Middle East And Africa High Strength Steel Market

Market Size in USD Billion

USD

492.50 Billion

USD

967.02 Billion

2024

2032

USD

492.50 Billion

USD

967.02 Billion

2024

2032

| 2025 - 2032 | |

| USD 492.50 Billion | |

| USD 967.02 Billion | |

| % | |

|

High Strength Steel Market Size

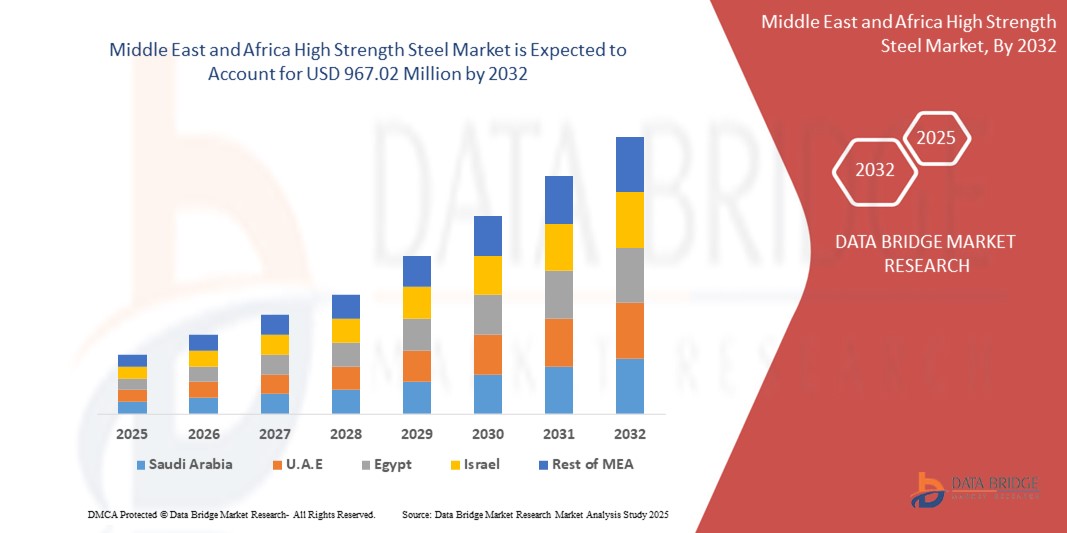

- The Middle East and Africa High Strength Steel market size was valued at USD 492.50 Million in 2024 and is expected to reach USD 967.02 Million by 2032, at a CAGR of 8.8% during the forecast period

- This growth is driven by factors such as the increasing infrastructure development, rising demand from the automotive and construction industries, and growing adoption of lightweight and fuel-efficient materials.

High Strength Steel Market Analysis

- High Strength Steels are crucial materials used in the automotive, construction, and heavy machinery industries due to their superior strength-to-weight ratio, durability, and resistance to wear and impact. These steels enable manufacturers to produce lighter, safer, and more fuel-efficient structures and vehicles.

- The demand for High Strength Steel is significantly driven by rapid urbanization, infrastructure development, and the growing focus on vehicle weight reduction to improve fuel efficiency and reduce carbon emissions.

- Saudi Arabia is expected to dominate the High Strength Steel market due to its large-scale infrastructure projects under the Vision 2030 initiative and strong investments in the automotive and construction sectors.

- U.A.E. is expected to be the fastest-growing region in the High Strength Steel market during the forecast period due to increasing construction activities, a booming logistics sector, and government focus on sustainable development.

- The automotive segment is expected to dominate the market with a significant market share due to stringent fuel efficiency regulations, rising vehicle production, and the growing adoption of advanced materials to improve crash performance and reduce vehicle weight.

Report Scope and High Strength Steel Market Segmentation

|

Attributes |

High Strength Steel Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

High Strength Steel Market Trends

“Growing Adoption of High Strength Steel in Automotive Lightweighting and Infrastructure Projects”

- One prominent trend in the Middle East and Africa High Strength Steel market is the rising adoption of high strength steel (HSS) in automotive lightweighting and large-scale infrastructure development projects.

- Automakers are increasingly using HSS to reduce vehicle weight while maintaining structural integrity and crashworthiness, helping to meet fuel efficiency and emission reduction targets.

- For instance, governments across the Gulf Cooperation Council (GCC) region are investing heavily in smart city initiatives and sustainable transportation, driving the demand for HSS in electric vehicles and public transit systems..

- These trends are reshaping the market landscape, accelerating the shift toward high-performance materials and reinforcing the strategic role of HSS in both industrial and urban development.

High Strength Steel Market Dynamics

Driver

“Growing Demand from Automotive and Construction Sectors”

- The increasing use of high strength steel (HSS) in automotive and construction applications is a key driver of market growth across the Middle East and Africa.

- In the automotive sector, manufacturers are increasingly turning to HSS for producing lightweight, fuel-efficient vehicles that meet stringent safety and emission standards.

- In the construction industry, HSS is widely used due to its excellent mechanical properties, durability, and resistance to deformation, enabling the development of more resilient infrastructure.

- As countries in the region invest heavily in urban development, smart cities, and transportation infrastructure, demand for strong, reliable materials like HSS is rising rapidly.

For instance,

- In 2023, Saudi Arabia launched construction on multiple giga-projects including NEOM and The Line, which heavily utilize advanced steel structures to meet modern architectural and environmental standards.

- As a result of the the growing demand from these sectors is significantly driving the adoption of High Strength Steel across the region.

Opportunity

“Expansion of Renewable Energy and Oil & Gas Infrastructure”

- The shift toward renewable energy and the expansion of oil & gas operations across the Middle East and Africa provide major growth opportunities for the HSS market.

- High strength steel is used extensively in wind turbine structures, transmission towers, and offshore oil rigs due to its superior strength-to-weight ratio and corrosion resistance.

- Government-backed renewable energy initiatives and infrastructure modernization programs are increasing the adoption of advanced steel grades in energy applications.

For instance,

- In March 2024, the UAE announced plans to invest over USD 54 billion in renewable energy projects by 2030, including wind farms and solar parks, which are expected to boost the demand for durable and high-performance materials like HSS.

- The infrastructure developments offer a growing opportunity for steel manufacturers to supply specialized grades tailored to energy sector requirements.

Restraint/Challenge

“High Production Costs and Limited Local Manufacturing”

- The high cost of producing High Strength Steel, especially advanced grades like dual-phase and transformation-induced plasticity (TRIP) steels, poses a significant challenge in the region.

- Limited local manufacturing capabilities in parts of the Middle East and Africa lead to dependency on imports, which increases overall costs due to tariffs, logistics, and lead times.

- Smaller construction firms and automotive suppliers may struggle to afford premium-grade HSS, which can restrict its widespread adoption.

For instance,

- According to the World Steel Association, in 2024, the Middle East and Africa imported over 60% of its specialty steel requirements, primarily from Europe and Asia, increasing costs by up to 25% compared to domestic procurement.

- Consequently, cost barrier can slow down infrastructure and industrial projects, creating disparities in access to high-performance materials and affecting overall market growth.

High Strength Steel Market Scope

The market is segmented on the basis Grade, product type, technology, magnification type, end user, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Grade |

|

|

By Product Type |

|

|

By End User |

|

In 2025, the High Strength Low alloy is projected to dominate the market with a largest share in Grade segment

The High Strength Low alloy segment is expected to dominate the High Strength Steel market with the largest share of 56.22% in 2025 owing to its excellent mechanical properties, cost-effectiveness, and wide application in structural and automotive components. Its superior strength-to-weight ratio, corrosion resistance, and formability make it a preferred choice for manufacturers seeking durable and efficient materials. Additionally, the region's increasing investments in construction and transportation infrastructure are fueling the demand for HSLA steels, contributing to its segmental dominance.

The Automotive is expected to account for the largest share during the forecast period in End User market

In 2025, the Automotive segment is expected to dominate the market with the largest market share of 51.31% driven by the growing focus on vehicle weight reduction, fuel efficiency, and safety standards. High strength steels are integral in manufacturing body-in-white structures, crash components, and chassis systems. The rising production of vehicles, alongside governmental initiatives to localize automotive manufacturing and comply with emissions regulations, is further bolstering the adoption of HSS in this sector, securing its dominance in the regional market.

High Strength Steel Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, Middle East and Africa presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, Grade dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- JSW (India)

- SAIL – Steel Authority of India Limited (India

- Nucor Corporation (U.S.)

- ArcelorMittal (Luxembourg

- SHAGANG GROUP Inc. (China

- China BaoWu Steel Group Corporation Limited (China)

- The Shougang Group (China)

- POSCO (South Korea)

- Voestalpine AG (Austria)

- SSAB-AG S.R.L. (Sweden)

- China Ansteel Group Corporation Limited (China)

- Baosteel Group Hu (China)

- Thyssenkrupp AG (Germany)

- Shandong Iron And Steel Group Co., Ltd. (China)

- Benxi Steel Group (China)

- JFE Steel Corporation (Japan)Ocular Instruments (U.S.)

Latest Developments in Middle East and Africa High Strength Steel Market

- In February 2025, Emirates Steel Arkan, one of the largest integrated steel producers in the UAE, announced the commissioning of a new production line dedicated to high strength low alloy (HSLA) steel grades. This move aims to meet the increasing demand from the automotive, energy, and infrastructure sectors across the region. The new facility is expected to boost annual production capacity by 250,000 metric tons and reduce lead times for regional clients.

- In December 2024, Saudi Iron and Steel Company (Hadeed) unveiled plans to invest over USD 800 million into modernizing its steel rolling mills in Jubail. The upgrade will focus on expanding capacity for advanced high strength steel (AHSS) used in electric vehicle (EV) manufacturing and green infrastructure projects, aligning with Saudi Arabia’s Vision 2030 industrial diversification goals.

- In October 2024, South Africa-based Safal Steel announced a strategic collaboration with European technology providers to enhance its metallurgical process for dual-phase high strength steel production. The partnership is expected to improve product consistency and support local demand in mining and automotive applications, making South Africa a regional hub for value-added steel.

- In September 2024, Egypt’s Ezz Steel initiated a feasibility study to establish a new cold rolling complex focused on high strength flat steel products. The facility aims to support growing construction and renewable energy projects in North Africa and the Eastern Mediterranean. The company also emphasized its commitment to decarbonization by integrating hydrogen-based DRI technology.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Middle East And Africa High Strength Steel Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Middle East And Africa High Strength Steel Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Middle East And Africa High Strength Steel Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.