Middle East And Africa Laboratory Filtration Market

Market Size in USD Million

USD

259.54 Million

USD

445.93 Million

2025

2033

USD

259.54 Million

USD

445.93 Million

2025

2033

| 2026 - 2033 | |

| USD 259.54 Million | |

| USD 445.93 Million | |

| % | |

|

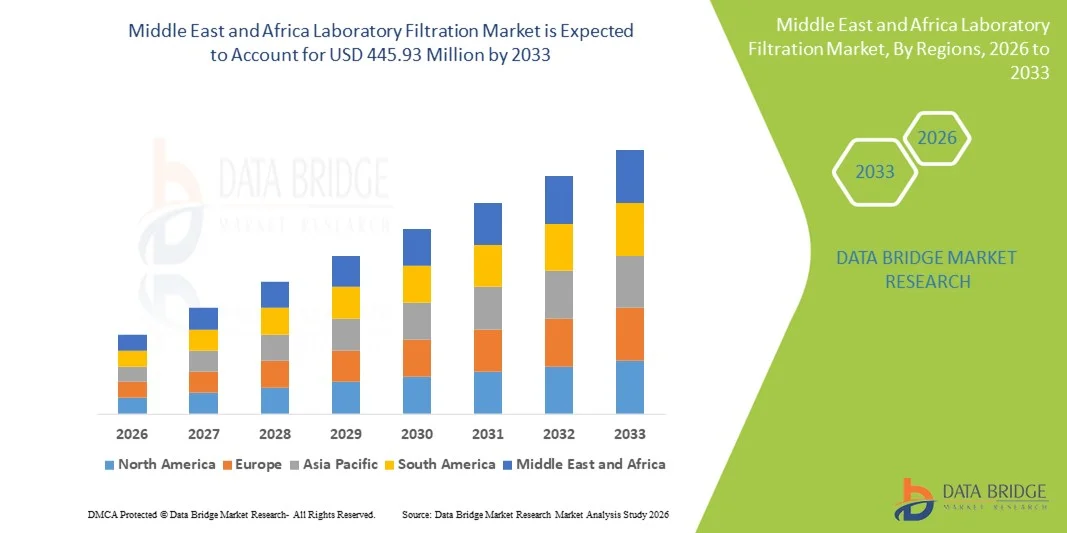

Middle East and Africa Laboratory Filtration Market Size

- The Middle East and Africa laboratory filtration market size was valued at USD 259.54 million in 2025 and is expected to reach USD 445.93 million by 2033, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced laboratory technologies, growing pharmaceutical and biotechnology sectors, and rising investment in research and development across the region

- Furthermore, escalating demand for high-quality filtration solutions in clinical, environmental, and industrial laboratories is driving the need for efficient, reliable, and cost-effective filtration systems. These converging factors are accelerating the uptake of laboratory filtration solutions, thereby significantly boosting the industry's growth

Middle East and Africa Laboratory Filtration Market Analysis

- Laboratory filtration solutions, providing critical separation, purification, and sterilization for liquids and gases, are increasingly essential components of modern laboratories in pharmaceutical, biotechnology, environmental, and industrial applications due to their precision, efficiency, and compliance with regulatory standards

- The rising demand for laboratory filtration is primarily driven by the growth of pharmaceutical and biotech industries, increasing R&D activities, and heightened focus on quality control and contamination prevention in clinical and industrial labs

- Saudi Arabia dominated the Middle East and Africa laboratory filtration market with the largest revenue share of 37.2% in 2025, characterized by strong healthcare infrastructure, growing investment in research facilities, and the presence of key industry players, with substantial adoption of advanced filtration systems in both government and private laboratories

- United Arab Emirates is expected to be the fastest-growing country in the laboratory filtration market during the forecast period due to expanding pharmaceutical manufacturing, rising healthcare expenditure, and increasing establishment of diagnostic and research laboratories

- Filtration Assembly segment dominated the Middle East and Africa laboratory filtration market by product with a market share of 42.9% in 2025, driven by its critical role in efficient and reliable separation processes across biotechnology, pharmaceutical, and diagnostic applications

Report Scope and Middle East and Africa Laboratory Filtration Market Segmentation

|

Attributes |

Middle East and Africa Laboratory Filtration Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle East and Africa Laboratory Filtration Market Trends

Advancement in Filtration Technologies and Automation

- A significant and accelerating trend in the Middle East and Africa laboratory filtration market is the growing adoption of advanced filtration technologies such as ultrafiltration, nano filtration, and reverse osmosis, combined with automated systems for higher efficiency and precision

- For instance, automated filtration systems in pharmaceutical labs in Saudi Arabia enable rapid processing of large sample volumes with minimal human intervention, improving consistency and throughput

- Integration of smart monitoring and control systems allows real-time tracking of filtration performance, ensuring higher reliability and reduced contamination risks. For instance, vacuum filtration units equipped with sensors can alert lab personnel when filter replacement is needed

- For instance, automated filtration systems in pharmaceutical labs in Saudi Arabia enable rapid processing of large sample volumes with minimal human intervention, improving consistency and throughput

- Such technological advancements facilitate centralized control over multiple filtration units, allowing laboratories to maintain uniform standards across processes and improve operational efficiency

- This trend towards automation and technologically advanced filtration systems is driving modernization of laboratory operations, leading companies such as Sartorius and Merck Millipore to introduce integrated systems with real-time monitoring and automated filtration cycle management

- The demand for automated and technologically advanced filtration solutions is rising across pharmaceutical, biotech, and diagnostic labs, as users increasingly prioritize efficiency, accuracy, and reproducibility

- Adoption of single-use and disposable filtration assemblies is increasing to reduce cross-contamination and cleaning requirements. For instance, many contract research organizations in UAE are switching to disposable membrane units for high-throughput screening

Middle East and Africa Laboratory Filtration Market Dynamics

Driver

Rising Demand from Pharmaceutical and Biotechnology Sectors

- The increasing growth of pharmaceutical and biotechnology industries in the Middle East and Africa is a significant driver for the rising demand for laboratory filtration solutions

- For instance, in March 2025, Saudi pharmaceutical companies invested in advanced filtration assemblies to scale up production of biologics and vaccines, supporting enhanced lab operations

- As laboratories expand their research and production capabilities, high-quality filtration systems for sterilization, purification, and separation become critical, boosting market adoption

- Furthermore, the rising focus on contamination control and quality assurance in pharmaceutical and food labs is reinforcing the need for reliable filtration solutions

- The convenience, reproducibility, and regulatory compliance provided by modern filtration systems are key factors propelling adoption in both research and industrial applications

- Increasing government funding and incentives for R&D infrastructure expansion are driving investments in advanced filtration systems. For instance, UAE government grants support biotech startups to acquire high-end membrane filtration units

- Collaboration between international filtration technology providers and local laboratories is enhancing technology transfer, accelerating adoption. For instance, Merck and local Saudi labs have partnered to implement state-of-the-art ultrafiltration systems

Restraint/Challenge

High Equipment Costs and Maintenance Requirements

- The relatively high initial cost of advanced laboratory filtration equipment, coupled with ongoing maintenance and consumable expenses, poses a significant challenge to widespread adoption

- For instance, ultrafiltration and reverse osmosis units in UAE research labs require regular membrane replacement and calibration, increasing operational expenditure. Smaller labs or budget-conscious institutions may hesitate to adopt high-end systems due to these financial constraints, limiting market penetration

- While reusable filtration systems can reduce long-term costs, initial investment and training requirements remain barriers, particularly in developing regions

- Addressing these challenges through cost-effective solutions, leasing options, and user training programs is crucial for wider adoption and sustained market growth

- Limited local technical expertise in some African countries can hinder installation, operation, and maintenance of sophisticated filtration systems. For instance, new labs in Nigeria face delays due to shortage of trained personnel for vacuum and nano filtration setups

- Regulatory compliance and certification requirements for certain filtration technologies can be complex and time-consuming, slowing adoption. For instance, some diagnostic centers in South Africa experience delays in deploying advanced ultrafiltration systems due to stringent FDA/ISO certifications

Middle East and Africa Laboratory Filtration Market Scope

The market is segmented on the basis of product, technology, utility, and end user.

- By Product

On the basis of products, the Middle East and Africa laboratory filtration market is segmented into filtration media, filtration assembly, and filtration accessories. The filtration assembly segment dominated the market with the largest market revenue share of 42.9% in 2025, driven by its critical role in supporting efficient and reliable separation processes across biotechnology, pharmaceutical, and diagnostic applications. Filtration assemblies combine media, housings, and other components into ready-to-use systems, reducing setup time and ensuring consistent performance. Laboratories prioritize assemblies for high-throughput operations, where reproducibility and contamination control are essential. Companies offering pre-configured assemblies with automation features and quality certifications gain preference among end users. The ease of integration with existing laboratory workflows and compatibility with multiple technologies further strengthens their adoption. In addition, the durability and ability to handle various sample types make filtration assemblies the preferred choice in research and production environments.

The filtration media segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing need for specialized membranes and filter materials tailored for specific applications such as ultrafiltration of proteins or microfiltration in diagnostic labs. Filtration media innovations, including high-flux membranes and chemically resistant materials, are driving adoption among pharmaceutical and biotechnology companies. The growing emphasis on product quality, purity, and regulatory compliance also propels the demand for advanced filtration media. Academic and research institutes increasingly seek customized membranes to support experimental workflows, contributing to market growth.

- By Technology

On the basis of technology, the market is segmented into microfiltration, ultrafiltration, vacuum filtration, nano filtration, and reverse osmosis. The ultrafiltration segment dominated the market in 2025, capturing the largest revenue share due to its widespread use in pharmaceutical production, biotechnology research, and diagnostic applications. Ultrafiltration systems are preferred for their ability to remove macromolecules, bacteria, and endotoxins efficiently, ensuring product safety and quality. The technology’s versatility in handling a range of molecular weights makes it suitable for diverse applications, from protein purification to water purification for lab use. Laboratories prioritize ultrafiltration for its reproducibility and compliance with strict regulatory standards. In addition, ultrafiltration systems are often integrated with automated setups, allowing high-throughput operations and minimal manual intervention, further enhancing their adoption.

The nano filtration segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing applications in pharmaceutical and food & beverage sectors, particularly for water treatment and concentration of bioactive compounds. Nano filtration membranes offer selective separation capabilities, energy efficiency, and the ability to retain beneficial molecules while removing contaminants. Rising environmental regulations and quality requirements are pushing laboratories to adopt nano filtration solutions. Contract research organizations and diagnostic centers are also leveraging nano filtration for high-purity sample preparation, contributing to strong growth prospects.

- By Utility

On the basis of utility, the market is segmented into disposable and reusable. The reusable segment dominated the market with the largest revenue share in 2025, owing to its cost-effectiveness over multiple cycles and suitability for high-volume laboratory operations. Reusable filtration systems are preferred in pharmaceutical and biotechnology companies for large-scale processes, where initial investment is offset by long-term usability. They offer consistent performance, support various filter types, and comply with stringent regulatory standards. Academic and research institutes often use reusable units for diverse experiments, reducing operational costs while maintaining efficiency. Their compatibility with automated systems and ease of maintenance further reinforce adoption.

The disposable segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by the growing demand for contamination-free workflows and the rising adoption in contract research organizations and diagnostic centers. Disposable filters reduce cleaning requirements, eliminate cross-contamination risks, and save time for high-throughput labs. Emerging biotech and pharmaceutical startups prefer disposable systems for flexibility and operational efficiency. In addition, the increasing emphasis on single-use technologies for regulatory compliance accelerates the adoption of disposable filtration solutions.

- By End User

On the basis of end users, the market is segmented into biotechnology companies, pharmaceutical companies, food and beverage companies, contract research organizations, academic and research institutes, and diagnostic centers. The pharmaceutical companies segment dominated the market in 2025, capturing the largest revenue share due to the extensive use of laboratory filtration for drug development, biologics production, and quality control testing. Pharmaceutical labs require high-performance filtration solutions to ensure product purity, comply with regulatory guidelines, and maintain consistency across production batches. Investments in R&D, expansion of production facilities, and adoption of automated filtration systems further strengthen the segment’s dominance.

The contract research organizations (CROs) segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing outsourcing of research and testing activities by pharmaceutical and biotech companies in the region. CROs demand advanced, high-throughput, and contamination-free filtration solutions to meet client requirements. Growing focus on biopharmaceutical research, diagnostic testing, and specialized contract services is propelling adoption. The flexibility, reliability, and compliance capabilities of modern filtration technologies make them highly suitable for CRO operations, supporting rapid market expansion.

Middle East and Africa Laboratory Filtration Market Regional Analysis

- Saudi Arabia dominated the Middle East and Africa laboratory filtration market with the largest revenue share of 37.2% in 2025, characterized by strong healthcare infrastructure, growing investment in research facilities, and the presence of key industry players, with substantial adoption of advanced filtration systems in both government and private laboratories

- Laboratories in the region prioritize high-performance filtration solutions to ensure product purity, compliance with regulatory standards, and efficient workflow management, particularly in pharmaceutical and biotech sectors

- This widespread adoption is further supported by government initiatives to strengthen healthcare and R&D infrastructure, rising awareness of quality control requirements, and the presence of key international and local filtration technology providers, establishing filtration systems as a preferred choice for both research and production applications

The Saudi Arabia Laboratory Filtration Market Insight

The Saudi Arabia laboratory filtration market captured the largest revenue share of 37.2% in 2025 within the Middle East and Africa, fueled by growing investments in pharmaceutical manufacturing, biotechnology research, and advanced diagnostic laboratories. Laboratories in the country are increasingly prioritizing high-performance filtration systems to ensure product purity, compliance with stringent regulatory standards, and efficient workflow management. The growing adoption of automated and integrated filtration solutions further supports market expansion. Moreover, government initiatives to strengthen healthcare and R&D infrastructure, coupled with the presence of leading international filtration technology providers, are significantly contributing to market growth.

United Arab Emirates Laboratory Filtration Market Insight

The United Arab Emirates laboratory filtration market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rapid development in pharmaceutical and biotechnology sectors and rising investments in research and diagnostic facilities. Increasing awareness of quality control standards, coupled with the adoption of advanced filtration technologies such as ultrafiltration and nano filtration, is fostering market adoption. UAE laboratories are also integrating filtration systems with automated monitoring and data management platforms, enhancing operational efficiency. Government support and incentives for R&D expansion further stimulate growth, with both new facilities and existing labs upgrading their filtration infrastructure.

Egypt Laboratory Filtration Market Insight

The Egypt laboratory filtration market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing investments in healthcare infrastructure and pharmaceutical manufacturing. Rising demand for reliable and high-quality filtration solutions in research and diagnostic labs is encouraging adoption. Egyptian laboratories are progressively adopting advanced filtration assemblies and membrane technologies to improve process efficiency and compliance. The presence of international filtration solution providers and growing collaborations with local institutions further support market expansion. Moreover, the country’s focus on improving laboratory standards and safety protocols is expected to propel demand for modern filtration systems.

South Africa Laboratory Filtration Market Insight

The South Africa laboratory filtration market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of laboratory quality standards and the demand for advanced, contamination-free filtration systems. Pharmaceutical companies, diagnostic centers, and research institutes in the country are adopting filtration solutions that enhance product quality and operational efficiency. The emphasis on regulatory compliance and adoption of modern laboratory practices is promoting growth. In addition, collaborations between global filtration technology providers and local laboratories are facilitating technology transfer and adoption of automated filtration systems.

Middle East and Africa Laboratory Filtration Market Share

The Middle East and Africa Laboratory Filtration industry is primarily led by well-established companies, including:

- Merck KGaA, (Germany)

- Sartorius AG (Germany)

- 3M (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher (U.S.)

- GVS S.p.A (Italy)

- Cole‑Parmer Instrument LLC (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Ahlstrom‑Munksjö (Finland)

- Abcam PLC (U.K.)

- Purolite Corp. (U.S.)

- Repligen Corp. (U.S.)

- Parker Hannifin Corporation (U.S.)

- Sterlitech Corp. (U.S.)

- Advantec MFS Inc. (U.S.)

- GE Healthcare (U.S.)

- Cobetter Filtration Equipment Co. (China)

- Graver Technologies LLC (U.S.)

- Meissner Filtration Products (U.S.)

- Porvair Filtration Group (U.K.)

What are the Recent Developments in Middle East and Africa Laboratory Filtration Market?

- In November 2025, Toray Membrane Middle East LLC (TMME) inaugurated a new facility in Dammam, Saudi Arabia the first in the country to integrate full-cycle reverse osmosis (RO) membrane fabrication through to assembly

- In July 2025, Toray Membrane Middle East began pilot operations of a major reverse osmosis (RO) membrane desalination facility a development that highlights continuing growth in membrane filtration infrastructure in the region, which may indirectly support demand in labs needing high‑quality water and purification systems

- In July 2025, the same company supplied RO membranes to the new seawater desalination plant Shuaibah 3 IWP seawater desalination plant in Saudi Arabia, intended to deliver 600,000 m³/day of potable water underlining increasing adoption of high-performance membrane filtration solutions in the region

- In March 2024, Sartorius AG expanded its technical support centre in Riyadh, Saudi Arabia — aimed at providing enhanced on‑site assistance and consultation services to pharmaceutical manufacturers in the Gulf region, thereby helping integrate filtration systems into local production facilities

- In December 2023, Pall Corporation expanded its regional capabilities by announcing that its MEA subsidiary Pall Arabia upgraded its facility in Saudi Arabia to include filter coalescer manufacturing enhancing its capability to produce separation and purification solutions locally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.