Middle East And Africa Hepatitis B Infection Market

Market Size in USD Billion

USD

1.55 Billion

USD

2.31 Billion

2024

2032

USD

1.55 Billion

USD

2.31 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.55 Billion | |

| USD 2.31 Billion | |

| % | |

|

Middle East and Africa Hepatitis B Infection Market Size

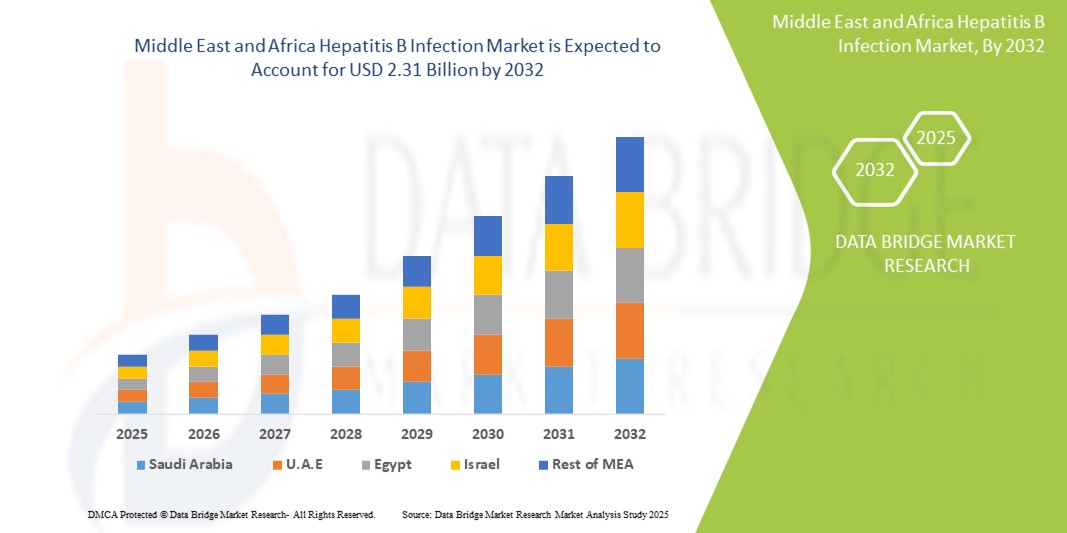

- The Middle East and Africa hepatitis B infection market size was valued at USD 1.55 billion in 2024 and is expected to reach USD 2.31 billion by 2032, at a CAGR of 5.20% during the forecast period

- The market growth is largely fueled by the growing adoption of advanced diagnostic technologies and therapeutic innovations for Hepatitis B, coupled with increasing digitalization and integration of electronic health systems across Europe

- Furthermore, rising consumer and public health demand for accurate, accessible, and preventive solutions is establishing Hepatitis B management protocols as a central focus of healthcare policy. These converging factors are accelerating the adoption of vaccination, screening, and antiviral therapies, thereby significantly boosting the Hepatitis B Infection market growth across the region

Middle East and Africa Hepatitis B Infection Market Analysis

- Hepatitis B treatments and diagnostics are increasingly vital components of the Middle East and Africa’s public health systems, especially across both hospital and community-based care settings, due to growing infection awareness, improved access to testing, and advancements in antiviral therapies

- The escalating demand for effective Hepatitis B management is primarily fueled by government-led vaccination programs, rising HBV-HDV co-infection screening, and the increasing burden of chronic liver diseases, particularly among aging and high-risk populations

- Saudi Arabia dominated the Middle East and Africa hepatitis B infection market with the largest revenue share of 34.7% in 2024, characterized by comprehensive national immunization programs, early adoption of advanced diagnostic tools, and wide-scale HBV screening initiatives. The country has experienced a steady increase in treatment uptake, particularly among at-risk populations, supported by strong awareness campaigns and accessible public healthcare services

- U.A.E. is expected to be the fastest growing region in the Middle East and Africa Hepatitis B Infection market, driven by widespread implementation of hepatitis screening in employment and visa processes, high vaccination coverage, and access to modern healthcare facilities. Continuous R&D efforts and the country’s thriving medical tourism sector also support innovation and growth in HBV management

- The chronic hepatitis B segment dominated the Middle East and Africa hepatitis B infection market with a market share of 62.4% in 2024, attributed to the persistent and long-term nature of the disease, requiring ongoing antiviral therapy and surveillance, along with enhanced detection rates due to expanded public health screening programs

Report Scope and Middle East and Africa Hepatitis B Infection Market Segmentation

|

Attributes |

Middle East and Africa Hepatitis B Infection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Middle East and Africa Hepatitis B Infection Market Trends

“Enhanced Convenience Through Integrated Care and Advanced Treatment Access”

- A significant and accelerating trend in the Middle East and Africa hepatitis B infection market is the growing integration of multidisciplinary care models and advanced treatment access through centralized healthcare systems. This trend is significantly improving patient outcomes and adherence by enabling seamless communication between general practitioners, hepatologists, and public health institutions

- For instance, several Western European countries have implemented national hepatitis action plans that allow patients to receive early diagnosis, antiviral treatment, and regular follow-up care under one coordinated framework. Germany’s integrated care model, for instance, enables efficient linkage from diagnosis to treatment, reducing disease progression rates

- Efforts such as centralized patient registries, digital health record systems, and streamlined referral pathways are optimizing hepatitis B infection management by enabling timely intervention and monitoring. These systems allow healthcare providers to track liver function, treatment response, and co-infections such as hepatitis D in real-time

- The integration of advanced diagnostics with routine primary care services facilitates early detection of both acute and chronic cases. This centralized approach, combined with affordable access to newer antiviral therapies, enhances both individual patient care and broader public health surveillance

- This trend toward more streamlined, coordinated, and technology-supported hepatitis B care is fundamentally reshaping expectations within national healthcare systems. As a result, many European governments are expanding access to viral hepatitis screening, particularly among vulnerable and high-risk populations such as migrants, intravenous drug users, and the elderly

- The demand for accessible, efficient, and integrated hepatitis B treatment models is rapidly growing across both public and private healthcare sectors, as stakeholders increasingly focus on long-term disease control and alignment with the World Health Organization’s 2030 hepatitis elimination goals

Middle East and Africa Hepatitis B Infection Market Dynamics

Driver

“Growing Need Due to Rising Disease Burden and Preventive Healthcare Adoption”

- The increasing prevalence of hepatitis B infections across Europe, along with heightened awareness about liver diseases, is significantly driving the demand for early diagnosis, vaccination, and treatment solutions

- For instance, in April 2024, GlaxoSmithKline plc (GSK) expanded its European hepatitis B vaccine supply through a strategic partnership with regional healthcare systems, aiming to improve immunization rates across high-risk populations. Such initiatives by key market players are expected to fuel growth in the Middle East and Africa Hepatitis B Infection market over the forecast period

- As public health authorities and consumers become more aware of the long-term complications associated with chronic hepatitis B—such as cirrhosis and liver cancer—the adoption of preventive strategies such as vaccination and early screening continues to rise

- Furthermore, the integration of hepatitis B testing into routine health check-ups and the growing popularity of point-of-care diagnostic technologies are making hepatitis B management more accessible and efficient across Europe

- The availability of effective vaccines, oral antiviral drugs, and the development of advanced immune modulators are enabling better disease control. Government funding, reimbursement policies, and WHO-led hepatitis elimination goals are also boosting adoption rates in both public and private healthcare settings

Restraint/Challenge

“Concerns Regarding Treatment Accessibility and High Cost of Advanced Therapies”

- Despite medical advancements, limited access to advanced antiviral therapies and immune modulators in certain parts of Middle East and Africa remains a challenge, particularly in Eastern and Southern Middle East and Africa where healthcare disparities persist

- For instance, studies published in early 2024 indicated that some EU member states still face shortages in hepatitis B vaccines and limited access to novel treatment regimens due to procurement and reimbursement issues

- Bridging this gap requires policy-level efforts to harmonize hepatitis B care standards across all European nations, particularly through EU-level funding support, price negotiations, and streamlined regulatory approvals

- Moreover, while first-line antiviral drugs are becoming more affordable, newer generation therapies with improved efficacy often come at a higher cost, potentially limiting their uptake among uninsured or low-income populations

- Public mistrust or vaccine hesitancy, especially in post-pandemic Europe, is another barrier that must be addressed through awareness campaigns and healthcare provider engagement

- Overcoming these challenges through expanded insurance coverage, public-private partnerships, and increased investment in regional healthcare infrastructure will be crucial to sustaining long-term growth in the Middle East and Africa Hepatitis B Infection market

Middle East and Africa Hepatitis B Infection Market Scope

The market is segmented on the basis of type, and treatment.

• By Type

On the basis of type, the Middle East and Africa hepatitis B infection market is segmented into chronic and acute. The chronic segment dominated the largest market revenue share of 62.4% in 2024, primarily due to the high prevalence of chronic HBV cases and the need for lifelong disease management through antiviral therapies and monitoring.

The acute segment is anticipated to witness the fastest growth rate with a CAGR of 6.4% from 2025 to 2032, fueled by enhanced early screening efforts, public health initiatives, and growing awareness leading to timely diagnosis and treatment.

• By Treatment

On the basis of treatment, the Middle East and Africa hepatitis B infection market is segmented into vaccine, antiviral drugs, immune modulator drugs, and surgery. The vaccine segment held the largest revenue share of 41.2% in 2024, supported by national vaccination drives, increased birth-dose immunization, and strong uptake among high-risk adult populations.

The antiviral drugs segment is projected to witness the fastest CAGR of 7.1% from 2025 to 2032, driven by the expanding chronic HBV patient pool, advancements in oral therapies, and favorable reimbursement policies.

Middle East and Africa Hepatitis B Infection Market Regional Analysis

- Middle East and Africa dominated the hepatitis B infection market with the largest revenue share of 33.27% in 2024, driven by strong public health infrastructure, high vaccination coverage, and increasing awareness about hepatitis B transmission and prevention

- The region is characterized by advanced diagnostic capabilities, well-established immunization programs, and active government-led hepatitis surveillance initiatives

- This widespread adoption of preventive and therapeutic measures is further supported by universal healthcare access, continuous R&D investments, and the growing focus on early screening and disease control, positioning Middle East and Africa as a key contributor to the global Hepatitis B Infection market

Saudi Arabia Hepatitis B Infection Market Insight

The Saudi Arabia hepatitis B infection market accounted for 34.7% of the Middle East and Africa Hepatitis B infection market revenue in 2024. The market benefits from strong public health infrastructure, mandatory vaccination for infants and healthcare workers, and comprehensive awareness programs. The government’s focus on early detection and treatment, along with digitized health tracking, supports robust market performance.

U.A.E. Hepatitis B Infection Market Insight

The U.A.E. hepatitis B infection market contributed 16.7% of the regional revenue share in 2024. Widespread implementation of hepatitis screening in employment and visa processes, high vaccination coverage, and access to modern healthcare facilities are driving market growth. Continuous R&D efforts and medical tourism also support innovation in HBV management.

South Africa Hepatitis B Infection Market Insight

The South Africa hepatitis B infection market held a 15.2% market share in 2024. Government-backed hepatitis B vaccination programs, integration of HBV care into HIV treatment platforms, and growing community-level education campaigns are accelerating diagnosis and treatment rates, especially in under-resourced regions.

Egypt Hepatitis B Infection Market Insight

The Egypt hepatitis B infection market represented 13.8% of the regional hepatitis B infection market in 2024. The country’s focus on infectious disease control, universal infant immunization, and public-private healthcare partnerships are key drivers. Increased screening in antenatal and rural health programs is boosting early detection.

Middle East and Africa Hepatitis B Infection Market Share

The Middle East and Africa Hepatitis B Infection industry is primarily led by well-established companies, including:

- Gilead Sciences, Inc. (U.S.)

- GSK plc (U.K.)

- Dynavax Technologies (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Arrowhead Pharmaceuticals Inc. (U.S.)

- Arbutus Biopharma (Canada)

- Teva Pharmaceuticals, Inc. (Israel)

- Zydus Pharmaceuticals (India)

- Aurobindo Pharma (India)

- Lupin Pharmaceuticals, Inc. (India)

Latest Developments in Middle East and Africa Hepatitis B Infection Market

- In September 2024, Gilead Sciences and Genesis Therapeutics announced a strategic collaboration to discover and develop novel small molecule therapies using Genesis’ GEMS AI platform. Gilead gained exclusive rights to develop and commercialize products from this partnership

- In July 2024, Gilead Sciences, Inc. presented research data, showcasing long-term efficacy and safety of Biktarvy in diverse HIV populations, including Hispanic/Latine individuals and older adults with comorbidities. Investigational once-daily and weekly dosing regimens were also highlighted

- In February 2024, GSK completed its acquisition of Aiolos Bio, including the promising AIO-001 monoclonal antibody for severe asthma. GSK paid USD 1000 million upfront and up to USD 400 million in milestone payments, expanding its respiratory biologics portfolio

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET

1.4 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 MULTIVARIATE MODELLING

2.7 THERAPEUTICS LIFELINE CURVE

2.8 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.9 DBMR MARKET POSITION GRID

2.1 VENDOR SHARE ANALYSIS

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHT

4.1 PESTAL ANALYSIS

4.2 PORTER FIVE FORCES

5 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: REGULATIONS

5.1 REGULATORY AUTHORITIES IN THE ASIA-PACIFIC REGION

5.2 NORTH AMERICA REGULATORY SCENARIO

5.3 EUROPE REGULATORY SCENARIO

5.4 MIDDLE EAST AND AFRICA REGULATORY SCENARIO

5.5 SOUTH AMERICA REGULATORY SCENARIO

6 PIPELINE ANALYSIS

7 EPIDEMILIOGY

8 MARKET OVERVIEW

8.1 DRIVERS

8.1.1 INCREASING PREVALENCE OF HEPATITIS B INFECTIONS

8.1.2 TECHNOLOGICAL ADVANCEMENTS IN DIAGNOSTICS

8.1.3 DEVELOPMENT OF COMBINATION THERAPIES FOR HEPATITIS B

8.1.4 STRATEGIC INITIATIVES BY COMPANIES FOR HEPATITIS B INFECTION

8.2 RESTRAINTS

8.2.1 SIDE EFFECTS AND DRUG RESISTANCE

8.2.2 INSUFFICIENT VACCINE COVERAGE FOR HEPATITIS B INFECTION

8.3 OPPORTUNITY

8.3.1 RISING NEW DRUG RELEASES AND INCREASING NEW DRUG PERMITS FOR HEPATITIS B

8.3.2 GOVERNMENT PROGRAMS TO RAISE AWARENESS OF HEPATITIS B INFECTION

8.3.3 ADVANCED RESEARCH AND DEVELOPMENT FOR CLINICAL TRIALS

8.4 CHALLENGES

8.4.1 THE COST OF HEPATITIS B TREATMENTS IS HIGH

8.4.2 STRINGENT REGULATORY POLICIES AND REGIONAL DISPARITIES IN TREATMENT ACCESS

9 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TYPE

9.1 OVERVIEW

9.2 CHRONIC

9.3 ACUTE

10 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TREATMENT

10.1 OVERVIEW

10.2 VACCINE

10.2.1 HOSPITAL PHARMACIES

10.2.2 DRUGS STORES AND RETAIL PHARMACIES

10.2.3 ONLINE PHARMACIES

10.3 ANTIVIRAL DRUGS

10.3.1 TENOFOVIR ALAFENAMIDE FUMARATE (TAF)

10.3.2 TENOFOVIR DISOPROXIL FUMARATE (TDF)

10.3.3 ENTECAVIR

10.3.4 OTHERS

10.4 IMMUNE MODULATOR DRUGS

10.4.1 PEGYLATED INTERFERON

10.4.2 INTERFERON ALPHA

10.5 SURGERY

11 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY REGION

11.1 MIDDLE EAST AND AFRICA

11.1.1 SOUTH AFRICA

11.1.2 SAUDI ARABIA

11.1.3 EGYPT

11.1.4 KUWAIT

11.1.5 QATAR

11.1.6 U.A.E

11.1.7 OMAN

11.1.8 BAHRAIN

11.1.9 REST OF MIDDLE EAST AND AFRICA

12 MIDDLE EAST AND AFRICA HEPATITIS B TREATMENT MARKET: COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: MIDDLE EAST AND AFRICA

13 SWOT ANALYSIS

14 COMPANY PROFILE

14.1 GILEAD SCIENCES, INC.

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 COMPANY SHARE ANALYSIS

14.1.4 PRODUCT PORTFOLIO

14.1.5 RECENT DEVELOPMENT

14.2 GLAXOSMITHKLINE PLC

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 COMPANY SHARE ANALYSIS

14.2.4 PRODUCT PORTFOLIO

14.2.5 RECENT DEVELOPMENT

14.3 DYNAVAX TECHNOLOGIES CORPORATION

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 COMPANY SHARE ANALYSIS

14.3.4 PRODUCT PORTFOLIO

14.3.5 RECENT DEVELOPMENTS

14.4 F. HOFFMAN-LA ROCHE LTD.

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 COMPANY SHARE ANALYSIS

14.4.4 PRODUCT PORTFOLIO

14.4.5 RECENT DEVELOPMENTS

14.5 BRISTOL-MYERS SQUIBB COMPANY

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 COMPANY SHARE ANALYSIS

14.5.4 PRODUCT PORTFOLIO

14.5.5 RECENT DEVELOPMENTS

14.6 ARROWHEAD PHARMACEUTICALS, INC.

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.4 RECENT DEVELOPMENTS

14.7 ARBUTUS BIOPHARMA

14.7.1 COMPANY SNAPSHOT

14.7.2 REVENUE ANALYSIS

14.7.3 PRODUCT PORTFOLIO

14.7.4 RECENT UPDATES

14.8 AUROBINDO PHARMA

14.8.1 COMPANY SNAPSHOT

14.8.2 REVENUE ANALYSIS

14.8.3 PRODUCT PORTFOLIO

14.8.4 RECENT UPDATES

14.9 LUPIN PHARMACEUTICALS, INC.

14.9.1 COMPANY SNAPSHOT

14.9.2 PRODUCT PORTFOLIO

14.9.3 RECENT UPDATES

14.1 MERCK & CO., INC.,

14.10.1 COMPANY SNAPSHOT

14.10.2 REVENUE ANALYSIS

14.10.3 PRODUCT PORTFOLIO

14.10.4 RECENT DEVELOPMENTS

14.11 NOVARTIS AG

14.11.1 COMPANY SNAPSHOT

14.11.2 REVENUE

14.11.3 PRODUCT PORTFOLIO

14.11.4 RECENT DEVELOPMENT

14.12 TEVA PHARMACEUTICAL INDUSTRIES

14.12.1 COMPANY SNAPSHOT

14.12.2 PRODUCT PORTFOLIO

14.12.3 RECENT DEVELOPMENTS

14.13 ZYDUS PHARMACEUTICALS, INC.

14.13.1 COMPANY SNAPSHOT

14.13.2 PRODUCT PORTFOLIO

14.13.3 REVENUE

14.13.4 RECENT DEVELOPMENT

15 QUESTIONNAIRE

16 RELATED REPORTS

List of Table

TABLE 1 MIDDLE EAST AND AFRICA CLINICAL TRIAL AND PIPELINE A-LYSIS AS PER THE COMPANY

TABLE 2 DISTRIBUTION OF PRODUCTS OR PROJECTS BY PHASE

TABLE 3 COUNTRY WISE EPIDEMIOLOGY FOR HEPATITIS B

TABLE 4 COST OF HEPATITIS B MEDICATIONS: BRAND VS. GENERIC PRICES

TABLE 5 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 6 MIDDLE EAST AND AFRICA CHRONIC IN HEPATITIS B INFECTION MARKET, BY REGION, 2022-2031 (USD MILLION)

TABLE 7 MIDDLE EAST AND AFRICA ACUTE IN HEPATITIS B INFECTION MARKET, BY REGION, 2022-2031 (USD MILLION)

TABLE 8 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 9 MIDDLE EAST AND AFRICA VACCINE IN HEPATITIS B INFECTION MARKET, BY REGION, 2022-2031 (USD MILLION)

TABLE 10 MIDDLE EAST AND AFRICA VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 11 MIDDLE EAST AND AFRICA ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY REGION, 2022-2031 (USD MILLION)

TABLE 12 MIDDLE EAST AND AFRICA ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 13 MIDDLE EAST AND AFRICA IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY REGION, 2022-2031 (USD MILLION)

TABLE 14 MIDDLE EAST AND AFRICA IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 15 MIDDLE EAST AND AFRICA SURGERY IN HEPATITIS B INFECTION MARKET, BY REGION, 2022-2031 (USD MILLION)

TABLE 16 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY COUNTRY, 2022-2031 (USD MILLION)

TABLE 17 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 18 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 19 MIDDLE EAST AND AFRICA ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 20 MIDDLE EAST AND AFRICA IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 21 MIDDLE EAST AND AFRICA VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 22 SOUTH AFRICA HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 23 SOUTH AFRICA HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 24 SOUTH AFRICA ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 25 SOUTH AFRICA IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 26 SOUTH AFRICA VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 27 SAUDI ARABIA HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 28 SAUDI ARABIA HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 29 SAUDI ARABIA ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 30 SAUDI ARABIA IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 31 SAUDI ARABIA VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 32 EGYPT HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 33 EGYPT HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 34 EGYPT ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 35 EGYPT IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 36 EGYPT VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 37 KUWAIT HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 38 KUWAIT HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 39 KUWAIT ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 40 KUWAIT IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 41 KUWAIT VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 42 QATAR HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 43 QATAR HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 44 QATAR ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 45 QATAR IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 46 QATAR VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 47 U.A.E HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 48 U.A.E HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 49 U.A.E ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 50 U.A.E IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 51 U.A.E VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 52 OMAN HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 53 OMAN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 54 OMAN ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 55 OMAN IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 56 OMAN VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 57 BAHRAIN HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

TABLE 58 BAHRAIN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 59 BAHRAIN ANTIVIRAL DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 60 BAHRAIN IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY TREATMENT, 2022-2031 (USD MILLION)

TABLE 61 BAHRAIN VACCINE, ANTIVIRAL DRUGS, IMMUNE MODULATOR DRUGS IN HEPATITIS B INFECTION MARKET, BY DISTRIBUTION CHANNEL, 2022-2031 (USD MILLION)

TABLE 62 REST OF MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TYPE, 2022-2031 (USD MILLION)

List of Figure

FIGURE 1 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: SEGMENTATION

FIGURE 2 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: DATA TRIANGULATION

FIGURE 3 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: DROC ANALYSIS

FIGURE 4 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: MIDDLE EAST AND AFRICA VS REGIONAL MARKET ANALYSIS

FIGURE 5 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: MULTIVARIATE MODELLING

FIGURE 7 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 8 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: DBMR MARKET POSITION GRID

FIGURE 9 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: VENDOR SHARE ANALYSIS

FIGURE 10 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: SEGMENTATION

FIGURE 11 TWO SEGMENTS COMPRISE THE MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, BY TYPE

FIGURE 12 EXECUTIVE SUMMARY

FIGURE 13 STRATEGIC DECISIONS

FIGURE 14 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET

FIGURE 15 CHRONIC SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET IN 2024 & 2031

FIGURE 16 DROC ANALYSIS

FIGURE 17 BURDEN OF HBV INFECTION IN THE GENERAL POPULATION BY WHO REGION, 2019

FIGURE 18 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: BY TYPE, 2023

FIGURE 19 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: BY TYPE, 2024-2031 (USD MILLION)

FIGURE 20 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: BY TYPE, CAGR (2024-2031)

FIGURE 21 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: BY TYPE, LIFELINE CURVE

FIGURE 22 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: BY TREATMENT, 2023

FIGURE 23 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: BY TREATMENT, 2024-2031 (USD MILLION)

FIGURE 24 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET: BY TREATMENT, CAGR (2024-2031)

FIGURE 25 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET BY TREATMENT, LIFELINE CURVE

FIGURE 26 MIDDLE EAST AND AFRICA HEPATITIS B INFECTION MARKET, SNAPSHOT

FIGURE 27 MIDDLE EAST AND AFRICA HEPATITIS B TREATMENT MARKET: COMPANY SHARE 2023 (%)

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.