Middle East And Africa Dish Antennas Market

Market Size in USD Billion

USD

0.80 Billion

USD

1.33 Billion

2024

2032

USD

0.80 Billion

USD

1.33 Billion

2024

2032

| 2025 - 2032 | |

| USD 0.80 Billion | |

| USD 1.33 Billion | |

| % | |

|

Dish Antennas Market Size

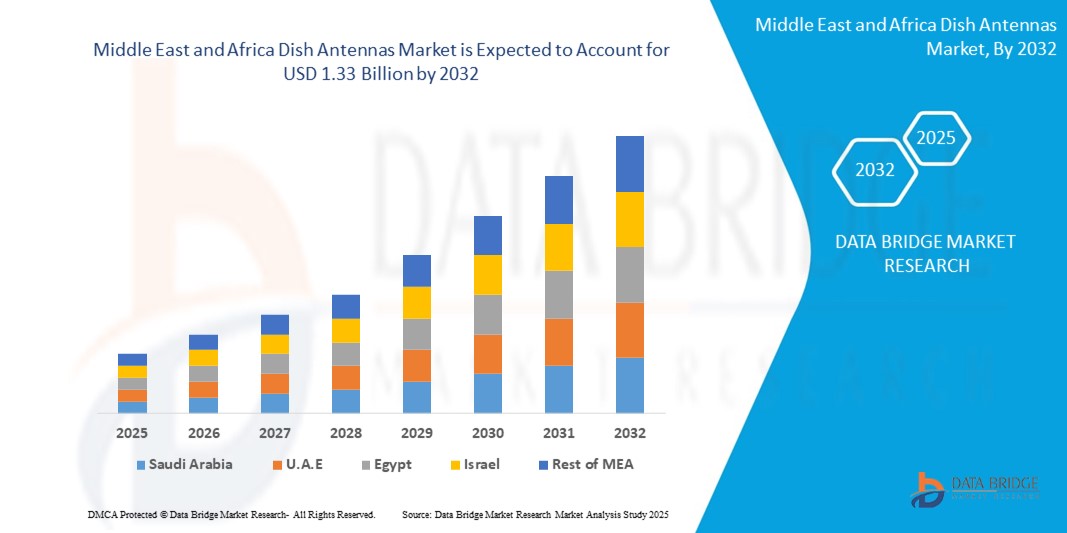

- The Middle East and Africa Dish Antennas Market size was valued at USD 0.80 billion in 2024 and is expected to reach USD 1.33 billion by 2032, at a CAGR of 6.54% during the forecast period

- This growth is primarily driven by the increasing penetration of high-speed internet and the proliferation of connected home ecosystems across the United States and Canada. The rise in over-the-air (OTA) content consumption and cord-cutting trends is leading to a renewed interest in advanced dish antennas capable of supporting HD and 4K transmissions. As consumers seek cost-effective alternatives to cable and satellite subscriptions, dish antennas are witnessing a significant resurgence in demand.

- Moreover, the growing integration of dish antennas with smart home technologies and IoT-based media systems is fostering their adoption in both residential and commercial sectors. Consumers are increasingly demanding compact, easy-to-install, and multifunctional antennas that not only receive signals but also integrate with smart TVs, home automation platforms, and voice assistants for enhanced user experience and control.

- Additionally, the expansion of 5G infrastructure and increased investments in broadcasting technology upgrades across Middle East and Africa are further reinforcing the role of modern dish antennas in supporting seamless communication and content delivery. The market is also benefiting from government initiatives focused on rural broadband access, which are enabling broader deployment of satellite-based and hybrid antenna solutions in underserved areas.

Dish Antennas Market Analysis

- Dish Antennas, which enable high-definition signal reception and integration with digital home entertainment and communication systems, are becoming increasingly essential in both residential and commercial environments across Middle East and Africa. Their ability to support over-the-air (OTA) broadcasts, satellite communications, and smart system connectivity positions them as key components in the evolution of connected homes and intelligent infrastructure.

- The rapid adoption of smart home technologies, such as voice-controlled systems, integrated home networks, and streaming services, is significantly driving the demand for advanced Dish Antennas in the region. Consumers are seeking versatile, cost-effective, and easy-to-install antenna solutions that enhance content accessibility while aligning with modern design and performance expectations.

- Furthermore, the market is witnessing robust growth due to increasing concerns over media access affordability, the trend of cord-cutting from traditional cable networks, and the desire for uninterrupted signal reception in both urban and rural areas. These preferences are propelling the transition towards next-generation digital antennas that support 4K, 5G, and hybrid broadcasting technologies.

- Saudi Arabia leads the Middle East and Africa Dish Antennas Market, accounting for the majority of the region’s 33.21% revenue share in 2024, driven by its rapid digital transformation, robust investments in satellite communication, and high demand across defense, residential, and media sectors.

- Reflector Antennas held the largest market share at 62.65% in 2024, primarily due to their wide usage in broadcasting, satellite communication, and defense applications.

Report Scope and Dish Antennas Market Segmentation

|

Attributes |

Dish Antennas Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Dish Antennas Market Trends

“Growing Need Due to Rising Security Concerns and Smart Home Adoption”

- The Middle East and Africa are experiencing rising urbanization and security concerns, particularly in high-density cities like Riyadh, Dubai, Johannesburg, and Lagos. This has prompted a surge in demand for advanced home and business surveillance systems.

- Dish antennas are increasingly integrated into smart security systems across MEA, serving as vital communication tools for satellite-linked surveillance cameras, intrusion detection systems, and emergency alert networks.

- In 2024, a growing percentage of new residential and commercial buildings in the Gulf region (especially in the UAE and Saudi Arabia) are being equipped with smart home technologies, many of which rely on dish antennas for satellite TV, broadband internet, and automated system connectivity.

- For instance, in April 2024, smart building projects in the UAE implemented IoT-based access controls with satellite communication modules—requiring reliable dish antenna integration.

- The growing popularity of DIY smart home solutions and voice-controlled ecosystems like Google Assistant (in multilingual Arabic support) and Amazon Alexa is driving demand for compact, easy-to-install dish antennas across the MEA region.

Dish Antennas Market Dynamics

Driver

“High Demand from Broadcasting and Satellite Communication Applications”

- MEA remains a strategic hub for satellite broadcasting and communication, driven by high television viewership rates and limited fiber infrastructure in rural and remote areas.

- Leading broadcasters and satellite providers like OSN, Nilesat, and Al Yah Satellite Communications (Yahsat) rely heavily on dish antennas for content delivery across the region.

- In 2024, more than 70% of households in key MEA countries like Egypt, Saudi Arabia, and Nigeria accessed media via satellite-based services, requiring reliable C-band and Ku-band dish antennas.

- Satellite-based internet services such as Starlink and YahClick have expanded their footprint across rural Africa and the Arabian Peninsula, leveraging dish antennas for broadband deployment in underserved regions.

- C-band dish antennas are increasingly favored for their weather-resilient connectivity—crucial in MEA's harsh desert and tropical climates where sandstorms and heavy rains can disrupt weaker signal bands..

Restraint/Challenge

“High Cost of Installation and Maintenance for Advanced Systems”

- In MEA, the high cost of advanced dish antennas remains a critical barrier, particularly in lower-income regions or among small businesses and public institutions.

- Multi-frequency and high-precision dish systems needed for satellite broadband, remote education, or public broadcasting require skilled technicians for installation, alignment, and maintenance—costing significantly more in regions with limited technical infrastructure.

- Infrastructure-related costs are also significant. For example, setting up satellite ground stations in remote areas of Africa or mountainous regions in North Africa requires expensive site development and logistics.

- In countries like Kenya or Ethiopia, commercial-grade Ka-band dish antenna installations can cost USD 25,000–100,000, which is prohibitive for rural schools, small telecom operators, or local government projects aiming for satellite connectivity..

Dish Antennas Market Scope

The Middle East and Africa Dish Antennas Market is segmented on the basis of antenna type, wireless network, component, frequency, antenna size, application, and end use.

- By Antenna Type

The market is segmented into reflector antennas, aperture antennas, and wire antennas. Reflector Antennas held the largest market share at 62.65% in 2024, primarily due to their wide usage in broadcasting, satellite communication, and defense applications. Their high directional gain and ability to focus signals efficiently make them the preferred choice for both terrestrial and space-based communications.

Aperture Antennas accounted for 21.80% of the market, favored for high-frequency and radar applications. Their compact size and efficient beamforming capabilities are ideal for airborne and shipborne systems, especially in defense and marine applications..

- By Wireless Network

The market is segmented into licensed and unlicensed networks. Licensed Wireless Networks dominated the segment with 67.27% market share in 2024, driven by extensive adoption across defense, aerospace, and broadcasting sectors. These networks offer interference-free communication, crucial for mission-critical operations and regulated spectrum usage.

Unlicensed Wireless Networks held 32.63%, supported by rising adoption in consumer applications like home satellite TV and local broadcasting. Their cost-efficiency and ease of deployment have led to increased usage in non-critical communication environments.

- By Component

The market is segmented into reflectors, feed horn, feed network, LNB converter, multiplexers, encoders, and others. Reflectors accounted for 43.58% of the component segment in 2024, driven by their pivotal role in shaping and directing signals in satellite TV dishes and deep-space antennas. Their dominance stems from widespread residential usage and institutional deployments (NASA, DoD).

Low Noise Block (LNB) Converters held 21.84%, essential for down-converting high-frequency satellite signals to lower frequencies for receiver compatibility. Their efficiency in improving signal clarity makes them integral to modern satellite communication.

- By Frequency

The market is segmented into X band, C band, L and S band, VHF/UHF band, K/Ka/Ku band, and others. C Band led the frequency segment with 36.89% share in 2024, owing to its superior performance in adverse weather and increasing demand for satellite TV and data services, especially across the U.S. and Canada.

K/Ka/Ku Band followed with 28.33%, driven by rising deployment in high-throughput satellite communications, offering higher data rates suitable for broadband, enterprise, and mobility applications.

- By Antenna Size

The market is segmented into small-sized dish, medium-sized dish, and large-sized dish. Large-Sized Dishes captured the largest share of 43.76% in 2024, particularly for space and ground station communications. Their capability to support long-range, high-capacity links is vital for space exploration, military, and scientific missions.

Medium-Sized Dishes held 34.02%, commonly used in commercial broadcasting and mobile communication hubs. Their balanced size-performance ratio supports scalable deployments in both urban and remote locations.

- By Application

The market is segmented into marine, land, space, and airborne. Land Applications dominated with 54.27% market share in 2024, primarily due to increasing deployment for television broadcasting, broadband, and navigation across urban and rural areas in Middle East and Africa.

Space Applications held 23.65%, fueled by growing investments in satellite launches and Earth observation missions. Agencies like NASA and private space firms are key contributors to this segment.

- By End Use

The market is segmented into aerospace and defense, media and entertainment, and industrial. Media and Entertainment remained the largest segment at 48.22% in 2024, driven by continued demand for satellite television, live broadcasts, and streaming services. Consumer preference for high-definition and uninterrupted content is bolstering this segment.

Aerospace and Defense accounted for 36.26%, driven by increasing investment in radar surveillance, secure communication systems, and military-grade satellite tracking across the U.S. and Canada.

Dish Antennas Market Regional Analysis

- Saudi Arabia leads the Middle East and Africa Dish Antennas Market, accounting for the majority of the region’s 33.21% revenue share in 2024, driven by its rapid digital transformation, robust investments in satellite communication, and high demand across defense, residential, and media sectors.

- In urban centers such as Riyadh, Jeddah, and Dammam, home automation and security solutions are becoming increasingly popular among affluent consumers. These smart systems—integrating satellite TV, broadband internet, and remote surveillance—depend on dish antennas for seamless connectivity and real-time signal reception.

- The widespread adoption of smart city initiatives under Saudi Vision 2030, along with strong governmental support for IoT and connected infrastructure, accelerates the demand for dish antennas capable of supporting smart energy meters, surveillance systems, and communication devices.

- Leading technology providers in the Gulf region are aligning their products with global smart ecosystems such as Amazon Alexa (with Arabic language integration), Google Assistant, and Apple HomeKit, which boosts the demand for dish antennas compatible with smart devices and home automation setups.

- Saudi Arabia’s defense and aerospace sectors, including agencies like the Saudi Space Commission, are prominent users of high-performance dish antennas for satellite tracking, border surveillance, and aerospace communication. These sectors invest heavily in large-diameter, precision-aligned antennas to support secure, real-time data transmission.

- Across rural and underserved regions of the MEA, particularly in Sub-Saharan Africa and North Africa, governments and private companies are investing in satellite internet infrastructure, such as YahClick (UAE), Avanti (UK/Africa), and Starlink, which depend on durable, weather-resilient dish antennas to deliver broadband services in areas lacking terrestrial infrastructure.

- In the broadcasting and telecommunications sector, countries like Egypt, Nigeria, and South Africa rely on dish antennas for media transmission, satellite uplink/downlink, and DTH (Direct-to-Home) services. Providers such as Nilesat, MultiChoice (DStv), and Eutelsat continue to expand their coverage using advanced dish antenna systems.

- Rising disposable incomes in Gulf nations, along with a growing middle class across Africa, further fuel market growth as consumers seek improved connectivity and access to high-definition entertainment and secure communication platforms supported by satellite technology.

Dish Antennas Market Share

The Dish Antennas industry is primarily led by well-established companies, including:

- MTI Wireless Edge Ltd.(Israel)

- Helander(United States)

- Airbus S.A.S.(France)

- Honeywell International Inc.(United States)

- Mitsubishi Electric Corporation (Japan)

- Global Invacom (Singapore)

- Infinite Electronics International, Inc.(United States)

- C-COM Satellite Systems Inc.(Canada)

- Radio Frequency Systems(Germany)

- Eyecom Telecommunications Group(United States)

- Cobham Limited(United Kingdom)

- L3Harris Technologies, Inc.(United States)

- CPI International(United States)

- Eravant (United States)

- mWAVE Industries LLC (A Subsidiary of Alaris Holdings)(United States)

- Ventev (United States)

- Challenger Communications(United States)

Latest Developments in Middle East and Africa Dish Antennas Market

- In April 2024, C-COM Satellite Systems Inc., a leading Canadian provider of mobile auto-deploying satellite antenna systems, announced the successful testing of its next-generation electronically steerable flat panel antenna in partnership with the University of Waterloo. This breakthrough technology aims to deliver high-speed satellite internet access in remote and mobile environments, significantly expanding market opportunities in sectors like emergency response, defense, and rural broadband across Middle East and Africa. The development highlights C-COM’s role in driving innovation in the evolving mobile satellite communications landscape.

- In March 2024, L3Harris Technologies, Inc., a major U.S.-based defense contractor, secured a multi-million-dollar contract with the U.S. Space Force for the supply of high-gain dish antennas used in deep space tracking and surveillance. This contract emphasizes the growing demand for advanced satellite communication technologies in the defense sector, reinforcing L3Harris’s leadership in high-performance antennas tailored for strategic military operations across Middle East and Africa.

- In February 2024, Global Invacom Group, a global provider of satellite communications equipment, expanded its U.S. operations with a new manufacturing facility in Texas. The facility is aimed at scaling up production of parabolic and flat panel antennas to meet increasing regional demand from telecom and media companies, especially in response to rising consumption of satellite-based video streaming and broadcasting services.

- In January 2024, Eravant, a California-based manufacturer of millimeter-wave components and subsystems, launched a new line of compact, high-frequency dish antennas for use in 5G and aerospace applications. These antennas are designed to support next-gen communication infrastructures, meeting the demands of data-intensive networks while enabling satellite uplinks with minimal interference—key for urban and airborne deployments.

- In December 2023, Challenger Communications, a U.S. supplier of satellite antennas and ground station solutions, announced the delivery of a large aperture satellite dish system to a government contractor for use in national defense telemetry and tracking systems. This development reflects increasing government investments in secure and reliable satellite ground systems, reinforcing Challenger’s presence in the high-specification defense and aerospace segments of the Middle East and Africa dish antennas market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Middle East And Africa Dish Antennas Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Middle East And Africa Dish Antennas Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Middle East And Africa Dish Antennas Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.