Middle East And Africa Hunter Syndrome Treatment Market

Market Size in USD Million

USD

18.40 Million

USD

31.62 Million

2025

2033

USD

18.40 Million

USD

31.62 Million

2025

2033

| 2026 - 2033 | |

| USD 18.40 Million | |

| USD 31.62 Million | |

| % | |

|

Middle East and Africa Hunter Syndrome Treatment Market Size

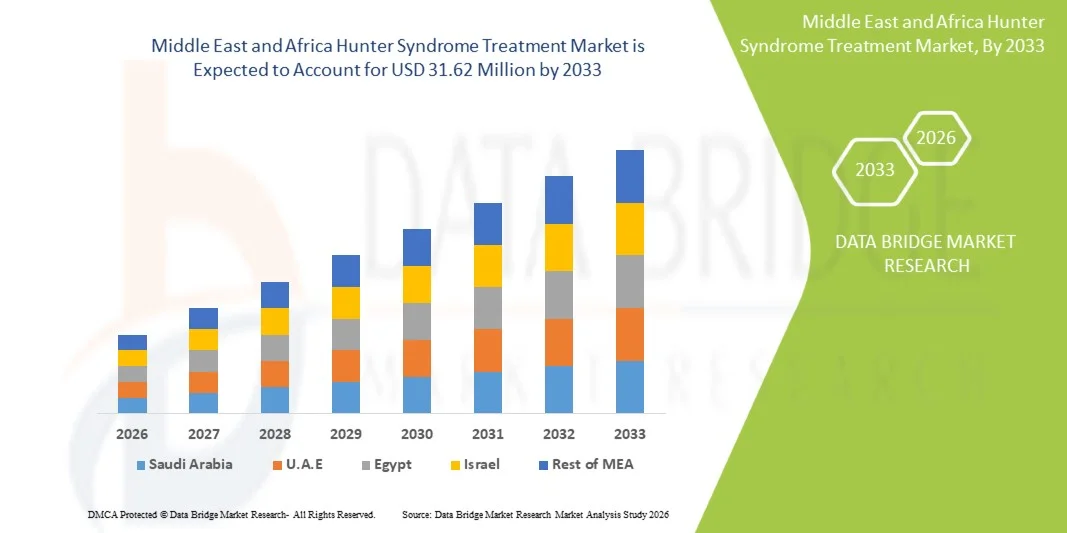

- The Middle East and Africa Hunter Syndrome treatment market size was valued at USD 18.40 million in 2025 and is expected to reach USD 31.62 million by 2033, at a CAGR of 7.0% during the forecast period

- The market growth is largely fueled by increasing government support, rising awareness about Hunter Syndrome, and growing adoption of enzyme replacement therapy (ERT) as the standard treatment in the region

- Furthermore, expanding healthcare infrastructure, rising newborn screening, and patient demand for early diagnosis and effective therapies are positioning Hunter Syndrome treatments as essential solutions for rare disease management. These converging factors are accelerating the uptake of therapies, thereby significantly boosting the industry's growth

Middle East and Africa Hunter Syndrome Treatment Market Analysis

- Hunter Syndrome treatments, including enzyme replacement therapy (ERT) and supportive care, are increasingly vital components of rare disease management in both pediatric and adult patients due to their ability to slow disease progression, improve quality of life, and manage complications associated with MPS II

- The escalating demand for Hunter Syndrome treatments is primarily fueled by growing awareness of the disease, increasing government support for rare diseases, and rising patient access to specialized healthcare facilities in the region

- Saudi Arabia dominated the MEA Hunter Syndrome treatment market with the largest revenue share of 37.2% in 2025, characterized by advanced healthcare infrastructure, strong government investment in orphan drugs, and early adoption of ERT in specialized hospitals

- South Africa is expected to be the fastest growing country in the MEA Hunter Syndrome treatment market during the forecast period due to increasing disease awareness, expansion of genetic testing, and improving access to rare disease therapies

- Enzyme Replacement Therapy (ERT) segment dominated the MEA Hunter Syndrome treatment market with a market share of 60.9% in 2025, driven by its status as the standard of care and its effectiveness in managing systemic and somatic manifestations of the disease

Report Scope and Middle East and Africa Hunter Syndrome Treatment Market Segmentation

|

Attributes |

Middle East and Africa Hunter Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Hunter Syndrome Treatment Market Trends

“Advancements in Enzyme Replacement Therapy (ERT) and Genetic Research”

- A significant and accelerating trend in the MEA Hunter Syndrome treatment market is the development and adoption of more effective ERT formulations and the exploration of gene therapy approaches, which aim to improve patient outcomes and reduce systemic complications

- For instance, idursulfase and next-generation ERT candidates are being increasingly administered in specialized hospitals across Saudi Arabia and UAE, offering improved tolerability and infusion protocols

- Genetic research integration enables earlier and more accurate diagnosis through newborn screening programs and advanced genetic testing, allowing timely treatment initiation and better long-term disease management

- The seamless collaboration of healthcare providers, government rare-disease programs, and biotech companies facilitates centralized patient management and access to specialized therapies in urban medical centers

- This trend towards more effective, patient-friendly, and personalized treatment approaches is fundamentally reshaping expectations for rare disease care, prompting companies such as Shire (Takeda) to develop improved ERT dosing regimens and infusion support programs

- The demand for advanced Hunter Syndrome treatments is growing rapidly across both pediatric and adult populations, as patients and caregivers increasingly prioritize early diagnosis, therapeutic efficacy, and comprehensive disease management

Middle East and Africa Hunter Syndrome Treatment Market Dynamics

Driver

“Increasing Awareness and Government Support for Rare Diseases”

- The growing recognition of Hunter Syndrome among healthcare providers and caregivers, coupled with rising government initiatives for rare disease treatment access, is a key driver of market growth

- For instance, in March 2025, Saudi Ministry of Health expanded its rare disease program to include Hunter Syndrome therapies, enabling subsidized treatment access at specialized centers

- As patient advocacy and awareness campaigns increase, more individuals are diagnosed early, generating higher demand for ERT and supportive care services

- Furthermore, expanding healthcare infrastructure, specialized hospital networks, and increasing availability of infusion centers are making Hunter Syndrome treatment more accessible in MEA countries

- The availability of subsidized treatment programs, improved insurance coverage, and patient support initiatives are key factors propelling the adoption of Hunter Syndrome therapies across both pediatric and adult populations

- Increasing participation of patient advocacy groups in Saudi Arabia, Egypt, and South Africa is raising awareness and facilitating faster treatment initiation

Restraint/Challenge

“High Treatment Costs and Limited Regional Accessibility”

- The high cost of Hunter Syndrome treatments, including ERT and emerging therapies, poses a significant barrier to broader market penetration in many MEA countries

- For instance, the annual cost of idursulfase therapy can reach tens of thousands of USD, limiting access for uninsured or underinsured patients in South Africa and other lower-income countries

- Limited local production and reliance on imported therapies increase logistical challenges and delays in treatment availability

- In addition, lack of widespread genetic screening and awareness in rural or underserved regions restricts early diagnosis and timely therapy initiation

- Overcoming these challenges through government subsidies, patient assistance programs, and expansion of specialized treatment centers will be vital for sustainable growth of the Hunter Syndrome treatment market in MEA

- For instance, delayed reimbursement approvals in Egypt and some Gulf countries have slowed patient access to new therapies, restricting market expansion

- Inadequate trained healthcare professionals for rare diseases in some MEA countries further limits effective treatment delivery and patient management

Middle East and Africa Hunter Syndrome Treatment Market Scope

The market is segmented on the basis of severity, type, complications, end user, and distribution channel.

- By Severity

On the basis of severity, the MEA Hunter Syndrome treatment market is segmented into mild to moderate and moderate to severe. The Moderate to Severe segment dominated the market in 2025, accounting for the largest revenue share. This is because patients with moderate to severe manifestations often require intensive care, frequent enzyme replacement therapy infusions, and ongoing management for complications such as respiratory and cardiovascular disorders. Hospitals and specialized clinics prioritize these patients due to their higher medical needs, leading to a larger market contribution. In addition, government and insurance programs typically focus support on severe cases, further boosting this segment’s market share. Awareness campaigns also emphasize the importance of early intervention in severe cases, creating higher adoption of treatment protocols in this subsegment.

The Mild to Moderate segment is expected to witness the fastest growth during the forecast period. Increasing awareness about early diagnosis, newborn screening programs, and proactive therapeutic interventions are driving adoption among mild to moderate patients. Families and caregivers are now seeking early enzyme replacement therapy to prevent disease progression and improve long-term quality of life. Growth is also supported by digital health initiatives and telemedicine programs in countries such as UAE and Saudi Arabia, which facilitate monitoring and management of less severe patients at home.

- By Type

On the basis of type, the MEA Hunter Syndrome treatment market is segmented into Enzyme Replacement Therapy (ERT), Stem Cell Transplant, Surgical Treatment, and Others. The Enzyme Replacement Therapy (ERT) segment dominated the market in 2025 with a market share of 60.9% due to its status as the standard of care for Hunter Syndrome. ERT is widely adopted across hospitals and specialized centers in Saudi Arabia, UAE, and South Africa for its proven ability to manage somatic symptoms and slow disease progression. High patient demand, government subsidies, and growing insurance coverage for ERT further drive the dominance of this segment. Pharmaceutical companies continue to invest in improving infusion protocols and developing next-generation ERTs, which enhances adoption rates. The convenience, reliability, and clinical effectiveness of ERT make it the preferred therapeutic option for physicians and caregivers asuch as.

The Stem Cell Transplant segment is anticipated to witness the fastest growth rate during the forecast period. Advances in hematopoietic stem cell transplantation and experimental gene-modified therapies are creating new treatment opportunities for patients who do not respond fully to ERT. Research collaborations between biotech firms and MEA hospitals are increasing availability of transplant programs, particularly in urban centers. Early success stories and clinical trials in GCC countries are raising confidence among caregivers and clinicians, encouraging broader uptake. In addition, growing investment in gene therapy pipelines is expected to drive future adoption in this segment.

- By Complications

On the basis of complications, the MEA Hunter Syndrome treatment market is segmented into respiratory disorders, neurological disorders, gastrointestinal disorders, cardiovascular, ophthalmic, audiologic, dental, musculoskeletal, and others. The Respiratory Disorders segment dominated the market in 2025, as respiratory complications are among the most common and life-threatening manifestations of Hunter Syndrome. Hospitals and specialized clinics allocate significant resources to managing respiratory distress, airway obstruction, and recurrent infections, which drives higher treatment costs and volume. Awareness programs emphasize respiratory monitoring and therapy, increasing treatment adoption. Respiratory care often requires multi-disciplinary management, including ERT and supportive care, contributing to a larger market share.

The Neurological Disorders segment is expected to witness the fastest growth in the forecast period. Expanding research on CNS-targeted therapies and growing recognition of cognitive and behavioral impairments in Hunter Syndrome patients are increasing treatment demand. Telemedicine and digital monitoring tools are being utilized to track neurological progression, particularly in UAE and Saudi Arabia. New therapeutic approaches aiming to address neurocognitive decline are in clinical trials, fostering optimism and driving adoption. Caregivers and hospitals are increasingly prioritizing early intervention in neurological complications to improve patient outcomes.

- By End User

On the basis of end user, the MEA Hunter Syndrome treatment market is segmented into hospitals, clinics, home healthcare, and others. The Hospitals segment dominated the market in 2025 due to the high concentration of specialized treatment facilities and infusion centers required for ERT administration. Hospitals in Saudi Arabia, UAE, and South Africa offer multi-disciplinary care teams, including pediatricians, geneticists, and respiratory specialists, which are essential for effective management of severe patients. In addition, hospitals often collaborate with pharmaceutical companies for patient support programs and therapy access, reinforcing their dominant position. Government and insurance reimbursement frameworks in MEA countries also favor hospital-based treatments.

The Home Healthcare segment is expected to witness the fastest growth during the forecast period. Increasing awareness of home infusion therapies, remote monitoring systems, and telemedicine support is enabling patients with mild to moderate disease severity to receive treatment at home. This reduces hospital visits, lowers healthcare costs, and improves patient convenience and adherence. Growth in this segment is further supported by digital patient tracking apps and caregiver training programs in UAE, Saudi Arabia, and Egypt. The trend towards patient-centered care is driving adoption in home healthcare settings.

- By Distribution Channel

On the basis of distribution channel, the MEA Hunter Syndrome treatment market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The Hospital Pharmacy segment dominated the market in 2025 due to the centralized distribution of ERT and other specialized therapies within hospital settings. Hospital pharmacies ensure proper storage, controlled dispensing, and professional administration of treatments, which is critical for rare disease management. Hospitals also provide associated monitoring services, increasing demand through their in-house pharmacies. Partnerships with pharma companies to deliver subsidized therapies further reinforce dominance.

The Online Pharmacy segment is expected to witness the fastest growth during the forecast period. Rising digital adoption, e-commerce platforms, and remote prescription fulfillment services are enabling patients in urban and semi-urban areas to access therapies conveniently. Online pharmacies reduce geographic barriers in MEA countries with sparse specialized treatment centers. Growth is also supported by increasing telemedicine consultations, which allow prescriptions to be delivered directly to patients’ homes. The convenience, efficiency, and growing regulatory acceptance of online pharmacy services are driving this segment’s rapid adoption.

Middle East and Africa Hunter Syndrome Treatment Market Regional Analysis

- Saudi Arabia dominated the MEA Hunter Syndrome treatment market with the largest revenue share of 37.2% in 2025, characterized by advanced healthcare infrastructure, strong government investment in orphan drugs, and early adoption of ERT in specialized hospitals

- Patients and caregivers in the region increasingly value early diagnosis, effective treatment protocols, and comprehensive care for managing systemic complications such as respiratory and cardiovascular disorders. This has led to higher adoption of ERT and associated therapies across major medical centers

- The widespread adoption is further supported by government subsidies, insurance coverage programs, growing awareness campaigns, and partnerships with pharmaceutical companies, establishing Saudi Arabia as the leading country for Hunter Syndrome treatment in MEA

The Saudi Arabia Hunter Syndrome Treatment Market Insight

The Saudi Arabia Hunter Syndrome treatment market captured the largest revenue share in the MEA region in 2025, fueled by government initiatives supporting rare disease management and the presence of specialized hospitals offering enzyme replacement therapy (ERT) and supportive care. Patients and caregivers increasingly prioritize early diagnosis, improved disease management, and accessibility to advanced therapies. The growing availability of genetic testing, newborn screening programs, and hospital-based infusion centers is driving adoption. In addition, government subsidies and insurance coverage programs are improving treatment accessibility. Saudi Arabia’s robust healthcare infrastructure, coupled with collaborations between pharmaceutical companies and hospitals, continues to support market expansion.

UAE Hunter Syndrome Treatment Market Insight

The UAE Hunter Syndrome treatment market is projected to expand at a substantial CAGR during the forecast period, primarily driven by investment in specialized rare disease centers and advanced healthcare infrastructure. The increase in awareness campaigns and patient support initiatives is fostering early diagnosis and therapy uptake. UAE patients benefit from integrated care programs, including telemedicine, home infusion services, and clinical monitoring, which enhance adherence and outcomes. Government-backed rare disease programs and partnerships with global biotech companies are stimulating growth. The adoption of innovative treatment approaches and ERT protocols is expanding across hospitals and clinics in the country.

South Africa Hunter Syndrome Treatment Market Insight

The South Africa Hunter Syndrome treatment market is gaining momentum due to growing awareness of rare diseases, improved diagnostic capabilities, and increasing hospital-based therapy access. Patients and caregivers are focusing on effective management of systemic complications, such as respiratory and cardiovascular disorders. The presence of specialized treatment centers, along with collaborations between hospitals and pharmaceutical providers, is driving adoption. South Africa’s expanding healthcare infrastructure and government support for orphan therapies are key factors promoting market growth. Early intervention programs and the rising number of infusion centers are improving treatment outcomes.

Egypt Hunter Syndrome Treatment Market Insight

The Egypt Hunter Syndrome treatment market is expected to grow at a considerable CAGR during the forecast period, fueled by rising awareness of rare diseases and expanding diagnostic services in urban hospitals and clinics. Government support and patient assistance programs are enhancing access to enzyme replacement therapy and supportive care. Hospitals are increasingly equipped to manage both moderate and severe cases, improving patient outcomes. Growth is further supported by collaborations between local healthcare providers and international pharmaceutical companies. Efforts to expand newborn screening and genetic testing are creating a more favorable environment for early treatment initiation.

Middle East and Africa Hunter Syndrome Treatment Market Share

The Middle East and Africa Hunter Syndrome Treatment industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company Limited (Japan)

- Denali Therapeutics (U.S.)

- REGENXBIO (U.S.)

- JCR Pharmaceuticals Co., Ltd. (Japan)

- GC Corp (South Korea)

- Generium JSC (Russia)

- ArmaGen Inc. (U.S.)

- Actigen Ltd (U.K.)

- Sangamo Therapeutics, Inc. (U.S.)

- BioMarin Pharmaceutical Inc. (U.S.)

- Ultragenyx Pharmaceutical Inc. (U.S.)

- Esteve Pharmaceuticals (Spain)

- Avrobio, Inc. (U.S.)

- Orchard Therapeutics plc (U.K.)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- Lysogene S.A. (France)

- Moderna, Inc. (U.S.)

- Amicus Therapeutics, Inc. (U.S.)

- Homology Medicines, Inc. (U.S.)

What are the Recent Developments in Middle East and Africa Hunter Syndrome Treatment Market?

- In August 2025, REGENXBIO Inc. announced that the FDA extended the review timeline of the BLA for RGX 121 (MPS II) from November 9, 2025 to February 8, 2026, following submission of longer term clinical data and inspections. Strengthens the such aslihood of nearterm approval of a new therapeutic option for Hunter syndrome, which could shift treatment paradigms globally including MEA

- In July 2025, the PureHealth group (UAE) and GEMMABio Therapeutics announced a strategic partnership to advance gene‑therapies in Abu Dhabi, backed by the Emirati Genome Programme (800,000+ genomes sequenced) and a push into rare disease innovation

- In May 2025, the U.S. Food & Drug Administration (FDA) accepted for Priority Review the Biologics Licence Application for RGX‑121 for MPS II (Hunter syndrome) and announced that a decision was expected imminently

- In June 2024, the Department of Health Abu Dhabi (DoH) and AstraZeneca signed a Memorandum of Understanding to establish a Rare Diseases Centre of Excellence in Abu Dhabi, with a focus on metabolic disorders (including MPS II) and comprehensive diagnosis/treatment programmes. This centre signals improved infrastructure for rare diseases in the Gulf region, such asly improving patient identification and treatment access for conditions such as Hunter syndrome

- In January 2024, a report noted that a “world first gene therapy trial for Hunter syndrome” had opened, exploring the first approach to cross the blood brain barrier for MPS II, signalling a new era for CNS targeted therapies. This represents a major step forward in treatment of Hunter syndrome which historically have been untreated by standard ERT

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.