Middle East And Africa Herpes Market

Market Size in USD Million

USD

34.35 Million

USD

51.92 Million

2025

2033

USD

34.35 Million

USD

51.92 Million

2025

2033

| 2026 - 2033 | |

| USD 34.35 Million | |

| USD 51.92 Million | |

| % | |

|

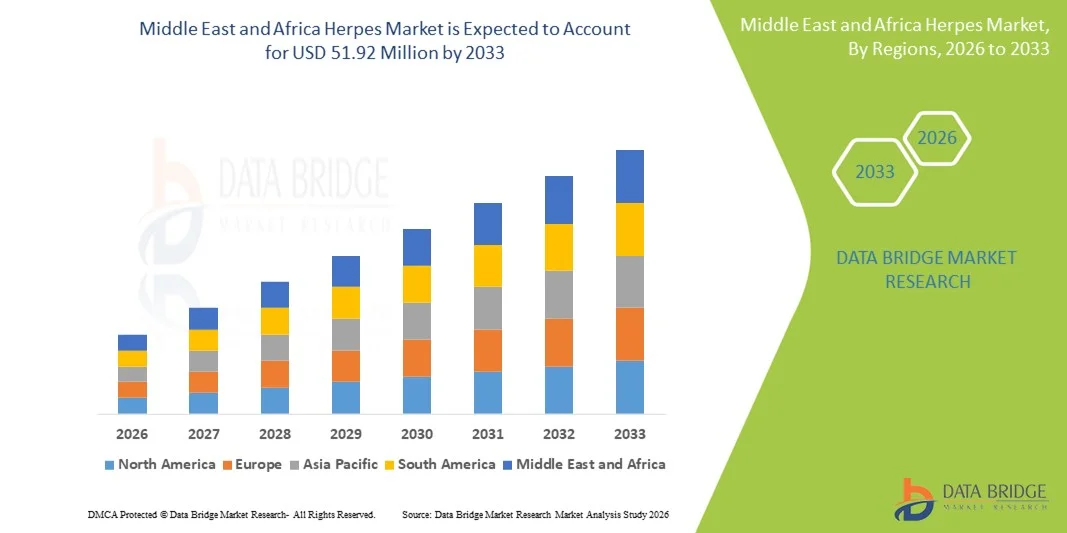

Middle East and Africa Herpes Market Size

- The Middle East and Africa herpes market size was valued at USD 34.35 million in 2025 and is expected to reach USD 51.92 million by 2033, at a CAGR of 5.3% during the forecast period

- The market growth is largely fueled by the rising prevalence of herpes infections across the region, increasing healthcare infrastructure investments, and greater adoption of antiviral therapies and advanced treatment options for both clinical and at-home management

- Furthermore, growing patient awareness, the expansion of hospital and pharmacy networks, and higher demand for effective prescription and over-the-counter treatments are establishing herpes care solutions as essential in regional infectious disease portfolios. These converging factors are accelerating the uptake of herpes therapeutic products, thereby significantly boosting the industry’s growth

Middle East and Africa Herpes Market Analysis

- Herpes treatments and diagnostics, including antiviral medications, topical therapies, and preventive care solutions, are increasingly vital components of infectious disease management in the Middle East and Africa across both hospital and outpatient settings due to the recurrent nature of herpes infections and the need for long-term symptom control and transmission reduction

- The escalating demand for herpes management is primarily fueled by the high prevalence of HSV-1 and HSV-2 infections, improving healthcare access, growing public awareness of sexually transmitted infections, and wider availability of antiviral therapies

- Saudi Arabia dominated the Middle East and Africa herpes market in 2025 with the largest revenue share 38.2%, characterized by relatively advanced healthcare infrastructure, higher healthcare spending, and strong access to branded antiviral medications, with the country experiencing steady growth in herpes diagnosis and treatment uptake driven by ongoing healthcare modernization programs

- South Africa is expected to be the fastest-growing country in the Middle East and Africa herpes market during the forecast period due to a large patient pool, expanding public healthcare programs, and increasing focus on the management of infectious and sexually transmitted diseases

- Acyclovir segment dominated the market with a market share of 34.9% in 2025, driven by its long-standing clinical use, cost-effectiveness, wide availability across hospital and retail pharmacies, and strong physician preference as a first-line antiviral therapy

Report Scope and Middle East and Africa Herpes Market Segmentation

|

Attributes |

Middle East and Africa Herpes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Herpes Market Trends

Advancing Antiviral Therapies and Awareness Initiatives

- A significant and accelerating trend in the Middle East and Africa herpes market is the improving access to antiviral therapies and expanding public health awareness programs focused on herpes simplex and herpes zoster infections. This combination is significantly enhancing early diagnosis and treatment uptake across patient groups

- For instance, widely used antivirals such as acyclovir, valacyclovir, and famciclovir are increasingly included in treatment protocols across hospitals and clinics, allowing patients to receive standardized and timely therapy. Similarly, topical formulations such as docosanol are gaining visibility for early-stage symptom management

- Advancements in herpes management enable approaches such as suppressive therapy to reduce recurrence frequency and lower transmission risk while supporting better long-term patient outcomes. For instance, healthcare providers are increasingly recommending continuous antiviral regimens for patients with frequent outbreaks and higher transmission concerns. Furthermore, patient education efforts offer individuals clearer guidance on symptom recognition and timely care seeking

- The growing integration of herpes management into broader sexual health and infectious disease programs facilitates more coordinated care delivery across healthcare systems. Through structured care pathways, patients can access diagnosis, counseling, and treatment in a more streamlined and confidential manner, creating a more supportive treatment environment

- This trend toward more proactive, informed, and accessible herpes care is gradually reshaping patient expectations for disease management. Consequently, pharmaceutical suppliers and healthcare providers are supporting improved antiviral availability, awareness materials, and counseling services to strengthen overall care delivery

- The demand for herpes treatments that offer reliable symptom control and recurrence reduction is growing steadily across both urban and semi-urban populations, as patients increasingly prioritize effective and accessible infectious disease management

- Increasing collaboration between public health agencies and private healthcare providers is strengthening outreach, screening, and early treatment efforts, contributing to more structured and accessible herpes management services

Middle East and Africa Herpes Market Dynamics

Driver

Growing Need Due to Rising Infection Burden and Treatment Awareness

- The increasing prevalence of herpes infections among adults and adolescents, coupled with gradually rising awareness about diagnosis and treatment options, is a significant driver for the heightened demand for herpes therapeutics

- For instance, in 2024, several Middle East and African healthcare systems expanded access to essential antiviral medications through hospital and retail pharmacy channels, aiming to strengthen infectious disease treatment availability. Such strategies by healthcare authorities are expected to support herpes treatment adoption in the forecast period

- As patients become more aware of symptoms and recurrence patterns, antiviral therapies offer benefits such as outbreak control, pain reduction, and lower transmission risk, providing a meaningful improvement over untreated infections

- Furthermore, the gradual strengthening of healthcare infrastructure and pharmaceutical distribution networks is making herpes treatments more accessible, supporting consistent drug availability across treatment centers and pharmacies

- The convenience of oral and topical antiviral options, physician-guided suppressive therapy, and improved counseling support are key factors propelling treatment adoption. The trend toward better sexual health education and reduced stigma further contributes to market growth

- Growing urbanization and healthcare investments in several MEA countries are improving access to clinical services, diagnostics, and pharmacy networks, indirectly supporting higher treatment uptake

- Support from international health organizations for infectious disease control programs is also encouraging better screening, reporting, and management of viral infections, including herpes

Restraint/Challenge

Limited Awareness and Social Stigma Hurdle

- Concerns surrounding limited public awareness and persistent social stigma associated with sexually transmitted infections pose a significant challenge to broader treatment uptake. As herpes remains underreported in many areas, patients may hesitate to seek timely medical care

- For instance, cultural sensitivities and misinformation about viral infections have made some individuals reluctant to pursue testing or professional consultation, slowing diagnosis and treatment rates

- Addressing these barriers through stronger awareness campaigns, confidential counseling, and patient education is crucial for improving treatment acceptance. Healthcare providers increasingly emphasize discreet services and accurate information to reassure patients. In addition, the recurring nature of herpes infections and the need for long-term therapy can create psychological and financial concerns for some patients

- While treatment access is improving, gaps in healthcare access and affordability can still hinder consistent therapy use, particularly in lower-resource settings or rural communities

- Overcoming these challenges through expanded education efforts, improved access to affordable antivirals, and supportive public health policies will be vital for sustained market growth

- Variability in healthcare infrastructure and diagnostic capacity across countries can lead to inconsistent detection and reporting, which limits timely intervention and treatment planning

- Concerns about long-term medication adherence and possible side effects may also reduce consistent therapy use among some patient groups, affecting overall treatment outcomes

Middle East and Africa Herpes Market Scope

The market is segmented on the basis of virus type, product, drug type, age group, route of administration, distribution channel, and end users.

- By Virus Type

On the basis of virus type, the herpes market is segmented into herpes simplex and herpes zoster. Herpes simplex segment dominated the market with the largest revenue share in 2025 due to the extremely high prevalence of HSV-1 and HSV-2 infections across MEA countries. The infection is lifelong and characterized by periodic recurrences, which creates continuous demand for antiviral drugs. A large sexually active adult population supports ongoing transmission rates. Growing awareness regarding genital and oral herpes is improving diagnosis levels. Physicians frequently prescribe suppressive and episodic antiviral therapies. The availability of cost-effective generic antivirals supports widespread treatment access. Public health STI programs are also increasing screening and counseling. All these factors collectively maintain segment dominance.

Herpes zoster segment is the fastest growing during forecast period due to the increasing incidence of shingles among aging populations. Life expectancy is improving in several MEA countries, expanding the elderly demographic. Older adults are more vulnerable to immune decline and viral reactivation. Complications such as postherpetic neuralgia encourage early treatment. Physicians are promoting faster antiviral initiation. Awareness regarding shingles symptoms is rising. Access to diagnostic care is gradually improving. These factors support faster segment expansion.

- By Product

On the basis of product, the market is segmented into acyclovir, docosanol, valacyclovir, famciclovir, and others. Acyclovir segment dominated the market in 2025 with a market share of 34.9% because it remains the most widely prescribed herpes antiviral. It has decades of proven clinical efficacy. The drug is significantly more affordable than newer options. Many public healthcare systems rely on acyclovir supply. It is available in oral, topical, and injectable forms. Generic manufacturing ensures high availability. Physicians are very familiar with its dosing. Retail and hospital pharmacies widely stock it. These factors sustain leadership.

Valacyclovir segment is the fastest growing during forecast period due to higher bioavailability and convenient dosing schedules. Fewer daily doses improve patient adherence. It is strongly recommended for suppressive therapy. Urban patients increasingly prefer advanced options. Physicians favor it for recurrent infections. Rising disposable income supports adoption. Increasing diagnosis rates boost prescriptions. Its strong clinical performance drives demand. Pharmaceutical companies are expanding distribution and marketing to capture growth in fast-growing markets

- By Drug Type

On the basis of drug type, the market is segmented into prescription drugs and over-the-counter drugs. Prescription drug segment dominated the market in 2025 since most herpes cases require physician supervision. Moderate and severe infections need monitored therapy. Clinical guidelines recommend prescription antivirals. Hospitals are primary dispensing points. Insurance systems often support prescriptions. Doctors supervise long-term suppressive use. Proper dosing requires medical guidance. Structured healthcare systems reinforce dominance.

Over-the-counter segment is the fastest growing during forecast period due to rising self-care awareness. Patients seek immediate symptom relief. Mild cases often rely on OTC creams. Retail pharmacies are expanding availability. Urban consumers prefer convenience. Marketing increases product visibility. Early-stage outbreaks often use OTC care. These factors drive faster growth. Marketing initiatives targeting preventive care and symptom management encourage adoption. Rising disposable incomes and e-pharmacy penetration support rapid segment growth

- By Age

On the basis of age, the market is segmented into adult and pediatrics. Adult segment dominated the market in 2025 because herpes prevalence is significantly higher among adults. Sexually active populations face greater exposure risks. Adults experience more frequent recurrences. Adults actively seek treatment. Stress and lifestyle triggers are common. Adults have stronger purchasing power. Workplace insurance aids affordability. Higher awareness supports treatment uptake. Ongoing R&D for adult-specific formulations strengthens market dominance.

Pediatrics segment is the fastest growing during forecast period due to improvements in child healthcare systems. Neonatal herpes awareness is increasing. Pediatric diagnosis capabilities are improving. Early treatment protocols are emphasized. Parental awareness is rising. Pediatric antiviral safety data is expanding. Child healthcare access is improving. These factors support growth. Increasing parental awareness of infection risks supports market growth. Collaboration with pediatric associations promotes safe and effective therapy use.

- By Route of Administration

On the basis of route of administration, the market is segmented into topical, oral, and parenteral. Oral segment dominated the market in 2025 because oral antivirals are the standard systemic therapy. They are easy to administer. Oral drugs support suppressive regimens. Physicians strongly prefer oral forms. They are widely available. Patients prefer pills over injections. Oral therapy balances cost and efficacy. Long-term management relies on oral drugs. Continuous R&D for bioavailability and taste-masked formulations reinforces dominance.

Topical segment is the fastest growing during forecast period due to demand for localized treatment. Topicals are used in early outbreaks. They are widely available OTC. Patients perceive fewer side effects. Easy application increases adoption. Pharmacies actively promote them. Mild cases often rely on topicals. Consumer preference supports growth. They are simple to apply. Pharmacies promote topical options. Mild cases rely on them. This drives faster growth. Consumer preference drives growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, drug stores, online pharmacies, and others. Hospital pharmacy segment dominated the market in 2025 because diagnosis commonly occurs in hospitals. Prescription antivirals are dispensed there. Severe cases rely on hospital supply. Public healthcare systems depend on hospitals. Doctors prefer hospital dispensing. Monitoring occurs in hospitals. Insurance processing is easier there. Trust in hospital supply is high.

Online pharmacy segment is the fastest growing during forecast period due to increasing digital adoption. Patients value privacy. The home delivery adds convenience. Internet usage is rising. E-pharmacy platforms are expanding. The discreet purchasing attracts users. Chronic patients prefer the refills online. Mobile health apps support the demand. E-pharmacy platforms are expanding. Discreet purchasing is appealing. Chronic patients prefer refills online. These factors accelerate growth.

- By End Users

On the basis of end users, the market is segmented into hospitals, specialty clinics, and others. Hospital segment dominated the market in 2025 due to strong diagnostic infrastructure. Hospitals manage complex cases. Severe infections are treated there. Specialists are available. Public funding supports hospitals. Advanced labs enable diagnosis. Patients trust hospital care. Referral systems favor hospitals. Government contracts and insurance coverage reinforce this segment’s market position.

Specialty clinics segment is the fastest growing during forecast period due to STI-focused services. Clinics offer confidential care. Counseling services are strong. Urban clinic numbers are increasing. Patients prefer privacy. Targeted therapies are available. Awareness programs refer patients. Flexible scheduling attracts users. They provide targeted counseling. Urban clinics are expanding. Patients prefer specialized care. This supports faster growth. Urban clinics are expanding. Patients prefer privacy.

Middle East and Africa Herpes Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa herpes market in 2025 with the largest revenue share 38.2%, characterized by relatively advanced healthcare infrastructure, higher healthcare spending, and strong access to branded antiviral medications

- Patients in the country increasingly value early diagnosis, reliable antiviral treatment, and physician-guided care for managing recurrent herpes infections and reducing transmission risk, leading to greater engagement with formal healthcare services

- This growing treatment adoption is further supported by higher healthcare spending, expanding pharmacy networks, and strengthening public health awareness programs, establishing antiviral therapies as a key solution for managing herpes infections across both hospital and outpatient settings

The Saudi Arabia Herpes Market Insight

The Saudi Arabia herpes market captured the largest revenue share of 38.2% in 2025, driven by the country’s well-established healthcare infrastructure, rising awareness of viral infections, and increased access to prescription antiviral therapies. Patients are prioritizing early diagnosis and effective treatment to manage recurrent infections and reduce transmission risk. The growing availability of antivirals such as acyclovir, valacyclovir, and famciclovir in both hospital and retail pharmacies is supporting adoption. Furthermore, public health campaigns and physician-led counseling are encouraging timely treatment. Urban population growth and high healthcare expenditure are facilitating wider market penetration. The country’s focus on healthcare modernization continues to drive sustained growth across hospital and outpatient settings.

South Africa Herpes Market Insight

The South Africa herpes market is poised to grow at the fastest CAGR during the forecast period, driven by a high prevalence of HSV-1 and HSV-2 infections, expanding public healthcare coverage, and increasing awareness of sexually transmitted infections. Patients are increasingly seeking professional consultation and antiviral therapy, supported by improved diagnostic facilities. The government’s initiatives to strengthen infectious disease management are enhancing access to care. Urbanization and better healthcare access are driving adoption of both hospital-based and specialty clinic treatments. In addition, rising patient awareness of treatment options and long-term management strategies is encouraging consistent therapy use. These factors collectively contribute to the rapid expansion of the South Africa herpes market.

Egypt Herpes Market Insight

The Egypt herpes market is expected to expand steadily due to rising incidence of both herpes simplex and herpes zoster infections, along with improving healthcare infrastructure in urban centers. Increasing public awareness campaigns on viral infections are encouraging timely diagnosis and treatment. Hospitals and specialty clinics are expanding access to antiviral therapies. The availability of affordable generic drugs such as acyclovir strengthens treatment adoption. Private pharmacies and emerging online pharmacy platforms are improving accessibility. In addition, growing urban populations and enhanced healthcare expenditure are supporting sustained market growth.

Nigeria Herpes Market Insight

The Nigeria herpes market is witnessing steady growth, fueled by increasing awareness of sexually transmitted infections, improving diagnostic capabilities, and broader availability of antiviral medications. Patients are prioritizing early treatment to reduce recurrence and transmission. Government programs targeting viral infections are strengthening healthcare access. Urban centers are seeing rising demand for hospital and pharmacy-based care. Retail and online pharmacy channels are helping improve accessibility for urban and semi-urban populations. Enhanced patient education on proper therapy adherence is also contributing to market expansion.

Middle East and Africa Herpes Market Share

The Middle East and Africa Herpes industry is primarily led by well-established companies, including:

- GSK plc (U.K.)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Limited (India)

- Emcure Pharmaceuticals Limited (India)

- Aurobindo Pharma Limited (India)

- Viatris (U.S.)

- Zydus Lifesciences Ltd. (India)

- Fresenius SE & Co. KGaA (Germany)

- AbbVie Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Gilead Sciences, Inc. (U.S.)

- CENTURION REMEDIES Pvt. Ltd. (India)

- Zeelab Laboratories Ltd. (India)

- Novartis AG (Switzerland)

- Merck & Co., Inc. (U.S.)

What are the Recent Developments in Middle East and Africa Herpes Market?

- In September 2025, a study conducted in the Aseer Region of Saudi Arabia found that despite high levels of awareness about the herpes zoster (shingles) vaccine among patients with diabetes, actual vaccine uptake remained low, highlighting a critical gap between knowledge and preventive action. The research showed that only a minority of participants had received the vaccine even though most believed it was safe and effective, underscoring a need for enhanced public health strategies

- In August 2025, research published on HSV seroprevalence dynamics emphasized the need for expanded surveillance and monitoring of genital herpes in the Middle East and North Africa, noting shifts in infection etiology and highlighting the requirement for better data to inform public health planning and resource allocation across countries in the region

- In December 2024, the World Health Organization updated its overview of herpes vaccine research and preferred product characteristics, outlining the global pipeline of HSV vaccine candidates (DNA, mRNA, protein subunits, and more). This WHO update sets the stage for future regional clinical trials and regulatory interest, potentially benefiting Middle East and Africa populations through harmonized vaccine development frameworks

- In December 2024, the World Health Organization (WHO) released updated global estimates stating that over 1 in 5 adults aged 15–49 are living with genital herpes infection worldwide, highlighting the major public health burden of HSV and the urgent need for improved prevention and treatment strategies. This report emphasized the high global prevalence of genital herpes, including significant impacts in regions such as Africa, and called for accelerated research into new therapeutic and preventive tools

- In September 2022, the Saudi Ministry of Health began offering the recombinant zoster vaccine (RZV) to adults aged ≥50 years, marking a key expansion of preventive services for herpes zoster (shingles) in the Kingdom. Despite low uptake, the initiative reflects a formal government effort to reduce the burden of herpes zoster among older adults and integrate herpes‑related vaccination into national immunization strategies

- https://www.sciencedirect.com/science/article/pii/S0163445325002361

- https://www.vax-before-travel.com/herpes-vaccine-availability-aspirational-2025-2024-12-25

- https://www.mdpi.com/2227-9032/13/19/2495

- https://www.who.int/news/item/11-12-2024-over-1-in-5-adults-worldwide-has-a-genital-herpes-infection-who

- https://pmc.ncbi.nlm.nih.gov/articles/PMC12419340/

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.