Middle East And Africa Genital Warts Market

Market Size in USD Million

USD

2,887.99 Million

USD

415.86 Million

2025

2033

USD

2,887.99 Million

USD

415.86 Million

2025

2033

| 2026 - 2033 | |

| USD 2,887.99 Million | |

| USD 415.86 Million | |

| % | |

|

Middle East and Africa Genital Warts Market Size

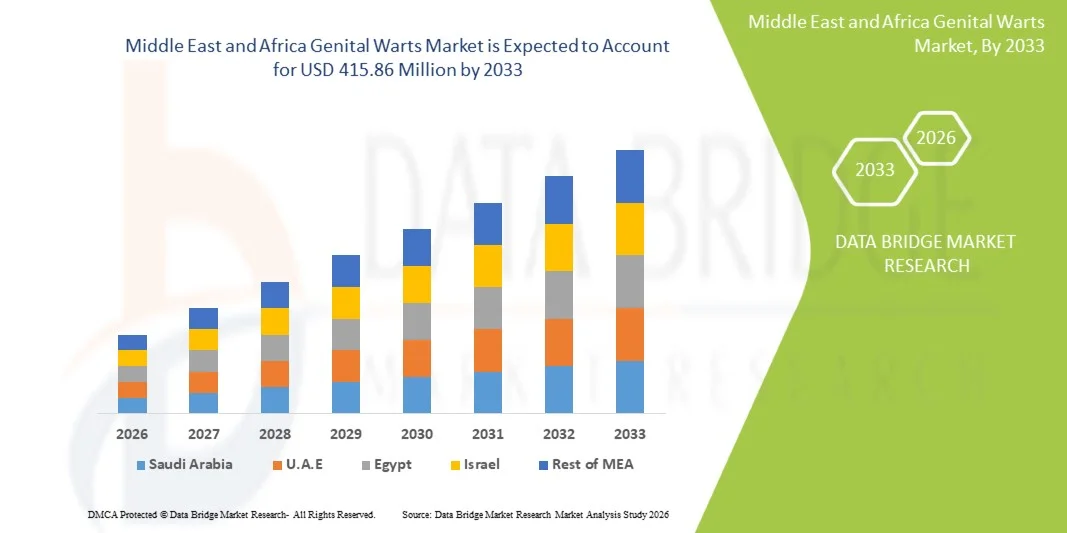

- The Middle East and Africa Genital Warts Market size was valued at USD 2887.99 Million in 2025 and is expected to reach USD 415.86 Million by 2033, at a CAGR of4.70% during the forecast period

- The market growth is largely fueled by the rising prevalence of human papillomavirus (HPV) infections worldwide, increasing awareness about sexually transmitted infections (STIs), and growing access to diagnostic and treatment services across both developed and emerging regions

- Furthermore, the expanding demand for effective, minimally invasive, and patient-friendly treatment options—such as topical therapies, cryotherapy, immunotherapy, and surgical removal—is accelerating the adoption of Genital Warts treatment solutions, thereby significantly boosting the industry's overall growth

Middle East and Africa Genital Warts Market Analysis

- The Middle East and Africa Genital Warts Market is primarily driven by the rising prevalence of HPV infections, increasing awareness about sexually transmitted diseases, and the growing accessibility of screening and treatment options across public and private healthcare systems in the U.S.

- The demand for genital warts treatments is further accelerated by the increasing adoption of topical therapies, cryotherapy, immunotherapy, laser treatment, and preventive vaccination programs, as well as the rising focus on early diagnosis and patient education initiatives

- Saudi Arabia dominated the Middle East and Africa Genital Warts Market with the largest revenue share of 42.5% in 2025, supported by advanced healthcare infrastructure, high awareness regarding STI prevention, strong HPV vaccination coverage, and widespread availability of effective treatment modalities. The Saudi market is fueled by robust screening programs, expanded HPV testing, and an increase in outpatient treatment procedures

- U.A.E. is expected to be the fastest-growing country in the Middle East and Africa Genital Warts Market during the forecast period, owing to rising investments in sexual health clinics, expanding vaccination initiatives, and increasing public health campaigns promoting HPV awareness and early treatment

- The Female segment dominated the market with a 53.4% share in 2025, driven by routine gynecological visits, higher screening rates, and targeted sexual health programs

Report Scope and Middle East and Africa Genital Warts Market Segmentation

|

Attributes |

Genital Warts Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Middle East and Africa Genital Warts Market Trends

“Rising Preference for Minimally Invasive & Patient-Friendly Treatment Approaches”

- A significant and rapidly expanding trend in the Middle East and Africa Genital Warts Market is the growing shift toward minimally invasive, patient-friendly, and non-surgical treatment options. This trend is driven by an increasing patient preference for therapies that reduce pain, recovery time, and procedural risks, especially in sensitive anatomical areas

- For instance, cryotherapy and topical immunotherapeutic agents such as imiquimod and podophyllotoxin continue gaining traction due to their non-invasive nature and suitability for outpatient or at-home use. Similarly, advancements in laser and electrosurgical devices are enabling clinicians to offer faster, more precise wart removal with reduced recurrence rates

- The integration of image-guided and precision-based dermatological tools is also supporting improved treatment outcomes. Some modern laser platforms now enable controlled tissue targeting, minimizing scarring and boosting patient confidence. Furthermore, the growing use of adjunct therapies that enhance immune response is strengthening long-term management effectiveness

- Increasing availability of home-based topical therapies, along with clinician-supervised combination treatments, is enabling customizable patient care. Through a single therapeutic plan, patients can combine topical, cryotherapy, and antiviral strategies for more comprehensive outcomes

- This shift toward flexible, minimally invasive, and cosmetically favorable treatment pathways is reshaping expectations for sexually transmitted infection (STI) management. As a result, pharmaceutical and dermatology device manufacturers are increasingly investing in improved formulations, advanced cryotherapy products, and safer laser solutions tailored for sensitive skin

- The demand for treatments that balance efficacy, comfort, privacy, and ease of use is growing rapidly across both male and female patient populations, reflecting an overall rise in awareness, early diagnosis, and proactive STI management

Middle East and Africa Genital Warts Market Dynamics

Driver

“Growing Global Prevalence, Rising Awareness, and Expanding Screening Programs”

- The increasing global burden of human papillomavirus (HPV) infections—especially HPV-6 and HPV-11, which cause over 90% of genital warts—remains a primary driver of the market. Rising sexually transmitted infection rates across both developed and developing regions continues to propel demand for effective treatment solutions

- For instance, in 2024, multiple national health agencies expanded HPV awareness and prevention campaigns, encouraging early diagnosis and timely treatment, thereby increasing patient inflow to clinics and hospitals

- As consumers become more aware of HPV transmission risks and available treatment options, demand for topical medications, cryotherapy, and surgical procedures continues to grow

- Furthermore, expanding sexual health screening programs, integration of HPV testing in routine gynecological and urological checkups, and increased accessibility of dermatology clinics are supporting market growth

- The availability of multiple therapeutic options—ranging from prescription topicals to advanced laser treatments—offers flexibility to patients and clinicians, further accelerating adoption. The growing acceptance of HPV vaccination is also indirectly supporting market growth through increased awareness and STI education among young adults

Restraint/Challenge

“High Recurrence Rates, Treatment Discomfort, and Social Stigma”

- One of the most significant restraints in the Middle East and Africa Genital Warts Market is the high recurrence rate associated with the condition, even after treatment. Since HPV can remain dormant, patients often experience repeated outbreaks, leading to increased treatment frequency and overall cost burden

- For instance, clinical reports in recent years indicate that recurrence rates for certain therapies can reach 25–65%, depending on the immune status of the patient and treatment type

- Social stigma associated with genital warts and other STIs also discourages many individuals from seeking timely care, resulting in delayed diagnosis and more severe disease progression

- Addressing these challenges through improved treatment protocols, better patient counseling, and development of long-acting therapeutics is crucial for broader adoption. Pharmaceutical companies are working to enhance topical formulations with improved skin absorption and reduced irritation, while clinicians emphasize patient education to reduce anxiety and embarrassment linked to STI treatment

- In addition, high procedure costs for laser and surgical interventions can be a barrier for patients in low-income regions. Ensuring affordability, improving accessibility, and reducing stigma through public health education will be vital for sustained market expansion

Middle East and Africa Genital Warts Market Scope

The market is segmented on the basis of morphology, type, cause, location, gender, dosage, end-user, and distribution channel.

• By Morphology

On the basis of morphology, the Middle East and Africa Genital Warts Market is segmented into Cauliflower-Like, Smooth Papular, Keratotic, and Flat Warts. The Cauliflower-Like warts segment dominated the largest market revenue share of 46.5% in 2025, owing to its higher prevalence, noticeable appearance, and the associated patient concern driving treatment demand. Clinicians often prioritize early intervention for this morphology due to its tendency to grow rapidly and cause discomfort or bleeding. Cauliflower-like lesions are widely reported across genital and perianal regions, which increases the frequency of outpatient consultations. The segment also benefits from well-established topical and procedural therapies, enhancing treatment uptake. Awareness campaigns and sexual health screenings further increase detection rates. Patients often seek medical attention quickly due to cosmetic and symptomatic impact, reinforcing market dominance. Public health initiatives and routine gynecological/urological examinations contribute to its high visibility. The segment’s prominence in clinical guidelines for HPV management ensures strong adoption in both preventive and therapeutic settings. Furthermore, healthcare providers’ familiarity with treatment protocols for cauliflower-like lesions facilitates consistent outcomes.

The Smooth Papular warts segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by rising early detection and increasing patient preference for minimally invasive management. Smooth papular lesions are often overlooked in early stages, but growing awareness among high-risk populations and expansion of sexual health checkups are improving diagnosis rates. Improved topical therapies suitable for sensitive areas are boosting adoption. Educational programs and awareness campaigns help patients recognize lesions sooner, increasing treatment uptake. The growing availability of combination treatments, including cryotherapy and immunomodulatory creams, supports market growth. Clinics are increasingly offering outpatient procedures, reducing recurrence and improving compliance. Enhanced screening in high-risk populations accelerates early treatment of smooth papular warts. Urban centers and sexual health clinics are witnessing higher patient flow. Pharmaceutical innovations focusing on shorter treatment duration further increase preference for smooth papular wart management.

• By Type

On the basis of type, the Middle East and Africa Genital Warts Market is segmented into Prevention, Diagnostics, and Treatment. The Treatment segment dominated the market with a 51.2% share in 2025, driven by the high global prevalence of HPV infections requiring active management. Increasing adoption of topical antivirals, cryotherapy, and laser-based interventions ensures treatment remains the primary revenue generator. Healthcare providers emphasize early intervention to prevent lesion growth and recurrence. Rising awareness about sexual health and the cosmetic impact of warts encourages patients to seek medical attention promptly. Expansion of dermatology and sexual health clinics facilitates easier access to treatments. Advanced formulations and improved procedural methods enhance efficacy, reinforcing treatment preference. Public health campaigns targeting STI management increase patient awareness and early care-seeking behavior. Government and private hospital programs also support treatment adoption through subsidized care initiatives.

The Prevention segment is projected to witness the fastest CAGR of 10.1% from 2026 to 2033, led by increasing HPV vaccination programs globally and rising awareness of prophylactic measures. School-based vaccination initiatives, targeted campaigns for adolescents, and government health schemes contribute to rapid growth. Preventive vaccines reduce wart incidence and recurrence, encouraging public health adoption. Patient awareness programs and sexual health campaigns strengthen demand. Accessibility improvements and insurance coverage expansion enhance uptake.

• By Cause

On the basis of cause, the market is segmented into HPV 6, HPV 11, and Others. The HPV 6 segment dominated the market with a 47.5% share in 2025, owing to its high prevalence in genital warts cases worldwide. HPV 6 is the most commonly reported strain, with well-documented clinical presentation and standardized treatment protocols. High infection rates across sexually active populations drive consistent demand for therapeutic interventions. Routine HPV screening in hospitals and diagnostic centers ensures early detection. Patient education programs and counseling sessions increase adherence to treatment regimens. HPV 6 infections are frequently targeted in awareness campaigns, reinforcing market visibility. Physicians and sexual health professionals are well-versed in its management, ensuring timely therapeutic intervention. Clinical guidelines emphasize management of HPV 6 due to its high recurrence potential. Public health initiatives promoting safe sexual practices support preventive measures. Insurance coverage for HPV-related treatments further boosts segment adoption. Increasing accessibility to topical and procedural treatments ensures steady market growth. The segment also benefits from ongoing research and pharmaceutical innovations focused on viral suppression and lesion removal.

The HPV 11 segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, driven by rising incidence among adolescents and young adults. Expansion of school-based and community vaccination programs targeting HPV 11 accelerates adoption. Early detection through routine sexual health checkups increases treatment-seeking behavior. Outpatient clinics are increasingly equipped to handle HPV 11 cases efficiently. Awareness campaigns improve recognition of lesions and reduce delay in care. Innovative topical and procedural treatments are gaining traction for HPV 11 management. Integration of HPV 11 testing in routine gynecological and urological exams supports growth. Targeted vaccination initiatives in high-risk populations enhance prevention. Research on long-term efficacy of vaccines promotes patient trust. Urban sexual health centers are expanding capacity to manage increasing cases. Government-supported HPV programs encourage early intervention. Accessibility of medications and topical therapies further supports CAGR growth.

• By Location

On the basis of location, the market is segmented into Vulva, Cervix Uteri, Urethra, Anus, and Scrotum. The Vulva segment dominated with a 44.8% share in 2025, due to high visibility and prevalence of lesions in this region among female patients. Routine gynecological examinations and early detection programs contribute to the segment’s dominance. Cosmetic concerns and symptomatic discomfort drive faster care-seeking behavior. Outpatient clinics provide standardized topical and procedural therapies. Patient compliance is higher due to easy access and less invasive treatment options. Education programs in sexual health encourage early consultation. Public awareness campaigns increase lesion identification and reporting. The segment benefits from established treatment protocols and physician familiarity. Specialized dermatology and sexual health departments enhance intervention efficiency. Clinical research supports optimized topical and minimally invasive interventions. Preventive counseling and HPV screening reinforce early management. Availability of insurance coverage for treatment improves access. Integration of screening with routine visits strengthens the segment’s prominence.

The Cervix Uteri segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, propelled by rising cervical screening programs, Pap smear tests, and early detection of high-risk HPV strains. Government-supported awareness campaigns enhance participation. Early intervention prevents lesion progression and reduces long-term complications. Hospitals and diagnostic centers are increasingly performing integrated HPV testing. Availability of minimally invasive therapies increases patient acceptance. Screening programs for high-risk populations support early treatment adoption. Outpatient gynecology clinics expand services to accommodate rising demand. Preventive vaccination initiatives targeting cervical HPV infections accelerate growth. Improved diagnostic accuracy through molecular testing supports early care. Patient education campaigns reinforce follow-up compliance. Technological advancements in cytology and imaging enhance detection rates. Research initiatives promote awareness of cervical lesion management.

• By Gender

On the basis of gender, the market is segmented into Male and Female. The Female segment dominated the market with a 53.4% share in 2025, driven by routine gynecological visits, higher screening rates, and targeted sexual health programs. Women are more likely to seek care due to cosmetic and symptomatic concerns. Public health awareness campaigns focus heavily on female sexual health. Early detection via Pap smears, colposcopy, and HPV testing ensures timely treatment. Outpatient clinics provide easy access to topical and procedural therapies. Insurance coverage for female sexual health enhances adoption. Educational programs in schools and universities promote prevention. Government initiatives encourage regular screening and early treatment. Clinical guidelines prioritize management of warts in women due to reproductive health implications. Research supports better therapeutic outcomes in female patients. Access to minimally invasive treatment options improves patient compliance. Awareness of HPV-related complications in females reinforces market dominance.

The Male segment is projected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by increasing awareness campaigns targeting men and expanding access to urological consultations. Rising incidence of anal and urethral warts accelerates demand. Outpatient dermatology and sexual health clinics for men are growing. Screening programs for high-risk populations improve early diagnosis. Educational programs increase recognition and prompt care-seeking. Novel topical therapies enhance treatment adherence. Research studies focusing on male sexual health expand awareness. Increased focus on prevention and vaccination supports growth. Accessibility of diagnostic services boosts patient confidence. Telemedicine consultations improve treatment follow-up. Hospitals are integrating male sexual health services into broader preventive care. Clinical guidelines now include male-specific wart management strategies.

• By Dosage

On the basis of dosage, the market is segmented into Cream, Gel, Ointment, Intramuscularly, and Others. The Cream segment dominated with a 48.2% share in 2025, due to ease of application, high patient compliance, and effectiveness in localized lesions. Creams provide convenient self-administration and quick symptom relief. They are widely available across retail pharmacies and clinics. Patient adherence is higher due to non-invasive nature and minimal side effects. Clinical guidelines recommend creams as first-line treatment for mild to moderate lesions. Physicians often prescribe cream formulations for outpatient management. Awareness campaigns encourage early treatment initiation. Creams are cost-effective compared to procedural interventions. Availability in multiple strengths enhances treatment flexibility. Training programs for healthcare providers improve application accuracy. Combination therapy with creams and procedural options enhances outcomes. Cream formulations are included in hospital formularies.

The Intramuscular segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by controlled antiviral therapies administered in hospital settings for severe or recurrent cases. Expansion of hospital-based sexual health clinics supports adoption. Intramuscular therapy ensures precise dosage for severe lesions. Specialist supervision improves safety and efficacy. Hospital formularies increasingly include intramuscular antivirals. Insurance coverage for inpatient therapies encourages utilization. Training programs ensure correct administration. Clinical trials support efficacy in severe HPV cases. Integration with outpatient follow-up programs strengthens patient compliance. Institutional procurement ensures availability. Research supports intramuscular route for rapid therapeutic response.

• By End-User

On the basis of end-users, the market is segmented into Hospitals, Diagnostic Centers, Surgical Centers, Ambulatory Surgical Centers, and Others. The Hospitals segment dominated with a 55.7% share in 2025, due to the availability of dermatology departments, outpatient care facilities, and procedural interventions such as cryotherapy and laser therapy. Hospitals provide comprehensive treatment options. They host specialized sexual health units. Availability of trained staff ensures effective care delivery. Hospital-based clinics integrate prevention, diagnosis, and treatment. Insurance coverage enhances patient access. Hospitals are central to large-scale vaccination initiatives. Educational programs run by hospitals increase awareness. Hospital formulary inclusion ensures drug availability. Specialized equipment facilitates advanced treatments. Public health collaborations enhance outreach. Multidisciplinary care improves treatment outcomes.

The Diagnostic Centers segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by increasing HPV screening and early detection services in specialized clinics. Rapid diagnostic tests improve detection efficiency. Outreach programs increase patient visits. Integration of molecular testing enhances accuracy. Preventive care initiatives promote early identification. Private diagnostic centers expand capacity to meet demand. Awareness campaigns direct patients to diagnostic services. Strategic collaborations with hospitals improve referrals. Adoption of telehealth diagnostics increases accessibility. Routine screening for high-risk populations supports growth. Advanced imaging and cytology techniques enhance early detection. Accreditation programs improve diagnostic quality.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Tender, Pharmacy Stores, and Others. The Pharmacy Stores segment dominated with a 52.3% share in 2025, due to widespread availability of topical and prescription medications across retail outlets. Easy accessibility drives patient preference. Retail pharmacies ensure consistent stock levels. Convenience and OTC availability improve compliance. Pharmacies are strategically located in urban and semi-urban areas. Trained pharmacists provide guidance on application. Strong supply chain networks ensure product availability. Affordability encourages continued use. Promotional campaigns support patient education. Pharmacy networks integrate with healthcare providers. Insurance acceptance boosts sales. Public health collaborations facilitate distribution.

The Direct Tender segment is expected to witness the fastest CAGR of 9.4% from 2026 to 2033, driven by hospital procurement programs, bulk supply agreements, and institutional purchasing for treatment initiatives. Centralized purchasing ensures cost efficiency. Government tenders for public hospitals increase adoption. Institutional agreements support large-scale treatment programs. Bulk procurement allows hospitals to stock high-demand medications. Contractual arrangements improve supply chain reliability. Inclusion in government health schemes promotes access. Procurement initiatives target preventive and therapeutic products. Hospitals benefit from predictable pricing and availability. Strategic collaborations with manufacturers accelerate deliveries. Tender-based procurement supports high-volume patient care.

Middle East and Africa Genital Warts Market Regional Analysis

- Middle East and Africa dominated the Middle East and Africa Genital Warts Market with the largest revenue share in 2025

- The growth is driven by advanced healthcare infrastructure, high awareness regarding sexually transmitted infections (STIs), strong HPV vaccination coverage, and widespread availability of effective treatment modalities

- The region is witnessing increased investments in sexual health programs, expanded screening and testing initiatives, and growing public health campaigns promoting early diagnosis and treatment

Saudi Arabia Middle East and Africa Genital Warts Market Insight

Saudi Arabia Middle East and Africa Genital Warts Market dominated the Middle East and Africa Genital Warts Market with the largest revenue share of 42.5% in 2025, supported by advanced healthcare infrastructure, high awareness regarding STI prevention, strong HPV vaccination coverage, and widespread availability of effective treatment modalities. The Saudi market is fueled by robust screening programs, expanded HPV testing, and an increase in outpatient treatment procedures, further strengthening patient access and treatment outcomes.

U.A.E. Middle East and Africa Genital Warts Market Insight

U.A.E. Middle East and Africa Genital Warts Market is expected to be the fastest-growing country in the Middle East and Africa Genital Warts Market during the forecast period, owing to rising investments in sexual health clinics, expanding vaccination initiatives, and increasing public health campaigns promoting HPV awareness and early treatment. Government-led initiatives to enhance STI screening, coupled with collaborations between healthcare providers and community programs, are expected to accelerate early diagnosis and improve treatment rates.

Middle East and Africa Genital Warts Market Share

The Genital Warts industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Johnson & Johnson (U.S.)

- Pfizer Inc. (U.S.)

- Sanofi S.A. (France)

- Roche Holding AG (Switzerland)

- Bharat Biotech International Ltd. (India)

- Serum Institute of India Pvt. Ltd. (India)

- Inovio Pharmaceuticals, Inc. (U.S.)

- Dynavax Technologies Corporation (U.S.)

- BioNTech SE (Germany)

- Moderna, Inc. (U.S.)

- VBI Vaccines Inc. (Canada)

- Zhejiang Tianyuan Bio-Pharmaceutical Co., Ltd. (China)

- LG Chem Life Sciences (South Korea)

Latest Developments in Middle East and Africa Genital Warts Market

- In July 2023, a network meta‑analysis published in Frontiers in Medicine demonstrated that intralesional immunotherapy (using Candida antigen, MMR antigens, or other immunogens) showed significant effectiveness for recalcitrant genital warts, suggesting it as a promising non‑surgical therapeutic option

- In September 2024, the European Association of Urology (EAU) updated its urological infection guidelines to reaffirm that imiquimod 5% cream (self-applied) remains a first-line treatment for anogenital warts, with proven clearance rates and acceptable safety

- In March 2025, a retrospective study published in the Journal of Clinical Medicine reported that three‑dose intramuscular HPV vaccination (Gardasil-9 or Gardasil-4), given to patients with recalcitrant genital warts in addition to standard therapy, resulted in 85% of patients showing complete or partial wart clearance after 12 months, versus 33% in controls

- In May 2025, a randomized controlled study (on non-genital, but immunotherapy-relevant warts) compared intralesional quadrivalent HPV vaccine vs Candida antigen, demonstrating the HPV vaccine to be effective in viral wart clearance; this supports potential off-label use in persistent wart cases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.