East and Africa Dengue Treatment Market Dynamics

Driver

Growing Need Due to Rising Dengue Incidence and Healthcare Awareness

- The increasing prevalence of dengue in the Middle East and Africa, coupled with rising awareness among healthcare providers and patients, is a significant driver for the heightened demand for effective Dengue Treatment solutions

- For instance, in April 2024, regional healthcare systems expanded outpatient programs and telemedicine platforms to support early diagnosis, patient monitoring, and adherence to treatment protocols. Such initiatives by healthcare providers are expected to drive Dengue Treatment market growth during the forecast period

- As patients and physicians become more aware of the risks associated with dengue and the benefits of timely intervention, hospitals and specialty clinics are adopting advanced antiviral medications, supportive care solutions, and AI-assisted monitoring platforms to improve patient outcomes

- Furthermore, government health programs and NGO initiatives promoting dengue awareness, vector control, and early treatment are making Dengue Treatment a critical component of regional healthcare strategies

- The convenience of telemedicine-enabled consultations, home-based care programs, and mobile health tracking applications are key factors propelling the adoption of Dengue Treatment across both urban and semi-urban populations. The trend toward digital health integration and increasing availability of patient-friendly treatment solutions further contributes to market growth

Restraint/Challenge

Concerns Regarding Treatment Accessibility and Cost

- Limited access to healthcare facilities and the relatively high cost of advanced dengue treatment options in certain regions pose challenges to broader market adoption. patients in rural or underserved areas may face difficulties in obtaining timely medications or accessing digital health solutions

- Addressing these accessibility challenges through government health programs, affordable medication initiatives, and telemedicine platforms is crucial for expanding market reach

- In addition, awareness gaps regarding dengue symptoms, treatment protocols, and preventive measures may hinder early intervention. Healthcare providers are investing in patient education campaigns, community outreach, and digital awareness platforms to mitigate this barrier

- While prices for standard dengue medications and supportive care solutions are gradually decreasing, advanced therapeutics and AI-assisted monitoring tools still carry higher costs, which can limit adoption in price-sensitive populations

- Overcoming these challenges through enhanced patient education, improved healthcare accessibility, cost-effective treatment programs, and digital health integration will be vital for sustained growth in the Middle East and Africa dengue treatment market

Middle East and Africa Dengue Treatment Market Scope

The market is segmented on the basis of strains, transmission, type, severity, route of administration, mode of purchase, end user, and distribution channel.

- By Strains

On the basis of strains, the dengue treatment market is segmented into DENV-1, DENV-2, DENV-3, DENV-4, and Others. The DENV-2 segment dominated the market with the largest revenue share of 36.8% in 2024, driven by its high prevalence in countries like Saudi Arabia, U.A.E and South Africa. Hospitals and clinics prioritize DENV-2 due to its association with moderate to severe dengue cases. The segment benefits from government health programs promoting early diagnosis and treatment. Clinical guidelines and standardized treatment protocols strengthen hospital adoption. Outpatient and hospital care integration ensures timely therapy administration. R&D programs targeting DENV-2 therapies are active in the region. Urban and semi-urban areas show higher treatment adoption rates. Continuous patient monitoring improves outcomes. Public awareness campaigns emphasize early intervention. Physician training programs reinforce best practices. Hospitals and specialty clinics ensure continuous medication supply and adherence. Government and private collaborations support clinical trials and research.

The DENV-3 segment is expected to witness the fastest CAGR of 8.5% from 2025 to 2032, driven by rising outbreaks in and increasing awareness of its clinical complications. Hospitals and specialty clinics are prioritizing DENV-3 due to its link with moderate to severe cases. Ongoing research and development of DENV-3-targeted vaccines and supportive therapies is fueling adoption. Public health initiatives are promoting preventive measures and early treatment. Expansion of diagnostic facilities allows for early detection. Physicians emphasize tailored treatment protocols for DENV-3 infections. Hospitals are ensuring better monitoring for complications. Government programs provide targeted support in outbreak-prone regions. Patient access is increasing in both urban and semi-urban areas. Integration with public health programs strengthens adoption. Clinical guidelines are being updated based on DENV-3 case trends. Community awareness campaigns drive timely hospital and clinic visits. Pharmaceutical R&D continues to improve treatment efficacy and safety.

- By Transmission

On the basis of transmission, the dengue treatment market is segmented into mosquito-to-human transmission and mother-to-child transmission. The Mosquito-to-Human Transmission segment dominated the market with the largest revenue share of 87% in 2024, as it represents the primary route of infection in endemic regions. Vector control programs and community awareness campaigns support hospitals and clinics in managing patient load. Early diagnosis and timely treatment in hospitals ensure better patient outcomes. Standardized clinical guidelines strengthen adoption. Urban and semi-urban populations exhibit higher incidence, driving treatment demand. Hospitals integrate supportive care and parenteral therapies. Physicians emphasize patient monitoring and follow-up. Government health programs and public campaigns reinforce preventive measures. Continuous availability of medications ensures uninterrupted treatment. Specialty clinics support hospital initiatives with outpatient care. Clinical research and case tracking enhance treatment protocols. Hospitals and clinics collaborate to optimize therapy management.

The Mother-to-Child Transmission segment is expected to register the fastest CAGR of 9.2% from 2025 to 2032, fueled by rising awareness of neonatal dengue risks and improvements in maternal healthcare facilities. Prenatal screening programs in hospitals are expanding. Specialty clinics provide follow-up care for newborns at risk. Preventive measures during pregnancy are increasingly adopted. Awareness campaigns educate healthcare providers and patients. Government initiatives target reduction of vertical transmission. Hospitals implement strict neonatal care protocols. Supportive medications and parenteral therapy aid rapid intervention. Physicians provide counseling for expectant mothers in endemic regions. Clinics integrate dengue care with maternal health programs. Early diagnosis and monitoring improve neonatal outcomes. Expansion of outpatient maternal care enhances accessibility. Continuous research and reporting inform clinical guidelines and public health strategy.

- By Type

On the basis of type, the dengue treatment market is segmented into medication, supportive care, vaccination, and others. The Medication segment dominated the market with a revenue share of 54.6% in 2024, driven by the widespread use of antivirals and adjunct therapies. Hospitals and clinics adopt standardized medication protocols. Outpatient care ensures timely administration. Government health programs promote access to medications. Urban and semi-urban adoption is high due to improved healthcare infrastructure. Physician adherence to clinical guidelines strengthens hospital adoption. Continuous R&D improves drug efficacy and safety. Clinical trials support introduction of new therapies. Patient monitoring and follow-up ensure effective outcomes. Insurance programs support medication costs. Public awareness campaigns promote early treatment. Hospitals and specialty clinics ensure consistent medication supply. Integration with supportive care and vaccination programs enhances patient recovery.

The Vaccination segment is expected to witness the fastest CAGR of 12.4% from 2025 to 2032, driven by government immunization programs, multi-serotype next-generation vaccines, and rising community awareness of dengue prevention. Hospitals and clinics prioritize vaccination in endemic regions. Public health campaigns educate communities on vaccine benefits. Expansion of vaccination centers increases accessibility in urban and semi-urban areas. Physicians recommend vaccines for high-risk populations. R&D investment improves efficacy and safety. Government subsidies and insurance programs support vaccine adoption. Awareness of outbreak prevention encourages uptake. Integration of vaccination programs with routine healthcare strengthens coverage. Follow-up and booster doses ensure long-term immunity. Distribution through hospital and retail pharmacies increases reach. Vaccination adoption complements supportive care and medication protocols. Monitoring of vaccine impact informs policy and clinical guidelines.

- By Severity

On the basis of severity, the dengue treatment market is segmented into uncomplicated and severe. The Uncomplicated segment dominated the market with a revenue share of 68% in 2024, as it accounts for the majority of dengue cases. Outpatient management and supportive care are widely adopted. Hospitals and clinics ensure adherence to standardized treatment protocols. Early diagnosis and timely intervention improve patient outcomes. Government health programs promote access to medications. Urban and semi-urban areas show higher adoption rates. Physicians monitor patient recovery and provide follow-up care. Community awareness campaigns support timely hospital visits. Insurance coverage enhances treatment affordability. Clinical guidelines reinforce proper management. Hospital pharmacies ensure medication availability. Integration with other healthcare services strengthens adherence. Hospitals and specialty clinics collaborate for effective management.

The Severe segment is expected to register the fastest CAGR of 10.1% from 2025 to 2032, driven by increasing incidence of dengue hemorrhagic fever and dengue shock syndrome. Hospitals are expanding critical care infrastructure to manage severe cases. Intensive monitoring and combination therapies are increasingly adopted. Physicians emphasize early diagnosis and rapid intervention. Specialty clinics support hospital care through outpatient follow-up. Government health programs provide targeted resources for high-risk patients. Parenteral therapy and advanced supportive care are widely implemented. Standardized hospital protocols ensure consistent treatment. Awareness campaigns encourage timely hospital visits. Expansion of tertiary care facilities improves accessibility. R&D focuses on optimizing treatments for severe dengue. Data collection informs clinical guidelines and policy. Hospitals and clinics collaborate to improve survival rates.

- By Route of Administration

On the basis of route of administration, the dengue treatment market is segmented into oral and parenteral. The Oral segment dominated the market with a revenue share of 62% in 2024, due to widespread use for fever reduction, platelet management, and supportive care. Outpatient treatment ensures compliance. Hospitals and clinics follow standardized guidelines. Government programs promote accessibility. Urban and semi-urban adoption is high. Easy administration supports patient adherence. Insurance coverage enhances affordability. Continuous medication supply ensures uninterrupted therapy. Physicians monitor patient progress and provide counseling. Integration with hospital and specialty clinic services improves outcomes. Clinical protocols guide safe administration. Public awareness campaigns encourage timely treatment. Hospitals and clinics optimize oral therapy for uncomplicated cases.

The Parenteral segment is expected to witness the fastest CAGR of 11.5% from 2025 to 2032, fueled by increasing hospitalizations for severe dengue, expansion of intensive care infrastructure, and adoption of intravenous fluid therapy and injectable antivirals. Hospitals equip critical care units with parenteral capabilities. Physicians emphasize rapid administration to reduce complications. Specialty clinics coordinate outpatient IV therapies. Supportive medications ensure timely intervention for high-risk patients. Government programs provide infrastructure support. Continuous R&D improves safety and efficacy. Tertiary care expansion enhances accessibility. Patient adherence and monitoring improve outcomes. Hospital pharmacies ensure medication supply. Integration with diagnostics enables immediate therapy. Insurance coverage supports inpatient and parenteral care. Clinical guidelines and monitoring strengthen adoption.

- By Mode of Purchase

On the basis of mode of purchase, the dengue treatment market is segmented into prescription and over the counter (OTC). The Prescription segment dominated the market with a revenue share of 77% in 2024, as physician-supervised treatment is essential for safe dengue management. Hospitals and clinics dispense medications directly. Regulatory adherence ensures standardized protocols. Insurance coverage supports affordability. Physician monitoring and follow-up strengthen outcomes. Outpatient and inpatient access improve adherence. Government programs and public health initiatives reinforce prescription use. Urban and semi-urban adoption is high. Standardized dosing reduces complications. Hospital pharmacies provide reliable supply. Specialty clinics support prescription-based care. Clinical guidelines reinforce proper administration. Physician education enhances patient compliance.

The OTC segment is expected to register the fastest CAGR of 9.8% from 2025 to 2032, driven by growing home-based care for uncomplicated dengue, availability of supportive medications without prescription, and expansion of retail and online pharmacy networks. Patients increasingly prefer OTC options for convenience and quick symptom management. Retail pharmacies promote accessibility and awareness. Online platforms enable home delivery and adherence tracking. Public education campaigns inform safe OTC use. Urban and semi-urban populations benefit from increased access. Physician guidance ensures proper self-management. Integration with supportive care enhances outcomes. Digital tools monitor compliance. OTC adoption reduces hospital load. Community health initiatives encourage responsible use. Specialty clinics integrate OTC care with outpatient management. Growing confidence in self-managed treatment supports expansion.

- By End User

On the basis of end user, the dengue treatment market is segmented into hospitals, specialty clinics, home healthcare, and others. The Hospitals segment dominated the market with a revenue share of 58% in 2024, due to comprehensive care for dengue patients including medications, supportive care, and parenteral therapy. Critical care units, physician expertise, and standardized protocols support effective management. Government health programs and insurance schemes improve accessibility. Urban and semi-urban adoption is high. Integration with diagnostics ensures early intervention. Hospitals monitor patient adherence and follow-up. Specialty clinics complement hospital care through outpatient services. Research and clinical trials support new therapies. Hospital pharmacies ensure continuous supply. Public awareness campaigns drive timely hospital visits. Tertiary care infrastructure strengthens treatment outcomes. Clinical guidelines reinforce standardized management.

The Specialty Clinics segment is expected to witness the fastest CAGR of 7.5% from 2025 to 2032, fueled by expansion of outpatient services, increased awareness among physicians and patients, and adoption of home-based care programs. Clinics provide oral therapy, monitoring, and follow-up for patients transitioning from hospital care. Urban and semi-urban accessibility improves treatment reach. Physicians integrate dengue care with other outpatient services. Preventive care and patient education reduce disease progression. Collaboration with hospitals ensures continuity of care. Telemedicine and digital monitoring support adherence. Community awareness campaigns drive clinic visits. Clinics stock both prescription and supportive medications. Staff training improves quality of care. Government health program integration ensures coverage. Expansion of specialty clinic networks strengthens market penetration. Clinics play a growing role in managing uncomplicated and moderate dengue cases.

- By Distribution Channel

On the basis of distribution channel, the dengue treatment market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and others. The hospital pharmacies segment dominated the market with a revenue share of 49% in 2024, as it ensures direct access to prescription medications, parenteral therapies, and vaccination programs. Hospitals integrate pharmacies into treatment protocols. Physician-dispensed medications reinforce adoption. Quality control and proper storage ensure efficacy. Government partnerships support subsidized therapies. Uninterrupted medication supply is maintained. Patient counseling and follow-up improve adherence. Urban and semi-urban adoption is high. Integration with diagnostic and clinical services strengthens treatment outcomes. Insurance programs support accessibility. Specialty clinics complement hospital pharmacy services. R&D and clinical trials drive adoption. Public health campaigns reinforce utilization. Continuous supply chains ensure reliable distribution.

The Online Pharmacies segment is expected to register the fastest CAGR of 9.1% from 2025 to 2032, fueled by e-commerce adoption, patient preference for home delivery, digital adherence programs, and wider accessibility in urban and semi-urban regions. Online platforms ensure convenient refills and discreet delivery. Patients on long-term therapy benefit from home delivery and monitoring. Retail and hospital pharmacy collaborations enhance availability. Telemedicine integration improves adherence. Internet penetration drives market growth. Extensive medication variety supports both prescription and OTC needs. Digital tools monitor patient compliance. Urban and semi-urban expansion increases accessibility. Awareness campaigns encourage adoption. Insurance and payment support enhance affordability. Home delivery reduces travel and exposure risk. E-commerce competition promotes wider availability.

Middle East and Africa Dengue Treatment Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa dengue treatment market with the largest revenue share of 38.5% in 2024, characterized by a high prevalence of dengue cases, strong healthcare initiatives, and well-established medical facilities, with hospitals and specialty clinics witnessing increasing demand for dengue treatment solutions

- The United Arab Emirates (UAE) is expected to be the fastest-growing country in the Middle East & Africa dengue treatment market during the forecast period due to increasing urbanization, rising healthcare access, proactive government programs, and growing investment in dengue prevention and treatment initiatives

- Increasing urbanization, better healthcare infrastructure, and greater adoption of antiviral therapies and supportive care programs are further supporting market growth across the region

Saudi Arabia Dengue Treatment Market Insight

The Saudi Arabia dengue treatment market dominated the dengue treatment market in the Middle East & Africa region with the largest revenue share of 38.5% in 2024, characterized by a high prevalence of dengue cases, strong healthcare initiatives, and well-established medical facilities. Hospitals and specialty clinics across the country are witnessing increasing demand for dengue treatment solutions, supported by government efforts to strengthen disease surveillance and public health programs.

United Arab Emirates (UAE) Dengue Treatment Market Insight

The United Arab Emirates (UAE) dengue treatment market is expected to be the fastest-growing country in the Middle East & Africa Dengue Treatment market during the forecast period. This growth is fueled by increasing urbanization, rising healthcare access, proactive government programs, and growing investment in dengue prevention and treatment initiatives. The country’s focus on public health awareness and early diagnosis is further encouraging the adoption of effective dengue treatment solutions in both residential and commercial healthcare settings.

Middle East and Africa Dengue Treatment Market Share

The Dengue Treatment industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company Limited (Japan)

- Sanofi S.A. (France)

- Cipla Ltd. (India)

- Biological E. Limited (India)

- Oxitec Ltd. (U.K.)

- BioNet-Asia (Thailand)

- Panacea Biotec (India)

- EMERGENT (U.S.)

- GeneOne Life Science (South Korea)

- VBI Vaccines Inc. (U.S.)

- SINOVAC (China)

Latest Developments in Middle East and Africa Dengue Treatment Market

- In May 2024, Takeda Pharmaceuticals received prequalification from the World Health Organization (WHO) for its dengue vaccine, Qdenga (TAK-003). This live-attenuated vaccine, effective against all four dengue virus serotypes, is administered in two doses over a three-month interval. The prequalification allows international procurement agencies like UNICEF and the Pan American Health Organization to purchase the vaccine, facilitating its distribution in high-risk areas

- In February 2024, Takeda announced a partnership with India's Biological E to scale up production of Qdenga. The collaboration aims to produce up to 50 million doses annually, contributing to Takeda's goal of 100 million doses per year by 2030. This initiative is part of Takeda's efforts to address the growing demand for dengue vaccines in endemic regions

- In August 2025, the European Centre for Disease Prevention and Control (ECDC) reported over 4 million dengue cases and over 2,500 dengue-related deaths from 101 countries/territories since the beginning of 2025. This surge underscores the global re-emergence of dengue fever and the urgent need for effective prevention and treatment strategies

- In August 2025, Takeda announced plans to conduct global clinical trials in India to accelerate the introduction of its innovative drugs, including the dengue vaccine developed in collaboration with Biological E. The move is part of Takeda's strategy to integrate India's clinical trial ecosystem into its global pipeline, aiming to increase access to advanced treatments in the country

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.